Oil prices steady near 1-mth high on US-Iran sanctions; OPEC+ meeting awaited

Introduction & Market Context

Five Star Bancorp (NASDAQ:FSBC) released its Q1 2025 investor presentation on April 29, highlighting the company’s 25th anniversary and financial performance. The bank reported earnings per share of $0.62, exceeding analyst expectations of $0.58, while revenue came in at $33.44 million, below the forecasted $35.22 million. Following the earnings release, FSBC shares rose 2.44% to $27.70, reflecting positive investor sentiment despite the revenue miss.

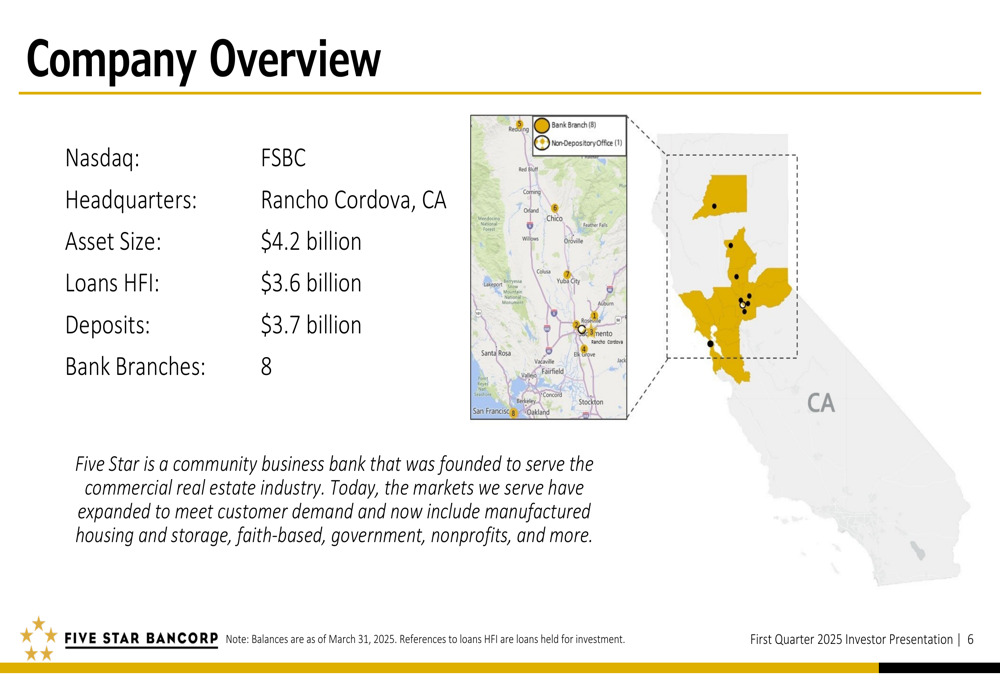

The California-based community business bank, which initially focused on serving the commercial real estate industry, has expanded its portfolio to include manufactured housing, storage, faith-based organizations, government, and nonprofits. With eight branches and assets of $4.2 billion, Five Star continues to demonstrate consistent growth in a competitive banking environment.

As shown in the following overview of the company’s key metrics:

