AZTR receives NYSE delisting warning over equity requirement

Introduction & Market Context

Frontdoor Inc (NASDAQ:FTDR) reported strong second-quarter 2025 results on August 5, with double-digit growth across key financial metrics, prompting management to raise its full-year guidance. The home warranty provider’s stock rose 4.96% in premarket trading to $61.39, building on its recent momentum.

The company’s performance comes amid a gradual shift in the housing market from a seller’s to a buyer’s market, with rising inventory levels providing a more favorable backdrop for Frontdoor’s services. Despite continued macroeconomic challenges, including high mortgage rates and low home sales volumes, Frontdoor has successfully stabilized its warranty business while accelerating growth in non-warranty revenue streams.

Quarterly Performance Highlights

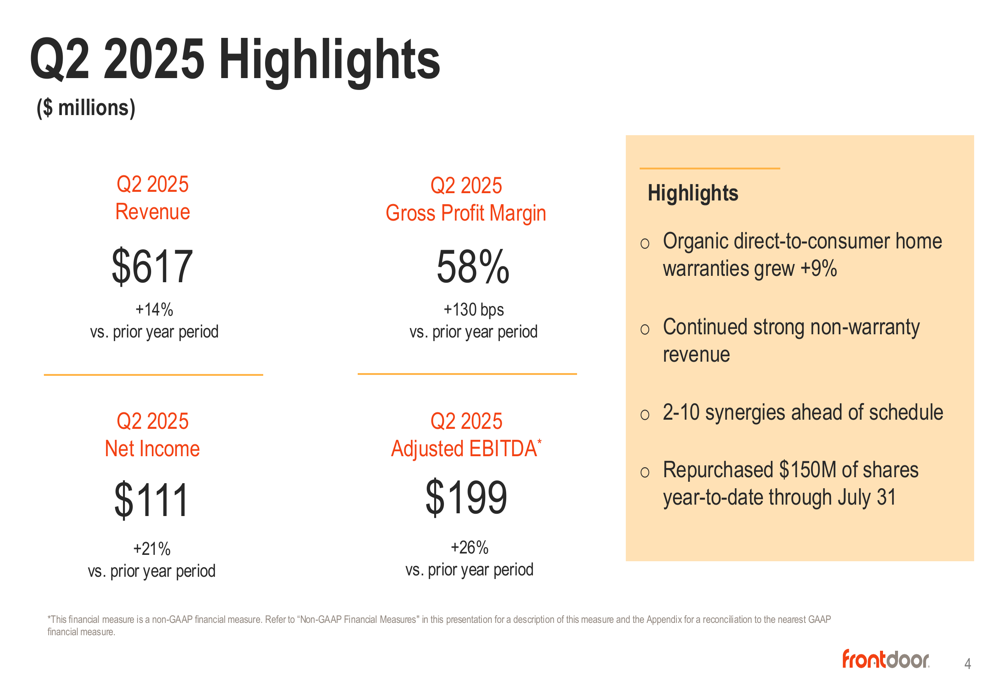

