Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

FMC Corporation (NYSE:FMC), a leading agricultural sciences company, reported significant year-over-year declines in its first quarter 2025 financial results during its earnings presentation on May 1, 2025. Despite the challenging start to the year, the company’s stock rose 2.1% in after-hours trading to $42.80, suggesting investors were encouraged by management’s outlook for improvement in the second half of the year.

The company faced headwinds from cautious customer purchasing behavior and deliberate inventory management across most regions, resulting in lower volumes. However, FMC maintained its full-year guidance, indicating confidence in a stronger performance during the remainder of 2025.

Quarterly Performance Highlights

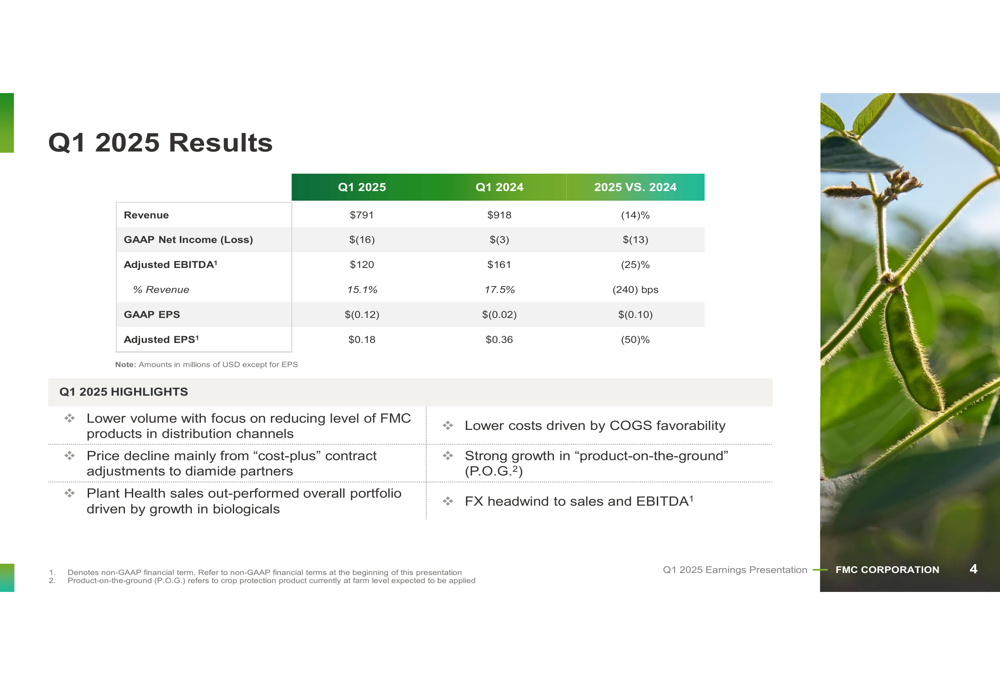

FMC reported Q1 2025 revenue of $791 million, representing a 14% decline compared to the same period last year. The company posted a GAAP net loss of $16 million, compared to a $3 million loss in Q1 2024. Adjusted EBITDA fell 25% year-over-year to $120 million, while adjusted EPS dropped 50% to $0.18.

As shown in the following financial results summary:

The decline in performance was attributed to lower volume due to cautious purchasing behavior, price declines from cost-plus contract adjustments, and foreign exchange headwinds. However, the company did note outperformance in Plant Health sales and lower costs driven by COGS favorability.

