Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Flushing Financial Corporation (NASDAQ:FFIC) reported continued improvement in its net interest margin and deposit growth during its second quarter 2025 earnings presentation on July 25. Despite the challenging banking environment, the company highlighted its conservative lending approach and strategic focus on Asian markets as key drivers of performance.

Quarterly Performance Highlights

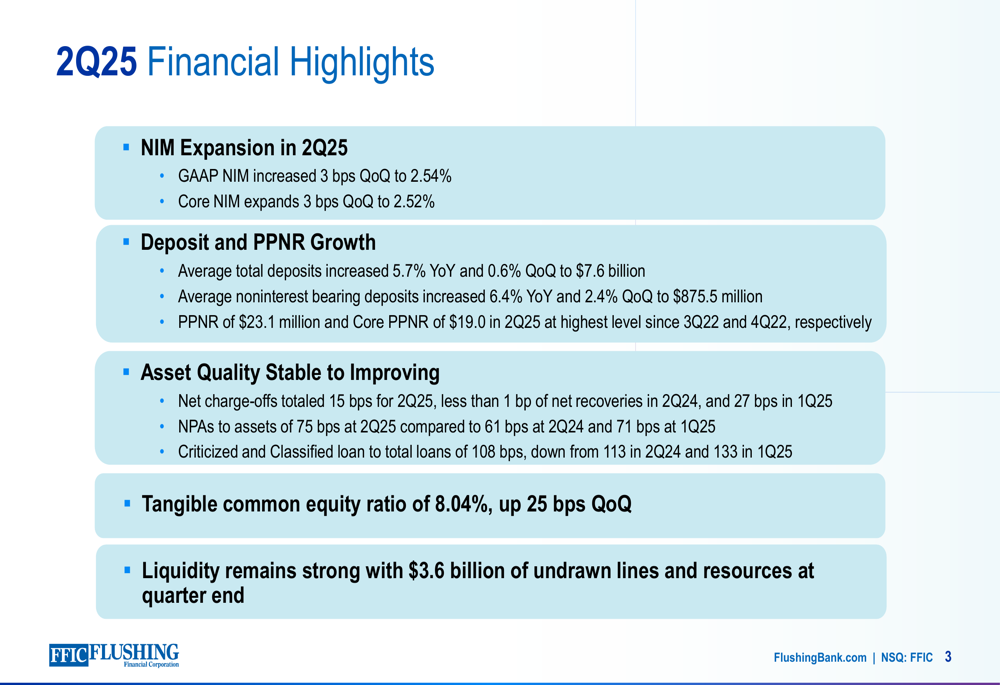

Flushing Financial reported several positive metrics for Q2 2025, including NIM expansion, deposit growth, and improved credit quality. The company’s GAAP net interest margin increased 3 basis points quarter-over-quarter to 2.54%, while core NIM also expanded 3 basis points to 2.52%.

As shown in the following financial highlights, the company saw improvements across multiple metrics:

Pre-provision net revenue (PPNR) reached $23.1 million in Q2 2025, representing the highest level since Q3 2022. Similarly, core PPNR hit $19.0 million, the highest since Q4 2022. These improvements came despite the stock declining 2.4% on July 24, 2025, according to the most recent market data.

