LIVE UPDATES: Fed Chair Jerome Powell to deliver major speech at Jackson Hole

Introduction & Market Context

Freshpet Inc . (NASDAQ:FRPT) presented its Q1 2025 earnings results on May 5, 2025, showcasing continued sales momentum despite recent market volatility. The fresh pet food manufacturer reported significant year-over-year growth in a quarter that followed a disappointing Q4 2024, when the company missed earnings expectations. Freshpet’s stock, which had dropped to $76.36 at the previous close, faced additional pressure with a 2.76% decline in premarket trading ahead of the earnings presentation.

The company emphasized its structural advantages in the growing pet food category, stating: "Despite the recent macro-economic headwinds, we believe Freshpet remains a structurally advantaged business with a long runway for growth in a category with long-term tailwinds."

Quarterly Performance Highlights

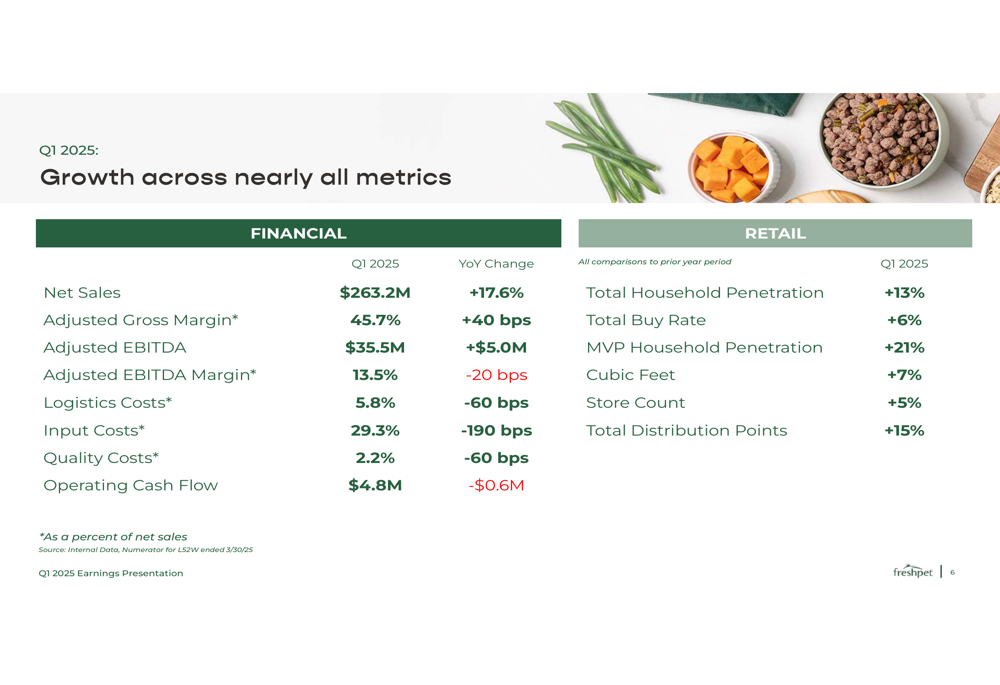

Freshpet delivered strong top-line growth in Q1 2025, with net sales reaching $263.2 million, representing a 17.6% increase year-over-year. This performance demonstrates the company’s ability to maintain growth momentum despite the previous quarter’s challenges. The company also reported an adjusted gross margin of 45.7%, up 40 basis points from the prior year.

As shown in the following comprehensive financial and retail performance summary:

On the profitability front, Freshpet reported adjusted EBITDA of $35.5 million, an increase of $5.0 million compared to Q1 2024. However, the adjusted EBITDA margin slightly contracted by 20 basis points to 13.5%. Operating cash flow was $4.8 million, down $0.6 million from the previous year.

The company’s retail metrics showed robust consumer adoption, with total household penetration increasing by 13% and total buy rate up 6%. Most notably, MVP household penetration (representing the company’s most valuable customers) grew by 21%, indicating strong loyalty among core consumers. Distribution metrics were also positive, with store count up 5% and total distribution points increasing by 15%.