Regional Performance Analysis

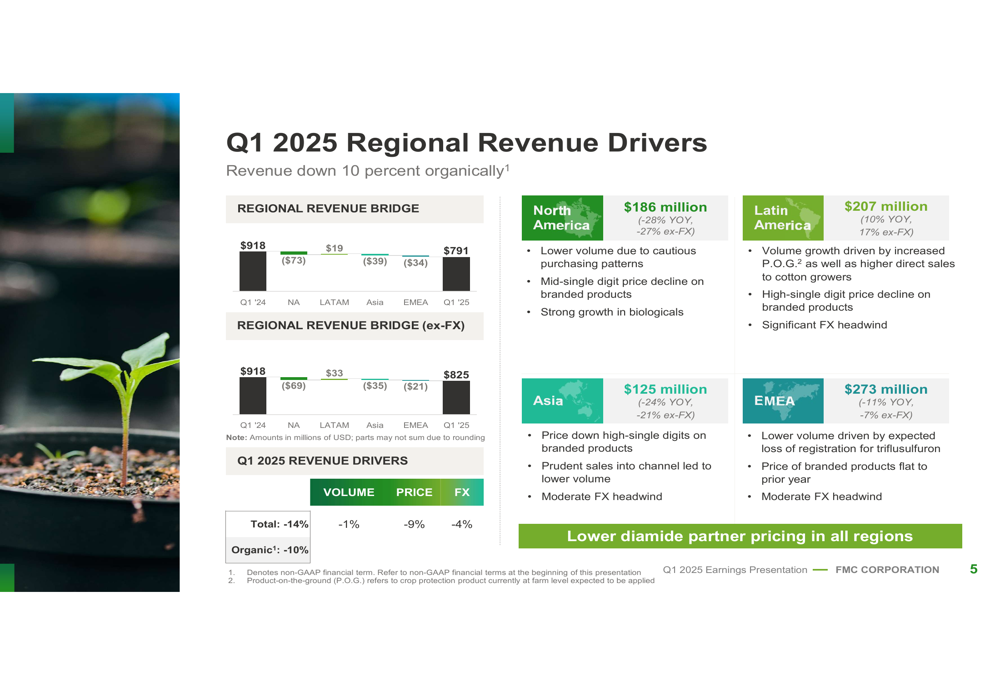

FMC’s regional performance showed significant variation, with Latin America being the only region to deliver positive growth. The company’s revenue declined organically by 10% across all regions combined.

The regional breakdown reveals the following performance:

North America experienced the steepest decline at 28% year-over-year, reaching $186 million in revenue. This was primarily due to cautious purchasing behavior and a mid-single digit price decline, though the company noted strength in biologicals.

Latin America was the bright spot, with revenue increasing 10% to $207 million (17% excluding FX effects). This growth was driven by increased "product-on-the-ground" sales, despite a high-single digit price decline and significant foreign exchange headwinds.

Asia and EMEA (Europe, Middle East, and Africa) saw declines of 24% and 11% respectively, with Asia affected by prudent channel sales and EMEA impacted by the expected loss of registration for triflusulfuron.

Strategic Initiatives

FMC outlined four key focus areas for 2025 to address current challenges and position the company for future growth:

1. Inventory Alignment: Correcting FMC inventory in the channel to align with customer target levels, with expected completion by the end of Q2 in all regions excluding Asia.

2. Rynaxypyr® Strategy: Implementing a strategy to take advantage of lower manufacturing costs to grow solo formulations and provide higher-value products through new formulations and mixtures.

3. Brazil Routes to Market: Establishing an additional route to market in Brazil by selling directly to large corn and soybean growers, with sales expected in the second half of 2025.

