NVIDIA expands Microsoft partnership with Blackwell GPUs for AI infrastructure

Introduction & Market Context

Frontdoor Inc. (NASDAQ:FTDR), a leading provider of home service plans, reported strong third-quarter 2025 results on November 5, with double-digit growth across key financial metrics. Despite the positive performance, shares fell 5.72% in regular trading, following a 3.47% decline in premarket activity, suggesting investors may have expected even stronger results or were concerned about specific aspects of the company’s outlook.

The company’s stock, which had surged 11.3% following its Q2 2025 earnings announcement, is now trading at $61.98, down from its previous close of $65.74, but still well above its 52-week low of $35.61.

Quarterly Performance Highlights

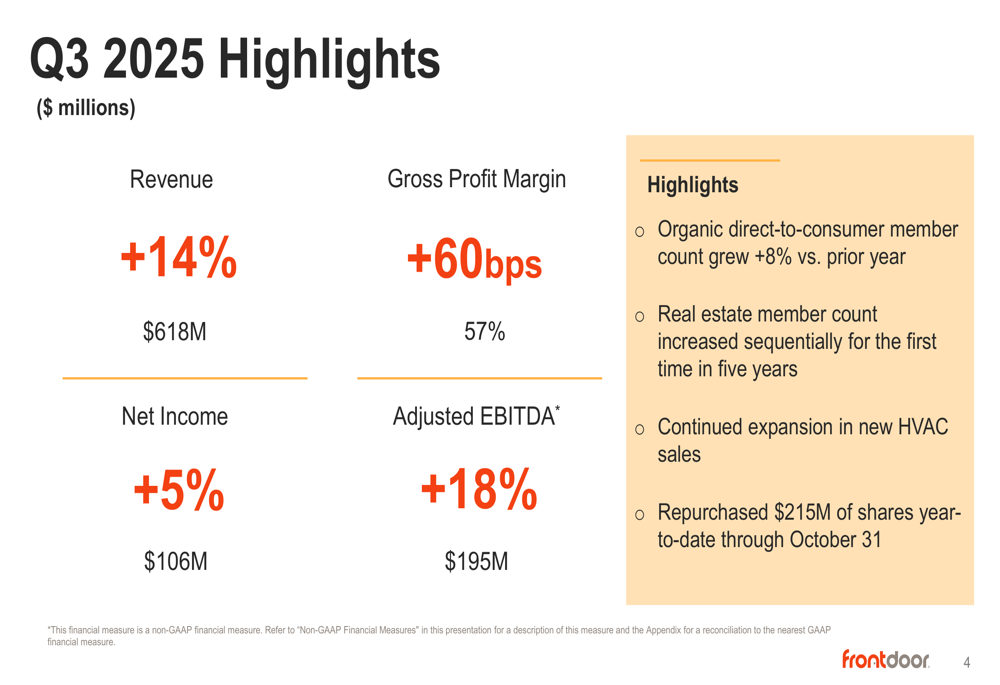

Frontdoor delivered impressive financial results for the third quarter of 2025, continuing the momentum from its strong second quarter performance.

As shown in the following key performance metrics:

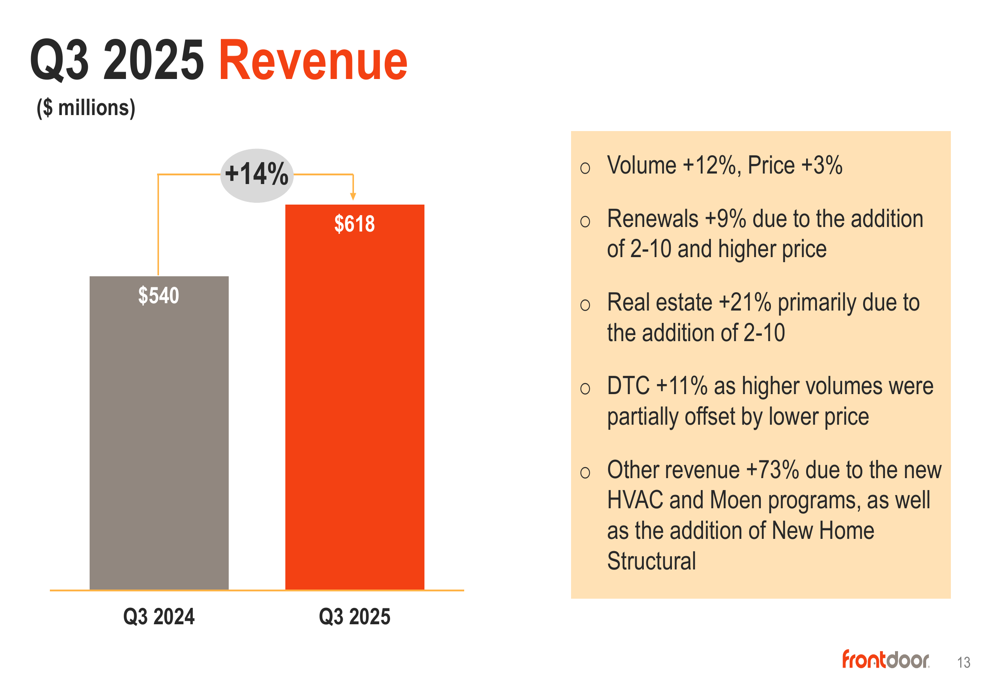

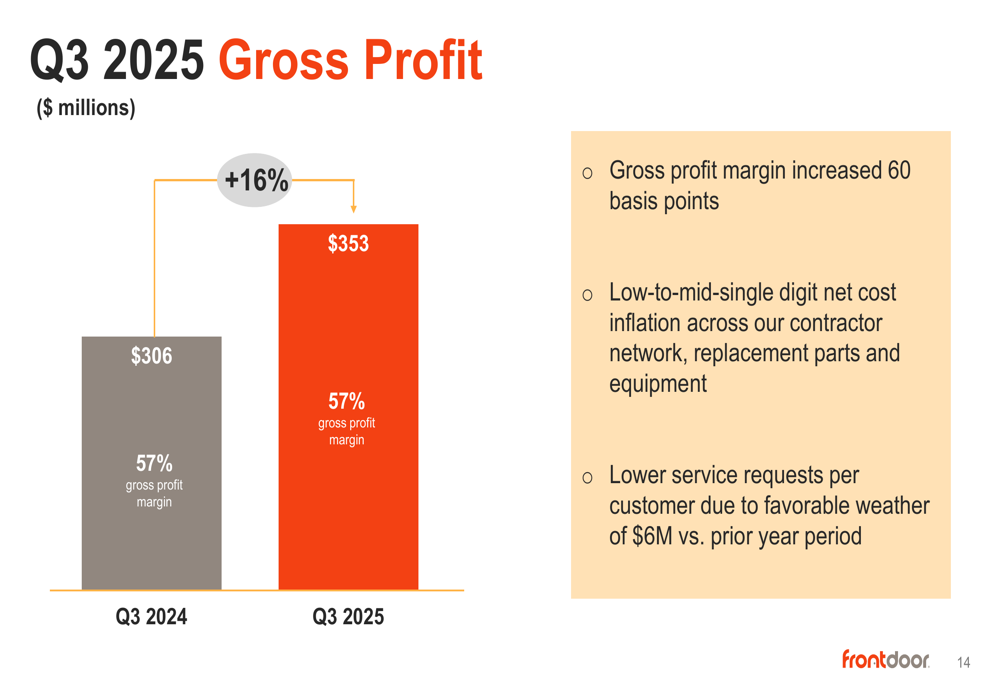

Revenue increased 14% year-over-year to $618 million, while gross profit margin improved by 60 basis points to 57%. Net income rose 5% to $106 million, and adjusted EBITDA jumped 18% to $195 million. These results were driven by organic direct-to-consumer member growth of 8% year-over-year and the first sequential increase in real estate member count in five years.

CEO Bill Cobb, who previously stated "Frontdoor continues to deliver" during the Q2 earnings call, highlighted the company’s operational excellence and strategic growth initiatives as key drivers of the strong performance.

Strategic Initiatives

Frontdoor’s presentation emphasized five key areas where the company is building momentum: operational excellence, positive direct-to-consumer (DTC) unit growth, improving real estate channel, continued strong retention rates, and expanding non-warranty services.