NIM Expansion and Profitability Improvement

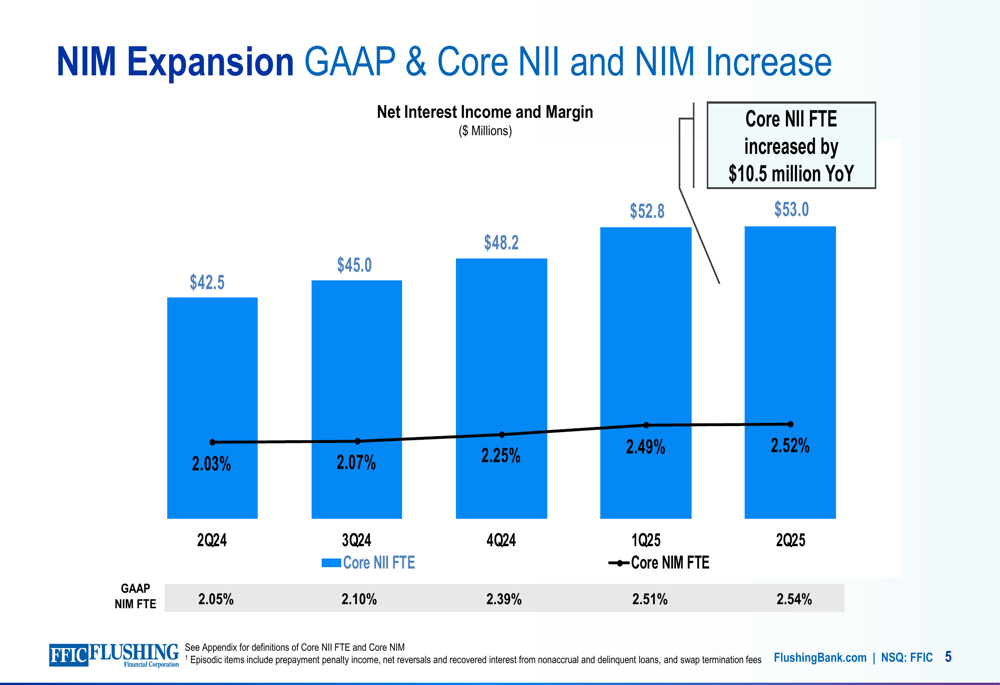

The company’s net interest margin has shown consistent improvement over the past year, rising from 2.03% in Q2 2024 to 2.52% in Q2 2025. This expansion has been driven by higher-yielding loan repricing and disciplined deposit cost management.

The following chart illustrates the steady growth in net interest income and margin over the past five quarters:

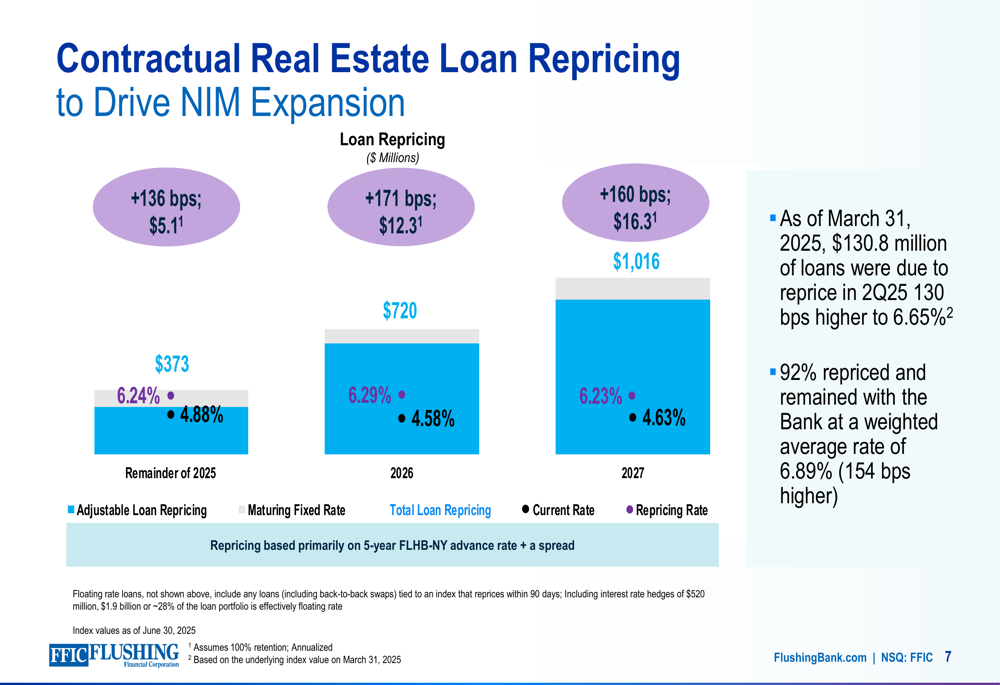

A key driver of future NIM expansion is the contractual repricing of the real estate loan portfolio. Flushing Financial expects significant benefits as loans reprice at higher rates through 2027, with approximately $33.7 million in additional interest income projected.

