60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

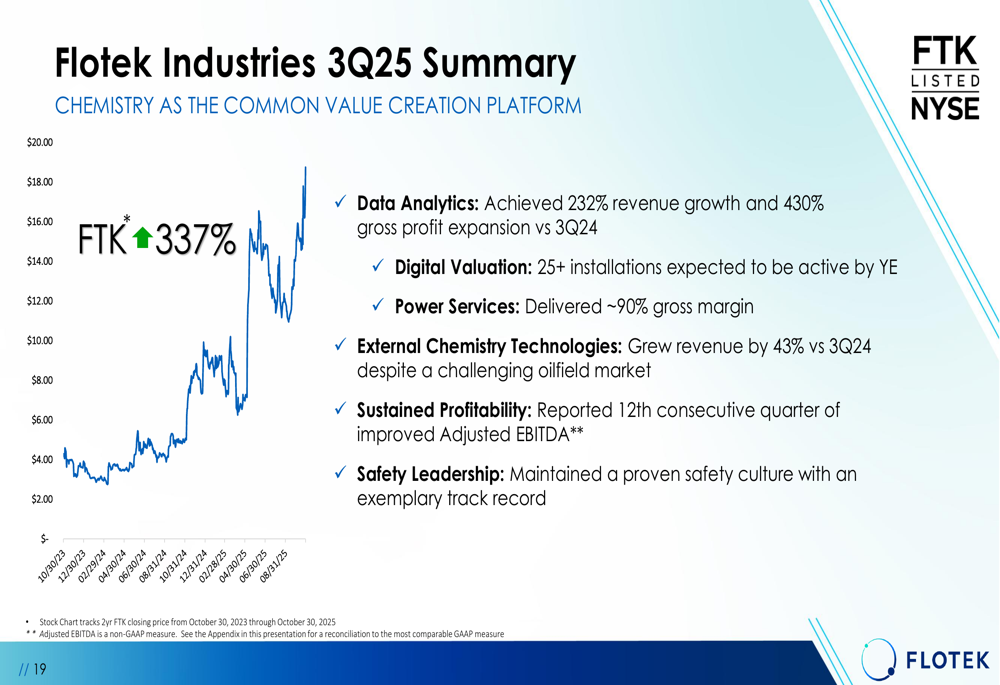

Flotek Industries Inc (NYSE:FTK) delivered a standout third quarter performance for 2025, according to its earnings presentation released on November 5. The company's strategic pivot toward data analytics is yielding substantial returns, with shares jumping 8.67% in premarket trading to $18.04, approaching the 52-week high of $18.96.