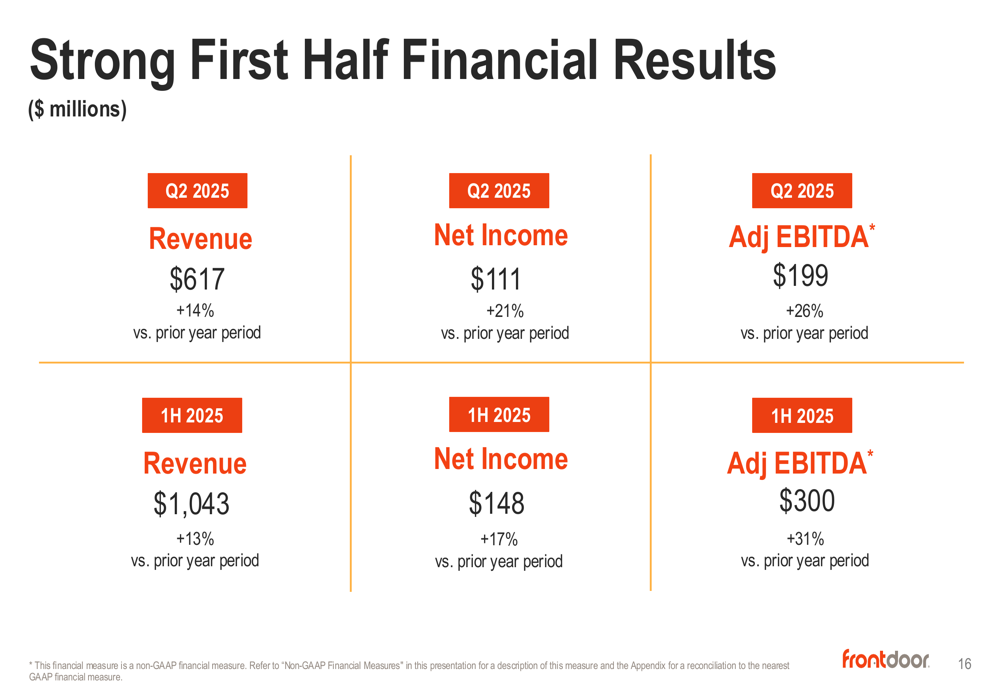

Frontdoor delivered impressive financial results for the second quarter, with revenue reaching $617 million, a 14% increase compared to the same period last year. This growth was driven by a combination of price increases (+2%) and volume growth (+12%).

As shown in the following chart of Q2 2025 highlights, the company achieved significant improvements across all key financial metrics:

Net income rose 21% year-over-year to $111 million, while adjusted EBITDA increased 26% to $199 million, representing a margin of 32% (up 320 basis points). Gross profit margin improved to 58%, up 130 basis points from the prior year period, reflecting the company’s enhanced operational efficiency and pricing strategies.

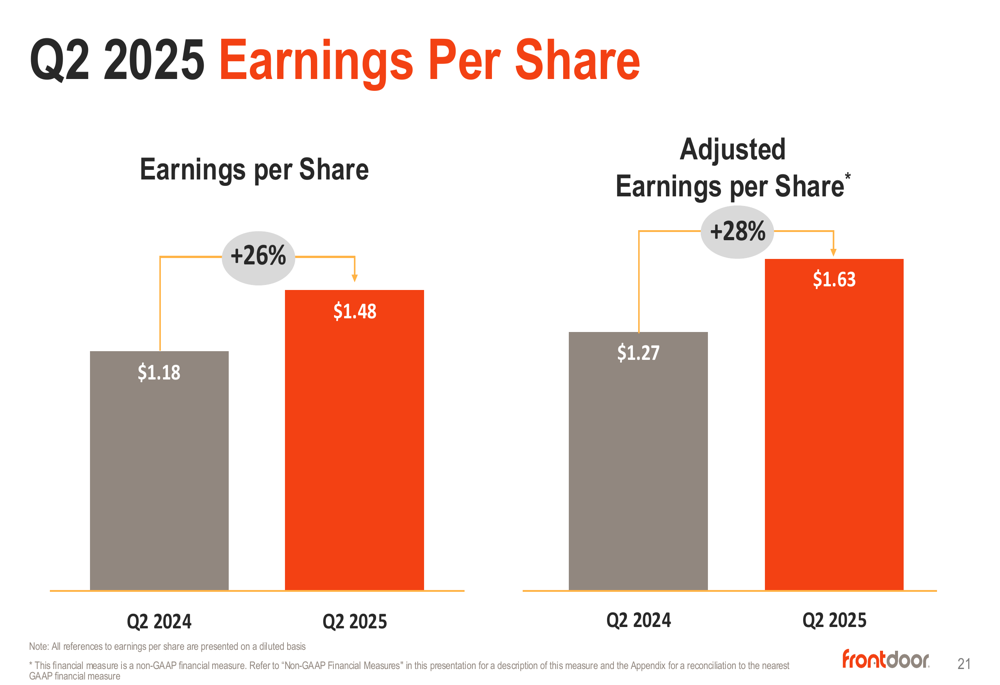

The strong performance extended to earnings per share, which grew 26% to $1.48, while adjusted earnings per share increased 28% to $1.63.