Operational Improvements

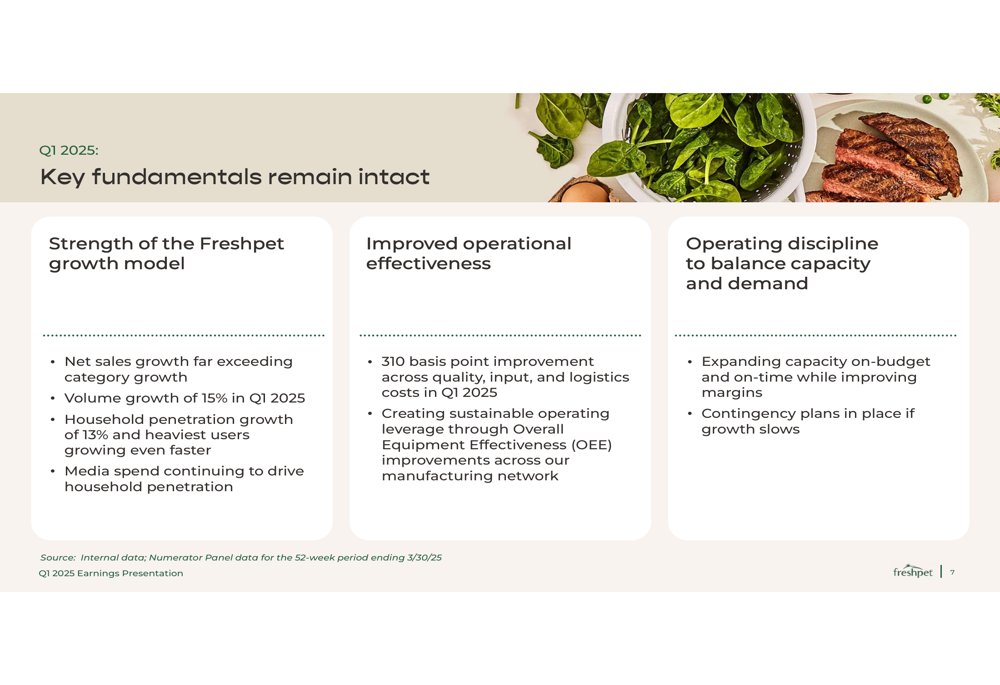

A key focus of Freshpet’s presentation was the significant operational improvements achieved during the quarter. The company highlighted a 310 basis point improvement across quality, input, and logistics costs in Q1 2025, demonstrating progress in operational efficiency.

The breakdown of these improvements includes:

- Logistics costs reduced to 5.8% (down 60 basis points)

- Input costs decreased to 29.3% (down 190 basis points)

- Quality costs improved to 2.2% (down 60 basis points)

These operational fundamentals are creating a foundation for sustainable growth:

The company emphasized its focus on "creating sustainable operating leverage through Overall Equipment Effectiveness (OEE) improvements" across its manufacturing network. Additionally, Freshpet reported that it is "expanding capacity on-budget and on-time while improving margins," with contingency plans in place if growth slows.

Market Position and Growth Strategy

Freshpet continues to see substantial growth opportunities within the pet food market. The company’s presentation highlighted that while the U.S. pet food category represents a $54 billion market, with the dog food category at $37 billion, Freshpet currently holds just 3.5% of the dog food market. However, within its specific niche, the company dominates with a 96% market share of the fresh/frozen segment in measured channels.

The following visualization illustrates Freshpet’s market position and growth runway:

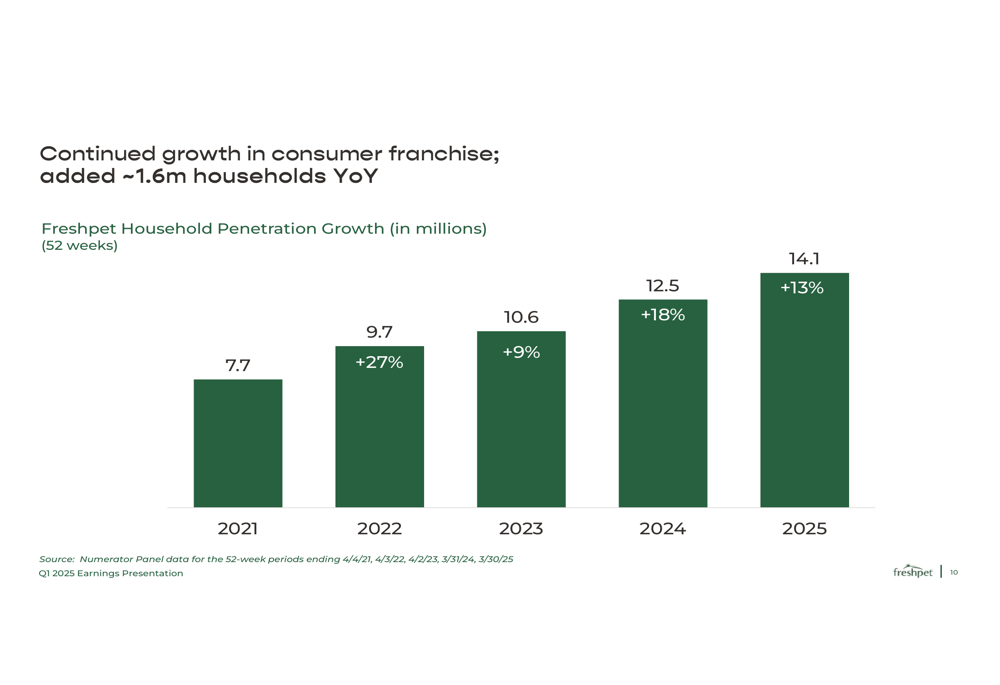

The company’s household penetration metrics further support this growth narrative, showing consistent expansion over the past five years. Freshpet added approximately 1.6 million households year-over-year, bringing its total household penetration to 14.1 million in 2025, a 13% increase from 2024.

This multi-year growth trajectory in household penetration demonstrates the company’s expanding consumer base:

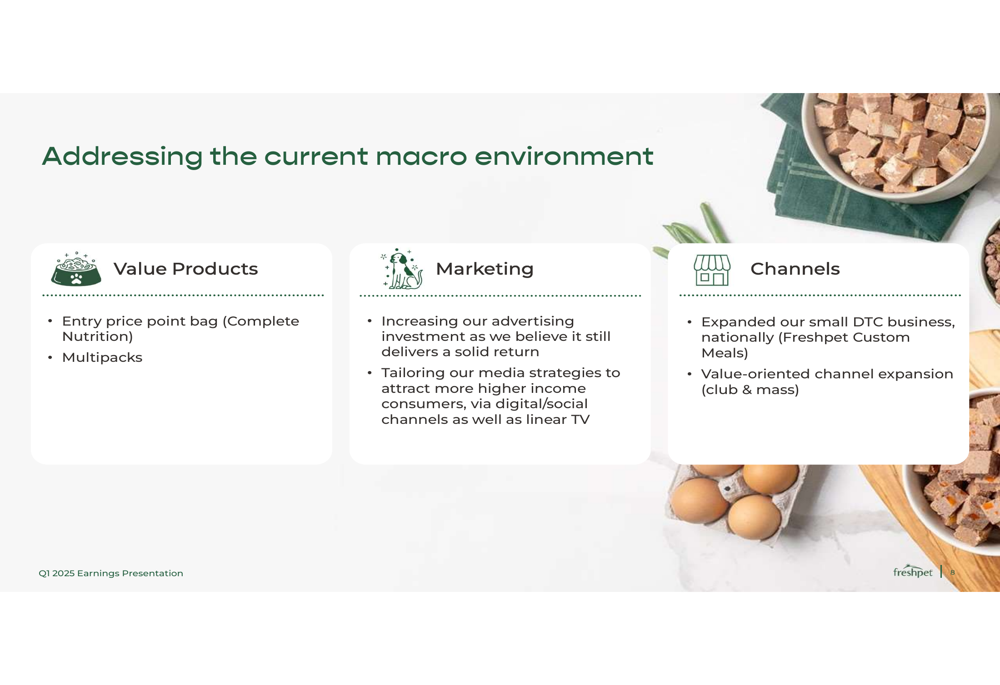

To address current macroeconomic challenges, Freshpet outlined a three-pronged strategy focusing on value products, marketing optimization, and channel expansion:

The company is introducing entry-price-point products and multipacks while tailoring its media strategies to attract higher-income consumers through digital, social, and linear TV channels. Additionally, Freshpet has expanded its direct-to-consumer business nationally and increased its presence in value-oriented channels such as club stores and mass retailers.

Forward-Looking Statements

Despite the slight decline in EBITDA margin and operating cash flow, Freshpet maintains a positive outlook based on its growing market penetration and operational improvements. The company’s previous guidance for 2025, issued during its Q4 2024 earnings, projected net sales between $1.180 billion and $1.210 billion, representing growth of 21% to 24%, with an adjusted EBITDA target of at least $210 million.

The Q1 results appear to keep Freshpet on track to meet these targets, though investors will be watching closely to see if the company can maintain its sales momentum while improving profitability metrics. The stock’s recent performance suggests continued market skepticism, with shares trading significantly below their 52-week high of $164.07, despite the company’s strong sales growth.

As Freshpet continues to expand its manufacturing capacity and distribution footprint, the balance between growth investments and margin improvement will remain a key focus for investors evaluating the company’s long-term potential in the premium pet food market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.