Fed’s Powell opens door to potential rate cuts at Jackson Hole

Introduction & Market Context

Freshpet Inc . (NASDAQ:FRPT) presented its Q2 2025 earnings results on August 4, 2025, highlighting significant profitability improvements despite a challenging consumer environment. The company, which holds a 3.6% share of the $37 billion dog food market, reported a notable turnaround in net income while continuing to expand its household penetration.

The results mark a strong recovery from Q1 2025, when Freshpet posted an unexpected loss of $0.26 per share. In pre-market trading following the Q2 announcement, Freshpet shares rose 1.75% to $67, according to available market data.

As shown in the following market positioning chart, Freshpet dominates the fresh/frozen pet food segment with 95% market share in measured channels, while still having substantial room for growth in the broader pet food category:

Quarterly Performance Highlights

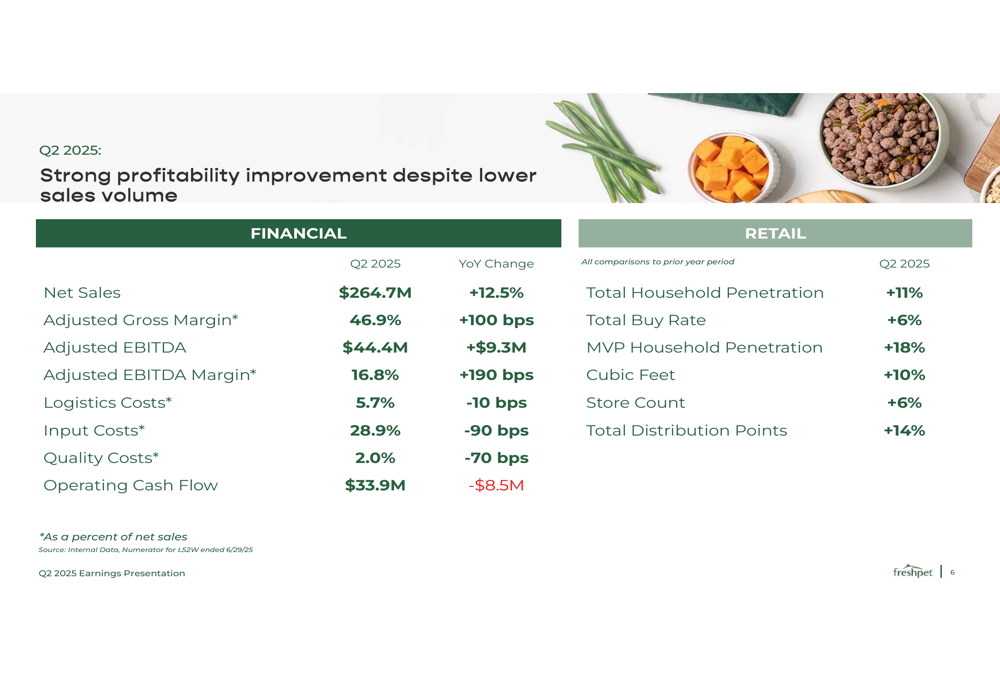