4. Growth Portfolio: Ensuring appropriate resources are in place for the growth portfolio to deliver full potential.

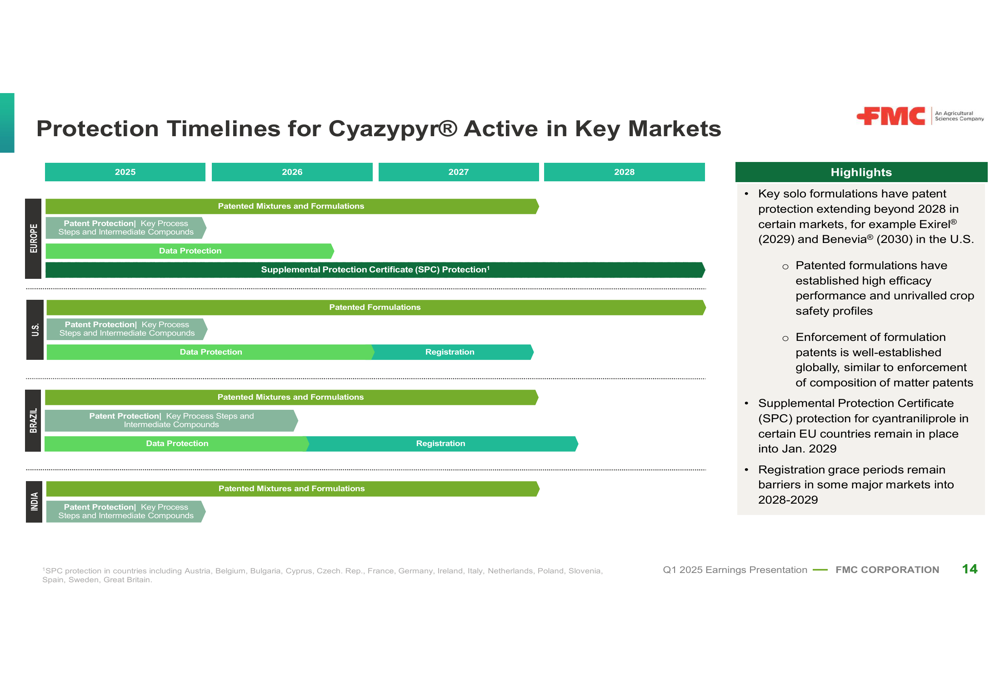

The company also highlighted its protection timelines for Cyazypyr® active in key markets, with patent protection extending beyond 2028 in major regions:

Financial Outlook

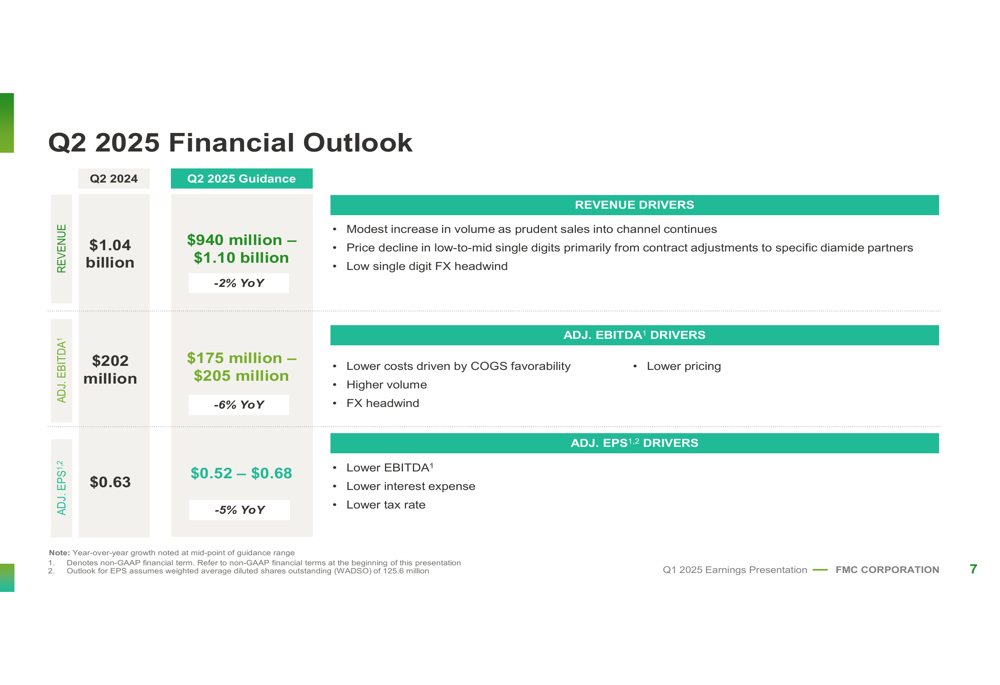

Despite the challenging first quarter, FMC maintained a relatively stable outlook for the remainder of 2025. For Q2 2025, the company expects:

The Q2 guidance projects revenue between $940 million and $1.10 billion (down 2% year-over-year), with adjusted EBITDA of $175-$205 million (down 6%) and adjusted EPS of $0.52-$0.68 (down 5%).

