Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Freehold Royalties Ltd . (TSX:FRU) presented its Q1 2025 corporate update on May 14, 2025, highlighting its expanding North American portfolio and focus on sustainable dividend returns. The company’s stock closed at $12.12 on May 13, 2025, up 1% for the day, and has traded between $10.53 and $14.62 over the past 52 weeks.

The presentation comes after Freehold reported stronger-than-expected Q4 2024 earnings of $0.33 per share, exceeding analyst forecasts by 37.8%, despite revenue coming in below expectations at $76.9 million. The company’s focus on high-margin royalty assets across both Canadian and US oil plays continues to support its attractive dividend yield.

Executive Summary

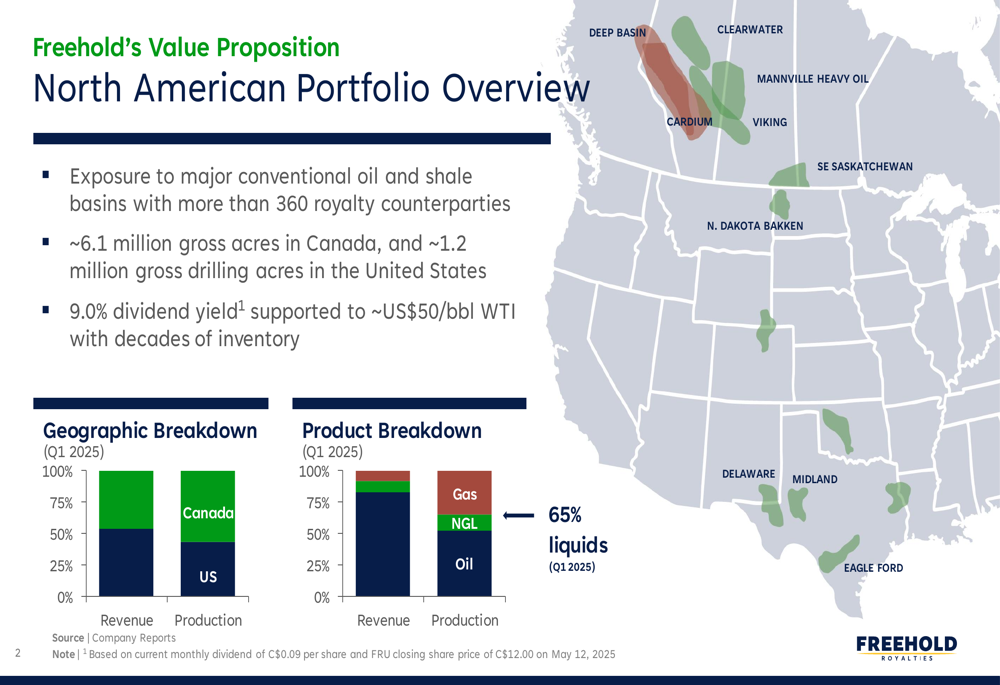

Freehold Royalties (OTC:FRHLF) has positioned itself as a unique North American royalty company with exposure to major conventional oil and shale basins across Canada and the United States. The company’s portfolio spans approximately 6.1 million gross acres in Canada and 1.2 million gross drilling acres in the US, providing diversification across multiple resource plays.

As shown in the following portfolio overview, Freehold’s revenue is increasingly weighted toward US assets, while production remains balanced between the two countries:

The company offers investors a compelling 9.0% dividend yield that management states is sustainable down to approximately US$50/bbl WTI oil prices. This dividend resilience is supported by a growing liquids-weighted production base and decades of development inventory across both countries.