Quarterly Performance Highlights

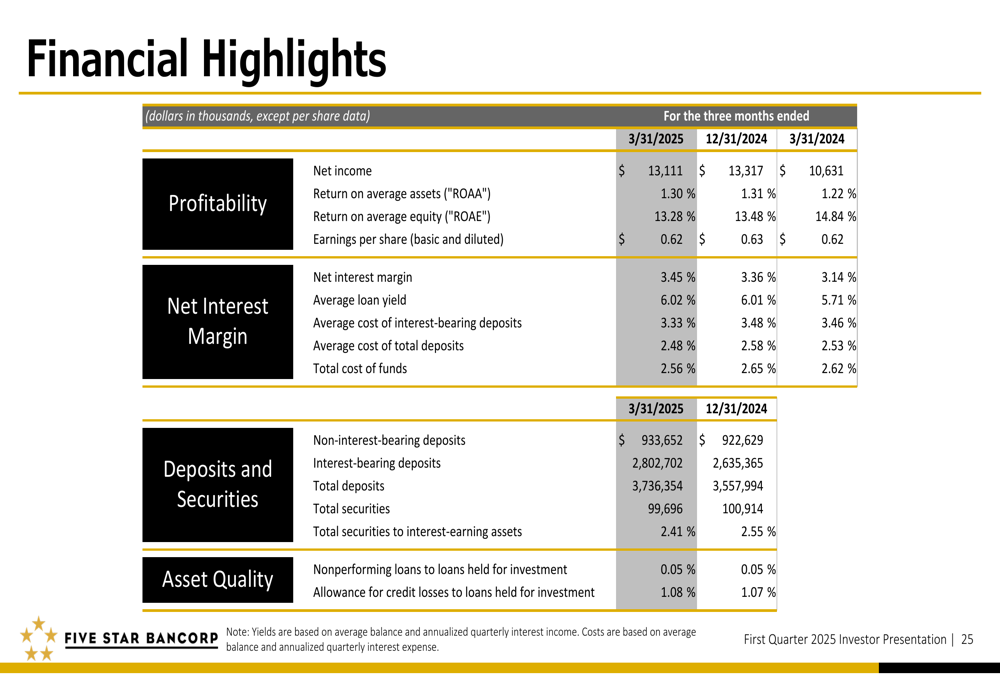

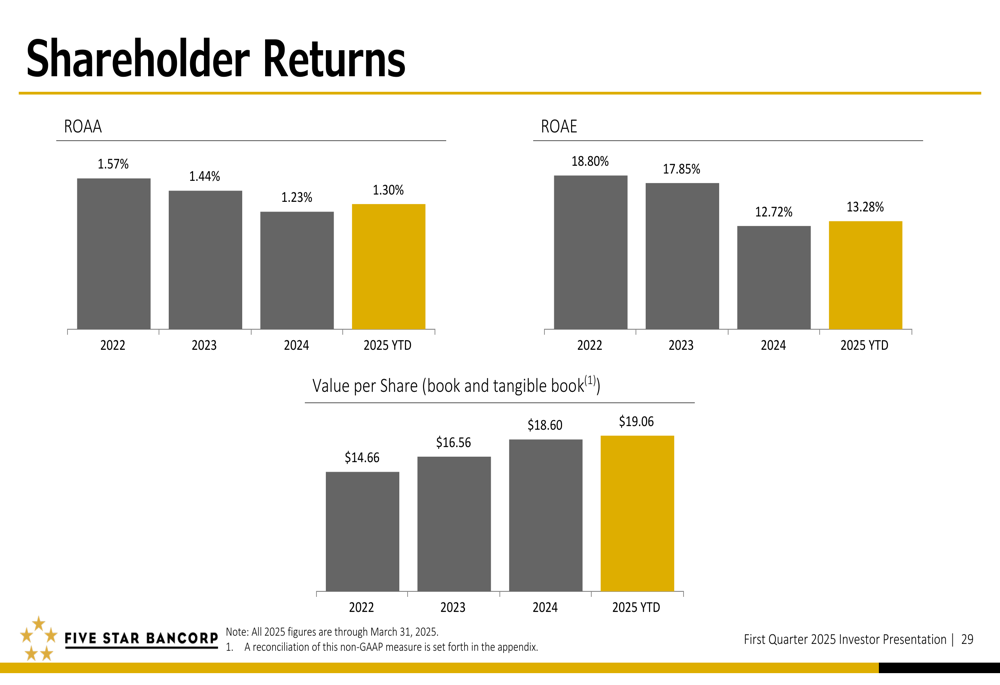

Five Star Bancorp reported net income of $13.1 million for Q1 2025, slightly down from $13.3 million in Q4 2024 but up from $10.6 million in Q1 2024. The company achieved a return on average assets of 1.30% and return on average equity of 13.28%, demonstrating solid profitability metrics despite challenging market conditions.

