Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

FleetPartners Group Limited (ASX:FPR) presented its third-quarter 2025 business update on July 23, highlighting resilient financial performance despite temporary disruptions from a major system implementation. The vehicle leasing and fleet management company’s stock closed at $3.11 on July 22, up 1.3% ahead of the update.

The presentation emphasized FleetPartners’ position as a "predictable cash generative business operating in a defensive asset class" with growth opportunities in underpenetrated markets. Management noted that while the operating environment remains stable with high tender activity, it faces a subdued macroeconomic backdrop, particularly in New Zealand.

Quarterly Performance Highlights

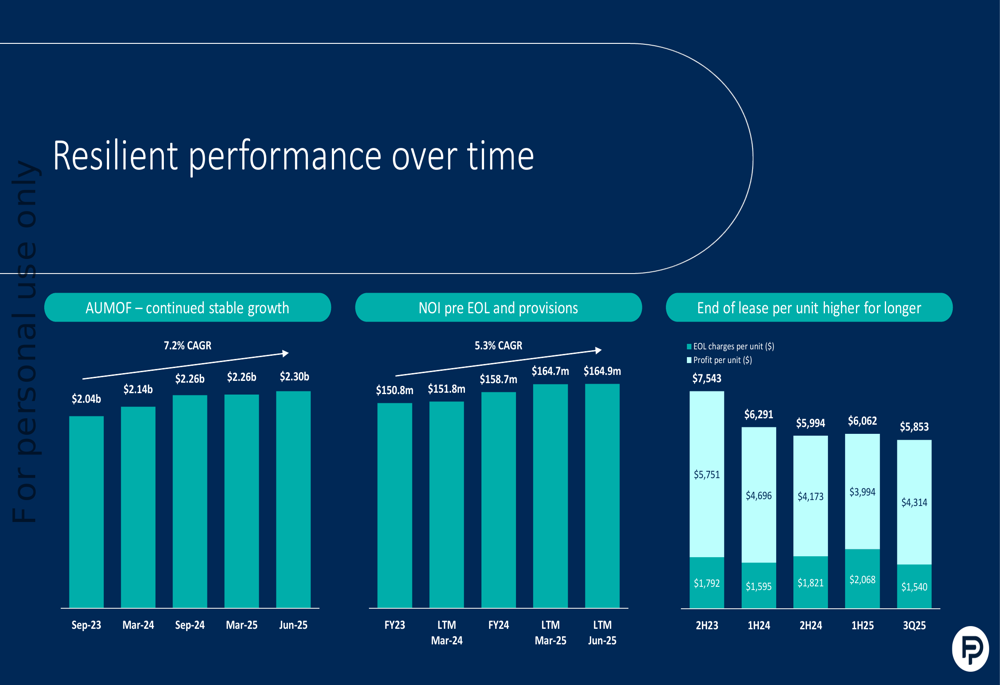

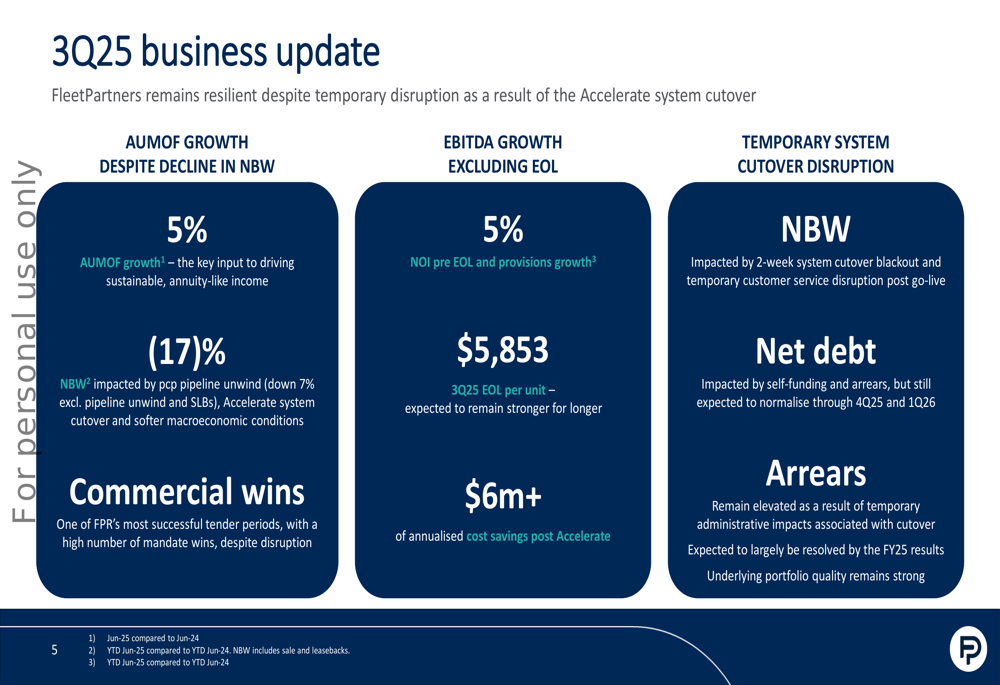

FleetPartners reported 5% year-over-year growth in Assets Under Management and On-Balance Sheet Financing (AUMOF), reaching $2.30 billion as of June 2025. The company also achieved 5% growth in Net Operating Income (NOI) pre-End of Life (EOL) and provisions compared to the previous corresponding period.

As shown in the following chart of financial performance over time, the company has maintained consistent growth in its key metrics:

However, New Business Writings (NBW) declined by 17% year-to-date, which management attributed to previous period pipeline unwinding, the "Accelerate" system cutover, and softer macroeconomic conditions. Excluding pipeline unwind and sale-leasebacks, the decline was limited to 7%.

The following slide summarizes the key 3Q25 metrics:

Detailed Financial Analysis