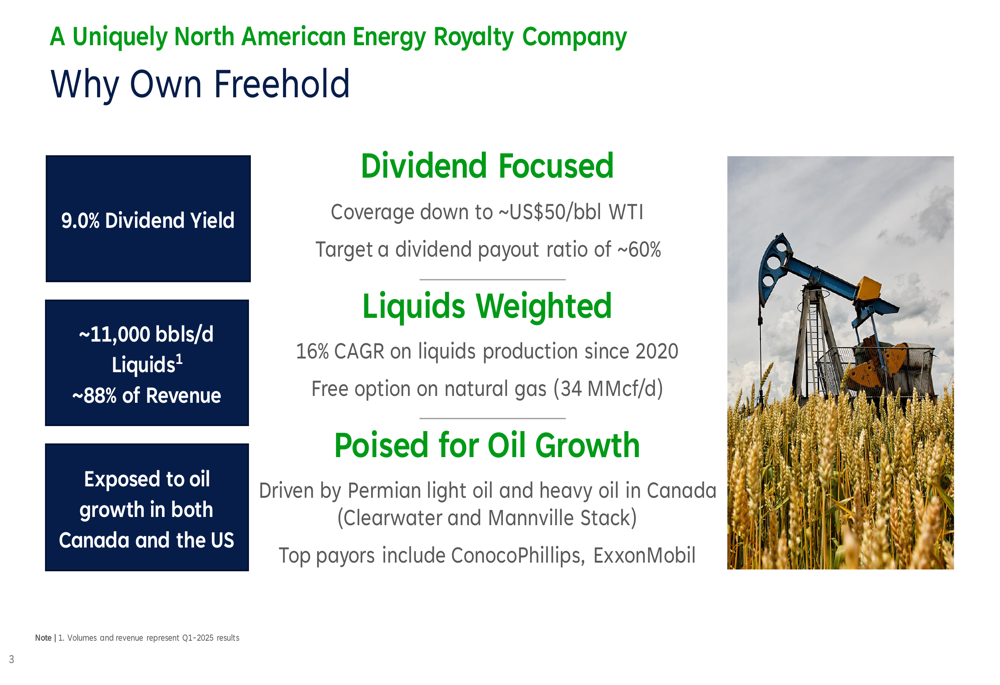

Freehold’s investment thesis centers on its high-margin business model, conservative balance sheet, and exposure to premium US oil pricing, as highlighted in the following slide:

Quarterly Performance Highlights

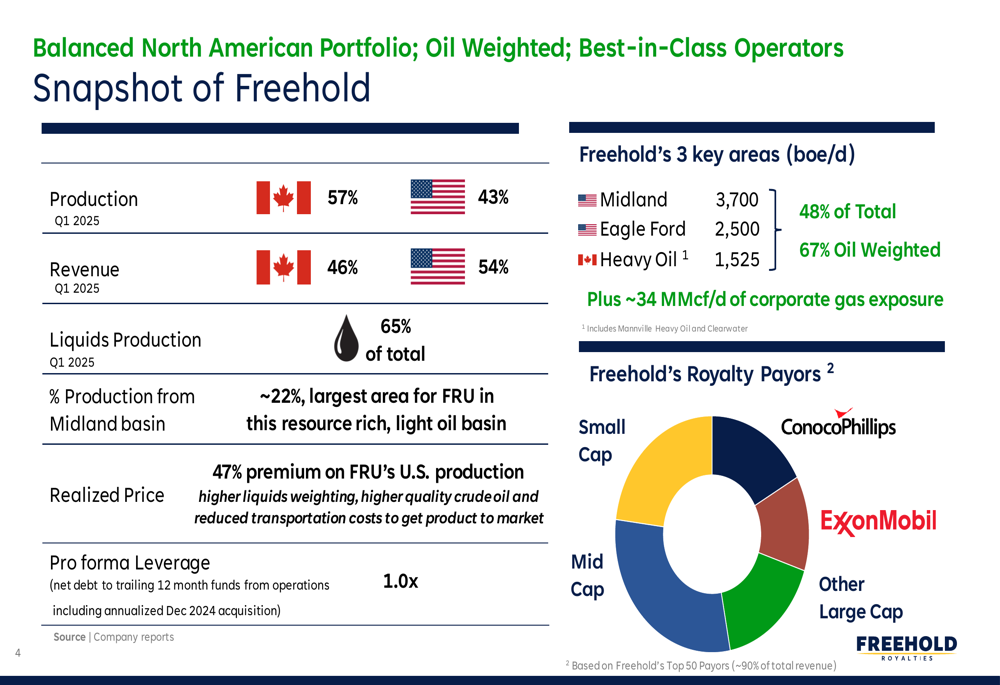

In Q1 2025, Freehold reported total production of 16,248 boe/d, with liquids (oil and NGLs) accounting for 65% of total production. The company’s production was split between Canada (57%) and the US (43%), while revenue showed a higher US contribution at 54% compared to 46% from Canadian assets.