The bank’s net interest margin improved to 3.45% in Q1 2025 from 3.36% in Q4 2024, driven by an increase in average loan yield to 6.02% and a decrease in the average cost of total deposits to 2.48%. This margin expansion contributed to the earnings beat and reflects the bank’s effective balance sheet management in a competitive rate environment.

The following table details the company’s financial highlights for Q1 2025 compared to previous quarters:

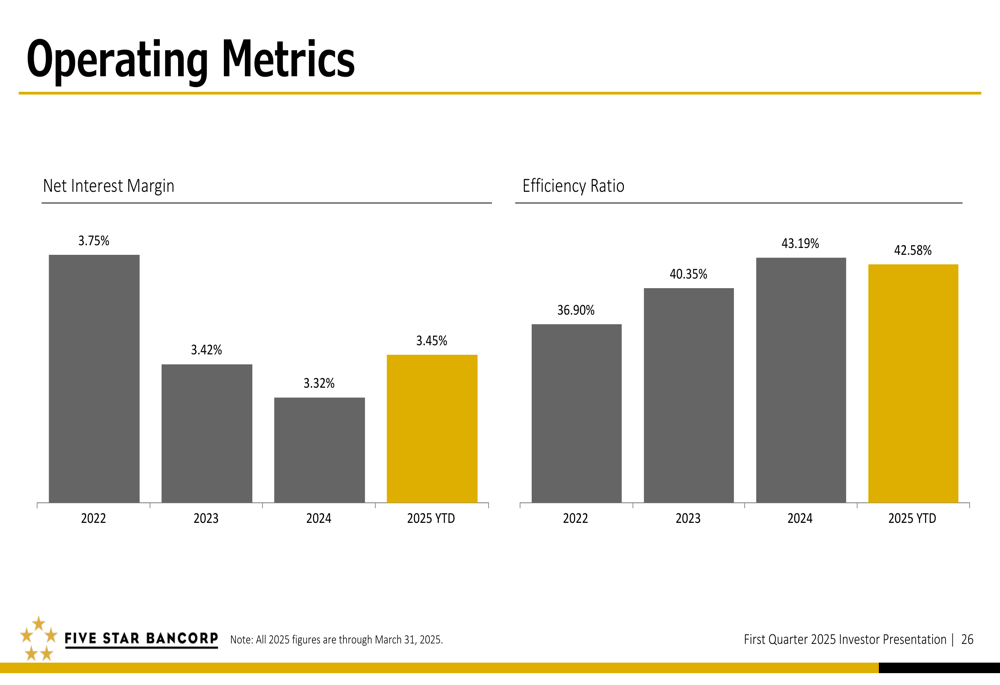

Five Star’s efficiency ratio for Q1 2025 stood at 42.58%, showing improvement from 43.19% for the full year 2024. This metric indicates the bank’s ability to generate revenue while controlling expenses, positioning it favorably compared to industry peers.

As illustrated in the operating metrics trends:

Loan Portfolio and Credit Quality

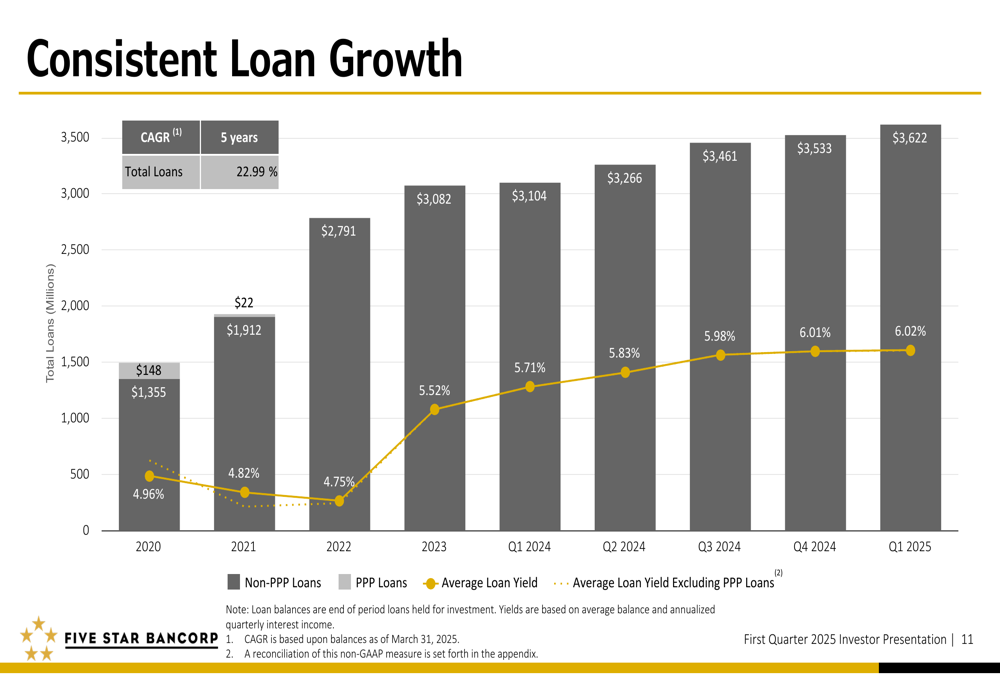

Five Star Bancorp reported strong loan growth in Q1 2025, with loans held for investment increasing by $89.1 million (2.52%) from December 31, 2024, to reach $3.62 billion. The bank has maintained consistent loan growth with a five-year compound annual growth rate (CAGR) of 22.99%.

The following chart demonstrates the bank’s consistent loan growth trajectory and yield trends:

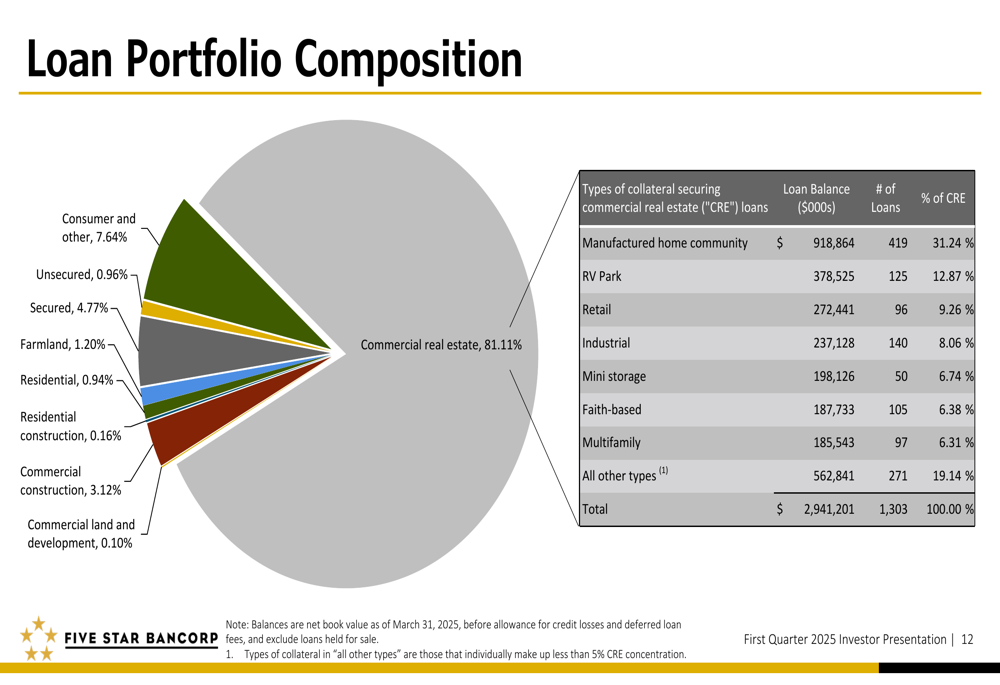

The loan portfolio remains heavily concentrated in commercial real estate (CRE) at 81.11%, with manufactured home communities representing the largest segment at 31.24% of CRE loans. Other significant CRE categories include RV parks (12.87%), retail (9.26%), and industrial (8.06%). During the earnings call, management highlighted strong performance in mobile home and RV park lending.