For the first half of 2025, Frontdoor’s results were equally robust, with revenue of $1.04 billion (+13%), net income of $148 million (+17%), and adjusted EBITDA of $300 million (+31%).

Strategic Initiatives

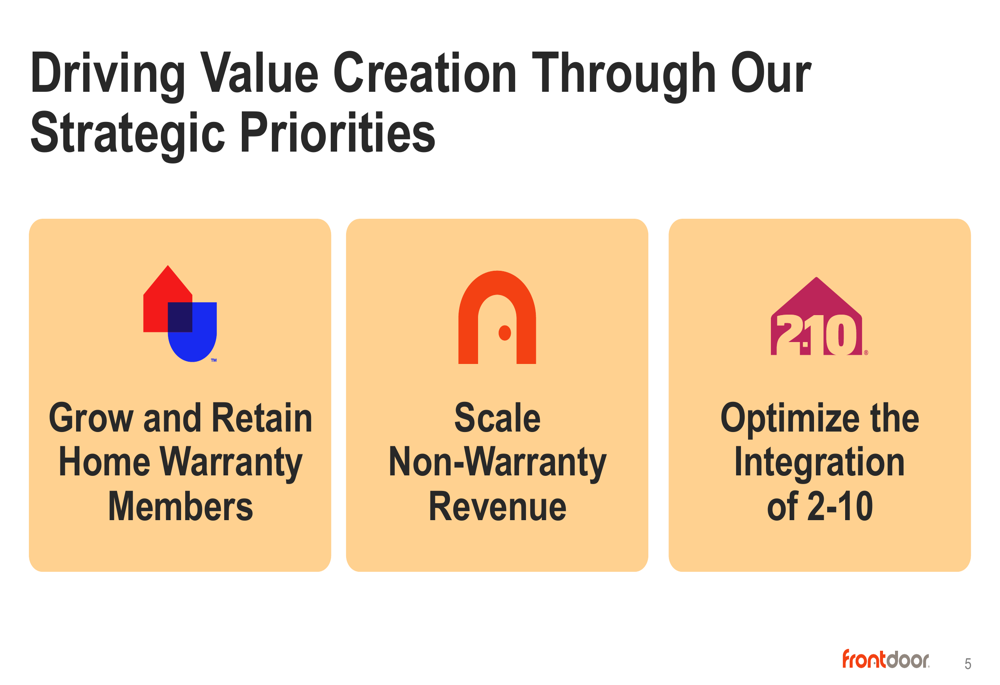

Frontdoor’s strategic focus centers on three key priorities: growing and retaining home warranty members, scaling non-warranty revenue, and optimizing the integration of 2-10, a complementary home warranty business acquired previously.

