Asia stocks surge as tech extends rebound, Dec rate cut bets grow

Introduction & Market Context

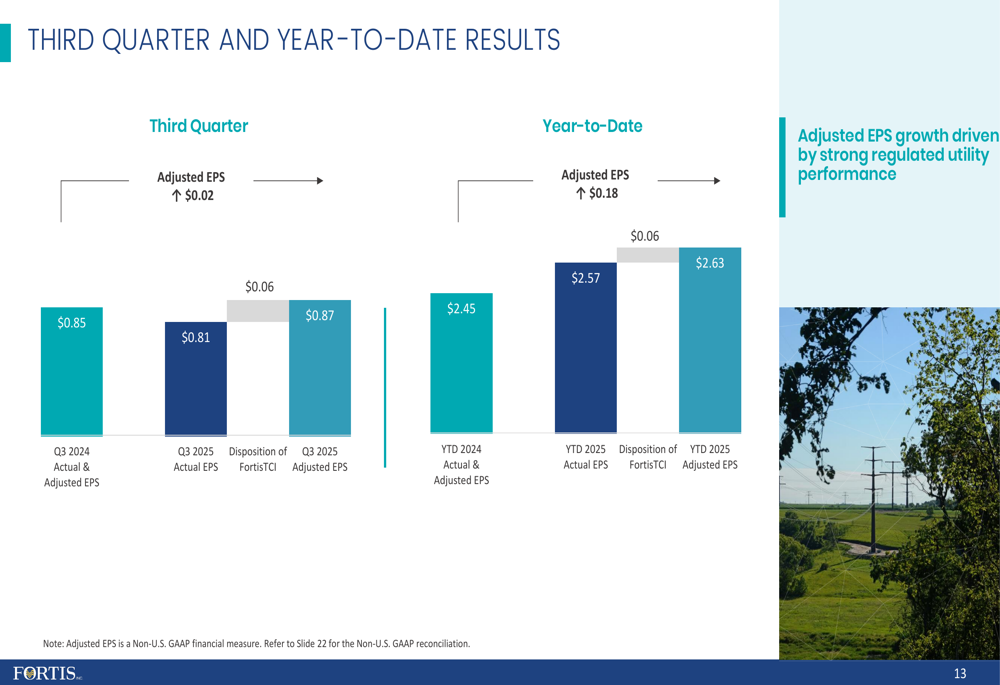

Fortis Inc (NYSE:FTS) reported its third quarter 2025 earnings on November 4, beating analyst expectations with an adjusted EPS of $0.87, compared to $0.85 in the same period last year. The company's strong performance was accompanied by the announcement of its largest-ever five-year capital plan of $28.8 billion for 2026-2030, aimed at driving a 7% compound annual growth rate in its rate base.

Despite the earnings beat, Fortis shares declined 2.21% in pre-market trading to $48.71, as revenue fell short of expectations at $2.07 billion against a forecast of $2.2 billion. The stock has been trading near its 52-week range of $40.32 to $52.47, reflecting broader market volatility in the utility sector.

Quarterly Performance Highlights

Fortis delivered adjusted earnings per share of $0.87 for Q3 2025, representing a 2.4% increase from $0.85 in Q3 2024. Year-to-date adjusted EPS reached $2.63, up 7.3% from $2.45 in the comparable period of 2024. The company also reported actual EPS of $0.81 for the quarter, with the difference primarily attributed to the disposition of FortisTCI.

As shown in the following quarterly results breakdown:

