Senate Republicans to challenge auto safety mandates in January - WSJ

Introduction & Market Context

Forward Air Corporation (NASDAQ:FWRD) presented its third quarter 2025 earnings results on November 5, 2025, highlighting operational stability despite ongoing challenges in the freight market. The logistics provider, which completed its integration with Omni Logistics, reported consistent EBITDA performance while focusing on margin improvement and cash generation.

The company's stock has faced significant pressure this year, trading at $18.14 at market close on the day of the earnings release, down 43% year-to-date and well below its 52-week high of $39.89. In aftermarket trading, the stock declined an additional 2.48%, reflecting continued investor caution despite the company's operational improvements.

Quarterly Performance Highlights

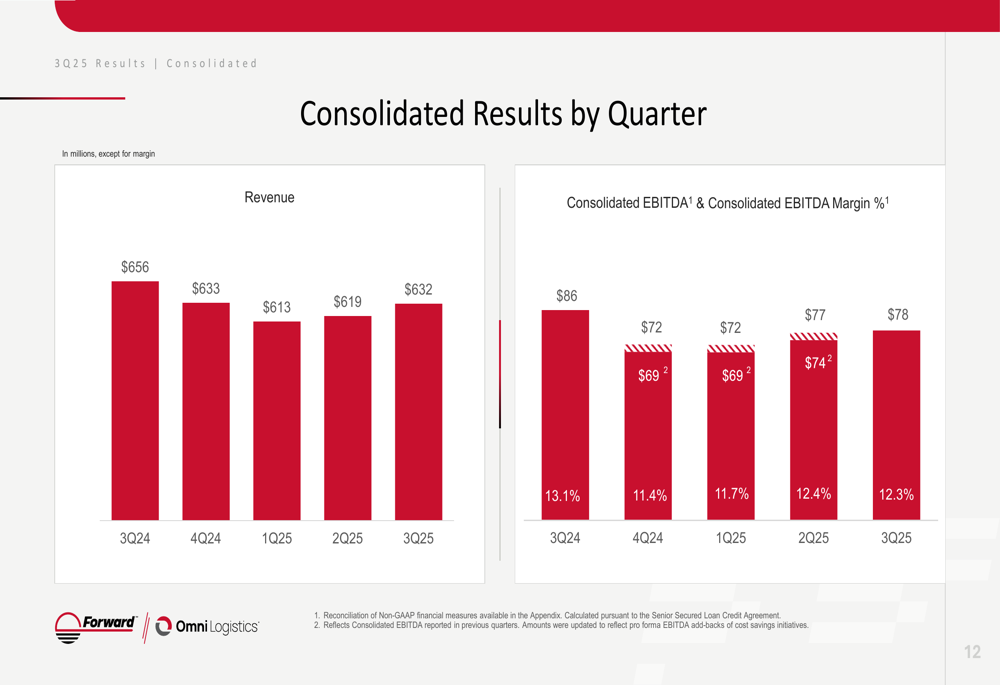

Forward Air reported Q3 2025 revenue of $632 million with consolidated EBITDA of $78 million, representing a 12.3% margin. Operating income reached $15 million for the quarter. The company has maintained EBITDA stability compared to the previous quarter while improving operating cash flow by $27 million sequentially.

As shown in the following financial highlights slide:

The company's performance reflects its efforts to enhance profitability amid challenging market conditions. Forward Air's consolidated quarterly results show revenue stabilizing after several quarters of decline, with Q3 2025 revenue slightly increasing from Q2 2025:

Segment Performance Analysis

Forward Air operates through three primary segments: Expedited Freight, Omni Logistics, and Intermodal. Each segment showed distinct performance trends in Q3 2025.