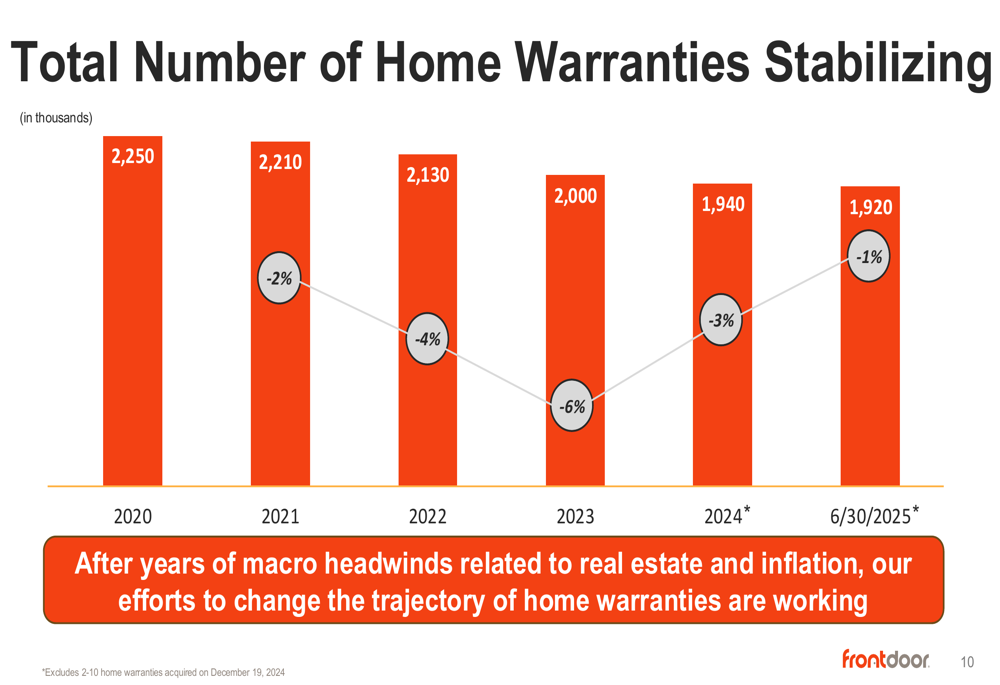

After years of decline due to macroeconomic headwinds, Frontdoor has successfully stabilized its total number of home warranties. As illustrated in the following chart, the total number of warranties decreased by just 1% in the first half of 2025, compared to steeper declines in previous years:

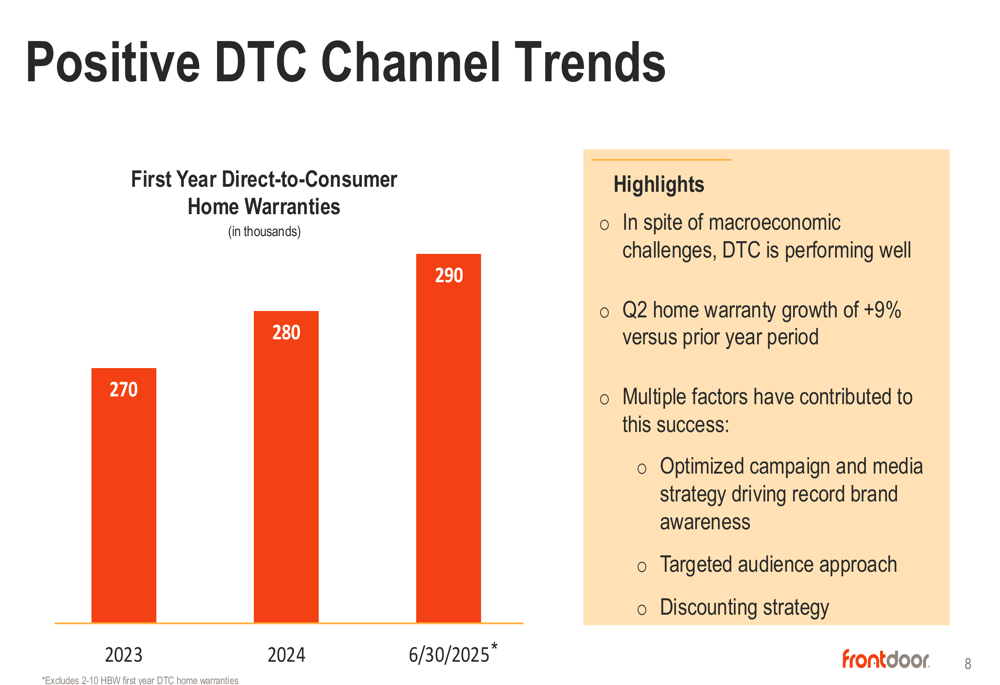

This stabilization has been achieved despite continued challenges in the real estate channel, where first-year home warranties have declined significantly since 2020. The company has offset this weakness through strong performance in its direct-to-consumer (DTC) channel, which grew 9% in Q2 2025.

Customer retention remains strong at 78.3%, supported by initiatives such as preferred contractor deployment, technology advancements including a mobile app (downloaded by 14% of members), and high autopay enrollment (84% of members).

