BTC Development Corp. completes $253 million IPO on NASDAQ

Introduction & Market Context

Forward Air Corporation (NASDAQ:FWRD) presented its first quarter 2025 earnings results on May 7, showing sequential margin improvement despite ongoing revenue challenges. The logistics provider, which completed its merger with Omni Logistics in late 2023, reported modest gains in profitability metrics while continuing to navigate a difficult freight environment.

The company’s stock closed at $16.75 on Wednesday, up 2.87% for the regular trading session, though it dipped slightly by 0.7% in aftermarket trading. Forward Air’s share price remains significantly below its 52-week high of $40.92, reflecting ongoing investor concerns about the company’s high leverage and integration challenges following the Omni acquisition.

Quarterly Performance Highlights

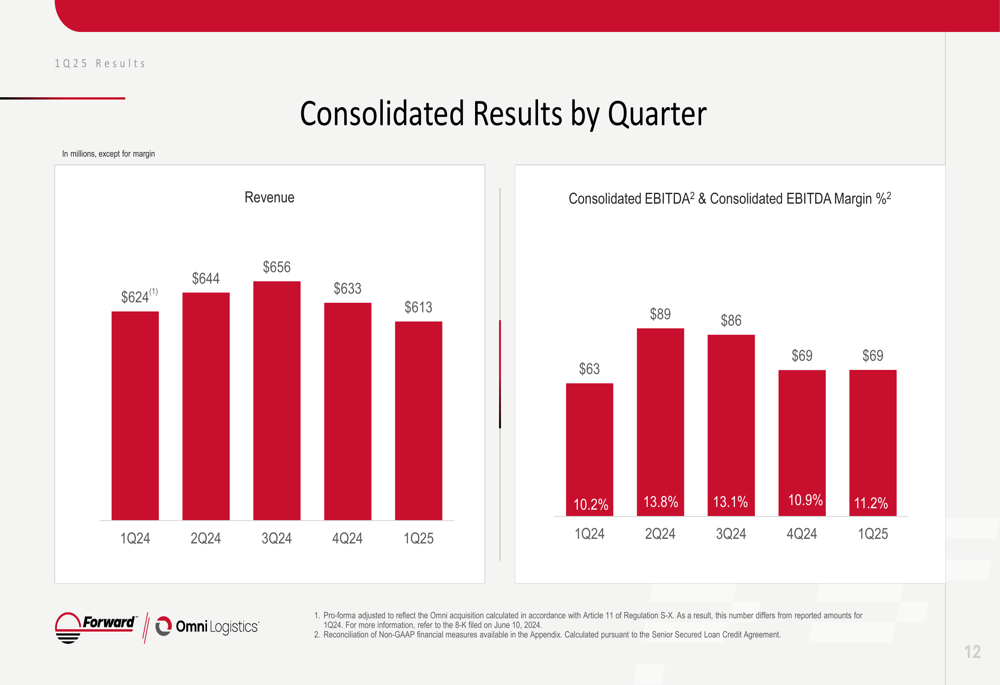

Forward Air reported first quarter revenue of $613 million, down from $633 million in the previous quarter and $624 million in the same period last year. Despite the revenue decline, the company achieved consolidated EBITDA of $69 million with an 11.2% margin, representing a slight improvement from the 10.9% margin in Q4 2024.

As shown in the following quarterly performance summary:

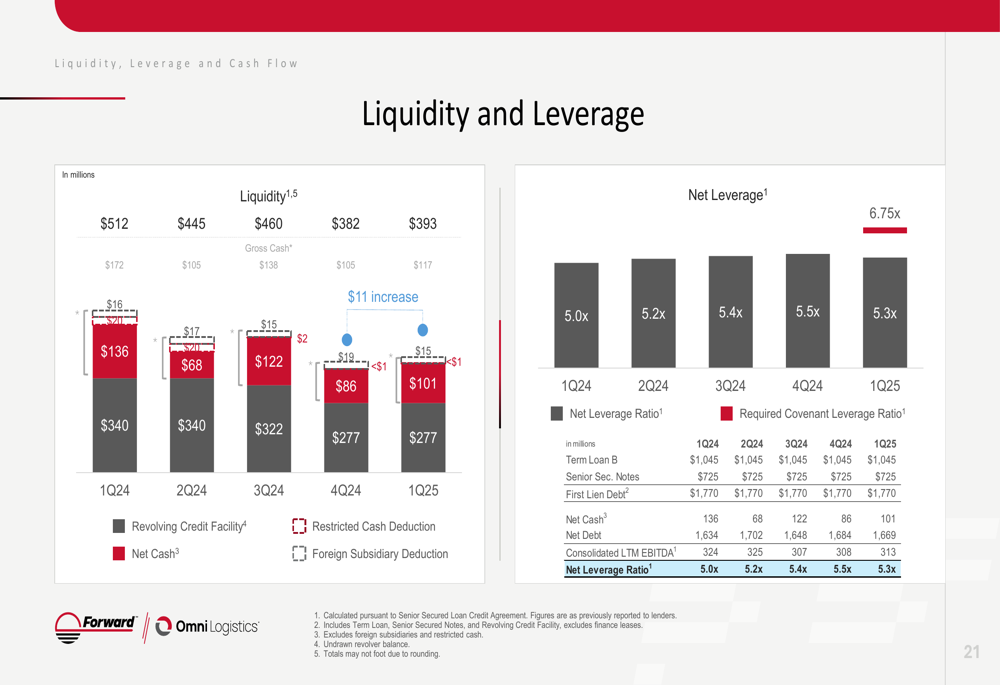

Operating income for the quarter was $5 million, while liquidity stood at $393 million. The company’s last twelve months (LTM) net leverage ratio improved slightly to 5.3x from 5.5x in the previous quarter, though it remains elevated compared to industry peers.

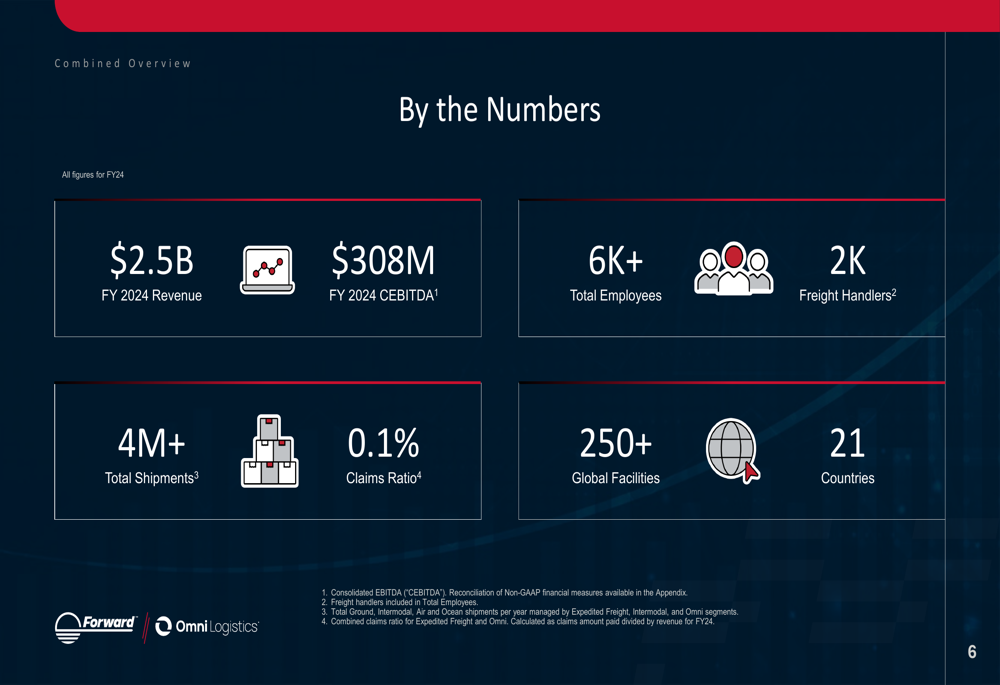

The company highlighted its key operational metrics for the combined entity, which now generates approximately $2.5 billion in annual revenue with over 4 million total shipments and operations spanning 21 countries:

Segment Performance Analysis

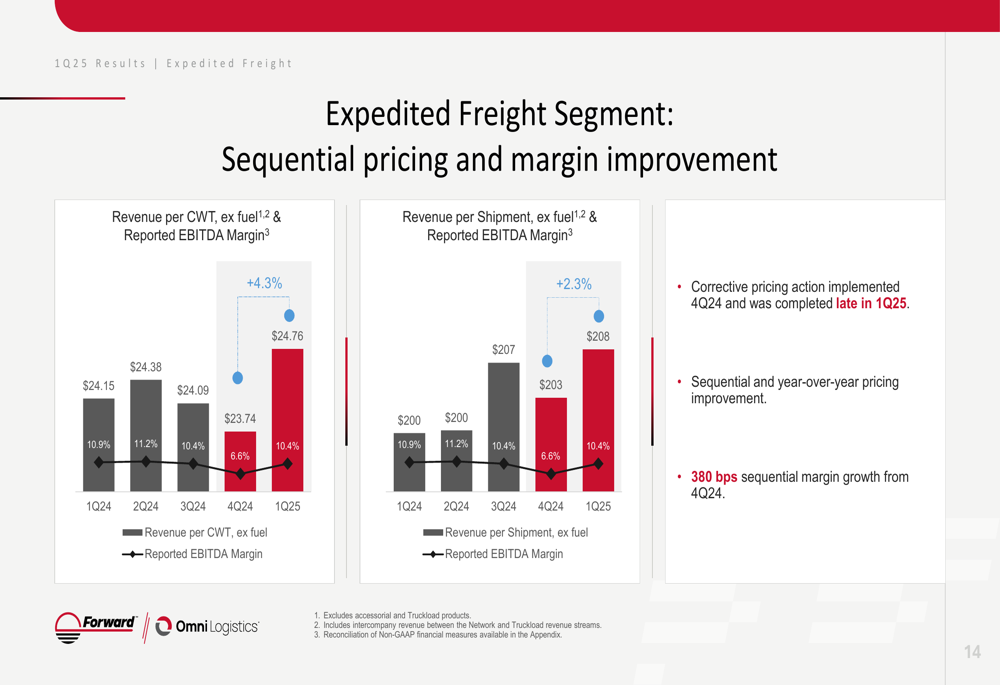

Forward Air’s Expedited Freight segment, which accounts for approximately 40% of total revenue, showed notable margin improvement despite revenue challenges. The segment generated $249 million in revenue for Q1 2025, down from $266 million in Q4 2024, but improved its EBITDA margin from 6.6% to 10.4% sequentially.

The margin improvement was driven by corrective pricing actions and operational efficiencies, as illustrated in the following chart:

The Expedited Freight segment maintained its industry-leading claims ratio of approximately 0.1%, providing superior service to 96% of all continental United States zip codes while focusing on customer service during the ongoing integration.

