First Brands Group debt targeted by Apollo Global Management - report

Introduction & Market Context

Four Corners Property Trust (NYSE:FCPT) released its Q2 2025 investor presentation highlighting the company’s continued portfolio growth and conservative financial approach. The real estate investment trust, which specializes in restaurant, auto service, and medical retail properties, has maintained its disciplined acquisition strategy while navigating market volatility. Despite missing earnings estimates in Q1 2025, FCPT’s stock has shown resilience, trading at $26.14 as of July 29, 2025, up 1.26% for the day.

Growth and Portfolio Diversification

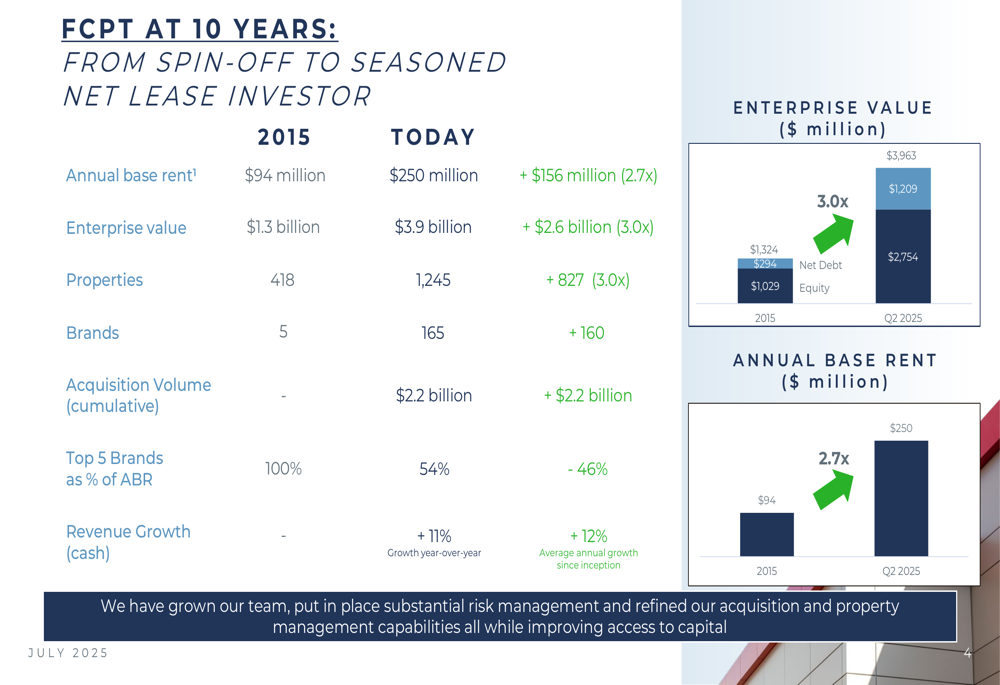

FCPT has demonstrated significant growth since its 2015 spin-off from Darden Restaurants (NYSE:DRI). The company has more than tripled its property count and enterprise value over the past decade, while substantially diversifying its tenant base beyond its original Darden-focused portfolio.

As shown in the following comparison of key metrics from 2015 to 2025:

The presentation highlights that annual base rent has increased from $94 million to $250 million (2.7x growth), while enterprise value has grown from $1.3 billion to $3.9 billion (3.0x growth). Property count has expanded from 418 to 1,245, and the company now works with 165 brands compared to just 5 at inception. Perhaps most notably, FCPT has reduced its concentration risk, with its top 5 brands now representing 54% of annual base rent, down from 100% at inception.

