Gold bars to be exempt from tariffs, White House clarifies

Introduction & Market Context

Funko Inc (NASDAQ:FNKO) released its Q2 2025 supplemental information presentation on August 7, highlighting strategic initiatives and top-performing properties while the company faces significant financial challenges. The presentation comes as Funko’s stock has declined over 68% year-to-date, with shares dropping an additional 8.74% in premarket trading to $3.34 following the release.

The pop culture collectibles company is attempting to navigate a difficult financial landscape after reporting a wider-than-expected loss in Q1 2025, with earnings per share at -$0.33 against a forecast of -$0.11. Despite these challenges, the presentation focused on growth opportunities, international expansion, and the company’s product portfolio performance.

Quarterly Performance Highlights

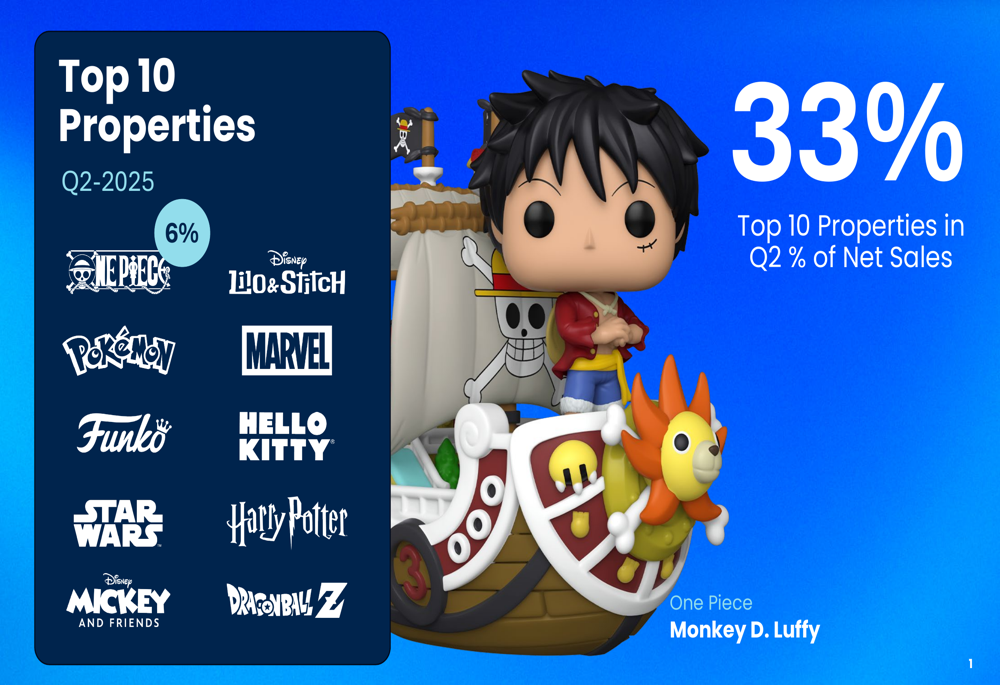

Funko’s presentation revealed that its top 10 properties accounted for 33% of net sales in Q2 2025, with the anime franchise One Piece representing 6% of total sales. The remaining top properties include major entertainment franchises such as Disney (NYSE:DIS)’s Lilo & Stitch, Pokémon, Marvel, Star Wars, Harry Potter, and Dragon Ball (NYSE:BALL) Z, alongside Funko’s own branded products, Hello Kitty, and Disney Mickey and Friends.

As shown in the following image highlighting Funko’s top-performing properties:

This concentration of sales among key franchises demonstrates Funko’s continued reliance on major entertainment properties, with anime franchises like One Piece and Dragon Ball Z featuring prominently in the company’s portfolio. The diversification across Disney, Warner Bros., and Nintendo properties suggests Funko maintains strong licensing relationships despite its financial difficulties.