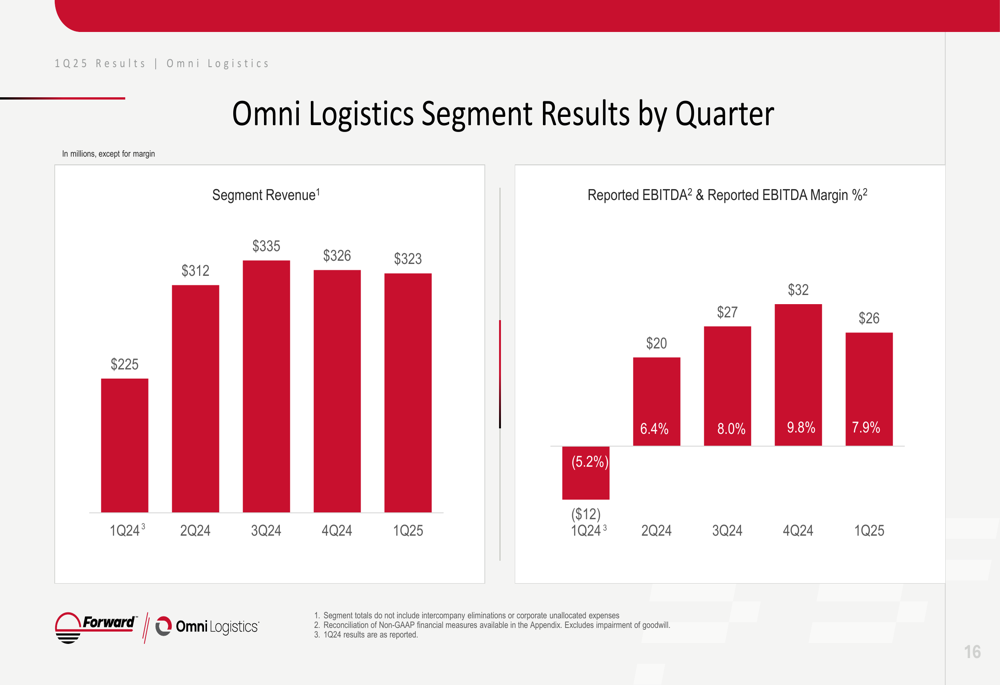

The Omni Logistics segment, which now represents the largest portion of Forward Air’s business at approximately 53% of revenue, reported $323 million in revenue with an EBITDA margin of 7.9%. This represents a slight decline from the 9.8% margin achieved in Q4 2024:

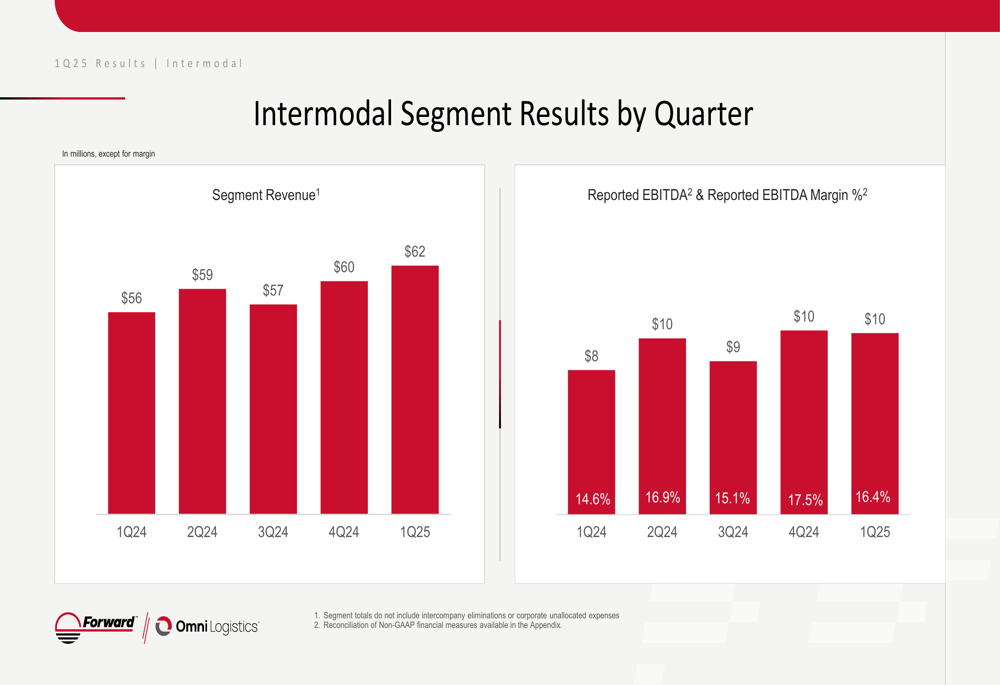

Meanwhile, the Intermodal segment continued to deliver the highest margins in the company’s portfolio, with $62 million in revenue and a 16.4% EBITDA margin:

Cash Flow and Liquidity

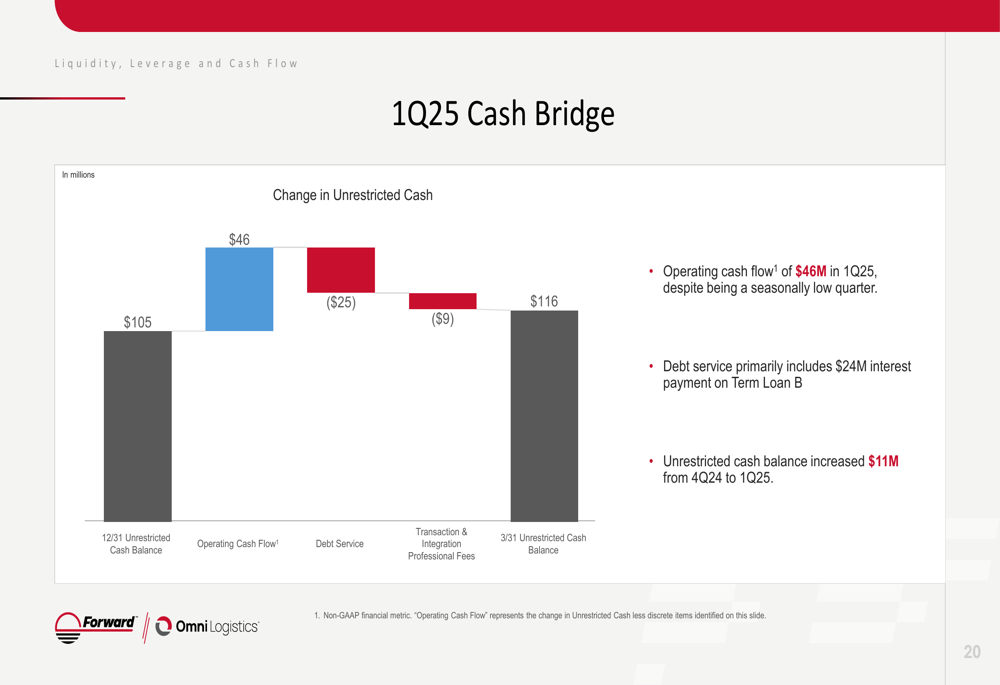

A key positive development in the quarter was Forward Air’s ability to generate positive cash flow despite seasonal headwinds. The company reported $11 million in positive cash flow for Q1 2025, a significant improvement from the $32 million cash outflow in Q4 2024.

Operating cash flow was particularly strong at $46 million, as illustrated in the following cash bridge:

The company’s liquidity position improved to $393 million, up from $382 million at the end of Q4 2024, while its net leverage ratio decreased slightly to 5.3x:

Forward Air emphasized its favorable debt maturity profile, with no significant maturities over the next five years. The company’s debt consists primarily of a $1.045 billion Term Loan B and $725 million in Senior Secured Notes.