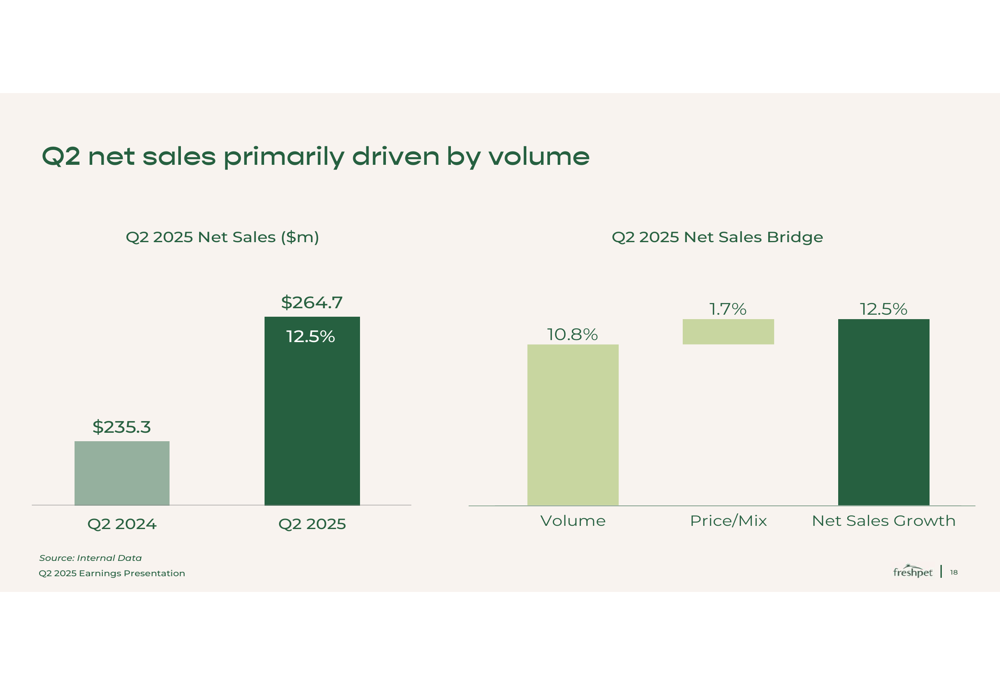

Freshpet delivered solid financial results in Q2 2025, with net sales increasing 12.5% year-over-year to $264.7 million, primarily driven by volume growth of 10.8%. The company achieved a significant profitability improvement, reporting net income of $16.4 million compared to a loss of $1.7 million in Q2 2024.

The following summary highlights Freshpet’s key financial and retail metrics for the quarter:

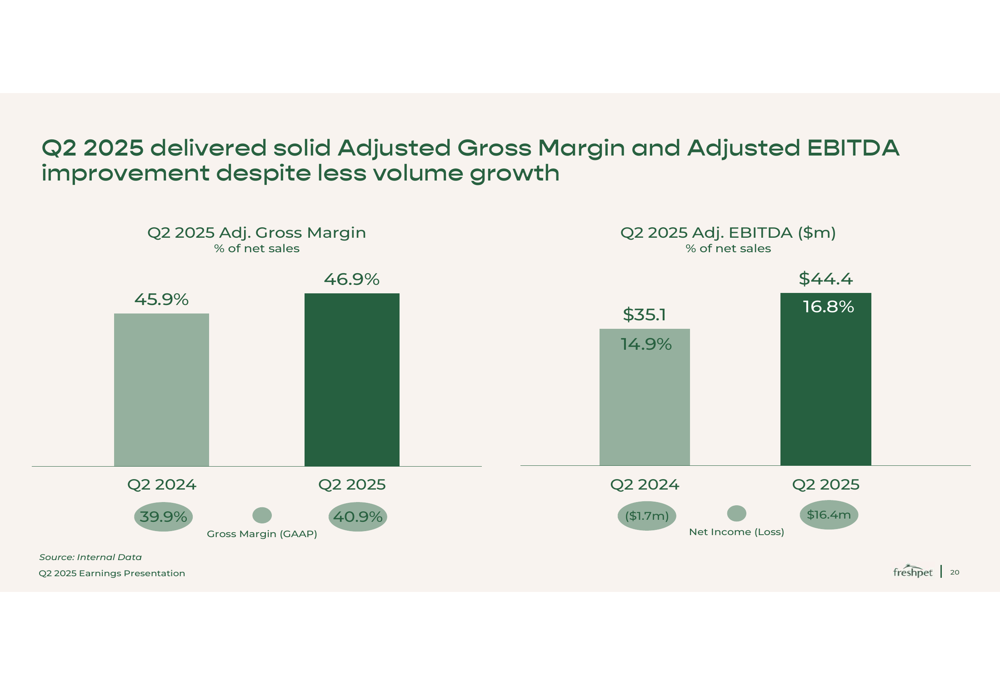

Adjusted gross margin expanded to 46.9%, up 100 basis points year-over-year, while adjusted EBITDA increased by $9.3 million to $44.4 million, representing a margin of 16.8% (up 190 basis points). These improvements reflect the company’s focus on operational efficiency and cost management.

The detailed breakdown of profitability metrics shows the substantial improvement in both adjusted gross margin and EBITDA:

Sales growth was primarily volume-driven, with price and mix contributing only 1.7% to the overall 12.5% increase:

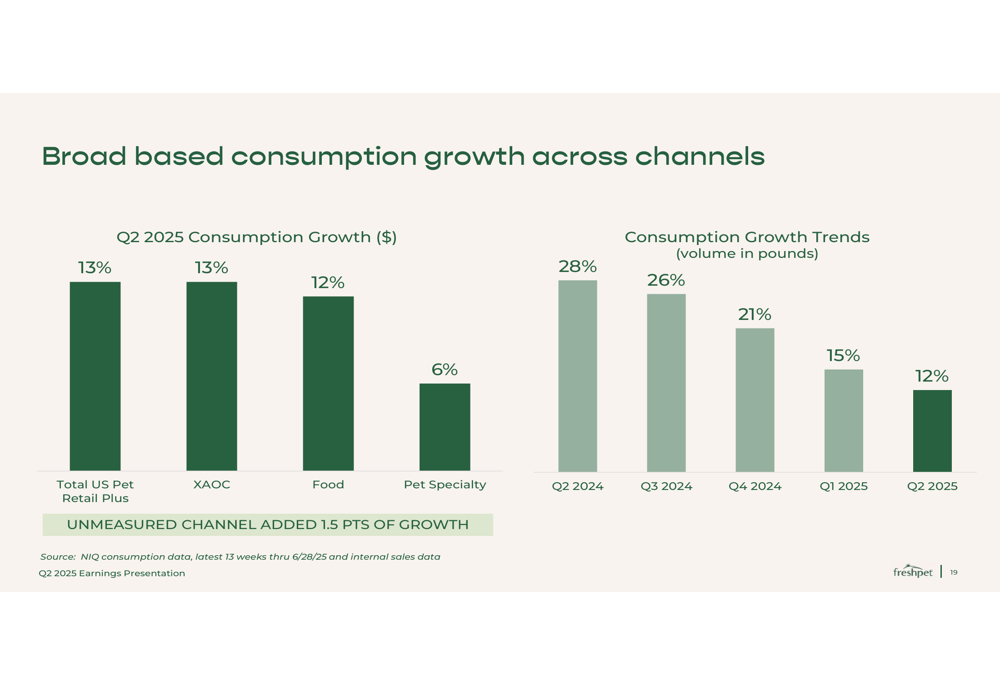

While sales growth remains strong, it represents a deceleration from previous quarters. Consumption growth trends show a gradual slowdown from 28% in Q2 2024 to 12% in Q2 2025:

Operational Improvements

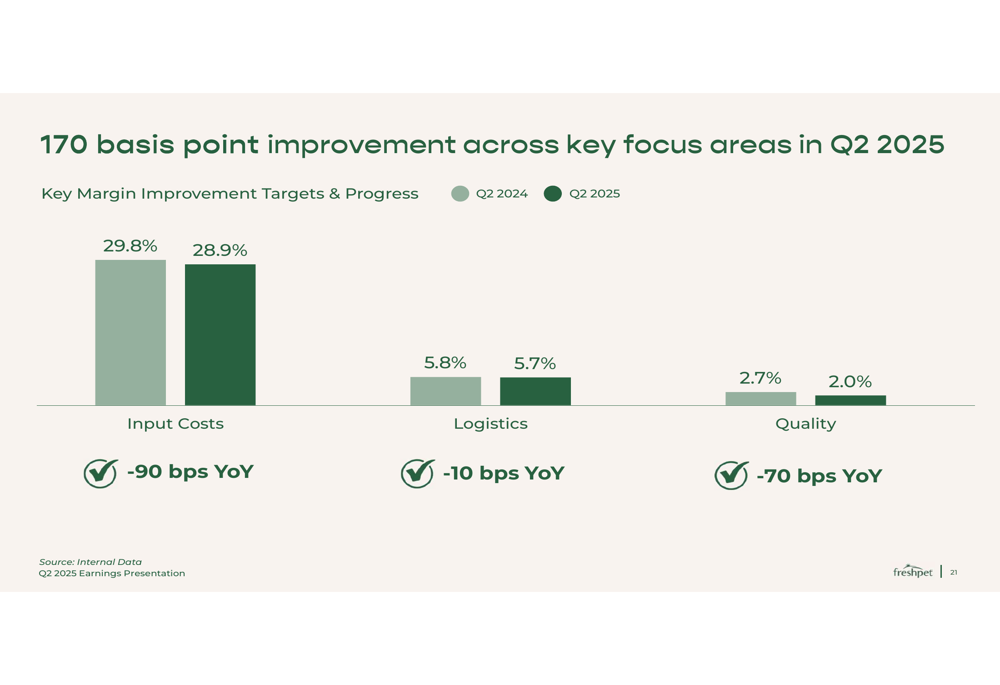

A key driver of Freshpet’s improved profitability was the 170 basis point reduction in combined input costs, logistics costs, and quality costs compared to the prior year. The company highlighted significant progress in operational effectiveness across its manufacturing network.

The following chart details these operational improvements:

Freshpet noted that its Ennis (NYSE:EBF) Kitchen has now become the most profitable facility in its network, achieving better profitability sooner than expected due to strong leadership and thoughtful design. The company expects this facility to produce more than 50% of its volume within the next few years.

