Nvidia, Amazon and Tesla rise premarket; Walmart falls

Introduction & Market Context

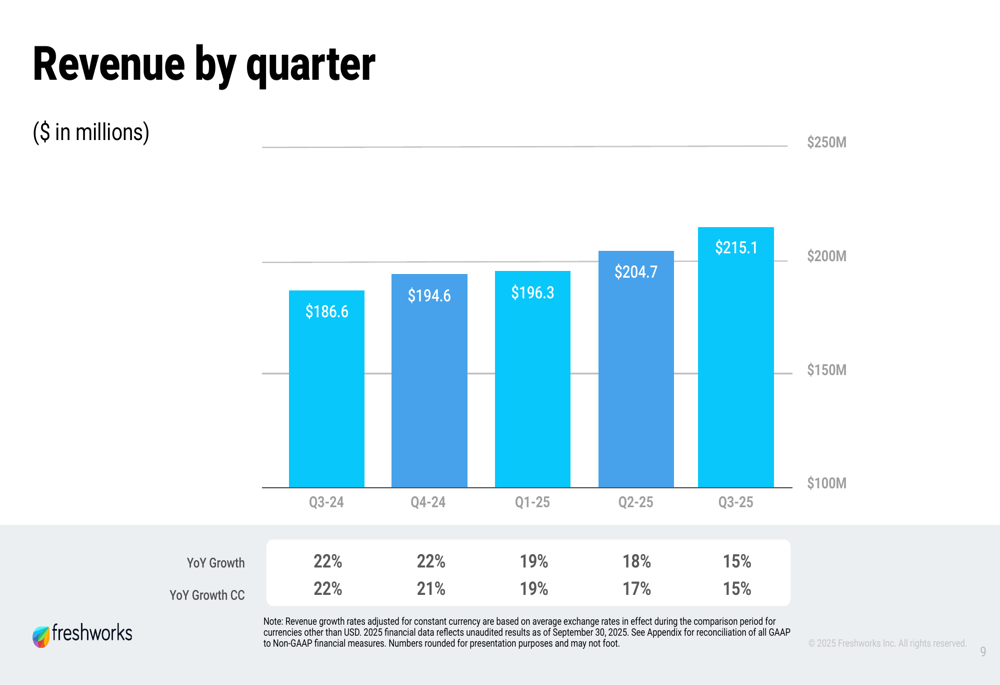

Freshworks Inc. (NASDAQ:FRSH) released its third quarter 2025 earnings presentation on November 5, revealing $215.1 million in revenue, a 15% year-over-year increase. The customer experience and IT service management software provider saw its shares rise 1.28% in after-hours trading to $10.96, reflecting investor confidence despite a growth rate that has gradually slowed from 22% a year ago.