The detailed breakdown of the loan portfolio composition is shown below:

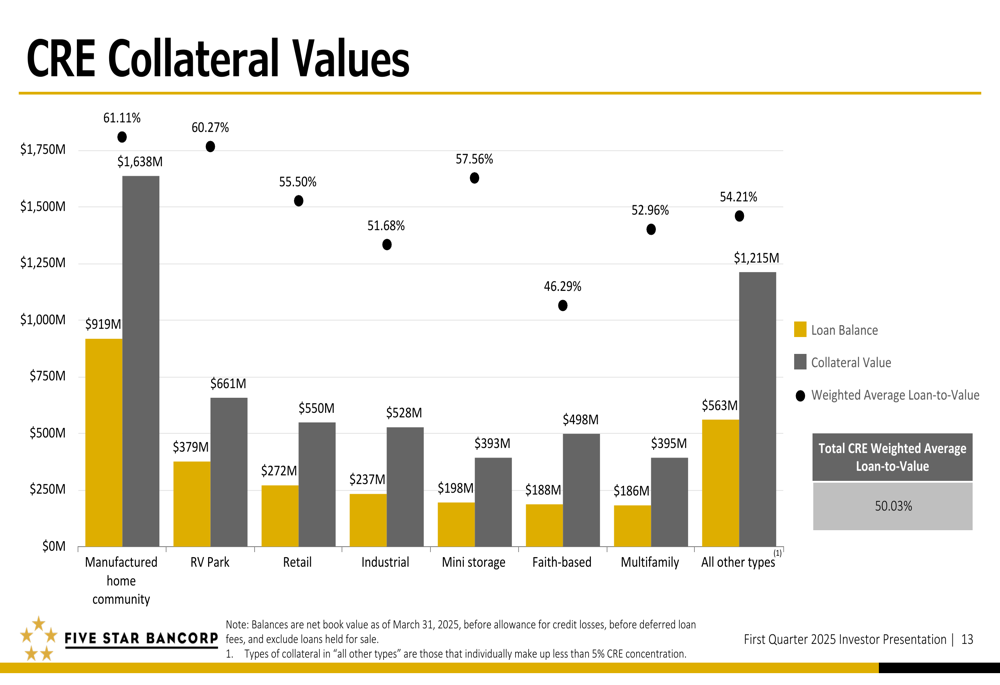

Five Star maintains conservative underwriting standards, with a weighted average loan-to-value ratio of 50.03% across its CRE portfolio. This conservative approach provides significant collateral protection and reduces risk in the event of market downturns.

The following chart illustrates the CRE collateral values and loan-to-value ratios:

Asset quality remains strong with nonperforming loans to loans held for investment at 0.05% and allowance for credit losses to loans held for investment at 1.08% as of Q1 2025, unchanged and slightly increased, respectively, from Q4 2024. The stability in these metrics reflects the bank’s disciplined credit risk management.