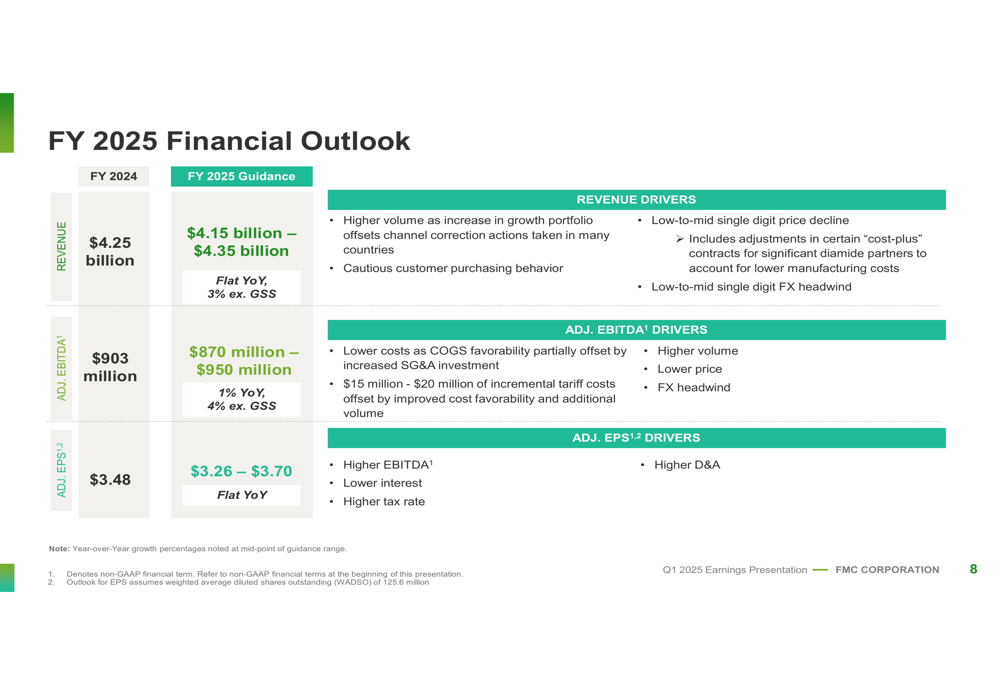

For the full year 2025, FMC provided the following guidance:

Full-year revenue is expected to be between $4.15 billion and $4.35 billion (flat year-over-year, but up 3% excluding Global Specialty Solutions). Adjusted EBITDA is projected at $870-$950 million (up 1% year-over-year, 4% excluding GSS), while adjusted EPS is expected to be $3.26-$3.70 (flat year-over-year).

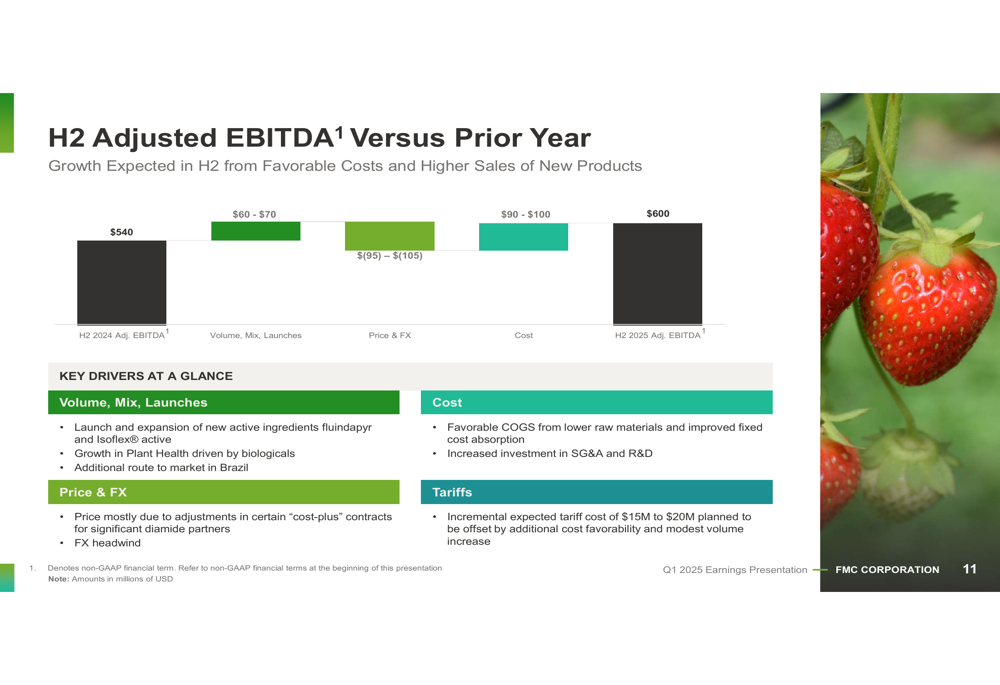

The company anticipates a significant improvement in the second half of 2025 compared to the same period in 2024:

This improvement is expected to be driven by volume growth of $60-$70 million and cost favorability of $90-$100 million, partially offset by price and FX headwinds of $95-$105 million.