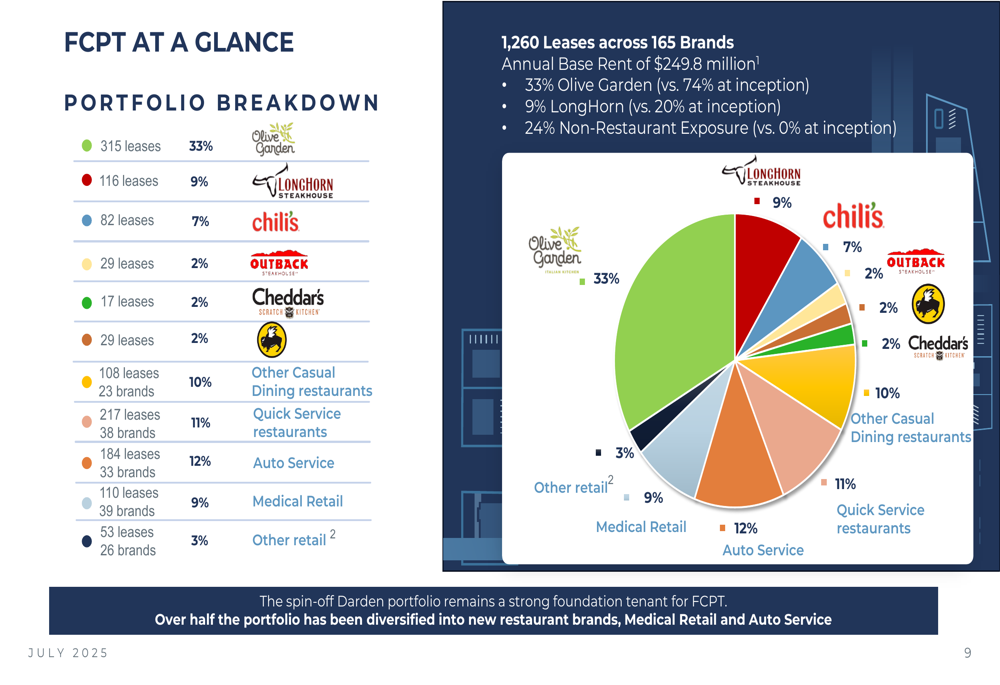

The company’s current portfolio breakdown shows continued diversification efforts, with Olive Garden representing 33% of annual base rent (down from 74% at inception) and non-restaurant exposure growing to 24% (up from 0% at inception):

Quarterly Performance Highlights

In Q2 2025, FCPT acquired $84 million in properties at a 6.7% cap rate, contributing to $344 million in acquisitions over the last twelve months at an average 6.9% cap rate. The company maintained strong occupancy at 99.4% with tenant EBITDAR coverage of 5.0x, demonstrating the quality of its tenant base.

The following snapshot provides a comprehensive overview of FCPT’s current operational and financial metrics:

These metrics reflect FCPT’s focus on maintaining a high-quality portfolio while pursuing growth. However, it’s worth noting that the company’s Q1 2025 results fell short of analyst expectations, with EPS of $0.26 missing the forecasted $0.28 and revenue of $63.5 million below the anticipated $66.31 million.

Financial Position and Strategy

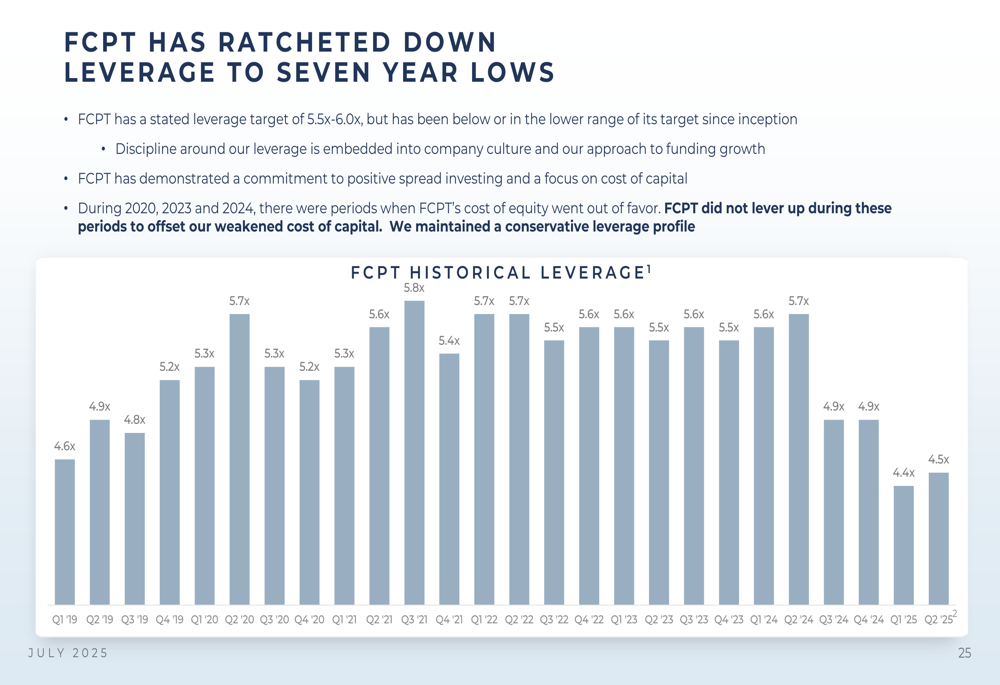

FCPT positions itself as "the calm port in the volatility storm," emphasizing its strong liquidity position and conservative financial approach. The company has over $500 million in liquidity, including a fully undrawn $350 million revolver, and has reduced its leverage to 4.5x net debt to adjusted EBITDAre, a seven-year low.

The presentation highlights FCPT’s defensive positioning in uncertain economic times:

This conservative approach extends to the company’s debt management, with 95% fixed-rate debt and no significant near-term maturities. FCPT has also been proactive in raising capital, with $206 million in unsettled forward equity as of June 30, 2025.