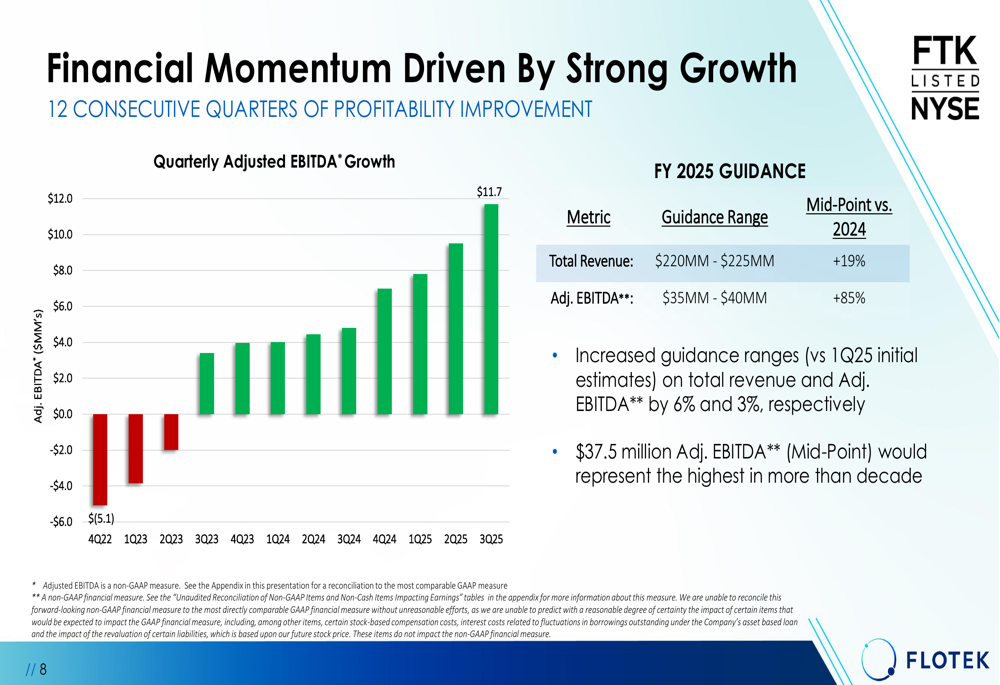

The Houston-based chemistry and data analytics provider has successfully transformed its business model, achieving its 12th consecutive quarter of improved adjusted EBITDA while expanding its footprint in high-margin data analytics services.

Quarterly Performance Highlights

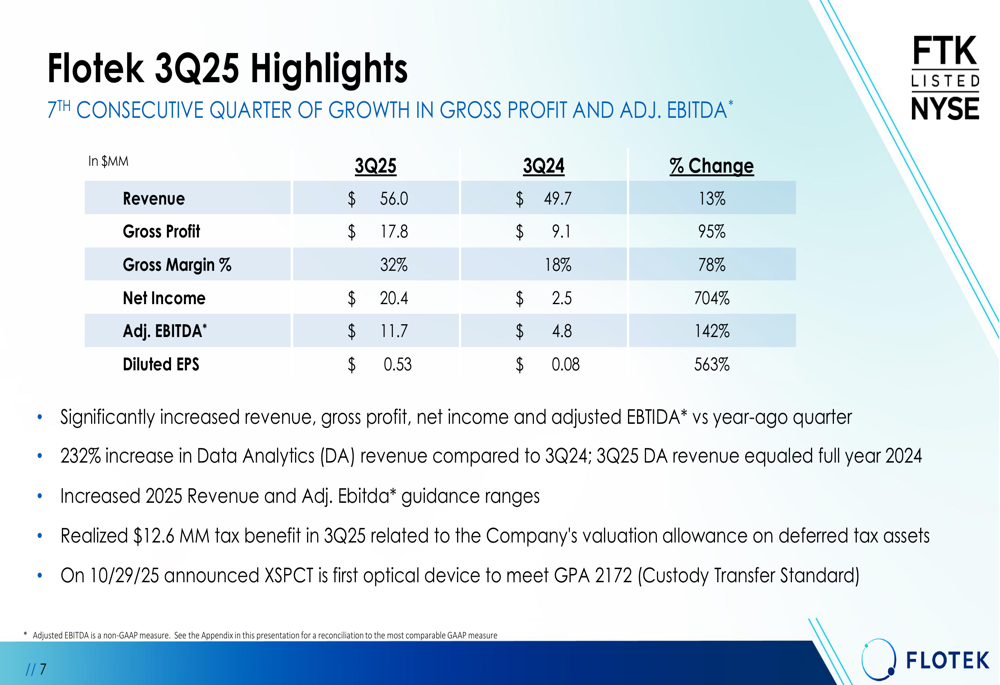

Flotek reported impressive financial results for Q3 2025, marking its seventh consecutive quarter of growth in gross profit and adjusted EBITDA. Revenue reached $56.0 million, up 13% year-over-year, while gross profit nearly doubled to $17.8 million, representing a 95% increase from Q3 2024.

The company's profitability metrics showed even more dramatic improvements, with net income surging 704% to $20.4 million and adjusted EBITDA climbing 142% to $11.7 million. Gross margin expanded significantly from 18% to 32%, reflecting the company's shift toward higher-margin business segments.

As shown in the following financial summary:

Notably, Flotek realized a $12.6 million tax benefit in Q3 2025, contributing to the substantial net income growth. Diluted earnings per share increased 563% year-over-year to $0.53.