The following chart details the loan repricing schedule and expected rate increases:

This repricing opportunity is particularly significant given that loans scheduled to reprice for the remainder of 2025 are expected to yield 136 basis points higher rates, while 2026 and 2027 repricing is projected at 171 and 160 basis points higher, respectively.

Deposit Growth and Asian Market Focus

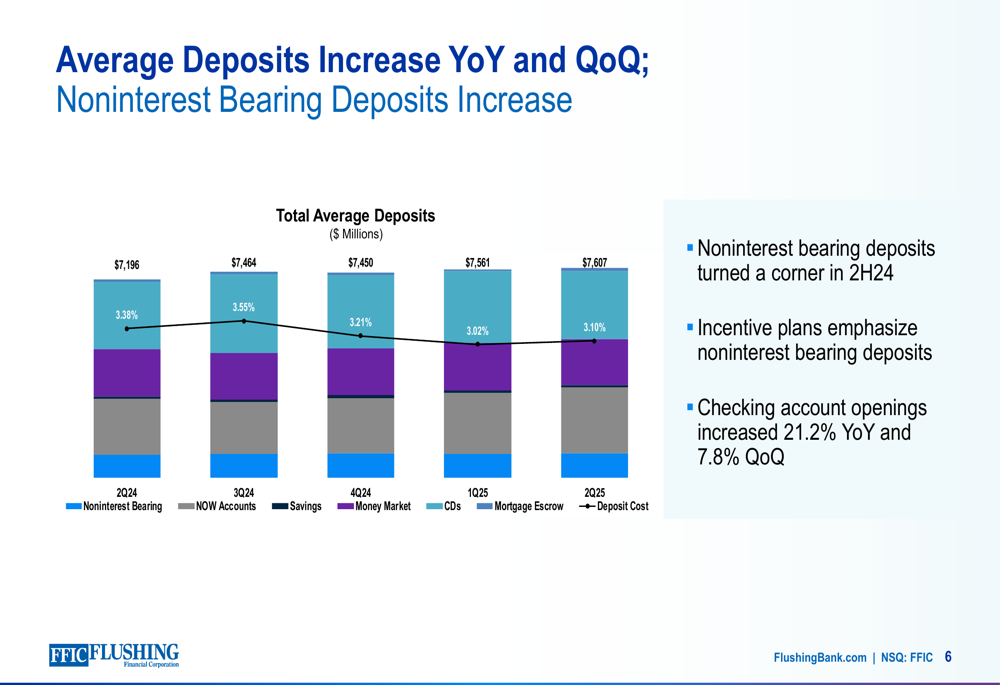

Average total deposits increased 5.7% year-over-year and 0.6% quarter-over-quarter to $7.6 billion. Notably, average noninterest-bearing deposits grew 6.4% year-over-year and 2.4% quarter-over-quarter to $875.5 million, helping to improve the company’s funding mix.

The following chart shows the consistent growth in deposits across various categories:

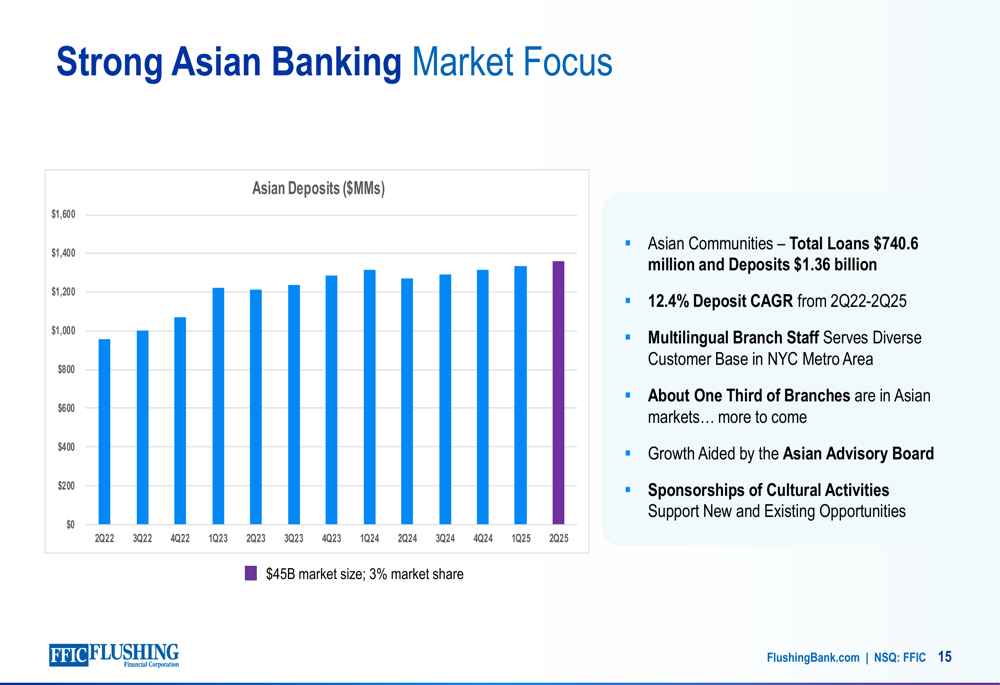

A standout element of Flushing Financial’s strategy is its focus on Asian communities, which has yielded impressive results. The company reported $740.6 million in loans and $1.36 billion in deposits from Asian communities, with a 12.4% deposit CAGR from Q2 2022 to Q2 2025.

The following chart highlights the consistent growth in Asian deposits:

This strategic focus aligns with comments made by CEO John Buran during the Q1 2025 earnings call, where he noted, "Our Asian markets with its dense population, high number of small businesses continues to be an important opportunity." The company plans to continue expanding in these markets, with approximately one-third of branches currently serving Asian communities and more planned.

Credit Quality and Conservative Lending Approach

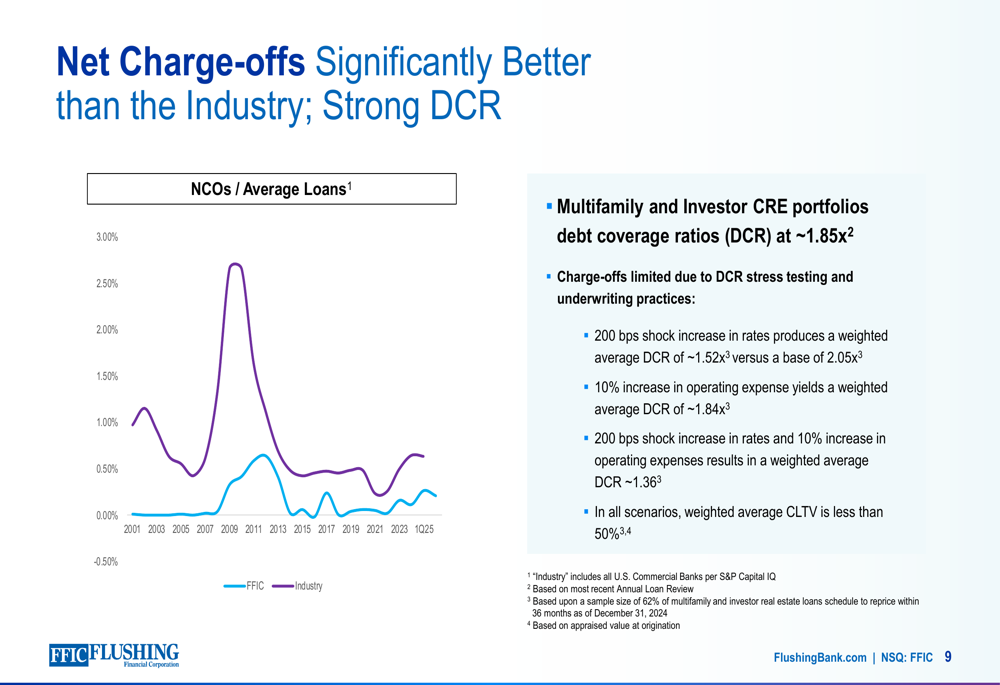

Flushing Financial emphasized its conservative credit approach, which has historically outperformed industry averages. Net charge-offs totaled 15 basis points for Q2 2025, compared to less than 1 basis point of net recoveries in Q2 2024 and 27 basis points in Q1 2025.