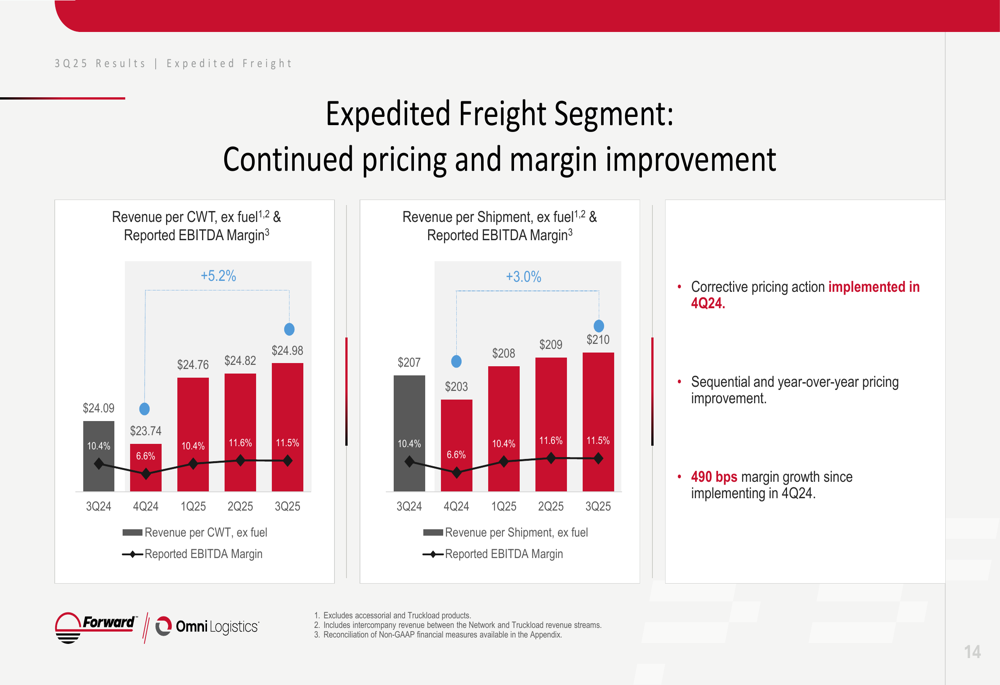

The Expedited Freight segment reported revenue of $259 million, a 9.2% decrease compared to Q3 2024. However, the segment achieved margin improvement, with EBITDA margin increasing from 10.4% to 11.5% year-over-year. This improvement reflects the company's focus on pricing discipline and operational efficiency.

The segment's pricing strategy has shown positive results, as illustrated in the following chart:

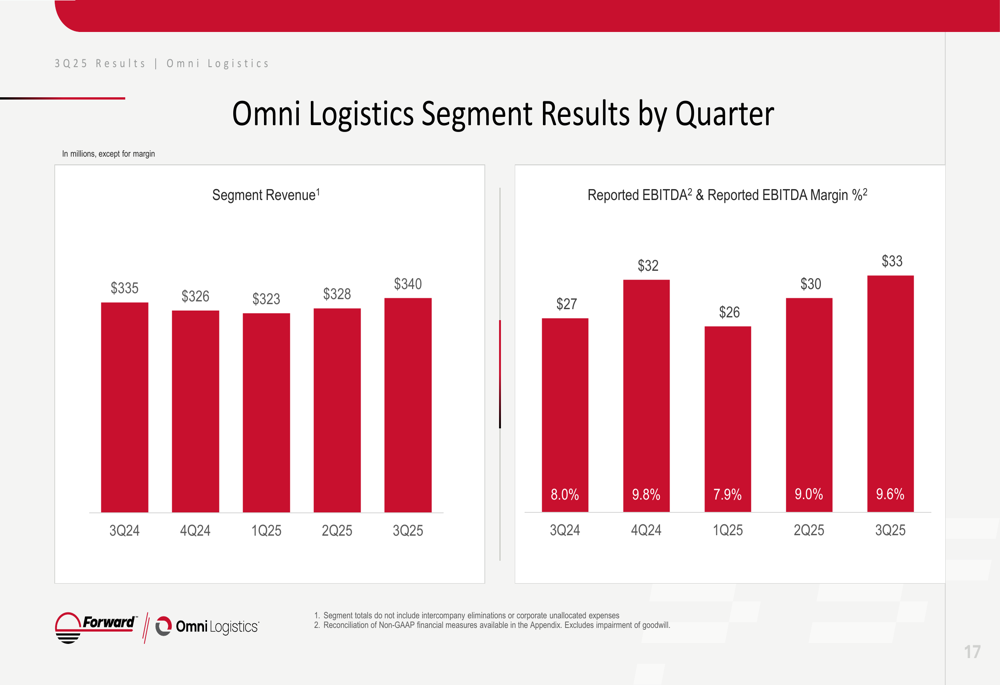

The Omni Logistics segment delivered the strongest performance, with revenue increasing 1.5% year-over-year to $340 million. More impressively, operating income surged 758.2% compared to Q3 2024, while EBITDA margin improved from 8.0% to 9.6%. This segment's quarterly performance is shown below:

The Intermodal segment reported modest revenue growth of 1.6% year-over-year to $58 million, though its EBITDA margin declined slightly from 15.1% to 14.5%.

Cash Flow and Liquidity Position

A key highlight of Forward Air's Q3 2025 results was its improved cash generation. Operating cash flow reached $79 million for the quarter and $176 million year-to-date, demonstrating the resilience of the company's asset-light business model even during what management described as a "freight recession."

The following chart illustrates the company's cash flow performance:

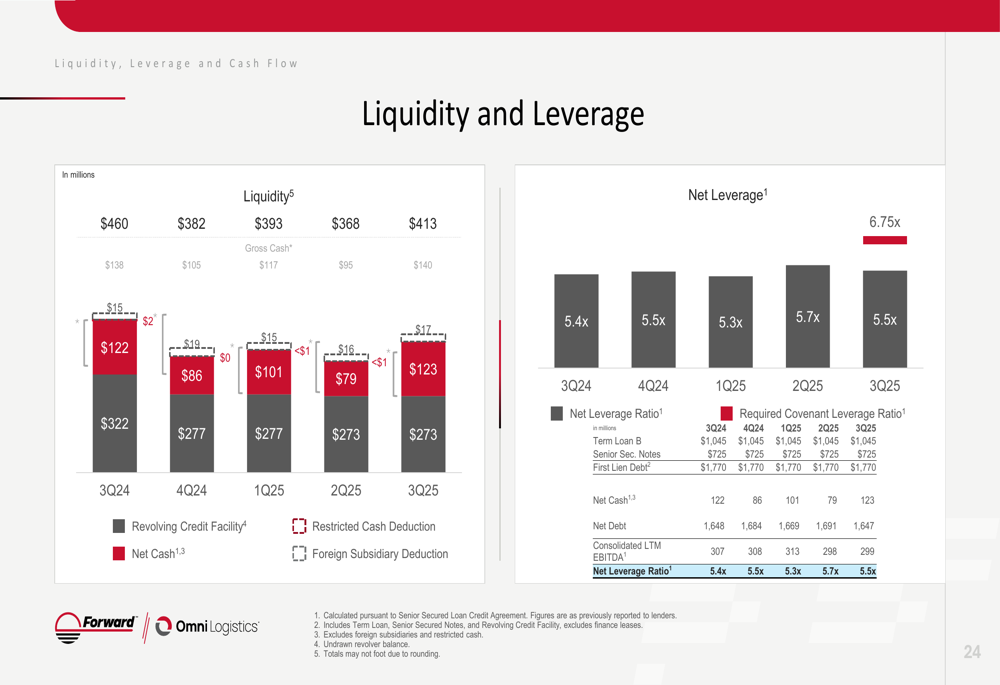

Forward Air reported total liquidity of $413 million, comprising $140 million in unrestricted cash and $273 million in revolver availability. The company's cash position improved by $45 million from Q2 2025 to Q3 2025.

Despite the improved cash position, Forward Air's leverage remains elevated at 5.5x net leverage ratio. However, the company highlighted its favorable debt maturity profile with no maturities over the next five years, as its first lien term loan matures in 2030 ($300 million) and senior secured notes in 2031 ($725 million).