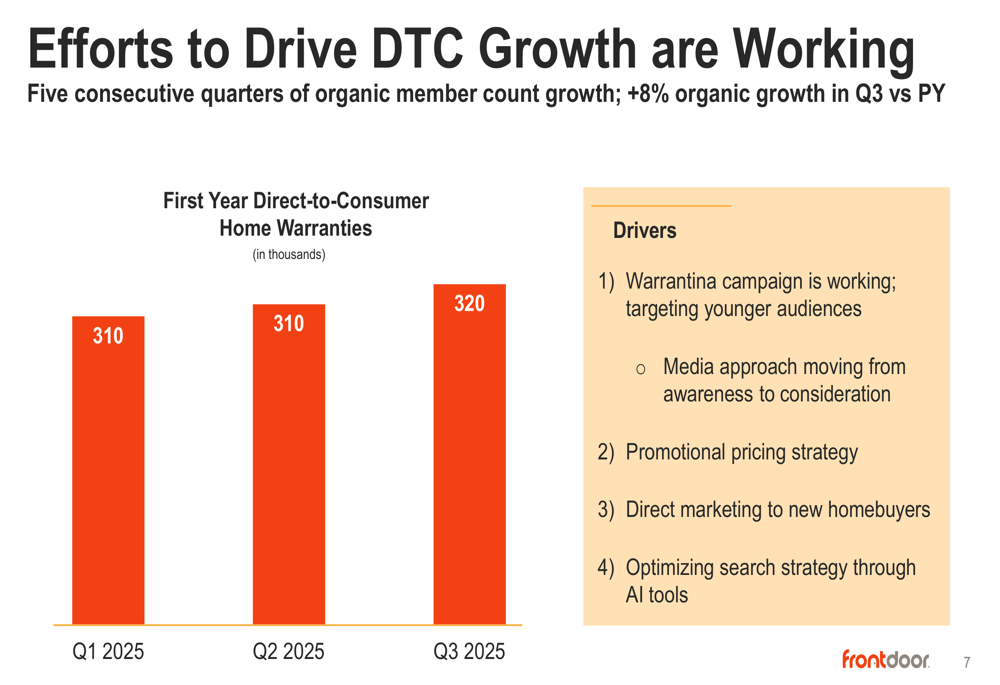

The company’s DTC growth strategy has yielded positive results for five consecutive quarters, with organic member count growth of 8% in Q3 compared to the prior year:

This growth has been fueled by the successful "Warrantina" marketing campaign, promotional pricing strategies, direct marketing to new homebuyers, and optimized search strategies leveraging AI tools. The campaign has shown particularly strong resonance with consumers under 45 years old.