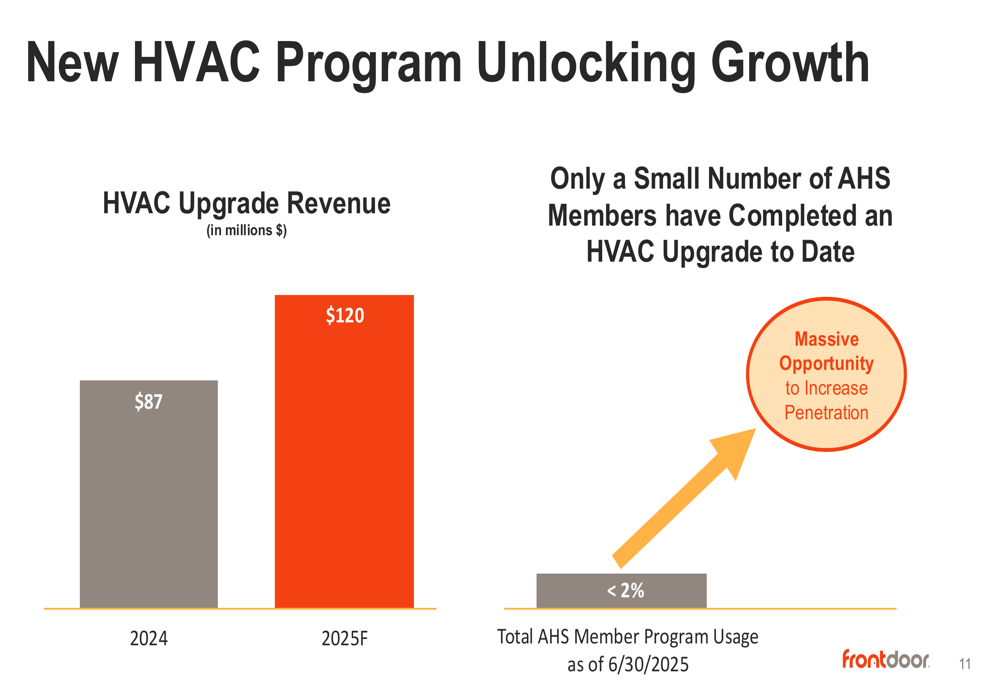

Frontdoor is also seeing significant growth in its non-warranty revenue, particularly through its HVAC upgrade program. This initiative is projected to generate $120 million in revenue for 2025, up from $87 million in 2024, with substantial room for further penetration as current usage among American Home Shield members is less than 2%.