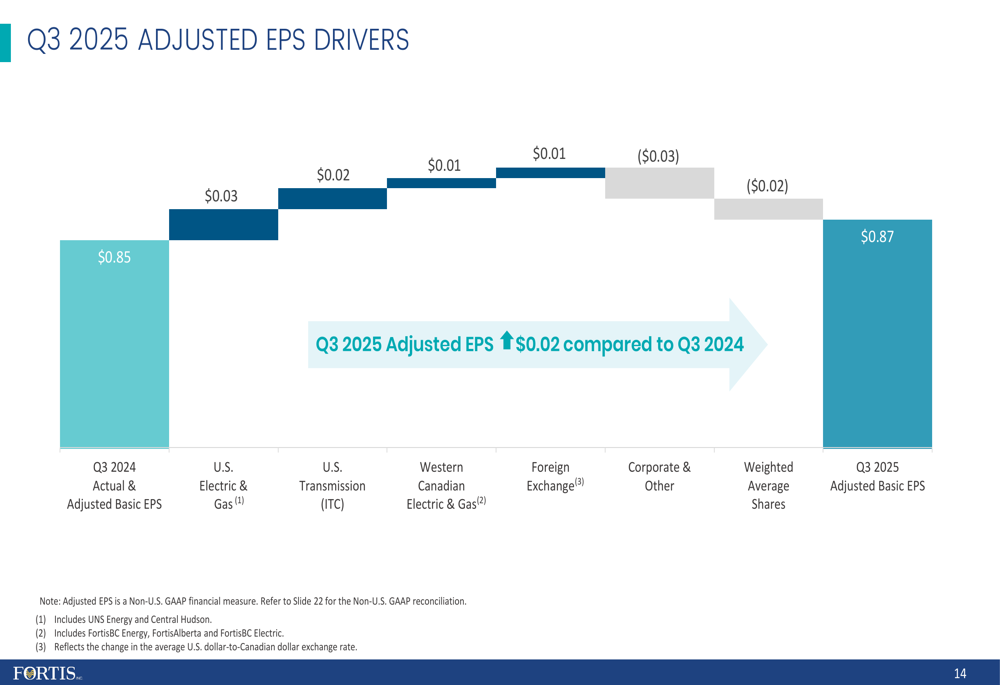

The quarterly performance improvement was driven by several factors, with U.S. Electric & Gas operations contributing the largest gain. A detailed analysis of the adjusted EPS drivers reveals the positive impact from U.S. operations and foreign exchange, partially offset by increased corporate expenses and dilution from additional shares:

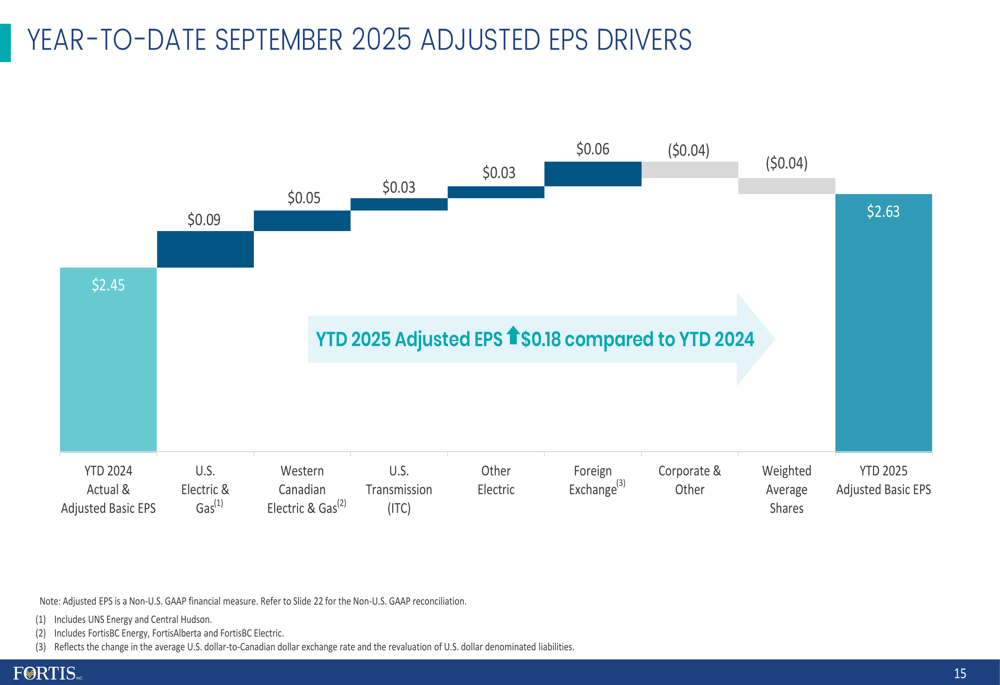

Year-to-date performance shows similar trends, with significant contributions from U.S. Electric & Gas and favorable foreign exchange impacts:

Capital Plan & Growth Strategy

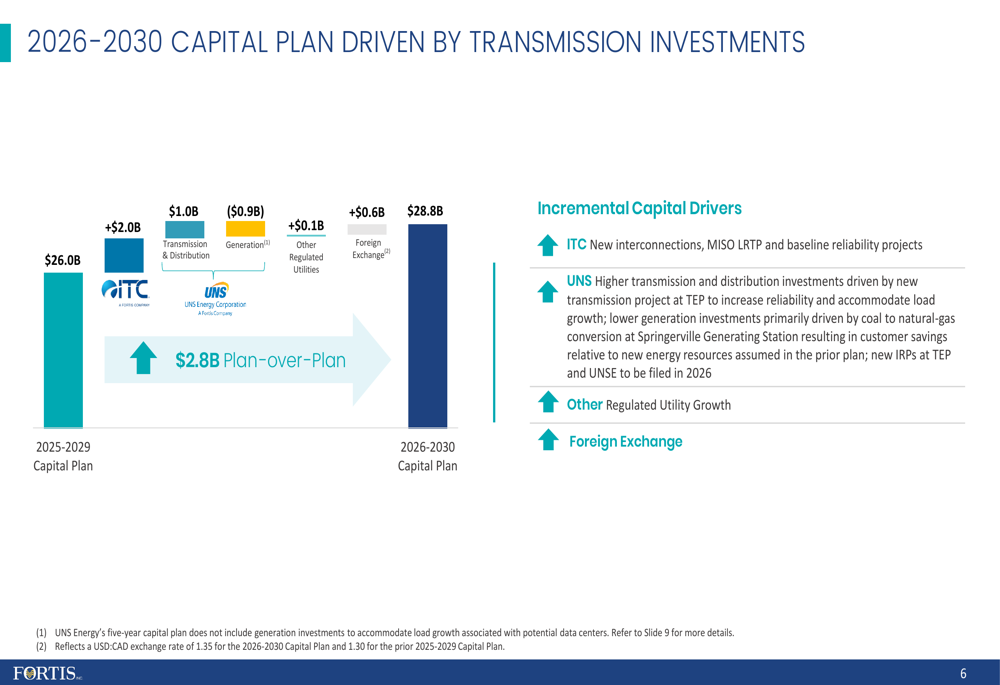

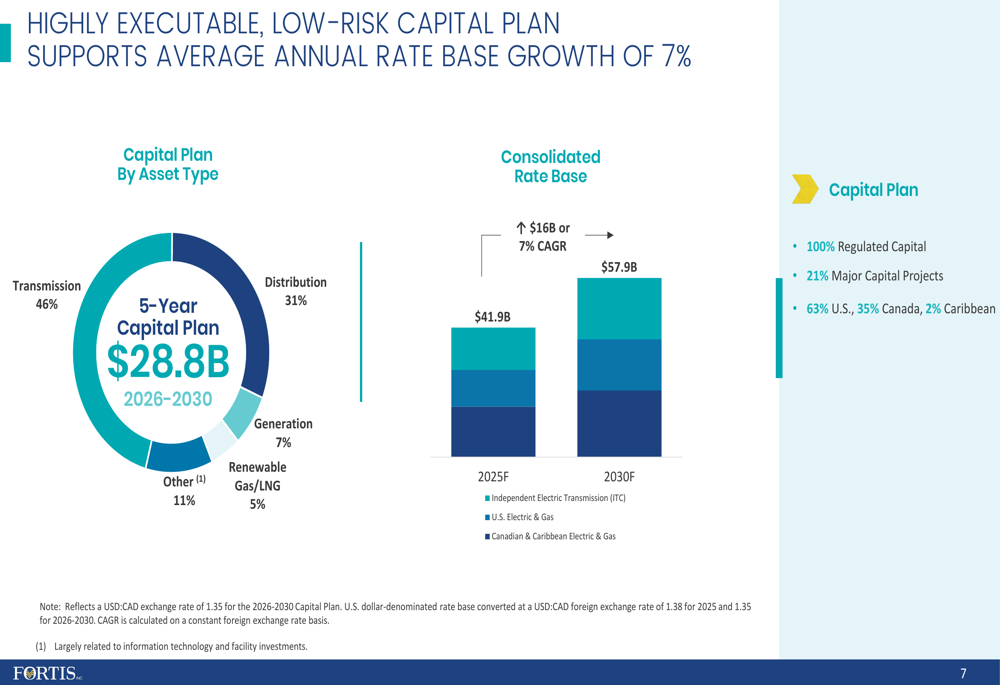

The centerpiece of Fortis' presentation was its new $28.8 billion five-year capital plan for 2026-2030, representing an increase of $2.8 billion over the previous plan. This record investment is expected to drive a 7% compound annual growth rate in rate base through 2030, which is 50 basis points higher than the prior plan's growth rate.

The company provided a clear breakdown of the capital plan changes, highlighting the significant increase in transmission and distribution investments:

Fortis emphasized that the capital plan is highly executable and low-risk, with 100% regulated investments. The plan is heavily weighted toward transmission (46%) and distribution (31%) assets, with the remainder allocated to generation and other investments. This focus on regulated transmission and distribution assets is designed to provide stable, predictable returns while supporting grid reliability and clean energy transition.