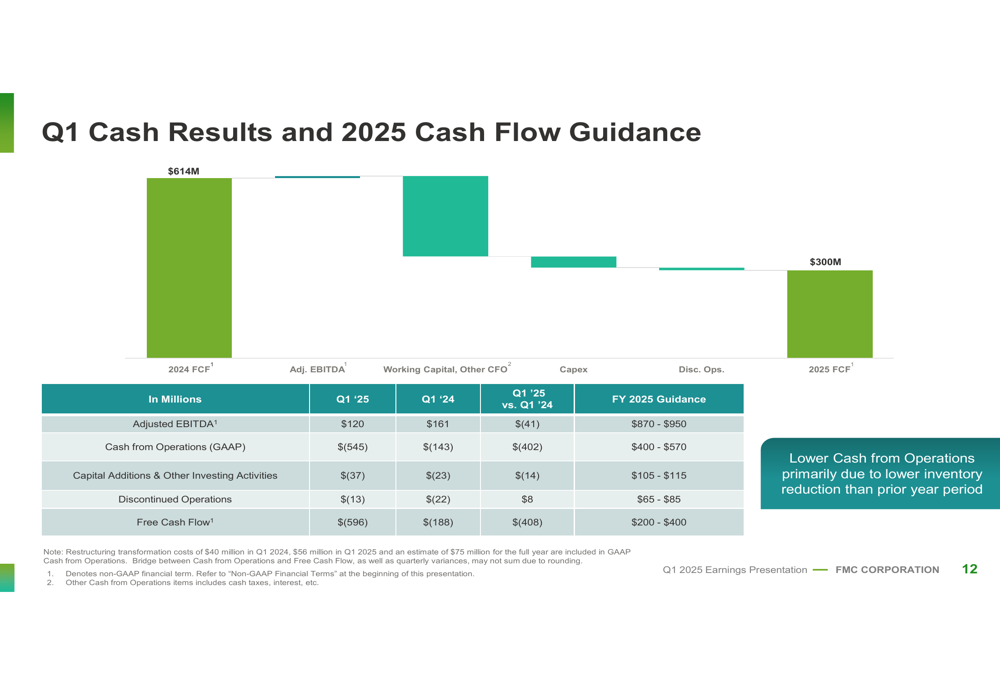

Cash Flow and Tariff Impacts

FMC’s cash flow performance in Q1 2025 was challenging, with negative cash from operations of $545 million compared to negative $143 million in Q1 2024. The company attributed this primarily to lower inventory reduction than the prior year period.

The cash flow results and guidance are summarized below:

Despite the weak Q1 performance, FMC maintained its full-year free cash flow guidance of $200-$400 million.