The following chart demonstrates how the company’s net charge-offs have consistently outperformed industry averages:

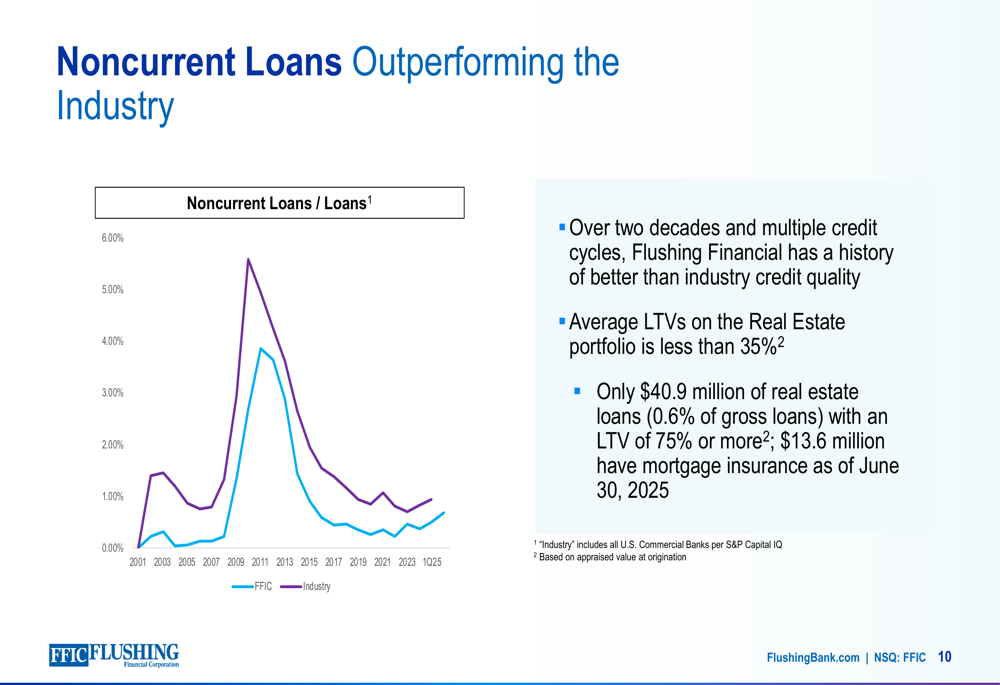

Similarly, noncurrent loans have remained well below industry averages over multiple credit cycles:

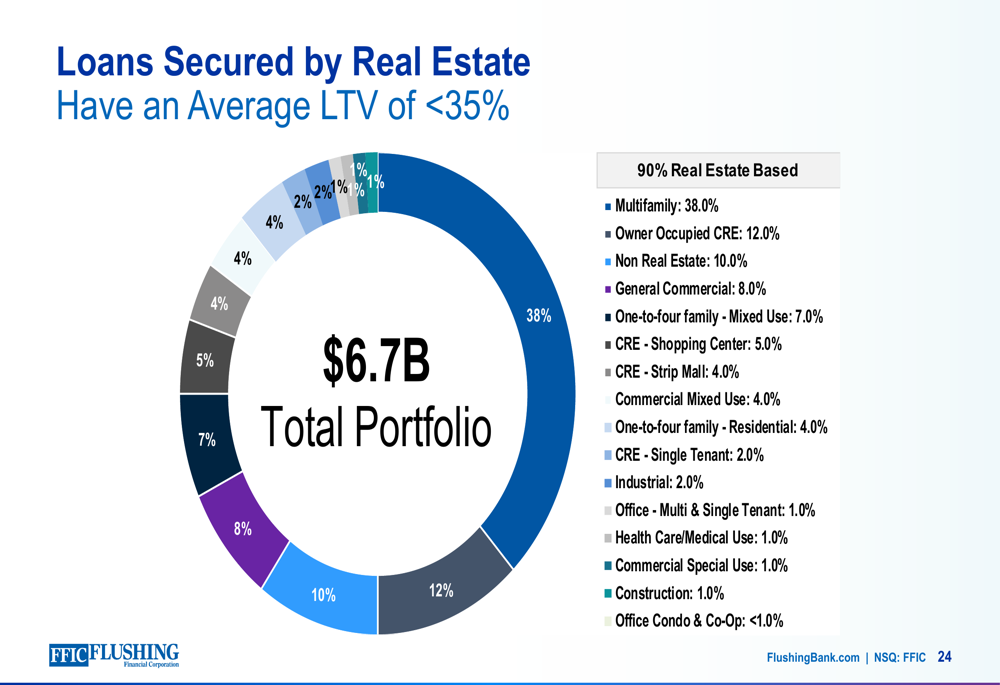

The company attributes this outperformance to its conservative underwriting standards, particularly in its multifamily and commercial real estate portfolios. Approximately 90% of the loan portfolio is secured by real estate with an average loan-to-value ratio of less than 35%, providing significant cushion against potential market downturns.

The following chart shows the composition of the company’s real estate-secured loan portfolio:

Forward-Looking Statements

Looking ahead, Flushing Financial provided several outlook points for the remainder of 2025:

- Stable total assets with loan growth dependent on market conditions

- Continued improvement in asset and funding mix

- Opportunity (SO:FTCE11B) to reprice $391.2 million of retail CDs maturing in Q3 2025 at potentially lower rates

- Approximately $373 million of loans scheduled to reprice 136 basis points higher in 2025

- Core noninterest expense expected to increase 4.5-5.5% from the 2024 base of $159.6 million

- Effective tax rate of 24.5-26.5% for the remainder of 2025

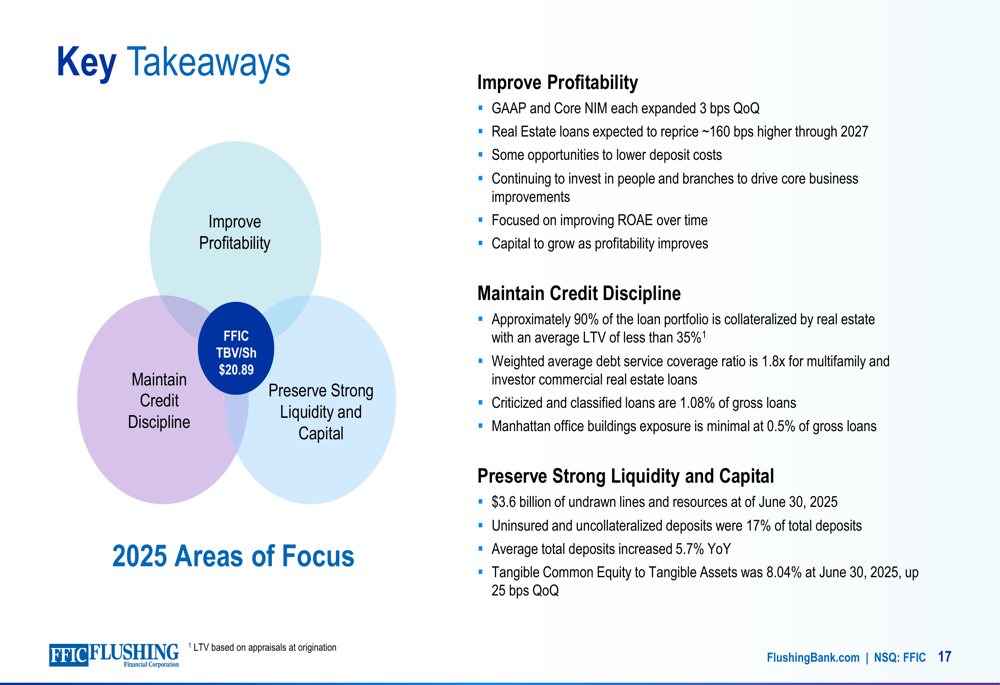

The company summarized its key strategic priorities in the following comprehensive overview:

While the Q2 presentation painted a positive picture of improving performance, it’s worth noting that the company reported a significant non-cash goodwill impairment charge of $17.6 million in Q1 2025, which was not directly addressed in this presentation. Additionally, the stock has faced pressure despite beating earnings expectations in recent quarters, suggesting ongoing investor concerns despite operational improvements.

Nevertheless, Flushing Financial’s focus on NIM expansion through loan repricing, continued deposit growth in Asian markets, and maintaining its conservative credit approach position the company to potentially improve profitability in the coming quarters as it navigates the current banking environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.