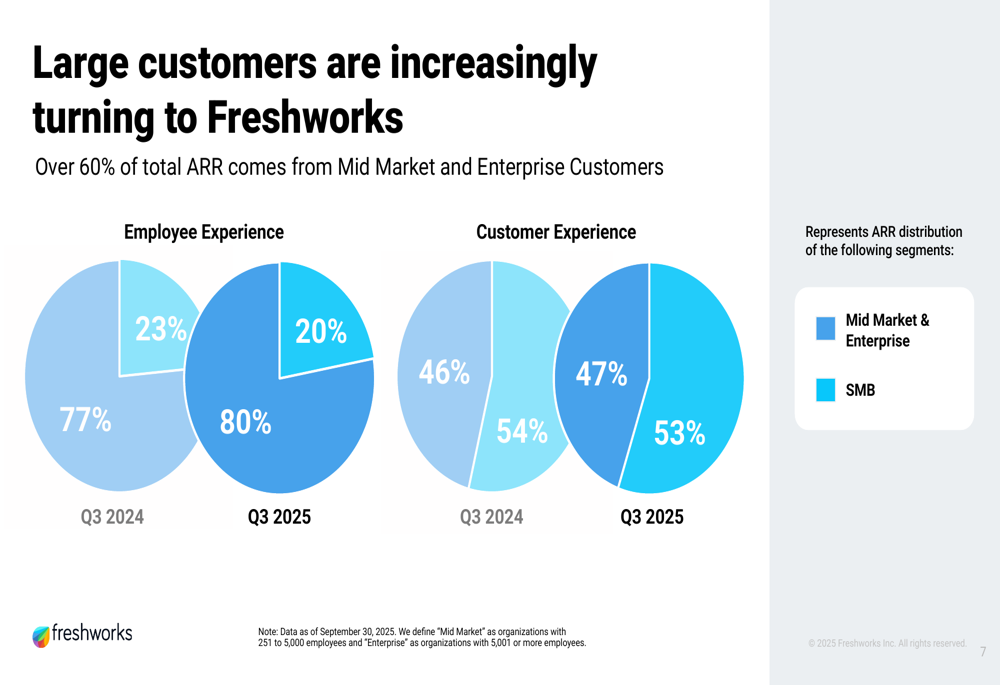

The company's presentation highlighted its strategic pivot toward larger customers, with over 60% of annual recurring revenue now coming from mid-market and enterprise segments. This shift comes as Freshworks continues to expand its AI capabilities across its product portfolio.

Quarterly Performance Highlights

Freshworks reported steady revenue growth over five consecutive quarters, though the pace has moderated from 22% year-over-year in Q3 2024 to 15% in the most recent quarter. The company maintained consistent performance in constant currency terms as well.

As shown in the following chart of quarterly revenue growth:

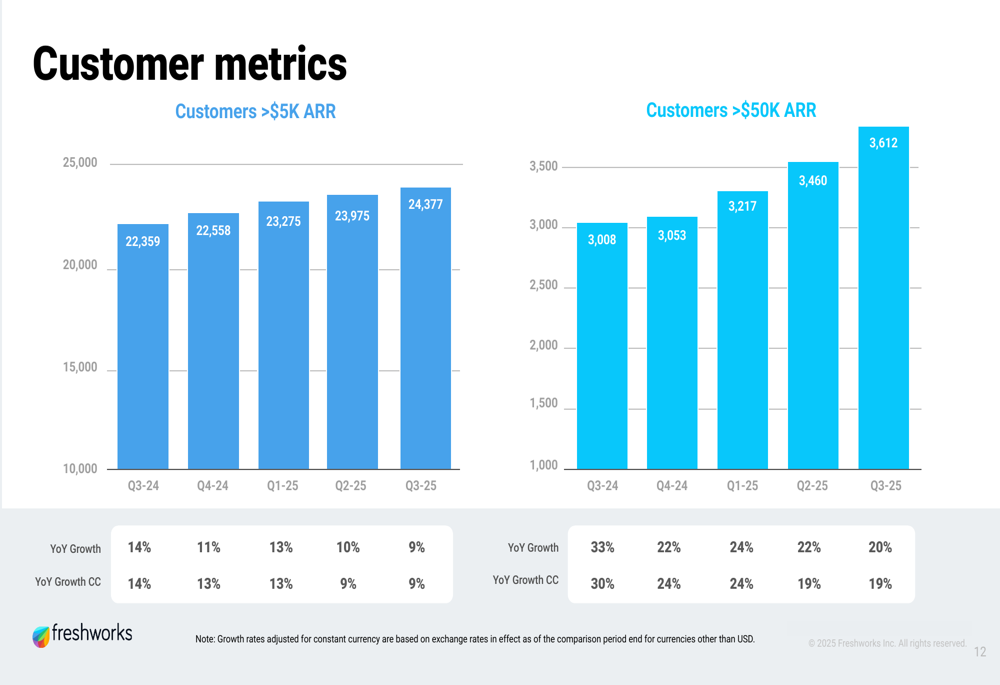

The company's customer base grew to nearly 75,000 paying customers across more than 120 countries, representing an 8% year-over-year increase. More significantly, Freshworks is seeing stronger growth in higher-value customer segments, with customers generating over $50,000 in annual recurring revenue increasing by 20% year-over-year to 3,612.

This customer segmentation trend is illustrated in the following chart:

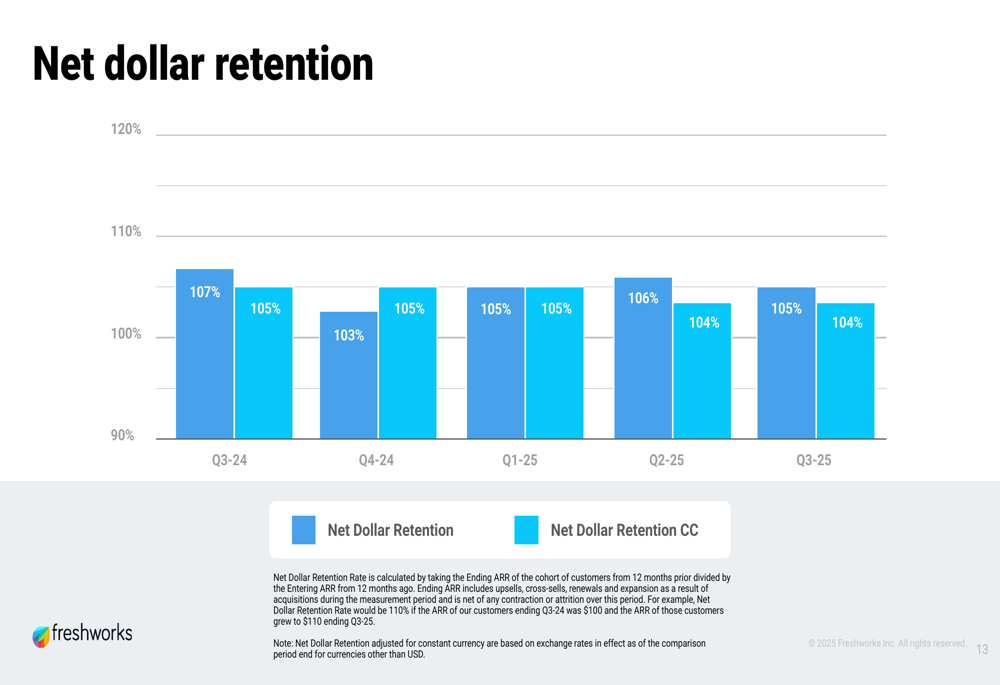

Freshworks' net dollar retention rate stood at 105% for Q3 2025, showing consistent customer spending patterns over the past five quarters:

Strategic Initiatives

A key strategic focus for Freshworks has been expanding its footprint with larger customers. The presentation revealed a significant shift in revenue composition, with mid-market and enterprise customers (organizations with more than 250 employees) now accounting for over 60% of total ARR.

This strategic pivot is clearly illustrated in the following breakdown:

The company continues to attract notable brands, welcoming new customers including Allsaints, Apollo Tyres, Société Générale, and Stellantis during the quarter. These additions complement an existing customer base that includes TaylorMade, S&P Global, Bridgestone, Marvel, and Databricks.

Freshworks is also heavily investing in AI-powered solutions across both its employee experience (EX) and customer experience (CX) product lines. The company's "Freddy AI" platform now encompasses AI Agent, AI Copilot, and AI Insights capabilities, which CEO Dennis Woodside emphasized in the earnings call as becoming increasingly essential for all customers.

Detailed Financial Analysis

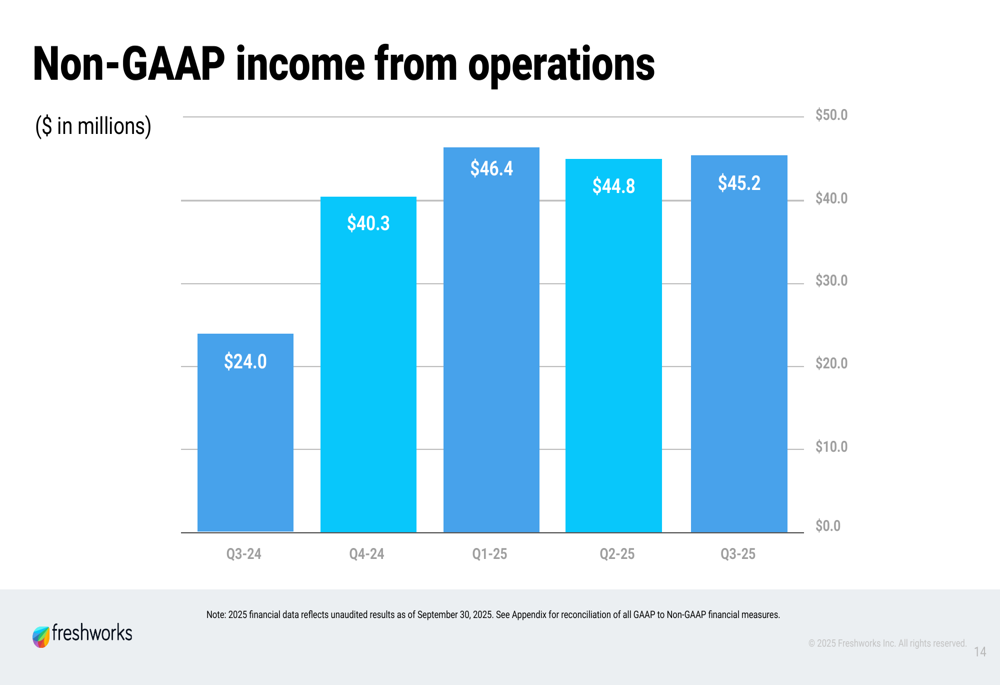

Beyond revenue growth, Freshworks demonstrated significant improvement in profitability metrics. Non-GAAP income from operations nearly doubled year-over-year to $45.2 million in Q3 2025, compared to $24.0 million in Q3 2024.