The company's current liquidity and leverage position is detailed below:

Strategic Initiatives and Outlook

Forward Air emphasized its transformation into a global logistics provider following the integration with Omni Logistics. The combined entity now operates over 250 facilities across 21 countries, with approximately 12% of revenue generated outside the United States.

The company's diversified revenue streams are illustrated in the following breakdown:

Forward Air highlighted its differentiated market position, combining a robust North American LTL network with international logistics capabilities. The company maintains a consistently low claims ratio of approximately 0.1%, demonstrating its focus on service quality.

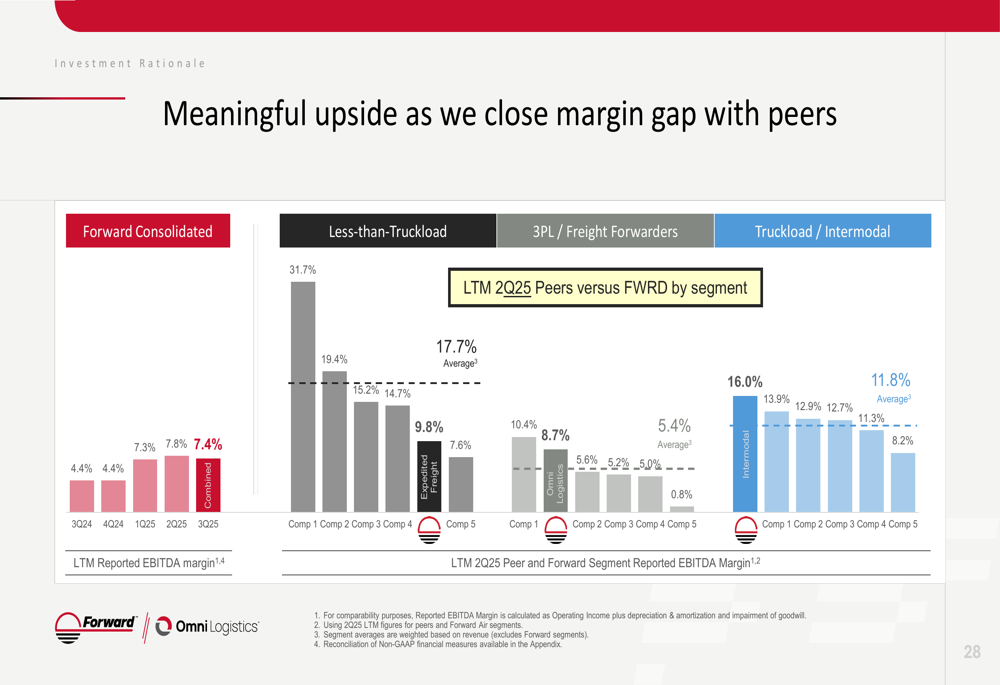

Management indicated that the company has realized over $100 million in annualized cost savings and is positioned for profitable growth as market conditions improve. The presentation also highlighted potential for margin expansion, as shown in the comparison with industry peers:

Market Response and Challenges

Despite operational improvements and strong cash generation, Forward Air continues to face investor skepticism, as evidenced by its stock performance. The company's high leverage ratio of 5.5x remains a concern, though management emphasized its focus on deleveraging through improved operational performance.

During the earnings call, CEO Shawn Stewart emphasized the company's flexible operational model, stating, "We are not a fixed-cost network. We're a variable-cost network." This adaptability is positioned as a key advantage as Forward Air navigates the current market landscape.

The freight environment remains challenging, with the ISM index below 50 for most of the past three years and reduced tonnage in the majority of recent months, according to the earnings call. These external pressures continue to impact Forward Air's performance despite its operational improvements.

Forward Air's Q3 2025 presentation reflects a company focused on operational stability and cash generation amid ongoing market challenges. While the company has made progress in improving margins and cash flow, its elevated leverage and stock performance indicate that investors remain cautious about its long-term trajectory in a difficult freight environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.