Nvidia’s desktop AI supercomputer now available to the general public

Introduction & Market Context

Freshworks Inc . (NASDAQ:FRSH) presented its Q2 2025 earnings results on July 29, 2025, revealing continued revenue growth and a strategic shift toward larger enterprise customers. The company, which provides enterprise-grade service software for customer and employee experience, reported an 18% year-over-year revenue increase to $204.7 million, slightly exceeding market expectations.

Following the earnings announcement, Freshworks stock showed positive movement in aftermarket trading, rising 1.07% to $14.15. This comes after the stock closed at $14.00, down 0.64% in regular trading.

Quarterly Performance Highlights

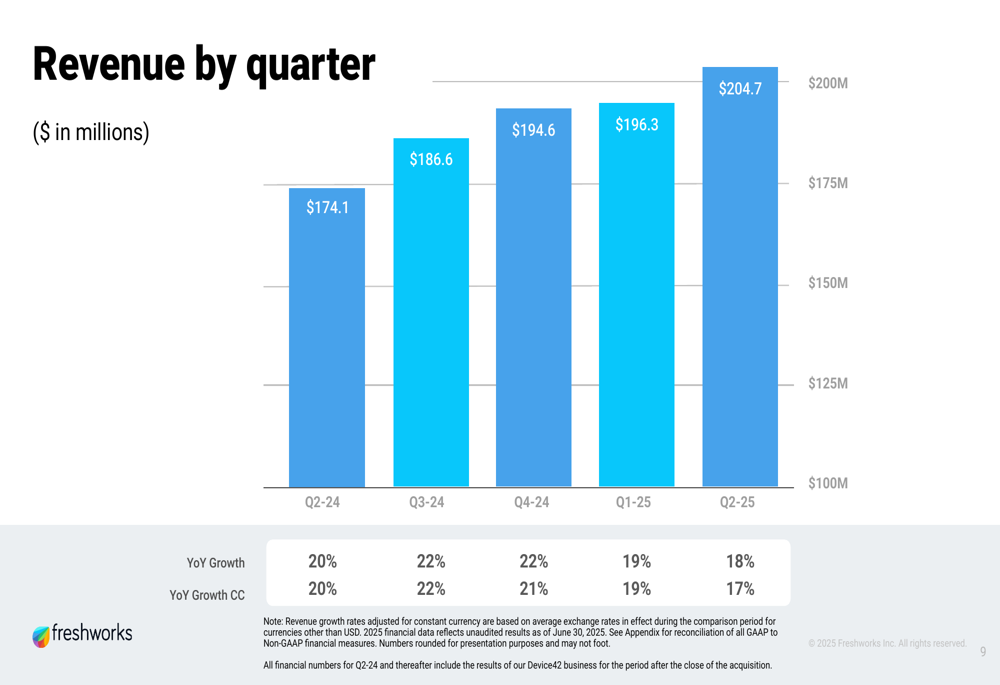

Freshworks maintained its growth trajectory in Q2 2025, with revenue reaching $204.7 million, representing an 18% year-over-year increase (17% in constant currency). This continues a pattern of steady growth over the past five quarters, though the pace has moderated slightly from the 20-22% growth seen in late 2024.

As shown in the following chart of quarterly revenue growth:

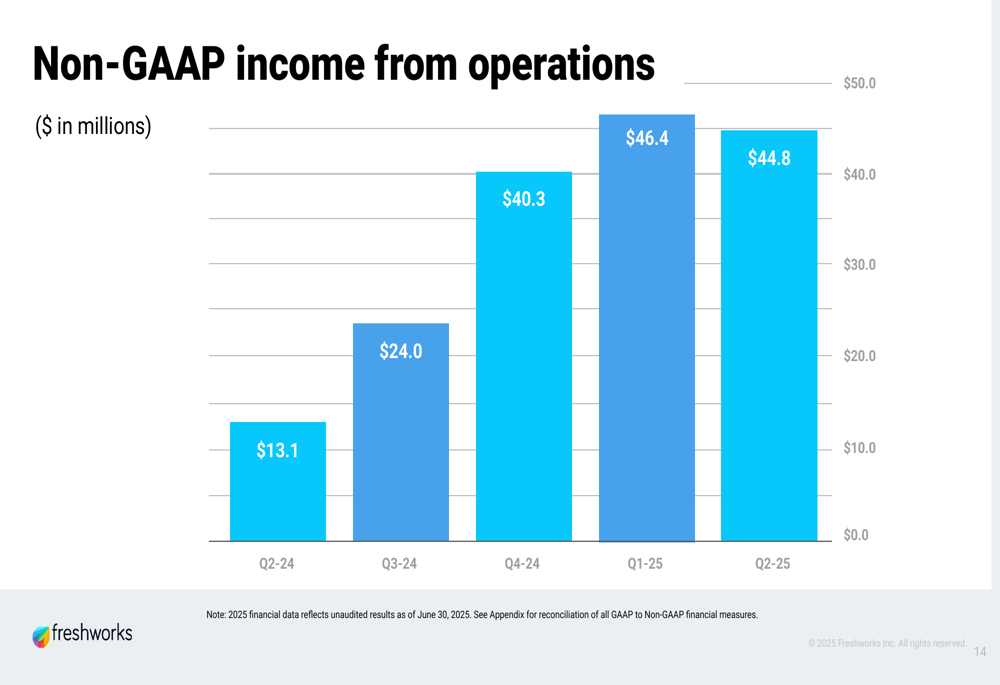

The company’s profitability metrics showed substantial improvement, with Non-GAAP income from operations reaching $44.8 million in Q2 2025, more than tripling from $13.1 million in the same quarter last year. This reflects Freshworks’ focus on operational efficiency and scale.

The following chart illustrates this dramatic improvement in Non-GAAP operating income:

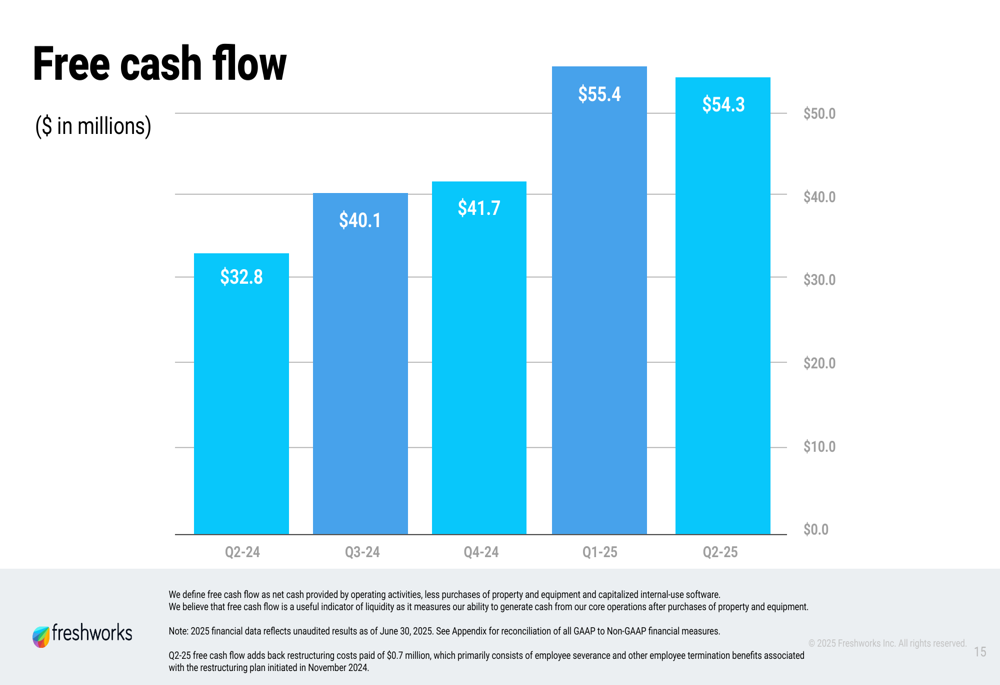

Free cash flow remained robust at $54.3 million for Q2 2025, compared to $32.8 million in Q2 2024, demonstrating the company’s ability to convert revenue into cash efficiently.

As shown in the free cash flow trend:

Customer Base Evolution

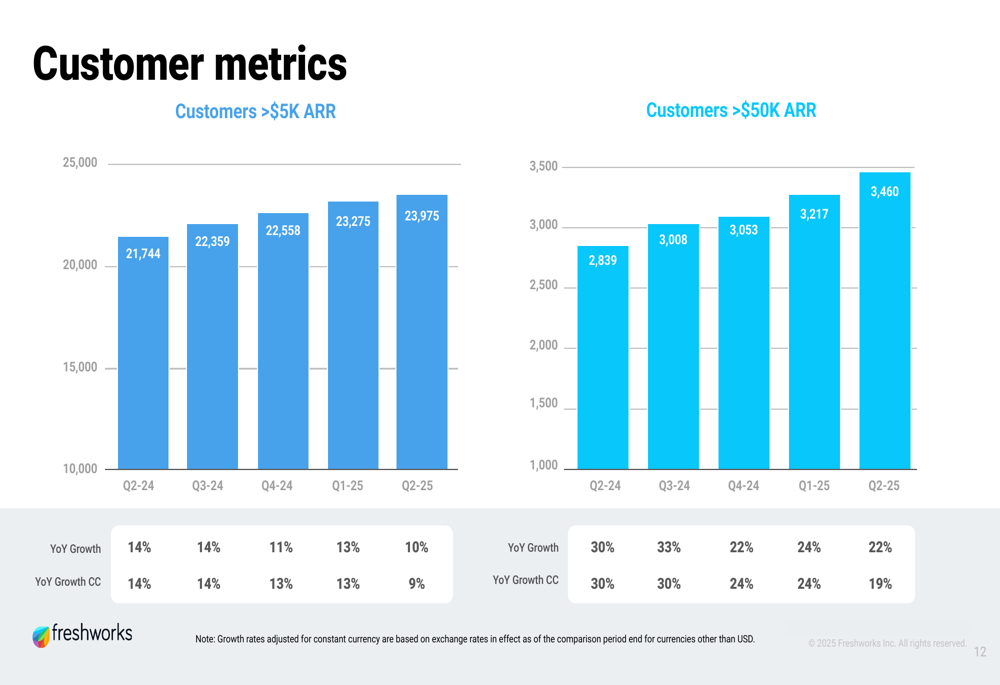

A key highlight from the presentation was Freshworks’ strategic shift toward larger customers. The company now serves 74,600 customers globally, an 8% increase year-over-year. More significantly, customers with annual recurring revenue (ARR) exceeding $50,000 grew by 22% to 3,460, indicating success in moving upmarket.

The following chart shows the growth in high-value customers:

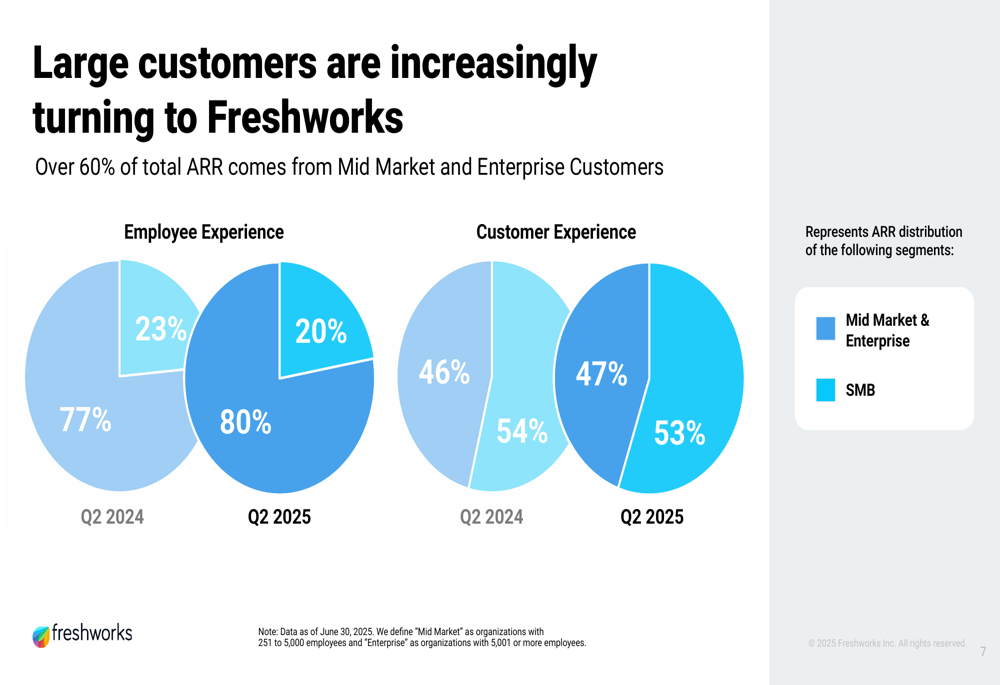

Perhaps the most dramatic transformation is visible in the company’s ARR distribution by customer size. For Employee Experience products, Mid Market & Enterprise customers now account for 80% of ARR, up dramatically from just 23% a year ago. Customer Experience products show a similar but less pronounced shift, with Mid Market & Enterprise customers now representing 53% of ARR, up from 46% in Q2 2024.