Strategic Initiatives and Outlook

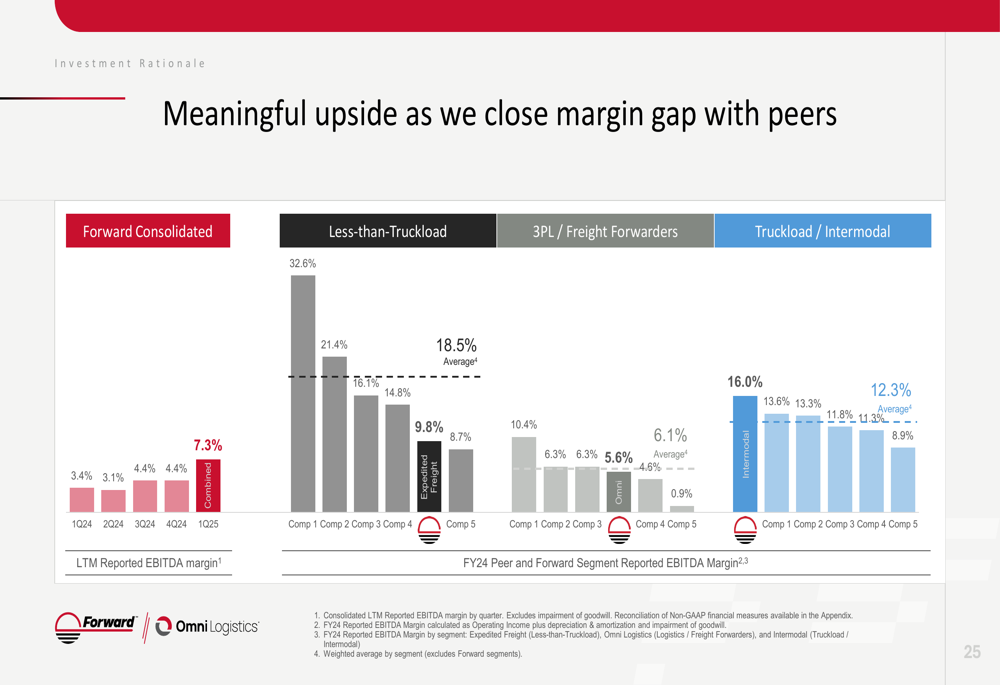

Forward Air highlighted its progress on integration synergies, reporting that it has realized over $100 million in annualized cost savings. The company’s strategic focus remains on closing the margin gap with industry peers, suggesting significant upside potential:

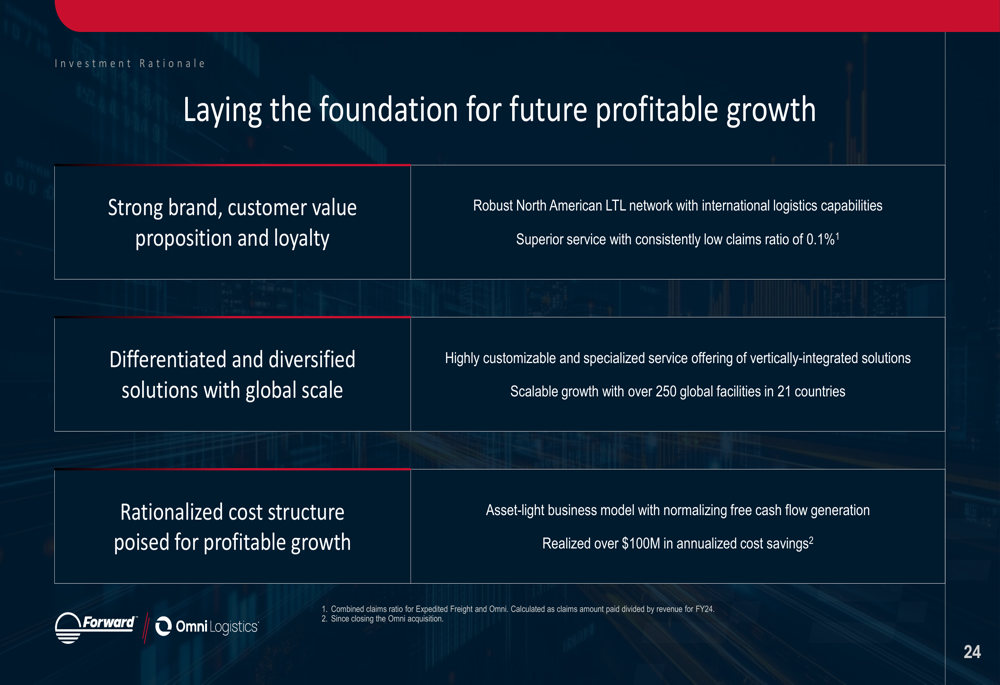

The company’s investment rationale emphasizes its strong brand position, differentiated and diversified solutions with global scale, and rationalized cost structure poised for profitable growth:

Forward Air’s product portfolio is now more diversified following the Omni Logistics acquisition, with Ground Transportation accounting for approximately 70% of revenue, Air & Ocean Forwarding for 12%, and Intermodal Drayage and Warehousing/Value-Added Services each contributing about 9%:

Looking ahead, management expressed confidence in continued margin improvement and cash flow generation as integration efforts progress. The company expects to benefit from its global footprint, with operations in 21 countries, though 88% of revenue still comes from the United States.

While Forward Air faces ongoing challenges including high leverage and a difficult freight environment, its Q1 2025 results suggest the company is making incremental progress on its post-merger integration and financial stabilization efforts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.