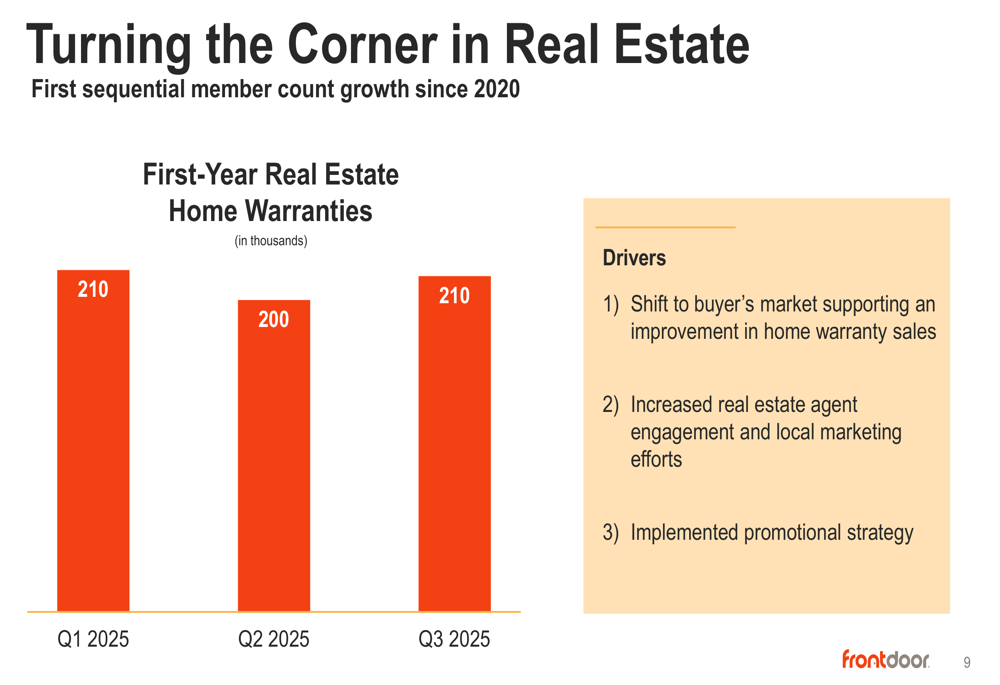

After years of challenges, Frontdoor’s real estate channel is showing signs of recovery:

The first sequential member count growth since 2020 represents a significant turnaround, attributed to a shift to a buyer’s market, increased real estate agent engagement, local marketing efforts, and an effective promotional strategy.

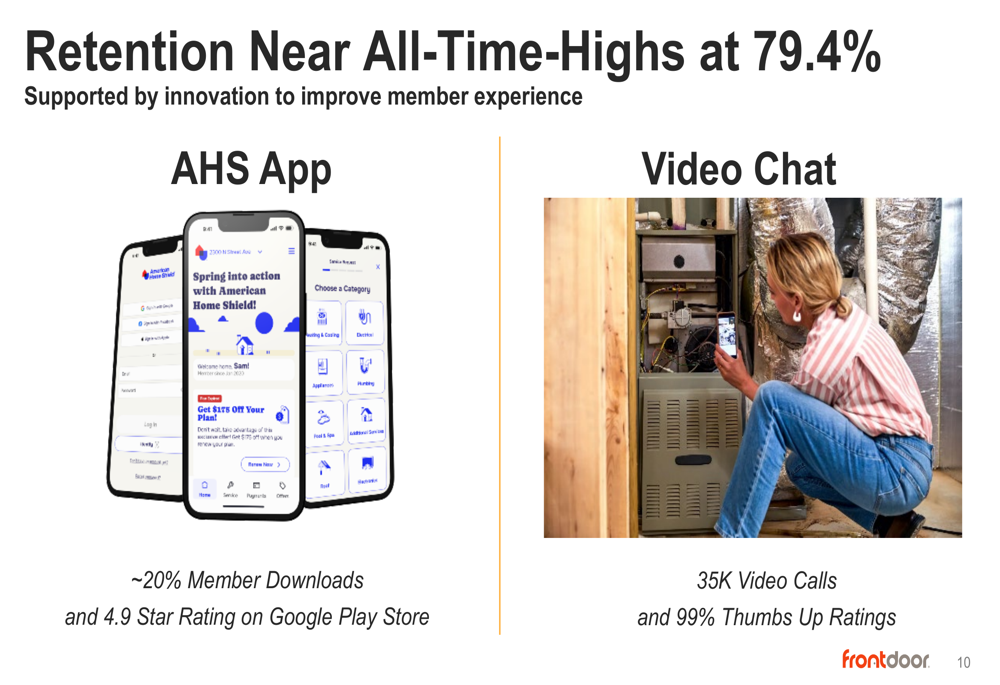

Customer retention remains a strength for Frontdoor, with rates near all-time highs at 79.4%:

The company’s focus on innovation to improve member experience has yielded positive results, with approximately 20% of members downloading the AHS App (which maintains a 4.9-star rating on Google Play Store) and 35,000 video calls conducted with a 99% thumbs-up rating.

Detailed Financial Analysis

Frontdoor’s revenue growth of 14% was driven by multiple factors, including volume growth of 12% and price increases of 3%:

The revenue breakdown shows renewals up 9%, real estate revenue up 21% (primarily due to the addition of 2-10), direct-to-consumer up 11%, and other revenue up 73% due to new HVAC and Moen programs, as well as the addition of New Home Structural.

Gross profit increased 16% year-over-year, with a margin expansion of 60 basis points:

The company managed to offset low-to-mid-single digit net cost inflation across its contractor network, replacement parts, and equipment through pricing actions and operational efficiencies. Favorable weather conditions also contributed $6 million in savings compared to the prior year period.