The following snapshot provides a comprehensive view of Freehold’s key metrics and production breakdown by region:

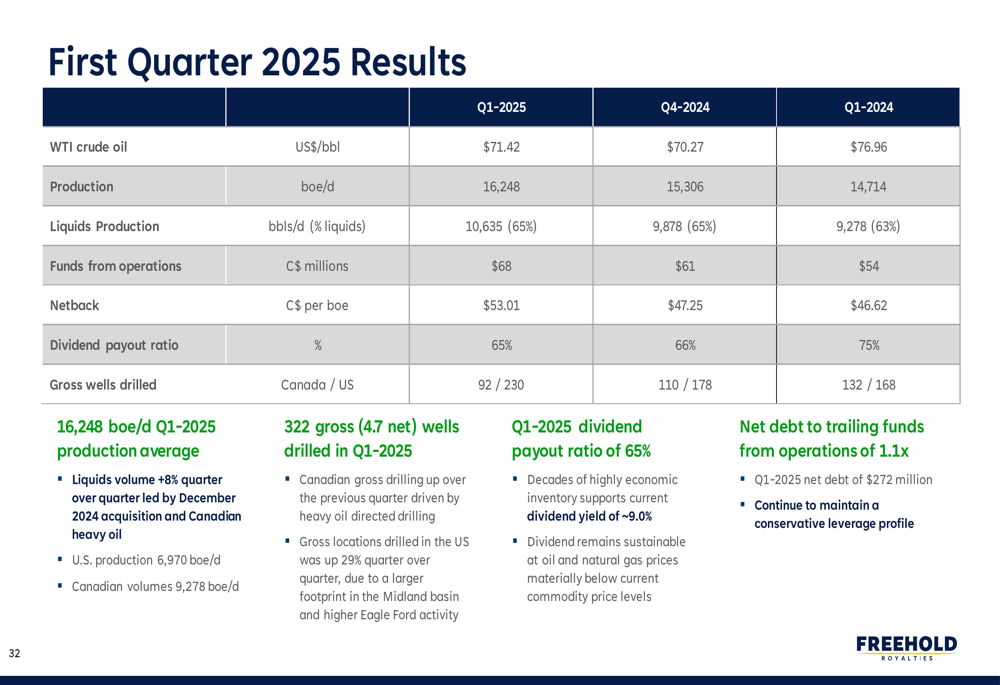

Q1 2025 results showed continued momentum, with liquids volumes increasing 8% quarter-over-quarter, driven by the December 2024 Midland Basin acquisition and growth in Canadian heavy oil production. The company maintained a dividend payout ratio of 65% in Q1, slightly above its target of 60%, while net debt stood at $272 million, representing a net debt to trailing funds from operations ratio of 1.1x.

The detailed quarterly results demonstrate Freehold’s financial performance across key metrics:

Strategic Initiatives

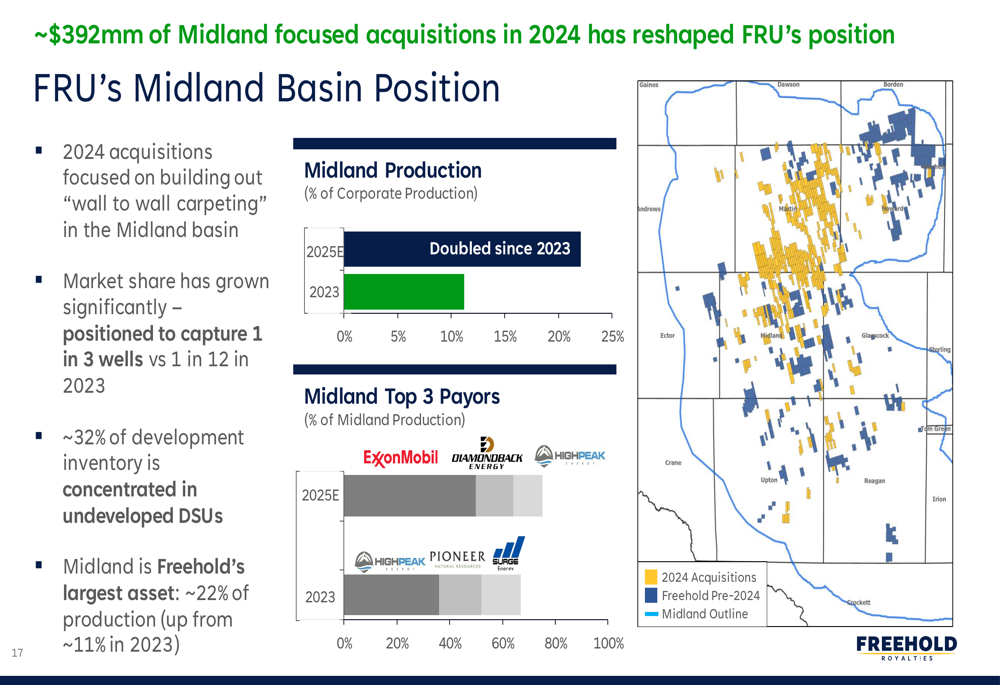

Freehold’s strategic focus on US expansion has been a key driver of its improved financial performance. The company has deployed $685 million across 20 unique transactions in the US, generating an 18% return on investment. Particularly significant has been the $392 million of Midland Basin-focused acquisitions in 2024, which have reshaped Freehold’s position in this prolific basin.

The following map illustrates Freehold’s expanded footprint in the Midland Basin, highlighting recent acquisitions:

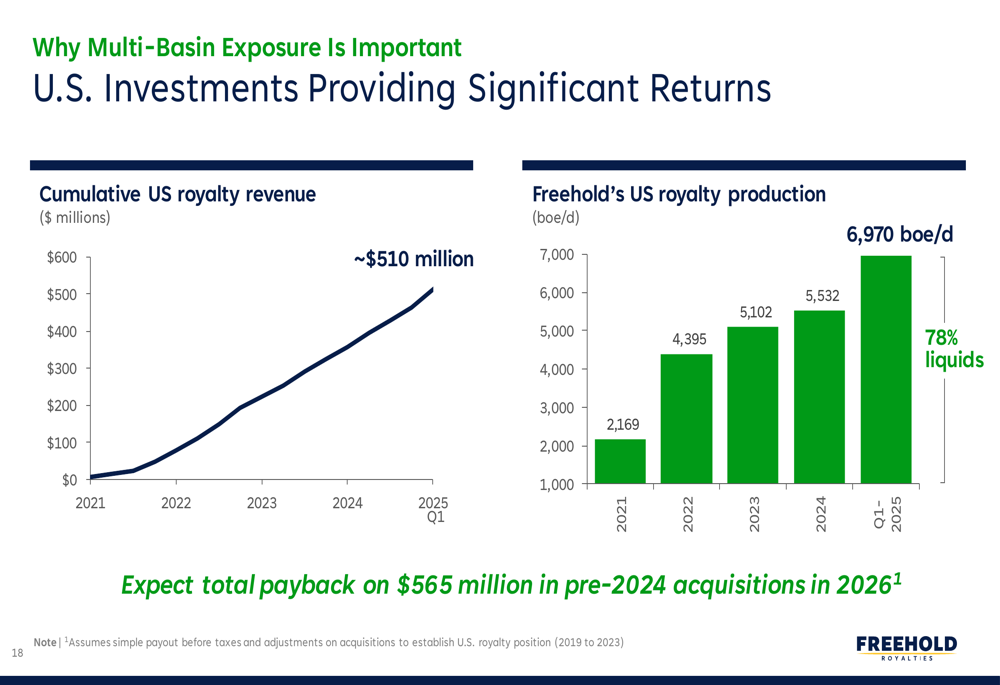

The company’s US investments have provided significant returns, with cumulative US royalty revenue reaching approximately $510 million. Freehold expects total payback on its $565 million in pre-2024 US acquisitions by 2026, demonstrating the strong economics of these investments.