Detailed Financial Analysis

FCPT’s financial strategy centers on maintaining lower leverage compared to historical levels. The company has consistently reduced its leverage ratio over the past several years:

This conservative financial positioning provides flexibility for future acquisitions while minimizing risk in an uncertain economic environment. The company’s Q2 2025 AFFO per share was $0.44, though this figure should be considered in context with the Q1 earnings miss reported earlier.

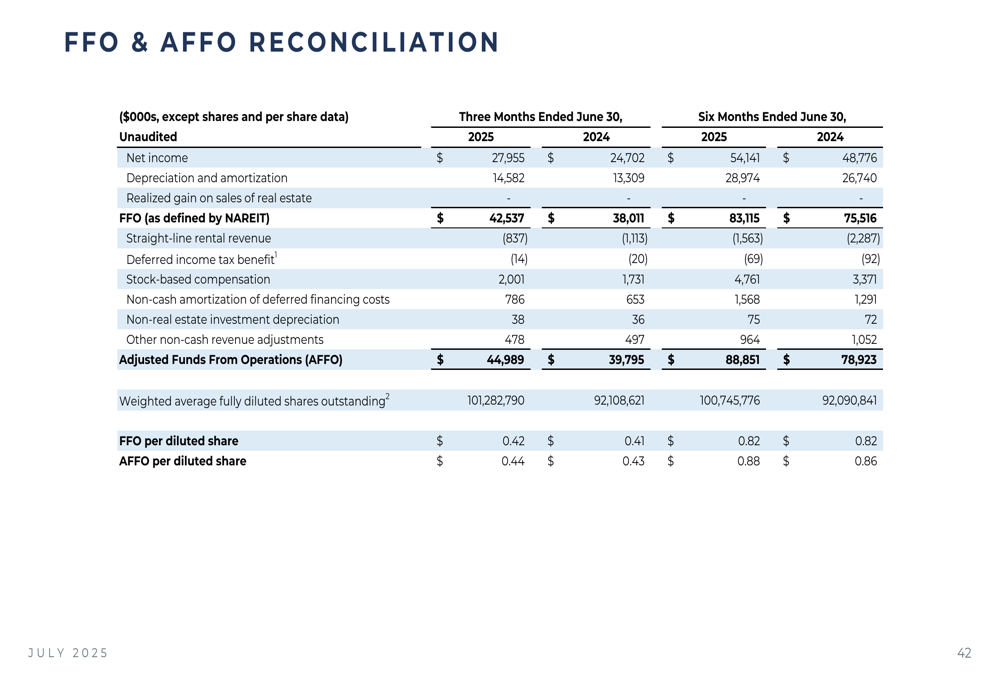

The company’s detailed financial reconciliations provide transparency into its performance metrics:

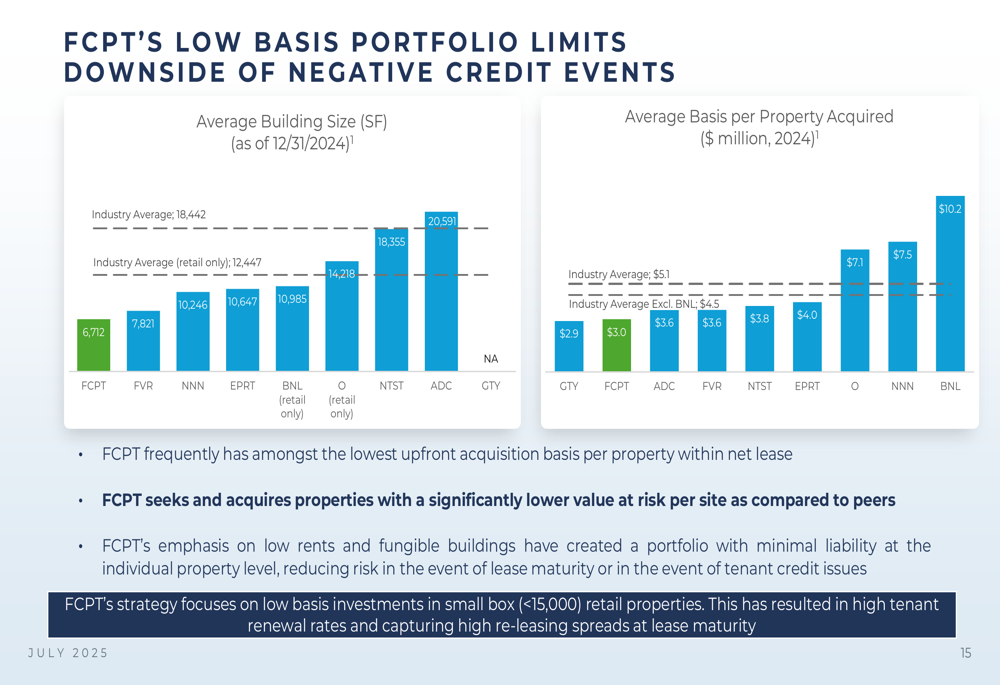

Competitive Industry Position

FCPT differentiates itself within the net lease REIT sector through its focus on smaller properties with lower acquisition costs. This approach is designed to limit downside risk from potential negative credit events.