Earnings per share showed strong growth, with diluted EPS up 9% to $1.42 and adjusted EPS increasing 15% to $1.58:

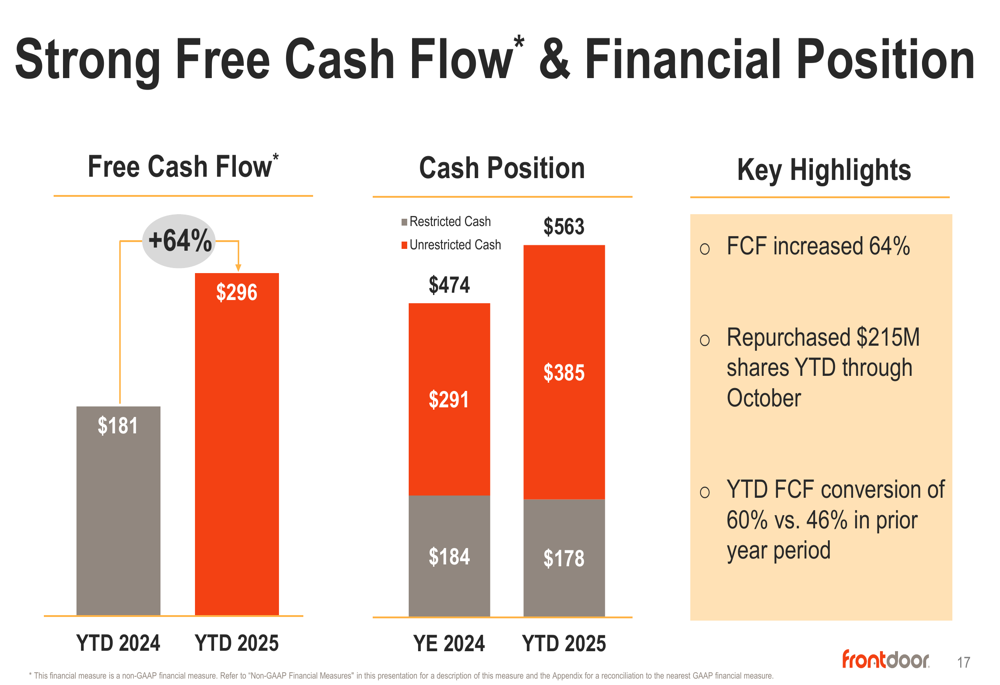

Free cash flow generation has been particularly impressive, with a 64% increase year-to-date to $296 million:

The company’s FCF conversion improved to 60% year-to-date, compared to 46% in the prior year period. Frontdoor has leveraged this strong cash position to repurchase $215 million in shares through October 31, 2025.

Forward-Looking Statements

Frontdoor provided guidance for both the fourth quarter and full year 2025:

For Q4 2025, the company expects revenue between $415 million and $425 million, with adjusted EBITDA between $50 million and $55 million.