US royalty production has grown steadily from 4,395 boe/d in 2021 to 6,970 boe/d in Q1 2025, with 78% liquids content:

In Canada, Freehold is capitalizing on technological advancements, particularly multilateral drilling techniques that are revitalizing plays in the Clearwater, Mannville heavy oil fairway, and Southeast Saskatchewan light oil regions. This approach is unlocking substantial resources that may have been marginal under previous drilling techniques.

Detailed Financial Analysis

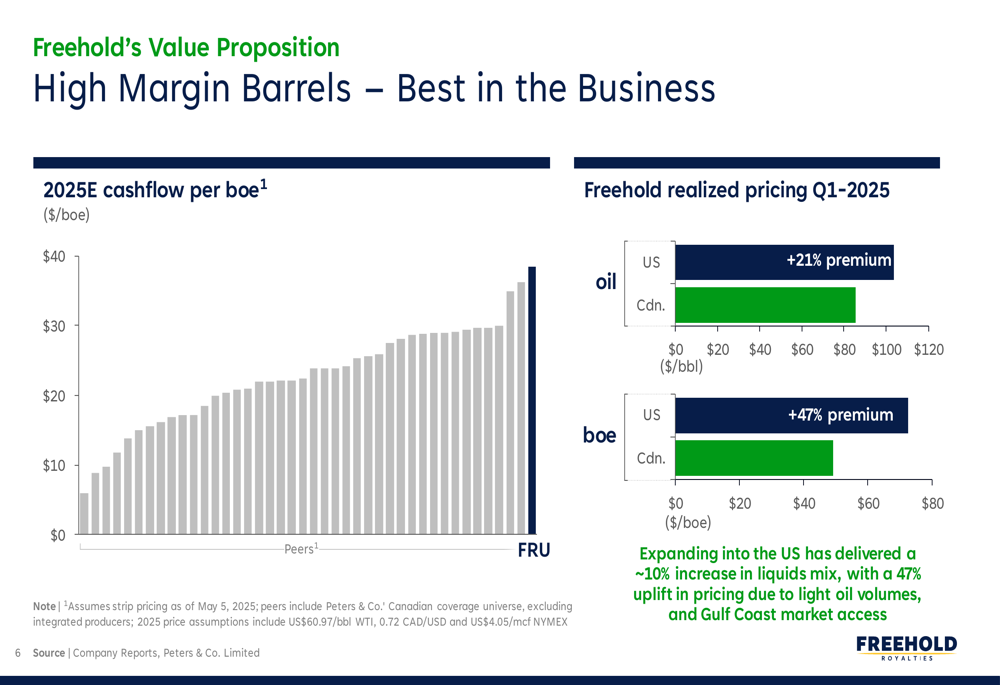

A key strength of Freehold’s business model is its high-margin barrels, which generate superior cash flow compared to peers. The company’s US production commands a significant premium, with realized oil pricing 21% above benchmark and overall boe pricing 47% higher than benchmark prices. This pricing advantage, combined with Freehold’s royalty model (which eliminates direct operating and capital costs), results in operating margins of approximately 85%.