Strategic Initiatives

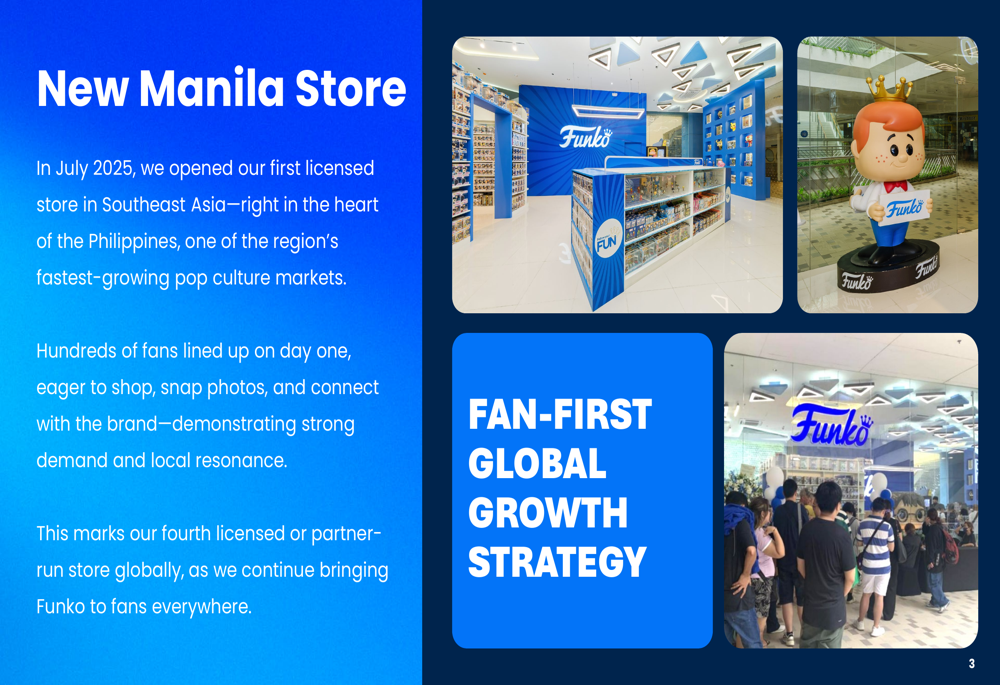

A key focus of Funko’s Q2 presentation was its international expansion strategy, highlighted by the opening of its first licensed store in Southeast Asia. Located in Manila, Philippines, the store opened in July 2025 and represents Funko’s fourth licensed or partner-run store globally.

The company emphasized the fast-growing pop culture market in Southeast Asia and noted strong consumer demand, with fans lining up on opening day. This expansion aligns with what the company describes as its "fan-first global growth strategy."

The following image showcases Funko’s new Manila store:

In addition to retail expansion, Funko highlighted its significant presence at San Diego Comic-Con (SDCC) 2025, where it hosted what it described as the largest physical footprint at the event. The company created four immersive zones in its "Funkoville" area, featuring its Bitty Pop!, Funko, Loungefly, and Mondo brands.

According to the presentation, all activations experienced high traffic, with product sellouts occurring daily. The company designed these experiences to "engage collectors of every age and fandom," reinforcing its focus on community building and direct consumer engagement.

The following image illustrates Funko’s presence at San Diego Comic-Con 2025:

Financial Reality Check

While Funko’s presentation emphasized growth initiatives and brand strength, it notably lacked financial details that would provide context for these developments. Based on the company’s Q1 2025 earnings report, Funko faces significant challenges, including a net loss of $17.8 million and total debt of $202.2 million, which increased by $19.4 million from the previous quarter.

The company previously withdrew its full-year 2025 outlook due to tariff uncertainties and is working to mitigate an estimated $45 million in incremental tariff costs. These financial pressures stand in stark contrast to the growth-focused narrative presented in the Q2 slides.

Operational improvements mentioned in previous communications include a 20% global workforce reduction and sourcing diversification, though these cost-cutting measures weren’t addressed in the current presentation.

Forward-Looking Statements

While the Q2 presentation doesn’t provide explicit forward guidance, Funko’s focus on international expansion and event marketing suggests the company is pursuing growth opportunities despite its financial challenges. The emphasis on top properties indicates Funko continues to leverage strong licensing relationships with major entertainment companies.

In previous communications, CEO Cynthia Williams stated, "We’re staying disciplined, moving with speed, and adjusting in real time to protect the business," highlighting the company’s proactive approach to operational challenges. The Q2 presentation appears to align with this strategy, focusing on targeted growth initiatives while presumably continuing cost-control measures behind the scenes.

Analysts tracked by InvestingPro maintain a moderate outlook for Funko, with consensus forecasts expecting the company to return to profitability this year with projected earnings of $0.13 per share. However, the recent premarket trading decline suggests investors may be skeptical about the company’s ability to overcome its current challenges through the initiatives highlighted in the Q2 presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.