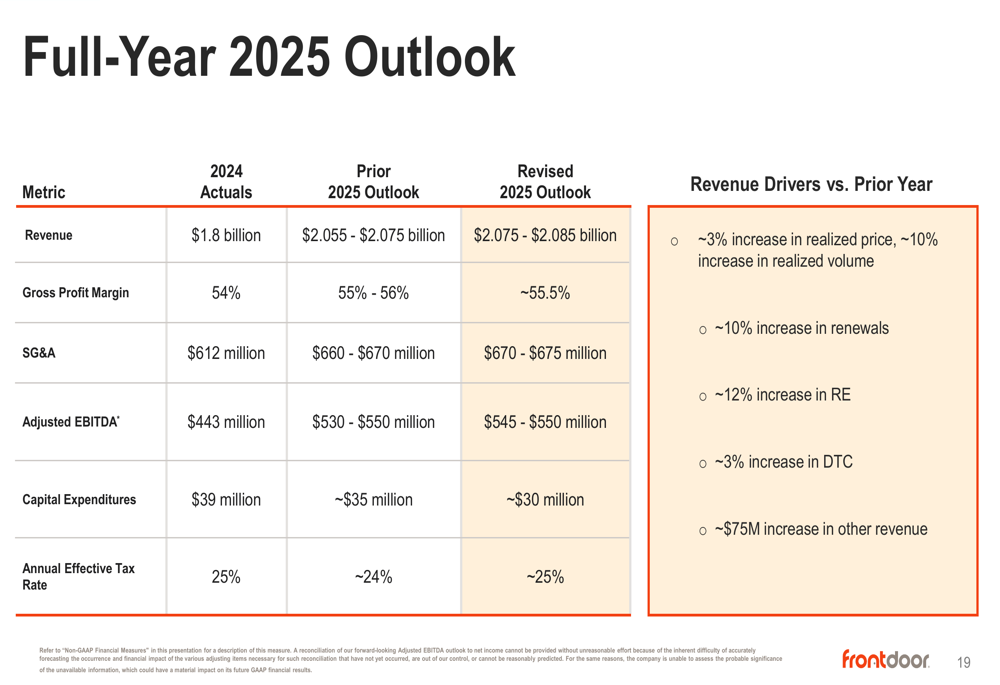

The full-year 2025 outlook was raised slightly from previous guidance, with revenue now projected at $2.075-$2.085 billion (up from $2.055-$2.075 billion) and adjusted EBITDA at $545-$550 million. The company anticipates a gross profit margin of approximately 55.5% and capital expenditures of around $30 million.

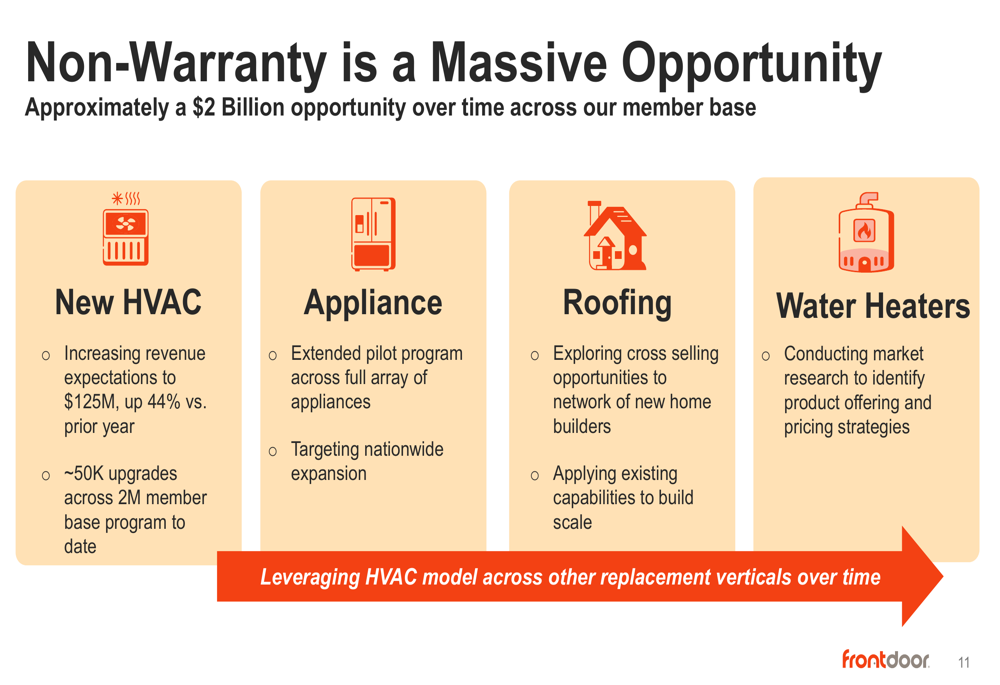

A significant growth opportunity lies in non-warranty services, which Frontdoor estimates represents a $2 billion opportunity across its member base:

The company’s new HVAC program is expected to generate $125 million in revenue, up 44% versus the prior year. Frontdoor is also expanding pilot programs for appliances, exploring cross-selling opportunities for roofing, and conducting market research for water heater offerings.

Despite the strong results and raised outlook, the market’s negative reaction suggests investors may have concerns about the sustainability of growth or the impact of potential economic headwinds on the home service sector. However, with its strong cash position, expanding service offerings, and improving operational metrics, Frontdoor appears well-positioned to continue its growth trajectory into 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.