Deposit Growth and Funding

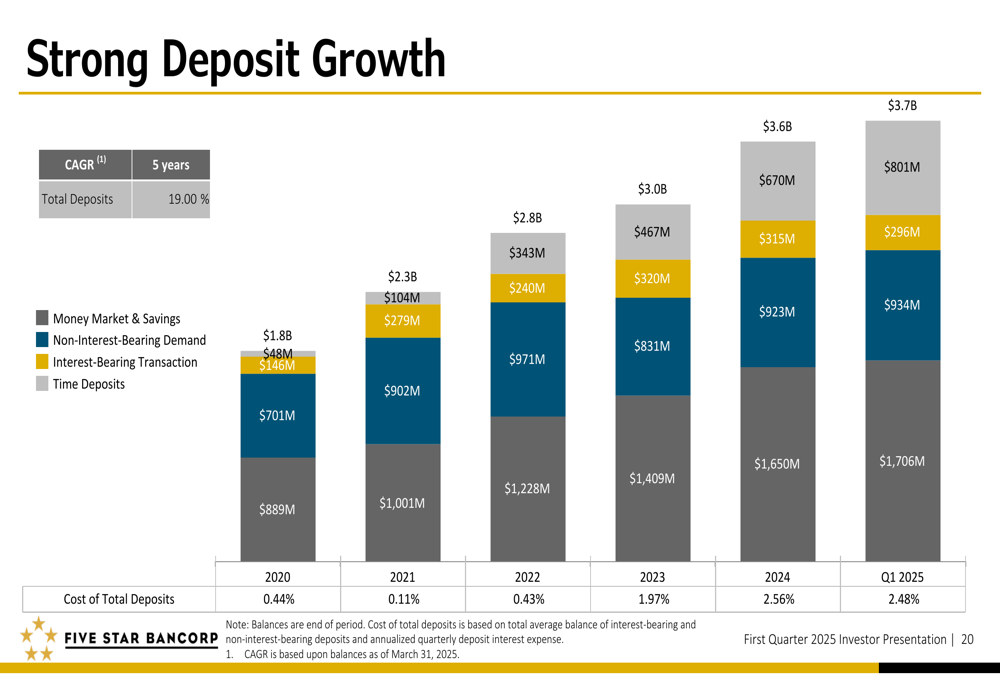

Total (EPA:TTEF) deposits reached $3.7 billion in Q1 2025, representing a 5.0% increase from Q4 2024 and continuing the bank’s strong deposit growth trajectory with a five-year CAGR of 19.00%. Non-wholesale deposits increased by $48.4 million since December 31, 2024, demonstrating the bank’s ability to attract core deposits.

The following chart shows the bank’s deposit growth and cost trends:

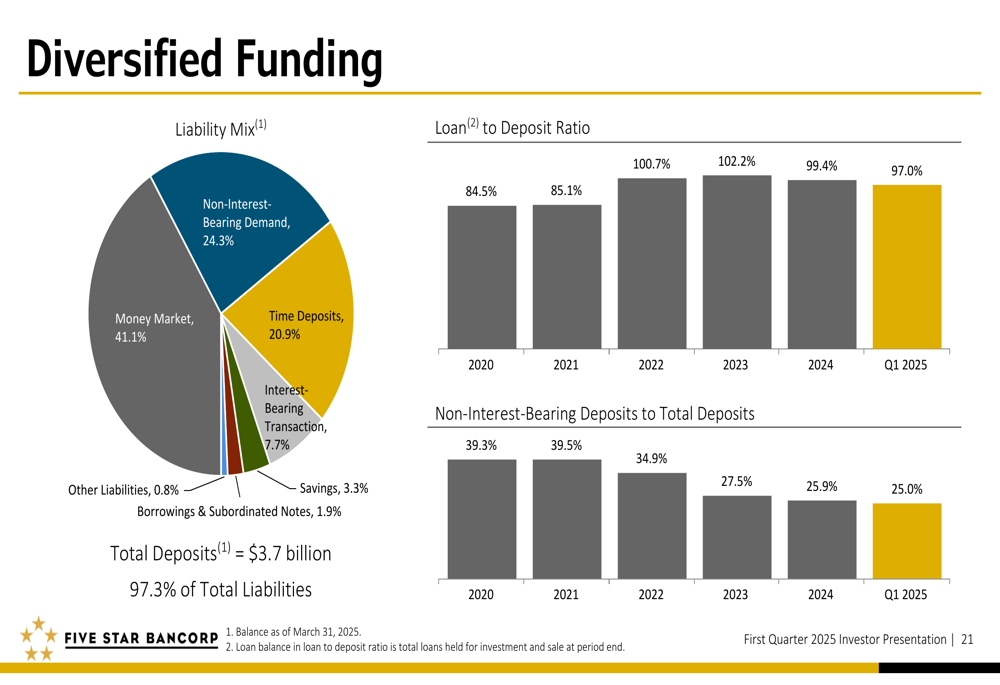

The deposit base remains diversified, with non-interest-bearing demand deposits comprising 24.99% of total deposits. Money market accounts represent the largest component at 41.1%, followed by time deposits at 20.9%. The loan-to-deposit ratio improved to 97.0% in Q1 2025 from 99.4% in Q4 2024, indicating enhanced liquidity.