As illustrated in the following comparison with industry peers:

FCPT’s average basis per property acquired ($3.0 million) is significantly lower than the industry average ($5.1 million), providing a competitive advantage in terms of risk management. Similarly, the company’s average building size of 6,561 square feet is well below the industry average of 18,442 square feet.

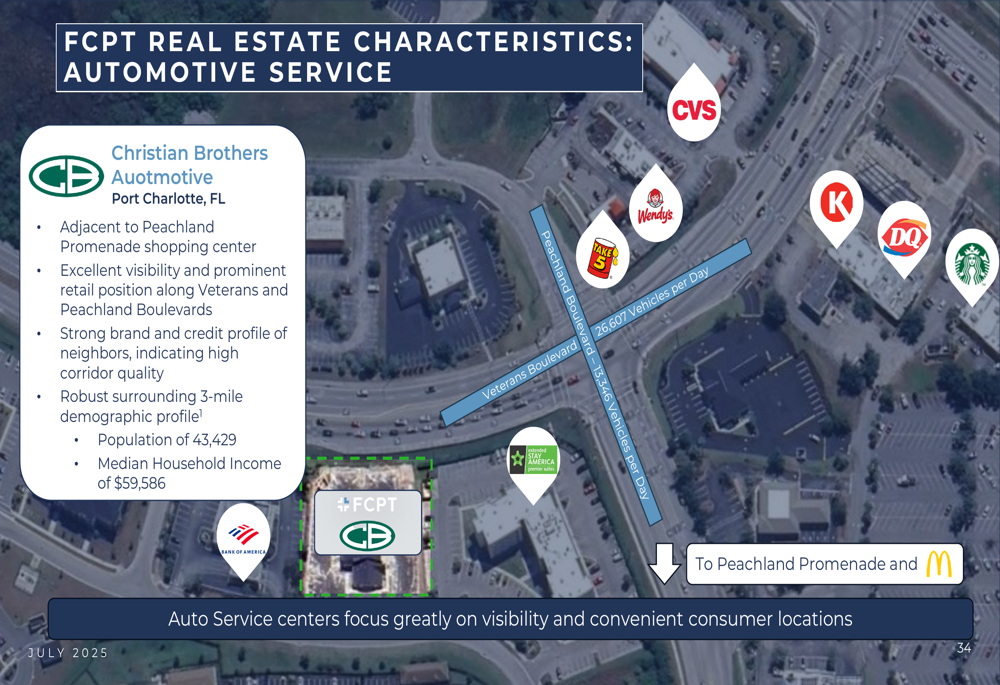

Strategic Initiatives

FCPT’s acquisition strategy focuses on three primary sectors: restaurants (76% of annual base rent), auto service (12%), and medical retail (9%). Within each sector, the company applies specific criteria to target high-quality properties with strong demographics and visibility.

The company’s real estate selection process is illustrated through examples like this Olive Garden property in Burlington (NYSE:BURL), NC:

Similarly, in the auto service sector, FCPT targets properties with strong visibility and demographic profiles:

These examples demonstrate FCPT’s focus on acquiring properties in high-traffic retail corridors with strong demographic characteristics, supporting the company’s thesis of investing in fungible real estate with national brand tenants.

Forward-Looking Statements

Looking ahead, FCPT plans to continue its disciplined acquisition approach while maintaining its conservative financial position. The company has emphasized its preparedness for potential economic uncertainties, with an executive quoted in the Q1 earnings call stating, "We love being very liquid when there’s stress in the streets."

While the presentation does not provide specific acquisition volume guidance for the remainder of 2025, it does indicate that the company expects cash G&A expenses to range between $18 million and $18.5 million for the year.

Conclusion

FCPT’s Q2 2025 investor presentation portrays a company focused on steady growth through disciplined acquisitions while maintaining a conservative financial approach. The company has successfully diversified its portfolio since its 2015 spin-off and positioned itself to weather potential economic volatility.

However, investors should consider the recent Q1 earnings miss alongside the positive narrative presented in the slides. While FCPT emphasizes its strong operational metrics and growth trajectory, the gap between expectations and actual performance in Q1 suggests potential challenges in meeting market forecasts.

With its focus on smaller, high-quality properties in recession-resistant sectors, FCPT appears well-positioned to continue its growth strategy while managing risk in an uncertain economic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.