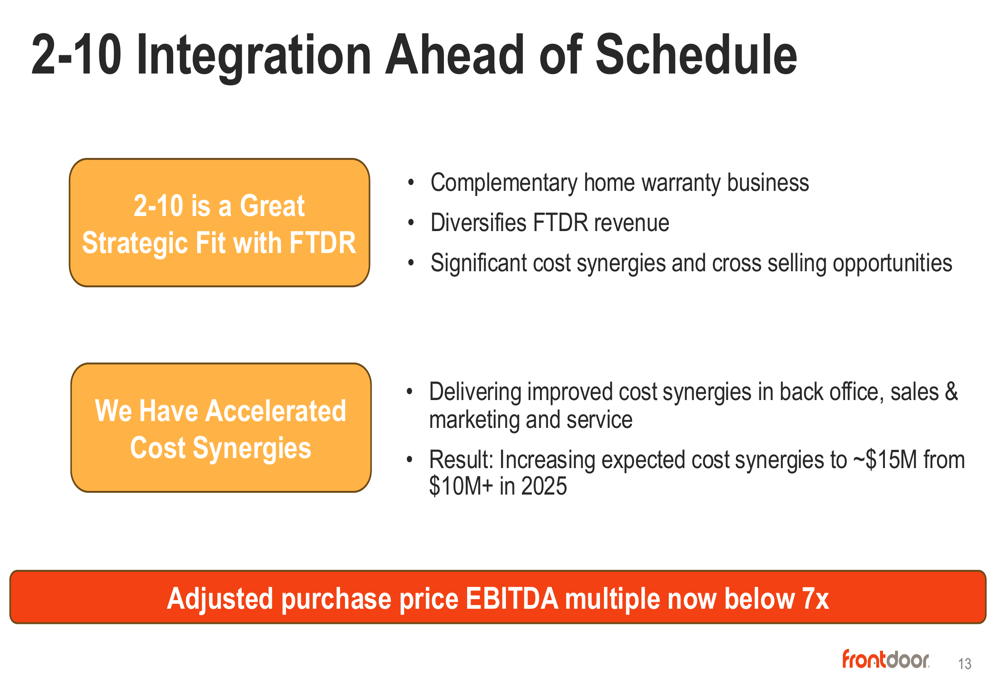

The integration of 2-10 is proceeding ahead of schedule, with cost synergies now expected to reach approximately $15 million in 2025, up from the initial target of $10+ million. The adjusted purchase price EBITDA multiple has improved to below 7x.

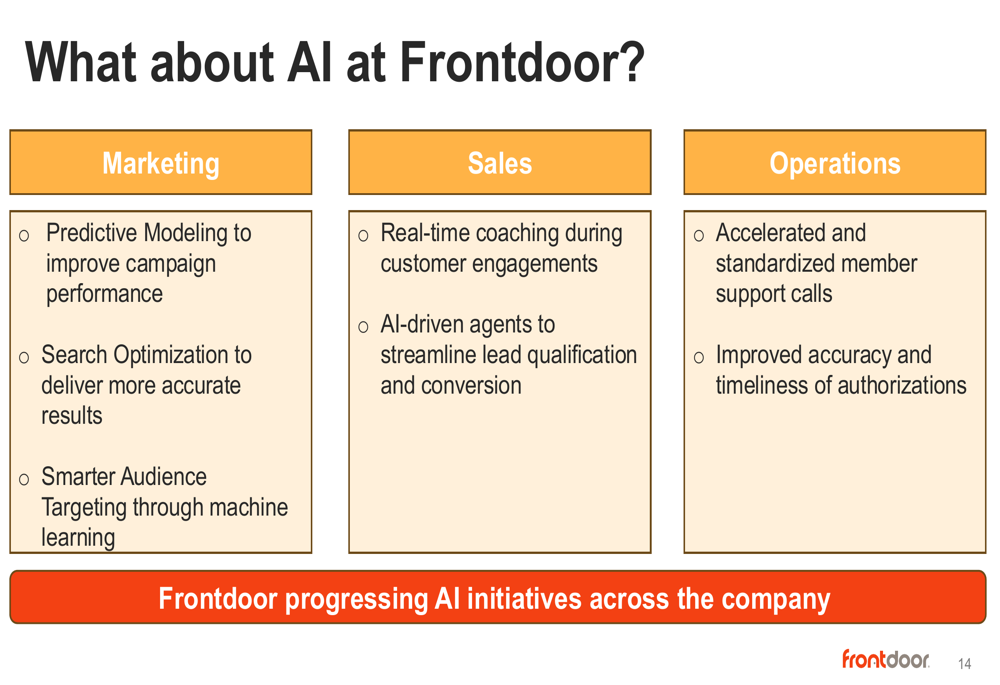

Frontdoor is also leveraging artificial intelligence across its business operations to enhance marketing effectiveness, sales performance, and operational efficiency:

Cash Flow and Capital Allocation

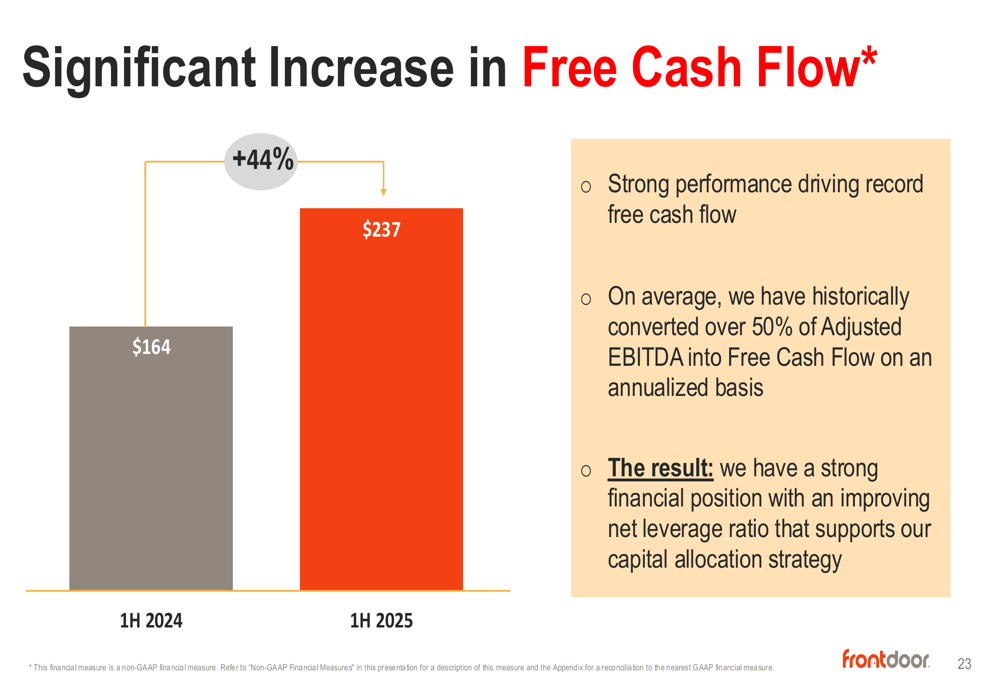

Frontdoor’s strong operational performance has translated into robust cash flow generation. Free cash flow for the first half of 2025 increased 44% to $237 million compared to the same period in 2024.

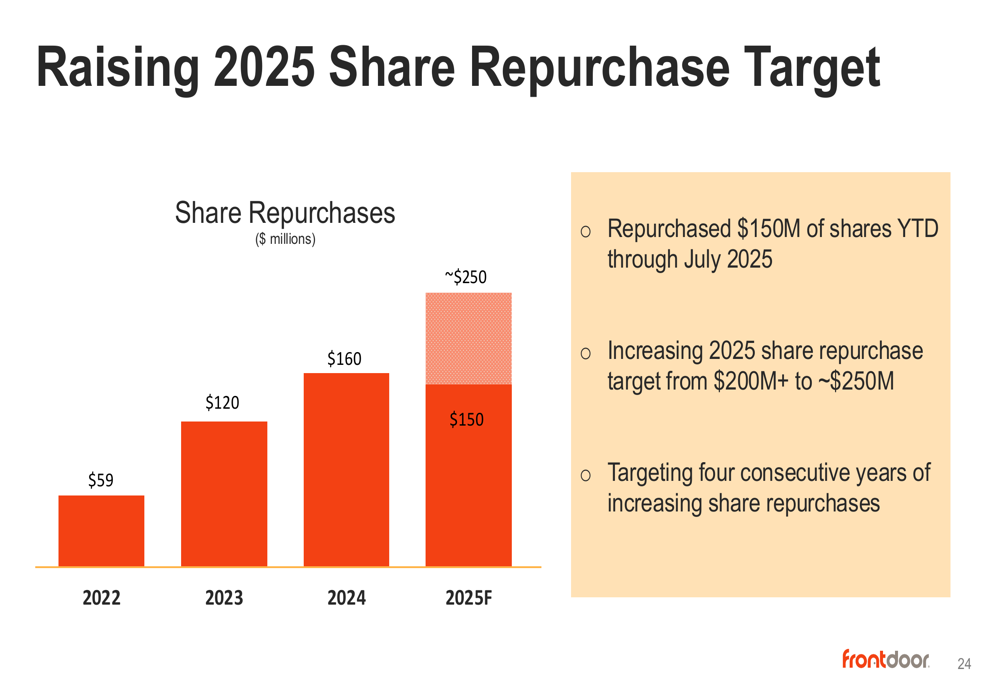

This strong cash generation has enabled Frontdoor to significantly increase its share repurchase program. The company has already repurchased $150 million of shares year-to-date through July 31 and has raised its 2025 share repurchase target from $200+ million to approximately $250 million, marking the fourth consecutive year of increasing share repurchases.