This strategic pivot is illustrated in the following chart:

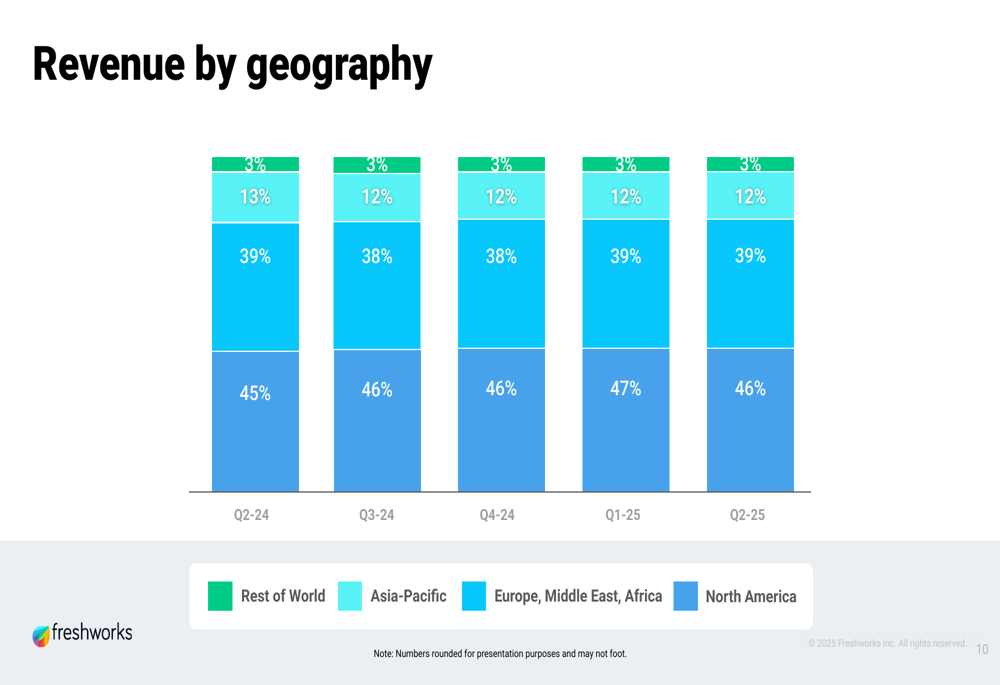

Freshworks continues to maintain a diverse customer base across industries and geographies, with North America representing 46% of revenue, followed by Europe, Middle East, and Africa at 39%.

The geographic distribution of revenue is shown here:

Product Portfolio and AI Strategy

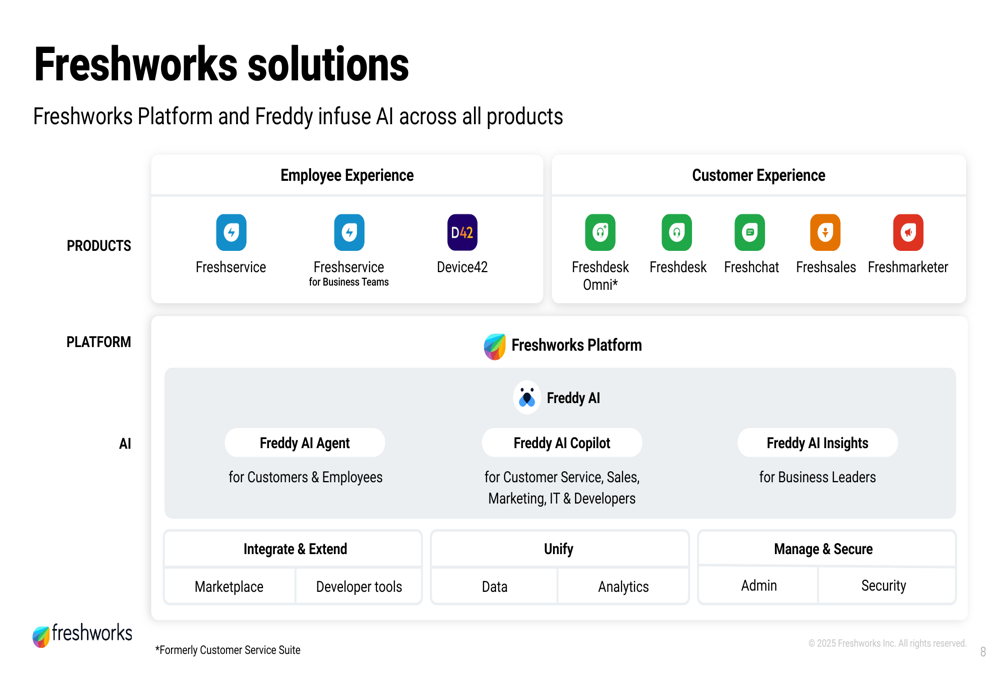

Freshworks’ product portfolio spans two main categories: Employee Experience (including Freshservice and Device42) and Customer Experience (including Freshdesk, Freshchat, and Freshsales). The company has been infusing AI capabilities across its product suite through its Freddy platform, which includes Agent, Copilot, and Insights functionalities.