The following chart illustrates this profitability trend:

Free cash flow also showed strong growth, reaching $57.2 million in Q3 2025, up from $40.1 million a year earlier. This represents a free cash flow margin of approximately 27%, indicating efficient capital management and operational leverage.

As shown in the free cash flow progression:

From a geographic perspective, Freshworks maintained a consistent revenue distribution with North America accounting for 46% of revenue, Europe, Middle East and Africa at 39%, Asia-Pacific at 12%, and Rest of World at 3%. This stability suggests the company's global expansion strategy has reached a steady state.

Forward-Looking Statements

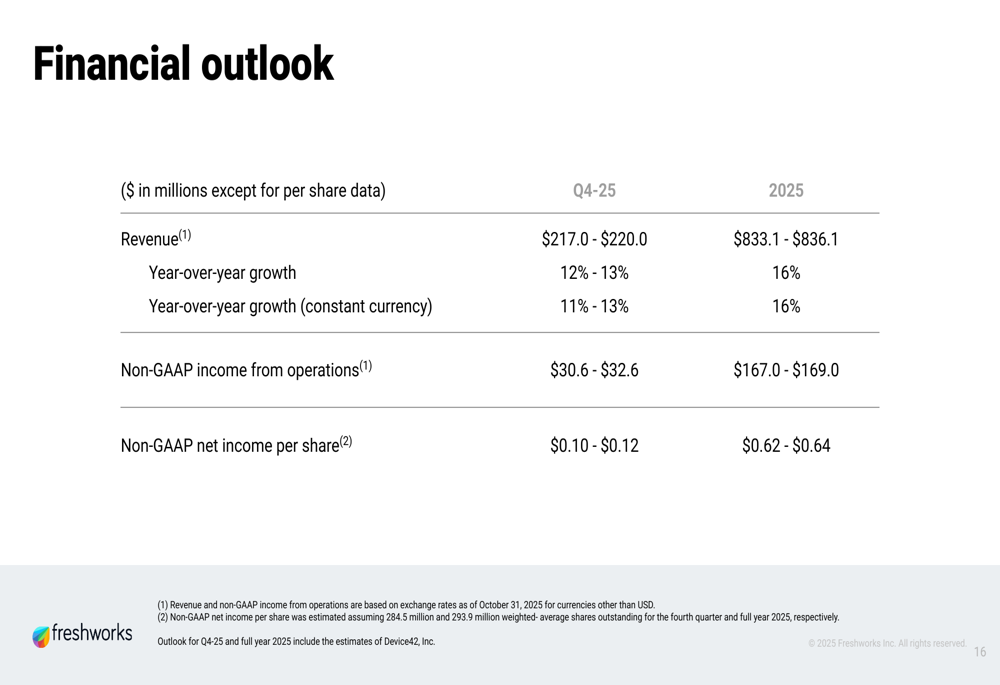

Looking ahead, Freshworks provided guidance for both Q4 2025 and the full year. For the fourth quarter, the company expects revenue between $217.0 and $220.0 million, representing 12-13% year-over-year growth. Non-GAAP income from operations is projected at $30.6 to $32.6 million with non-GAAP earnings per share of $0.10 to $0.12.

For the full year 2025, Freshworks anticipates revenue of $833.1 to $836.1 million, reflecting 16% year-over-year growth. The company projects non-GAAP income from operations of $167.0 to $169.0 million and non-GAAP earnings per share of $0.62 to $0.64.

The detailed financial outlook is presented in the following table:

During the earnings call, management indicated expectations for 13-14% revenue growth in 2026, with a target operating margin exceeding 23% by Q4 2026. CFO Tyler Sloat noted the company has "strung together four really, really good quarters," reflecting confidence in Freshworks' execution despite the moderating growth rate.

While Freshworks continues to show solid financial performance, the company faces ongoing challenges including competition from larger incumbents and potential macroeconomic pressures affecting enterprise spending. The gradual slowing of year-over-year growth rates will likely be a focus for investors in coming quarters, even as profitability metrics continue to improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.