The following chart illustrates how the capital plan is expected to drive rate base growth from $41.9 billion in 2025 to $57.9 billion by 2030:

Strategic Initiatives

Fortis' growth strategy centers on three key subsidiaries with significant investment opportunities:

1. ITC (Independent Transmission Company) - A $9.8 billion capital plan supporting approximately 8% rate base CAGR, with significant investments in MISO Long Range Transmission Planning (LRTP) projects and customer connections.

2. UNS Energy - A $5.6 billion capital plan supporting approximately 7% rate base CAGR, with potential upside from retail load growth, particularly from data centers. The company noted negotiations for 300 MW of contracted load with potential to expand to 1,100-1,300 MW across multiple sites.

3. FortisBC - A $4.9 billion capital plan supporting approximately 6% rate base CAGR, with a focus on natural gas infrastructure reliability, LNG projects, and renewable gases.

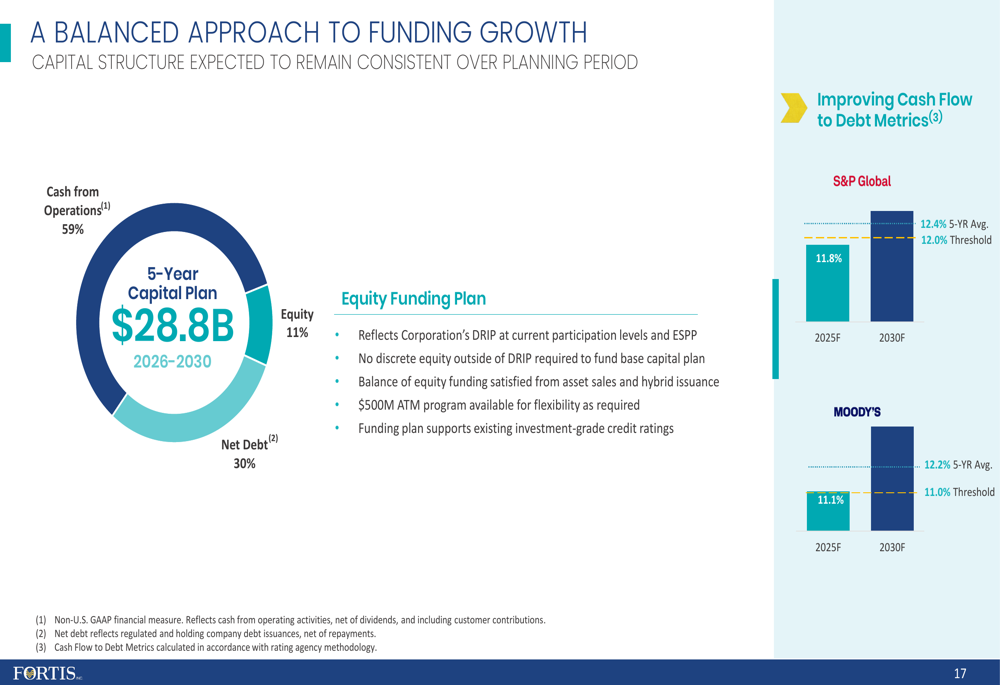

The company's approach to funding this growth remains balanced, with 59% expected to come from cash from operations, 30% from net debt, and 11% from equity:

Dividend Growth & Shareholder Returns

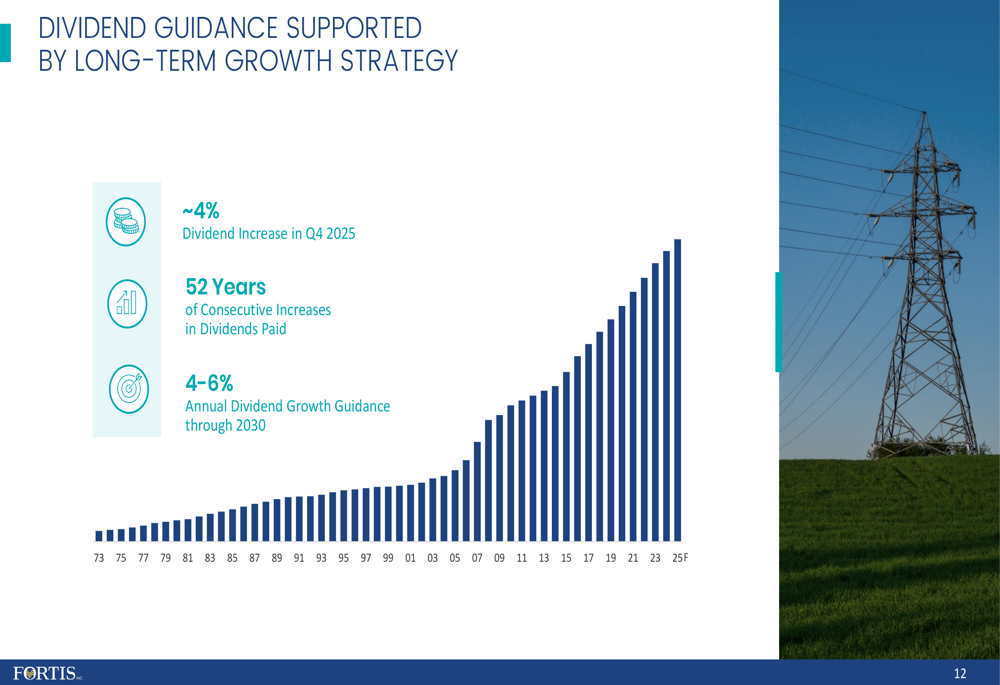

Fortis announced a dividend increase of approximately 4% for Q4 2025, marking the 52nd consecutive year of dividend increases. The company also extended its 4-6% annual dividend growth guidance through 2030, reinforcing its commitment to delivering consistent shareholder returns.

The following chart demonstrates Fortis' impressive history of dividend growth:

Forward-Looking Statements

Looking beyond the current capital plan, Fortis identified several opportunities for additional growth. At ITC, these include MISO LRTP Tranche 2.1 projects worth $3.3-3.8 billion post-2030 and potential for over 8,000 MW of customer load connections. UNS Energy has opportunities related to data center load growth, while FortisBC has potential LNG expansion projects.

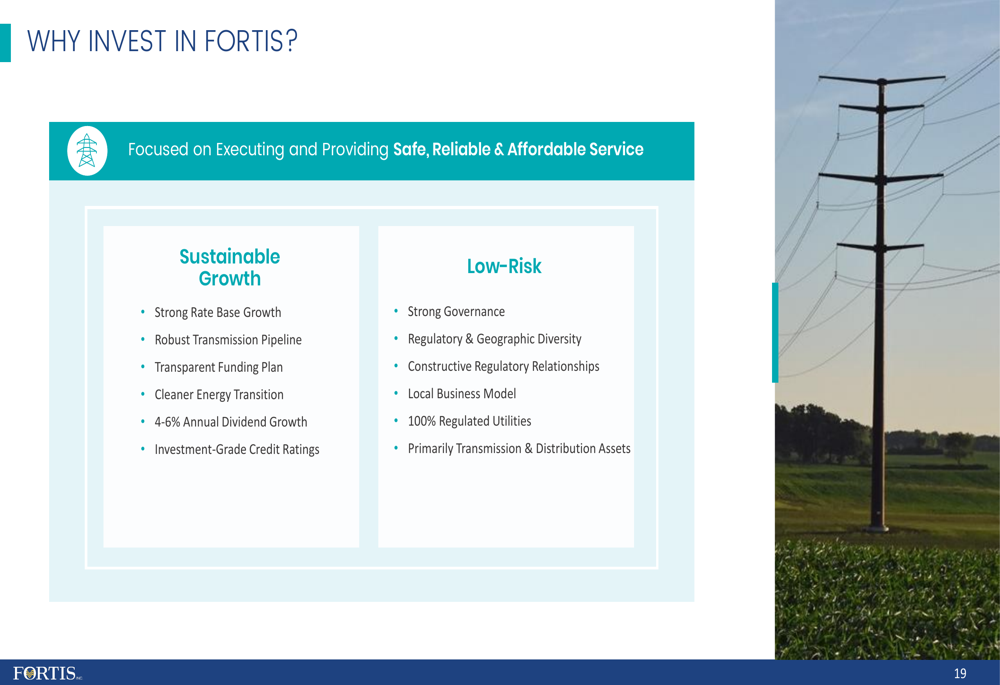

The company summarized its investment thesis, highlighting its focus on sustainable growth through strong rate base expansion, robust transmission pipeline, and 4-6% annual dividend growth, all supported by a low-risk business model:

Analyst Perspectives

During the earnings call, analysts focused on the timing of data center load growth, which Fortis management indicated would primarily impact the 2028-2030 timeframe. Questions also centered on potential generation investments contingent on customer agreements and the company's approach to hybrid debt issuances for funding future growth.

Despite the positive earnings surprise and ambitious capital plan, the revenue miss has tempered some investor enthusiasm. The stock's pre-market decline suggests that while the long-term growth strategy appears solid, near-term challenges including regulatory changes, supply chain disruptions, and economic conditions affecting utility demand remain concerns for investors.

As Fortis continues to execute on its regulated growth strategy with a focus on transmission and distribution assets, the company's ability to deliver on its ambitious capital plan while maintaining affordable customer rates will be key to future performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.