Strategic Initiatives

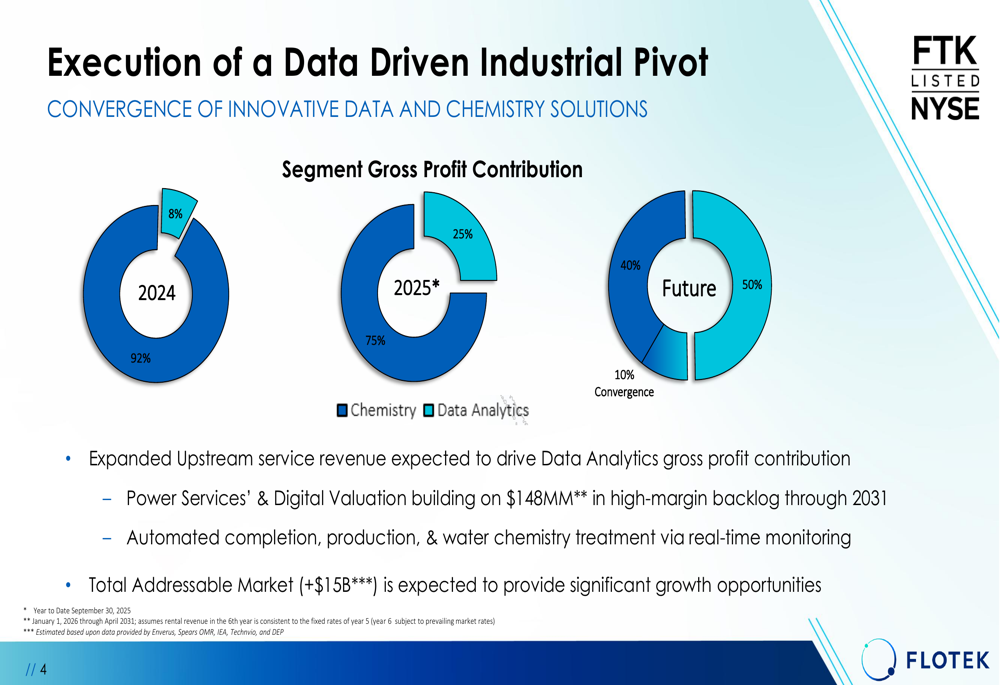

The cornerstone of Flotek's transformation is its "Chemistry as the Common Value Creation Platform" strategy, which leverages the company's traditional chemistry expertise while aggressively expanding into data analytics. This pivot is reshaping the company's revenue mix and profitability profile.

The presentation highlights how segment gross profit contribution is evolving from predominantly chemistry-based to a more balanced portfolio:

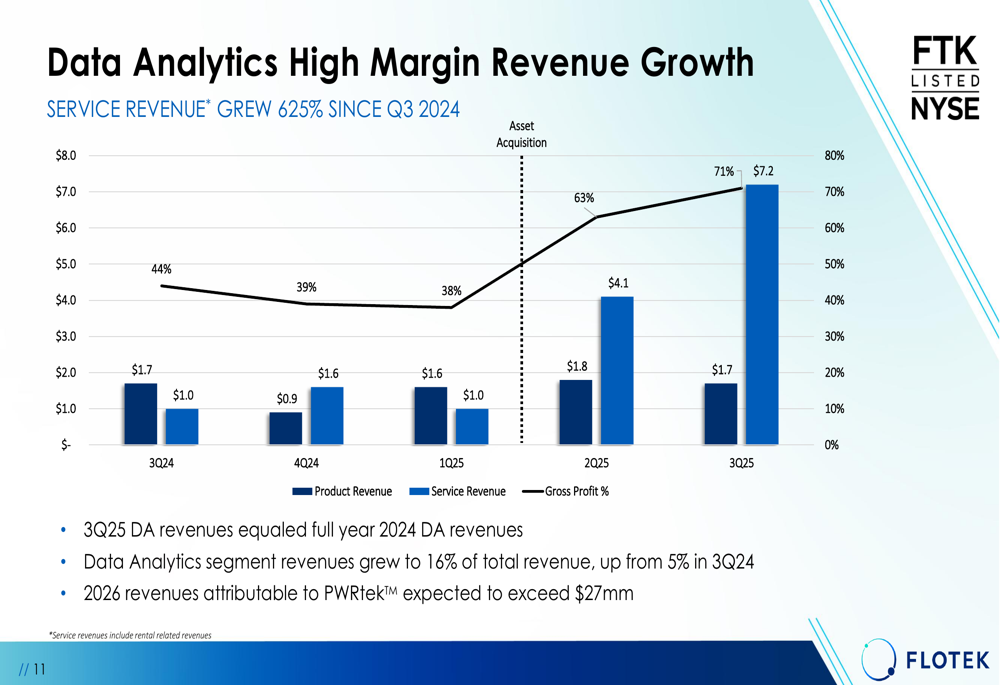

The data analytics segment has shown remarkable growth, with revenue increasing 232% compared to Q3 2024. This segment now represents 16% of total revenue, up from just 5% a year earlier. Even more impressive, data analytics service revenue grew 625% since Q3 2024, as illustrated in this chart:

CEO Ryan Ezell emphasized the company's strategic direction during the earnings call, stating: "We are committed to shaping the industry's digitalized future by leveraging chemistry as the common value creation platform."

Detailed Financial Analysis

Flotek's financial momentum is clearly demonstrated in its 12 consecutive quarters of profitability improvement. The company has transformed from negative adjusted EBITDA in late 2022 to $11.7 million in Q3 2025, representing a remarkable turnaround.

The presentation tracks this progression alongside key strategic milestones:

The chemistry business has shown resilience despite market contraction. While industry fleet counts declined from 238 to 179 year-over-year, Flotek achieved 54% growth in external chemistry sales for the first nine months of 2025 and a 21% increase in total chemistry revenue compared to the same period in 2024.

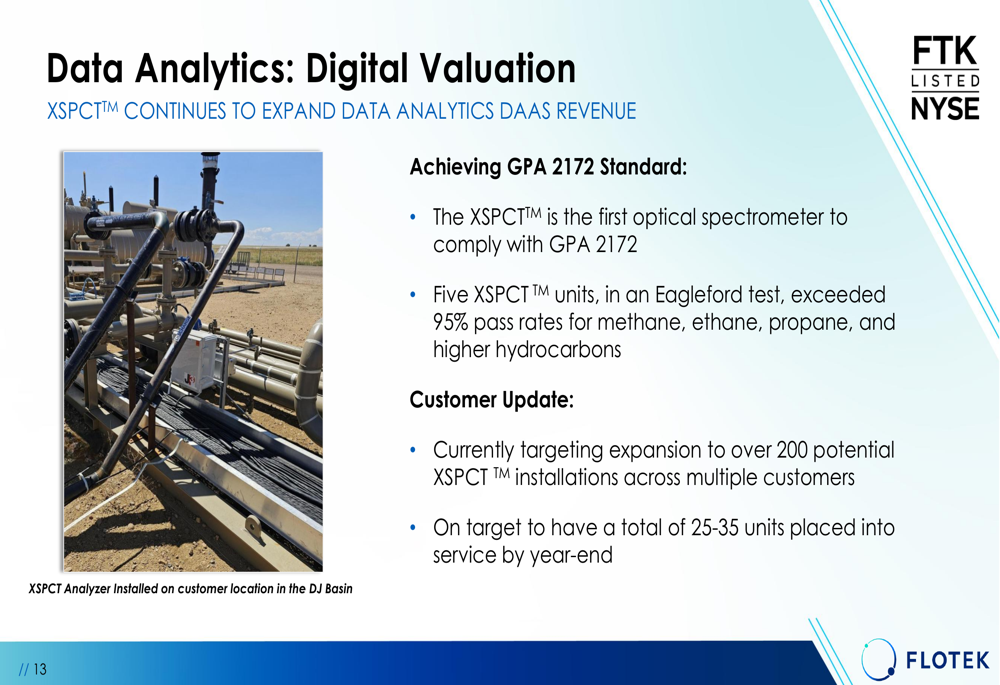

In the data analytics segment, Flotek has made significant technological advancements. Its XSPCT™ analyzer became the first optical spectrometer to comply with the GPA 2172 custody transfer standard, an important industry milestone that positions the company for further market penetration:

The company expects to have 25-35 XSPCT units in service by year-end, targeting over 200 potential installations. Additionally, Flotek's Power Services business is delivering approximately 90% gross margins, contributing to the overall profitability improvement.