The comprehensive solutions overview is illustrated below:

This AI-focused strategy aligns with comments made during the Q1 2025 earnings call, where CEO Dennis Woodside (OTC:WOPEY) emphasized that Freshworks is "in the next stage of generative AI and have moved from output to outcome." The continued investment in AI capabilities appears to be resonating with customers, particularly in the mid-market segment.

Financial Outlook

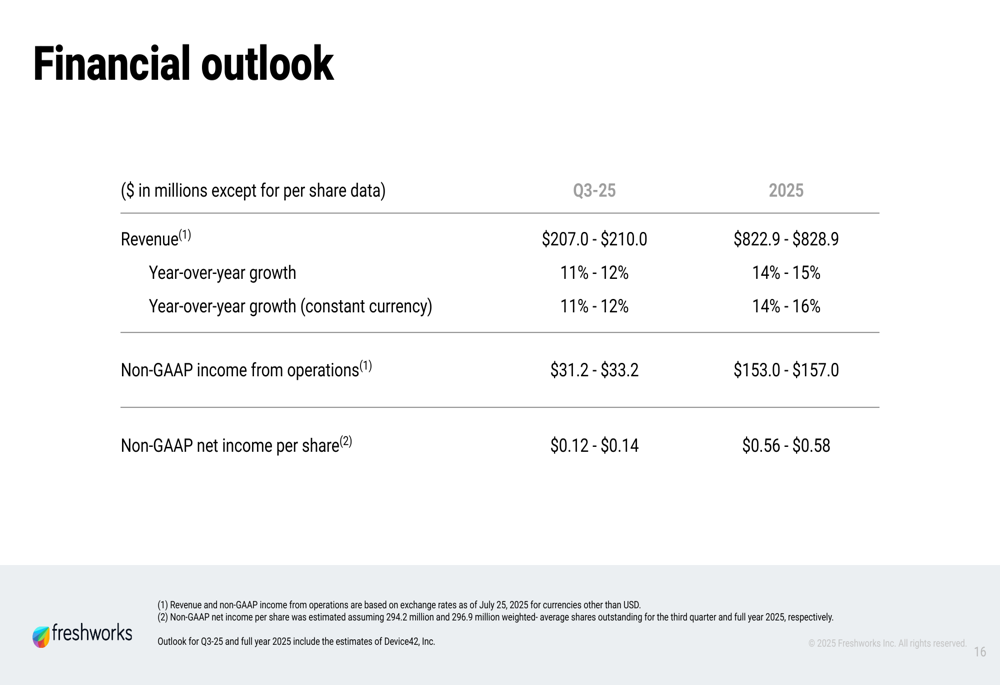

Looking ahead, Freshworks provided guidance for Q3 2025 and the full year. For Q3, the company expects revenue between $207.0 and $210.0 million, representing 11-12% year-over-year growth. For the full year 2025, Freshworks projects revenue between $822.9 and $828.9 million, indicating 14-15% growth.

The company also expects continued profitability, with Non-GAAP income from operations projected at $31.2-$33.2 million for Q3 and $153.0-$157.0 million for the full year. Non-GAAP net income per share is expected to be $0.12-$0.14 for Q3 and $0.56-$0.58 for the full year.

The detailed financial outlook is presented in this table:

Conclusion

Freshworks’ Q2 2025 results demonstrate the company’s successful execution of its strategic shift toward larger enterprise customers while maintaining overall growth. The significant improvements in profitability metrics suggest that this strategy is yielding positive financial results, even as year-over-year revenue growth has moderated slightly.

The company’s continued investment in AI capabilities across its product portfolio positions it to capitalize on the growing demand for intelligent automation in both customer and employee experience software. However, the projected slowdown in revenue growth for Q3 2025 (to 11-12%) indicates potential challenges ahead in maintaining the current growth trajectory.

As Freshworks continues its evolution from a primarily SMB-focused provider to one with a stronger enterprise presence, investors will be watching closely to see if the company can maintain its profitability gains while reigniting higher growth rates in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.