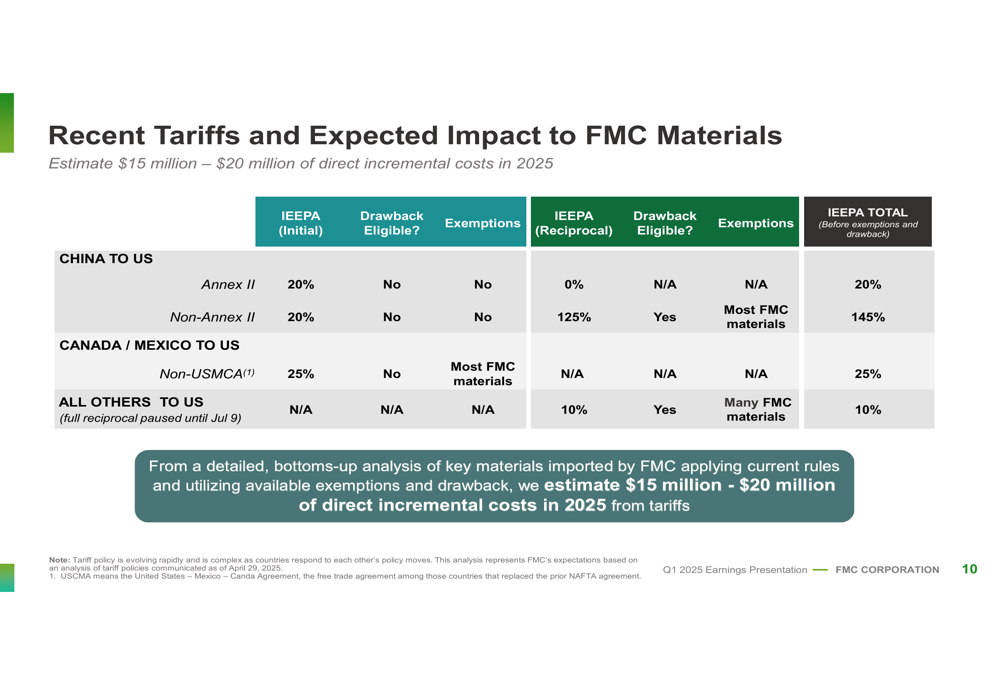

The company also addressed the evolving tariff environment and its potential impact:

FMC estimates $15-$20 million of direct incremental costs in 2025 due to recent tariffs, with the impact varying by region and tariff type. The company is considering drawback eligibility and exemptions to mitigate these costs.

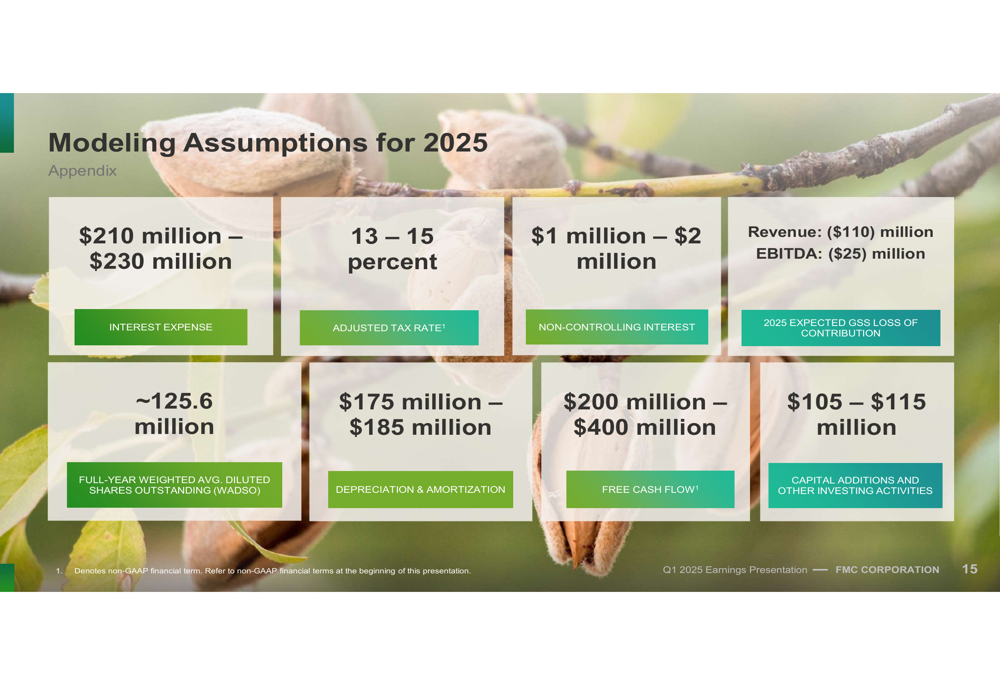

Modeling Assumptions

For investors and analysts modeling FMC’s performance, the company provided the following assumptions for 2025:

Key assumptions include interest expense of $210-$230 million, an adjusted tax rate of 13-15%, and depreciation and amortization of $175-$185 million.

In conclusion, while FMC faced significant challenges in Q1 2025, the company remains confident in its ability to improve performance in the second half of the year through strategic initiatives focused on inventory alignment, product strategy, and market expansion. Investors will be closely watching Q2 results for signs of the anticipated recovery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.