The following chart illustrates Freehold’s cashflow advantage per barrel compared to peers:

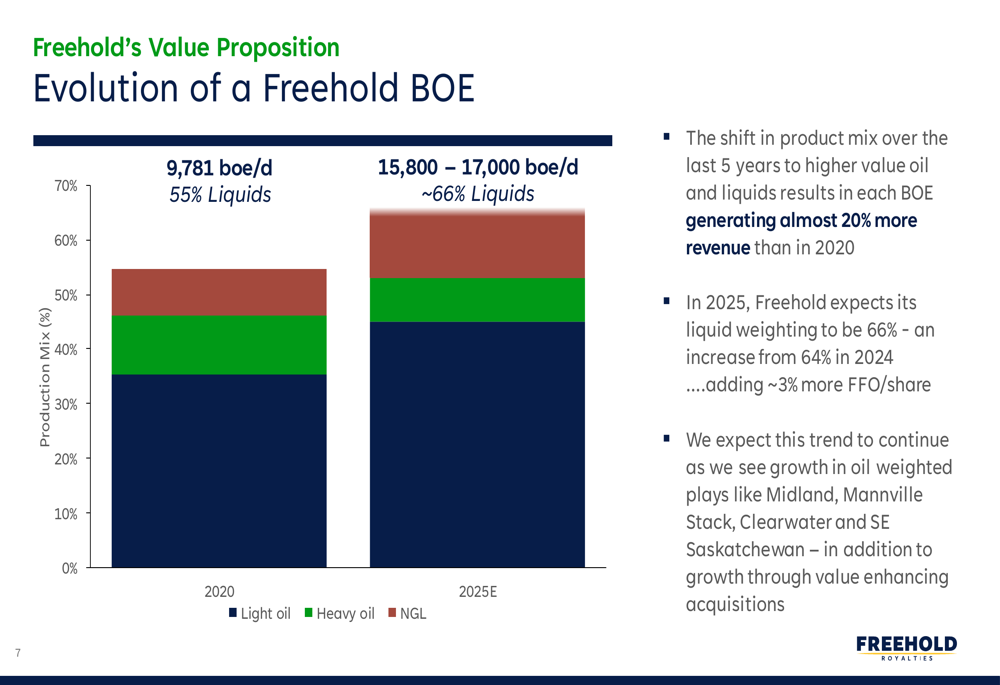

Freehold’s product mix has evolved significantly over the past five years, shifting toward higher-value oil and liquids. In 2020, liquids represented 55% of production, while in 2025, this is expected to reach approximately 66%. This shift has resulted in each barrel of oil equivalent generating almost 20% more revenue than in 2020:

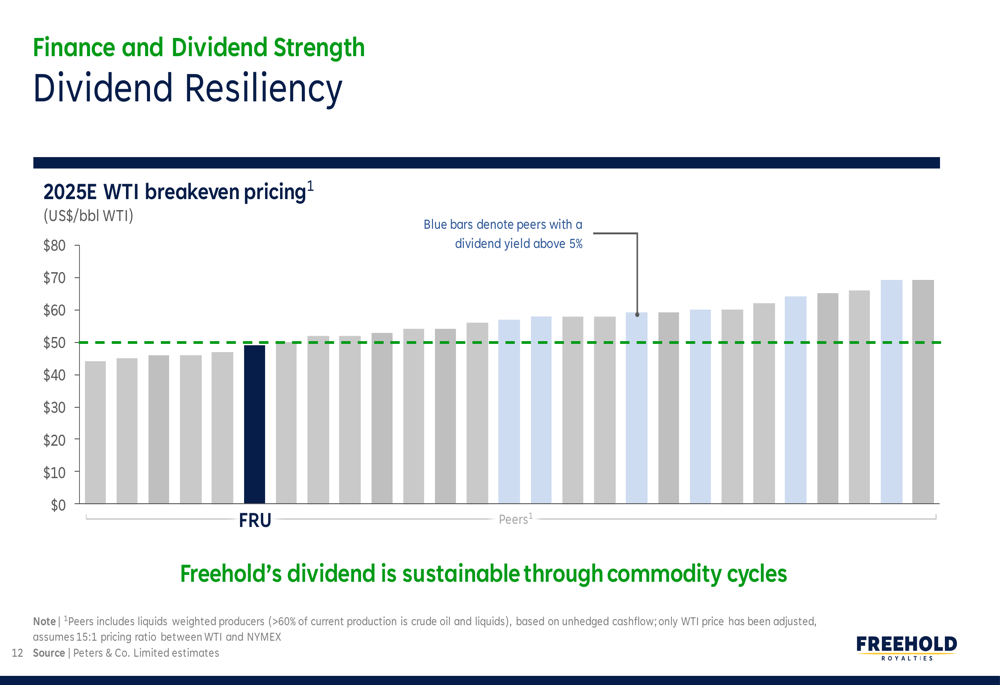

The company’s dividend has proven resilient through commodity price cycles, with cumulative dividends paid reaching $2.3 billion since inception. Freehold’s current monthly dividend of 9 cents per share is supported down to approximately US$50/bbl WTI, providing investors with confidence in the sustainability of returns:

Forward-Looking Statements

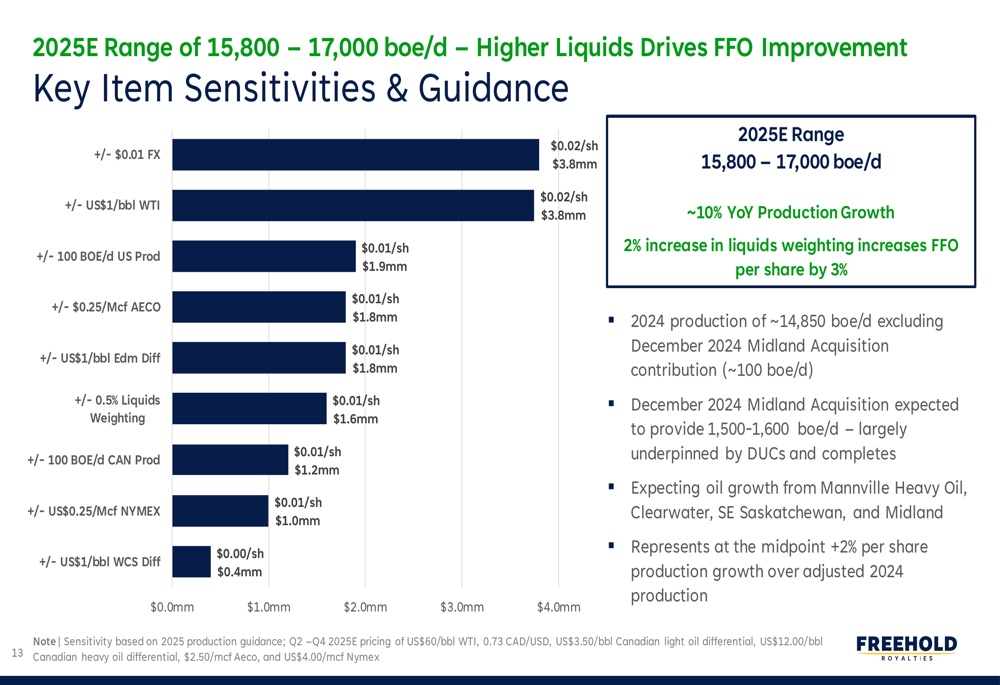

For 2025, Freehold has provided guidance of 15,800 to 17,000 boe/d, representing approximately 10% year-over-year production growth. The company expects its liquids weighting to increase to 66% in 2025, up from 64% in 2024, which is projected to add approximately 3% more funds from operations per share.

The following slide details Freehold’s 2025 guidance and sensitivities to various factors:

Freehold’s long-term growth potential is supported by decades of development inventory, with approximately 18,000 locations in Canada (representing about 40 years of inventory) and approximately 24,000 locations in the United States (about 30 years of inventory). This extensive inventory provides confidence in the sustainability of Freehold’s production and dividend model.

The company maintains a conservative balance sheet with pro forma leverage of 1.0x, providing flexibility for further acquisitions or debt reduction. Management has indicated that at current commodity prices and dividend levels, Freehold has capacity to pay down debt or pursue acquisitions with free funds from operations beyond current dividend levels.

Freehold’s strategic positioning in premium basins, combined with its high-margin royalty model and conservative financial approach, provides a solid foundation for continued growth and sustainable returns to shareholders in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.