Forward-Looking Statements

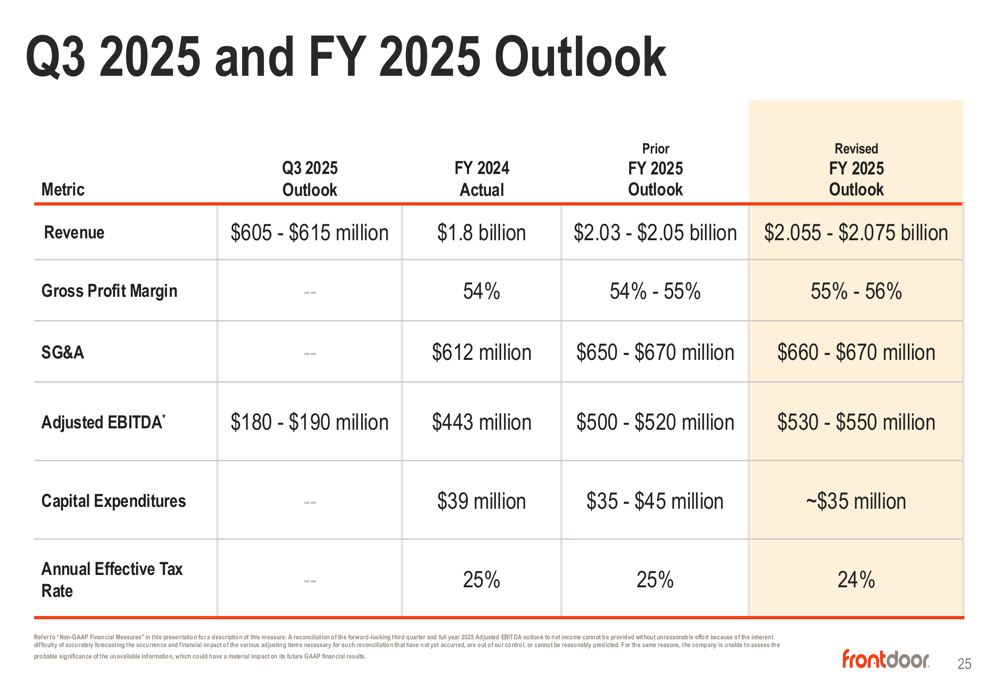

Based on its strong first-half performance, Frontdoor has raised its full-year 2025 guidance. The company now expects revenue of $2.055-$2.075 billion, up from its previous outlook of $2.03-$2.05 billion. Adjusted EBITDA guidance has been increased to $530-$550 million, compared to the previous range of $500-$520 million.

For the third quarter of 2025, Frontdoor projects revenue of $605-$615 million and adjusted EBITDA of $180-$190 million.

The company also improved its gross profit margin outlook to 55-56% (up from 54-55%) and lowered its expected annual effective tax rate to 24% (down from 25%).

Conclusion

Frontdoor’s Q2 2025 results demonstrate the company’s ability to execute effectively despite challenging macroeconomic conditions. The stabilization of its core warranty business, combined with strong growth in non-warranty revenue and successful integration of acquisitions, positions the company well for continued growth.

The raised guidance reflects management’s confidence in the company’s trajectory for the remainder of 2025. With strong cash flow generation supporting increased share repurchases and investments in strategic initiatives, Frontdoor appears well-positioned to maintain its positive momentum.

Following the 15.79% stock price surge after Q1 results and the current 4.96% premarket increase, investor sentiment appears increasingly positive about Frontdoor’s strategic direction and financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.