Forward-Looking Statements

Based on its strong performance, Flotek has raised its full-year 2025 guidance. The company now expects total revenue of $220-225 million, representing a 19% increase at the midpoint compared to 2024. Adjusted EBITDA guidance was increased to $35-40 million, an 85% improvement at the midpoint versus the previous year.

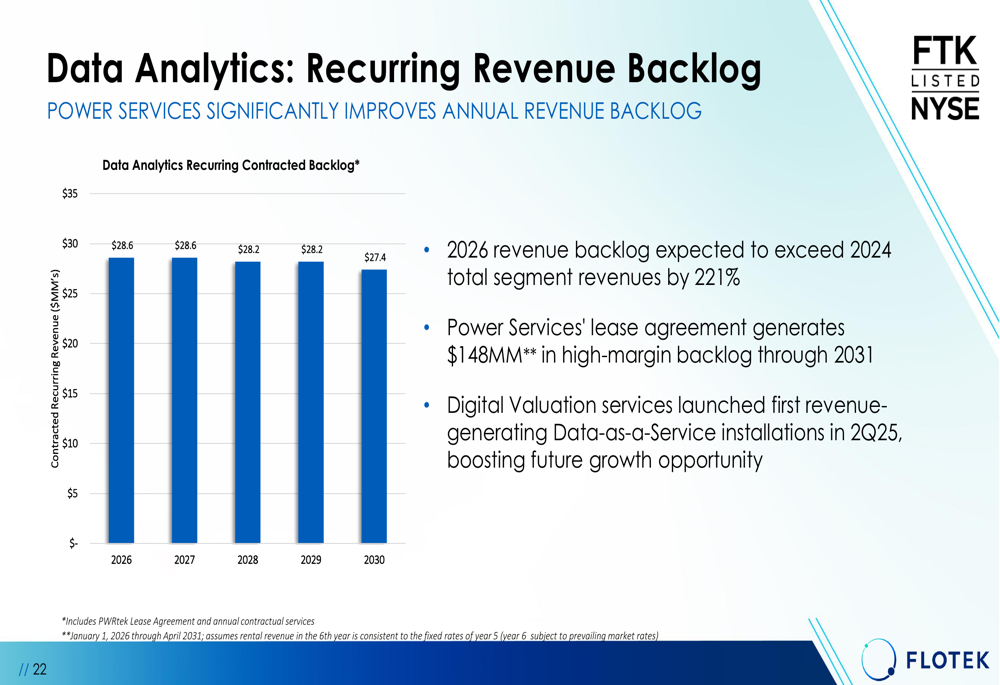

Looking further ahead, Flotek has built a substantial recurring revenue backlog in its data analytics segment, providing visibility into future performance. The company projects that 2026 revenue backlog will exceed 2024 total revenues by 221%, with Power Services' lease agreements generating $148 million in backlog through 2031.

PWRtek revenues are expected to exceed $27 million in 2026, while data analytics is projected to contribute over 50% of the company's profitability by that time.

Competitive Industry Position

Flotek's innovation strategy is driving market expansion across upstream, midstream, and downstream segments. The company's "Measure More Strategy" leverages its technologies to address a total addressable market exceeding $15 billion.

In the chemistry segment, Flotek maintains competitive advantage through its Prescriptive Chemistry Management (PCM)™ approach, which combines proprietary solutions with AI-driven analytics from data collected across 20,000 wells. The company holds over 130 patents supporting its technological edge.

For data analytics, Flotek is establishing leadership positions in several areas, including power services with patented technology for alternative fuel sources, digital valuation through its XSPCT™ platform, and flare monitoring solutions that comply with EPA requirements.

The company's stock performance reflects investor confidence in this strategy, with 337% price growth between October 2023 and October 2025, as highlighted in the presentation's summary:

As Flotek continues its transformation, the company appears well-positioned to capitalize on the convergence of chemistry and data solutions in the energy sector, with a strong financial foundation and clear strategic direction for sustained growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.