FleetPartners’ business segments showed mixed performance. Fleet Australia’s AUMOF on balance sheet grew to $666 million in June 2025 from $531 million in September 2023, while Fleet New Zealand’s AUMOF on balance sheet increased to NZ$569 million from NZ$531 million over the same period. The Novated leasing segment saw its AUMOF balance sheet grow to $611 million from $381 million.

End of lease income remains a significant profit driver for the company. EOL charges per unit were $4,314 in 3Q25, generating profit per unit of $1,540. While these figures are down from the 1H25 peak ($3,994 EOL charges with $2,068 profit per unit), they remain substantially above pre-COVID levels.

The following chart illustrates the end of lease income trends:

On the funding front, FleetPartners completed a $400 million Australian Asset-Backed Securities (ABS) issuance in July 2025, with Class A notes priced at 100 basis points. This strengthened the company’s liquidity position, with undrawn capacity increasing to $1,140 million post-ABS from $295 million.

Strategic Initiatives & System Implementation

A significant focus of the presentation was the company’s "Accelerate" system implementation, which caused temporary disruptions across the business. Management outlined a clear pathway to resolve these issues, with most expected to normalize by the FY25 results announcement.

The company highlighted that despite short-term challenges, the Accelerate program has delivered over $6 million in annualized cost savings and strengthened FleetPartners’ operating position by unifying operations under one brand and integrated platform.

The following slide outlines why investors should consider FleetPartners, emphasizing its market positioning and financial characteristics:

Forward-Looking Statements

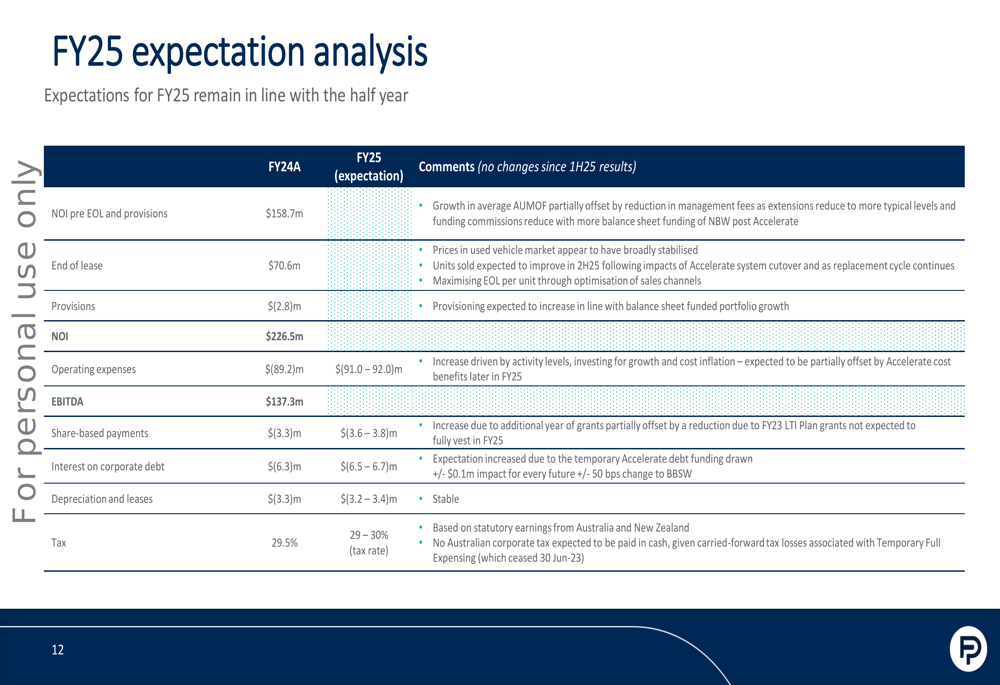

For the full fiscal year 2025, FleetPartners provided detailed expectations across key financial metrics. The company anticipates NOI pre EOL and provisions to reach $166-168 million, up from $158.7 million in FY24. End of lease income is expected to be $64-66 million, down from $70.6 million, reflecting the normalization of used vehicle prices, though still above pre-COVID levels.

The following table details the company’s FY25 expectations compared to FY24 actuals:

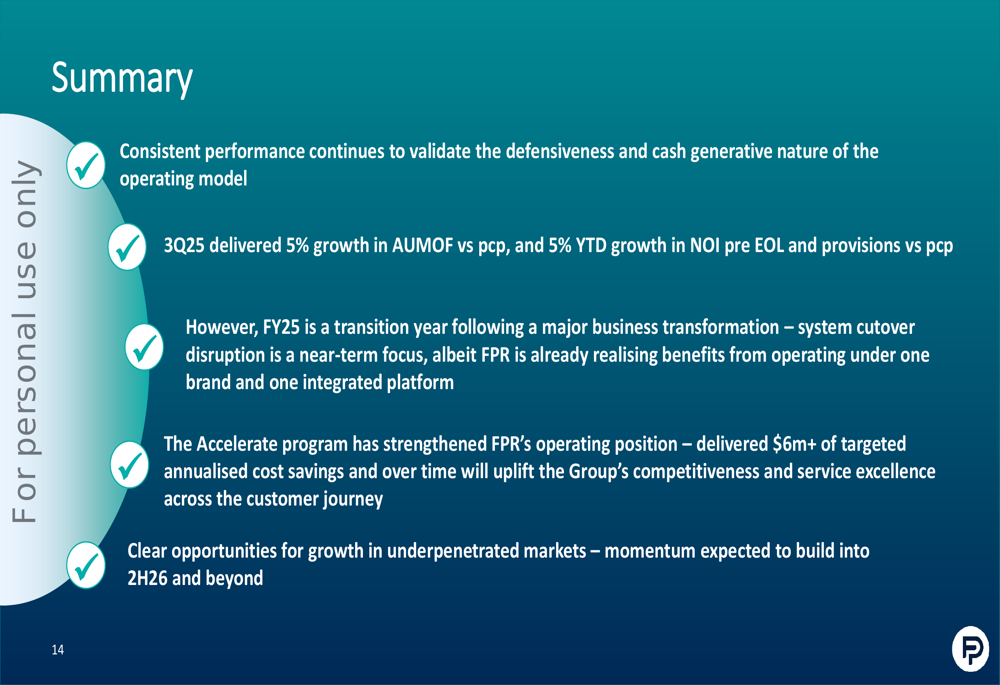

Management characterized FY25 as a "transition year" following the major business transformation but expressed confidence that the Accelerate program will enhance the group’s competitiveness and service excellence over time. Growth momentum is expected to build into the second half of 2026 and beyond.

The presentation concluded with this summary of key takeaways:

FleetPartners continues to demonstrate the defensive nature of its business model while navigating temporary disruptions from its system implementation. With $9.2 million of announced share buybacks completed in 2H25 and total capital returns of $39.2 million year-to-date, the company maintains its focus on shareholder returns while positioning for future growth in underpenetrated markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.