The company is also developing new production technologies designed to increase bagged product margins and decrease the margin gap between bags and roll products. These innovations aim to deliver higher quality products at lower costs through increased yields and throughput.

Strategic Initiatives

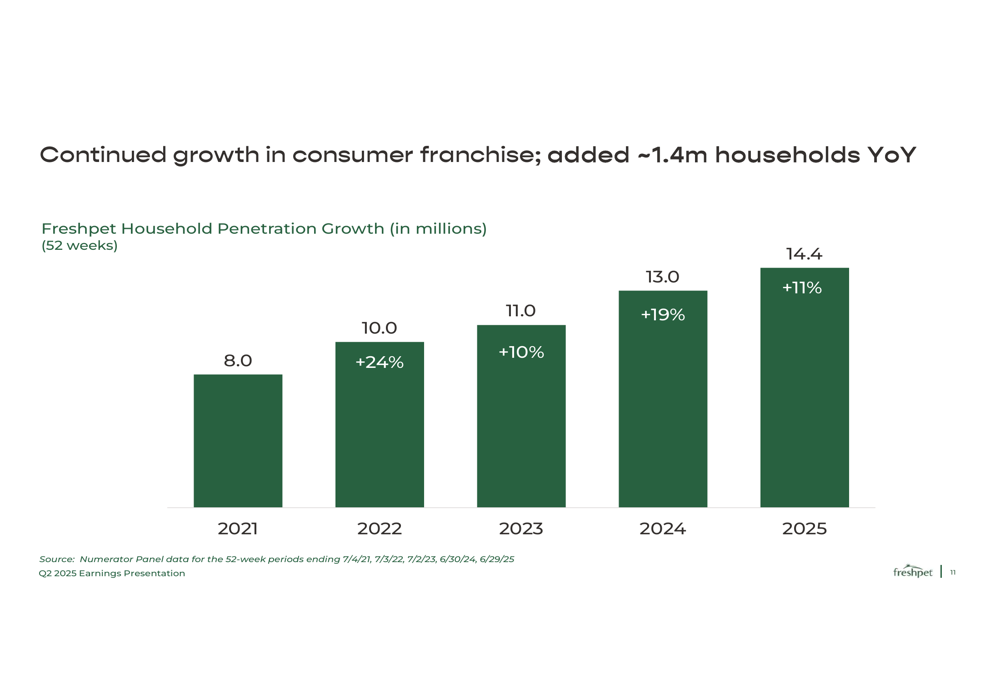

Despite the challenging consumer environment, Freshpet continues to expand its household penetration, which grew 11% year-over-year to 14.4 million households. Particularly notable is the 18% growth in MVP (Ultra/Super Heavy Buyers) households to 2.2 million, with their buy rate increasing to $501.

The company’s household penetration has shown consistent growth over the years:

To address the current consumer environment, Freshpet is implementing several strategic initiatives:

1. A new advertising campaign launching in August, complemented by increased social and digital campaigns targeting MVPs

2. Expansion in value-oriented channels, including an expanded test in club retail to 125 stores

3. Introduction of entry price point products and multipacks/bundles in select retailers

4. Expected outsized growth in digital channels, including expansion of Freshpet Custom Meals (direct-to-consumer)

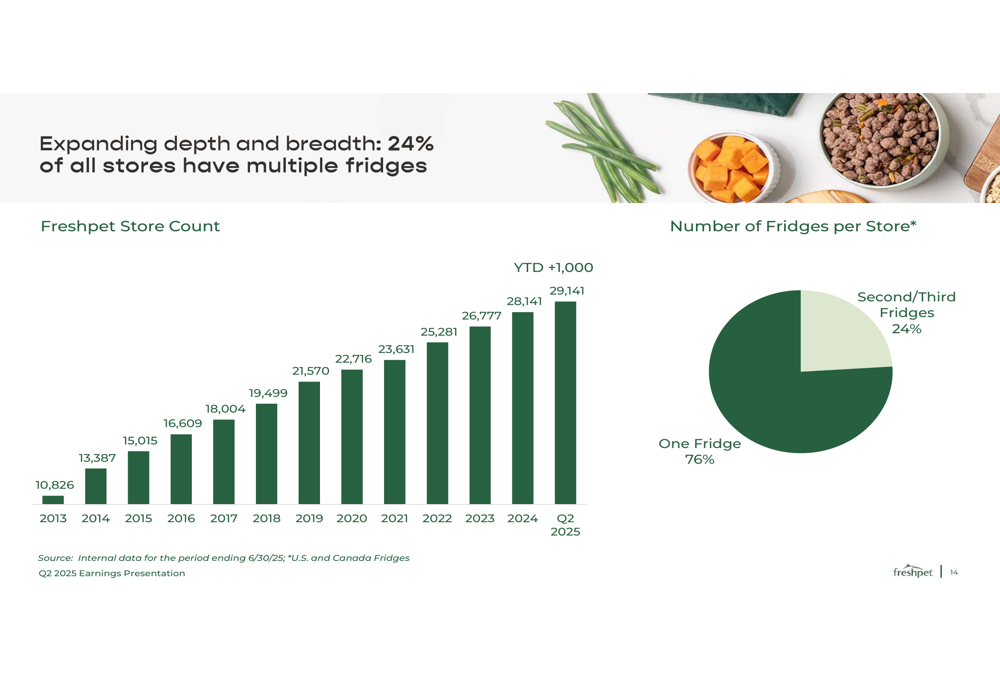

The company continues to expand its store count, which reached 29,141 in 2025, with 24% of stores now having multiple fridges:

Revised Guidance & Outlook

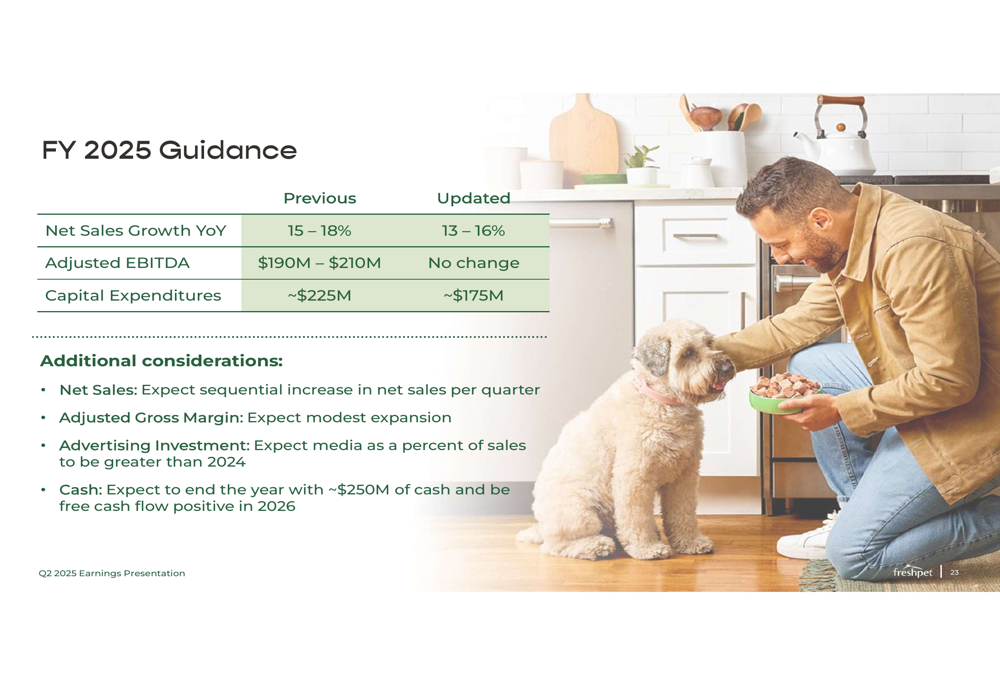

Freshpet has updated its full-year 2025 guidance, revising net sales growth expectations downward while maintaining its adjusted EBITDA targets and reducing capital expenditure plans:

The company now expects net sales growth of 13-16% for FY 2025, down from the previous guidance of 15-18%, reflecting the challenging consumer environment. However, Freshpet maintained its adjusted EBITDA guidance of $190-210 million, suggesting confidence in continued operational improvements offsetting the sales growth deceleration.

Notably, Freshpet reduced its capital expenditure guidance from approximately $225 million to $175 million, highlighting improved capital efficiency. The company expects to end the year with approximately $250 million in cash and achieve positive free cash flow in 2026.

Looking further ahead, Freshpet reaffirmed its 2027 targets of 22% adjusted EBITDA margin and 48% adjusted gross margin, demonstrating long-term confidence despite near-term headwinds.

The company’s capital efficiency framework focuses on three key areas: extracting more from existing production lines, maximizing output from existing sites, and developing new technologies to improve margins and reduce capital intensity in the coming years.

In conclusion, while Freshpet faces challenges in maintaining its historical growth rates amid a tougher consumer environment, the company’s Q2 2025 results demonstrate significant progress in operational efficiency and profitability, potentially positioning it for sustainable long-term growth with improved returns on capital.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.