The liability mix and funding diversification are illustrated below:

Insured and collateralized deposits totaled approximately $2.5 billion, representing 67.55% of total deposits, while cash and cash equivalents stood at $452.6 million or 12.11% of total deposits. These metrics highlight the bank’s strong liquidity position and reduced funding risk.

Capital Position and Shareholder Returns

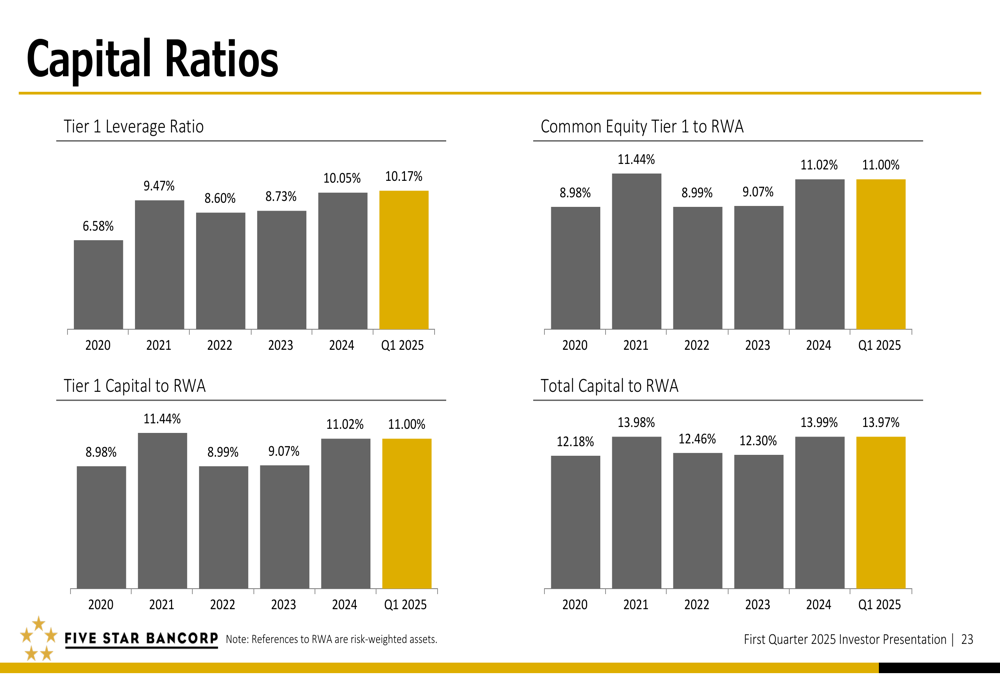

Five Star Bancorp maintains robust capital ratios, with all metrics exceeding well-capitalized regulatory thresholds. As of Q1 2025, the Tier 1 leverage ratio stood at 10.17%, Tier 1 capital to risk-weighted assets at 11.00%, and total capital to risk-weighted assets at 13.97%.

The following chart demonstrates the bank’s capital ratio trends:

Book value per share increased to $19.06 in Q1 2025 from $18.60 in Q4 2024, representing a 2.47% quarterly increase. The bank declared cash dividends of $0.20 per share for Q1 2025, maintaining its commitment to shareholder returns. According to the earnings article, Five Star has consistently raised its dividend for four consecutive years, currently offering a 2.96% yield.

The company’s shareholder return metrics are illustrated below:

Forward-Looking Statements

Looking ahead, Five Star Bancorp projects 10-12% loan growth for the remainder of 2025, as noted in the earnings call. CEO James Beckwith expressed optimism, stating, "We’re a little more bullish than the last time we spoke," indicating confidence in the company’s growth trajectory.

The bank’s expansion into the San Francisco Bay Area is expected to drive further growth opportunities. However, management acknowledged potential challenges, including tariff impacts on the portfolio, competitive loan pricing pressures, and possible increases in economic reserve requirements.

Five Star’s consistent financial performance, strong asset quality, and robust capital position position it well for continued growth as it celebrates its 25th anniversary. The bank’s focus on relationship banking and specialized lending niches in commercial real estate provides a competitive advantage in its markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.