EUR/USD likely to find a peak near 1.25: UBS

Gates Industrial Corporation plc (NYSE:GTES) reported a return to positive core sales growth in its Q1 2025 earnings presentation on April 30, 2025. The industrial manufacturer posted 1.4% year-over-year core sales growth, with particularly strong performance in replacement channels and mobility segments, while maintaining its full-year guidance despite facing significant tariff headwinds.

Quarterly Performance Highlights

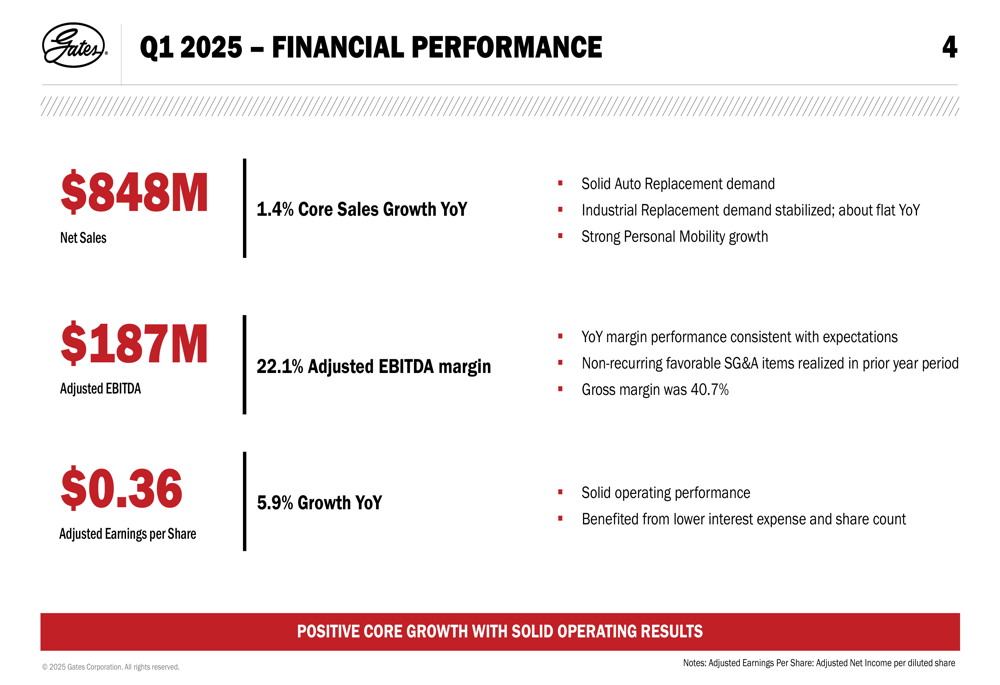

Gates reported net sales of $848 million for the first quarter of 2025, representing a 1.4% core sales growth compared to the same period last year. The company achieved an adjusted EBITDA of $187 million with a 22.1% margin, while adjusted earnings per share reached $0.36, marking a 5.9% increase year-over-year.

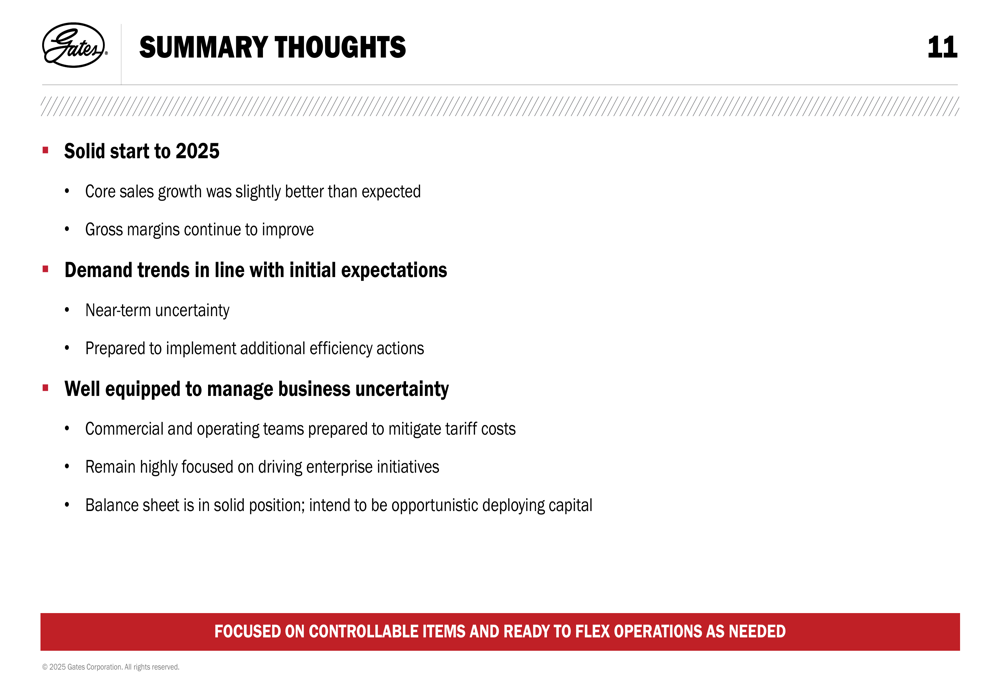

"We had a solid start to 2025, with core sales growth slightly better than expected and gross margins continuing to improve," the company noted in its presentation summary. Gross margin expanded to 40.7%, while net leverage declined slightly year-over-year to 2.3x.

As shown in the following financial performance overview:

The company highlighted strong automotive replacement demand and stabilized industrial replacement demand, which remained approximately flat year-over-year. Personal mobility continued to show robust growth, with the segment growing over 30% compared to Q1 2024.

Segment and Regional Analysis

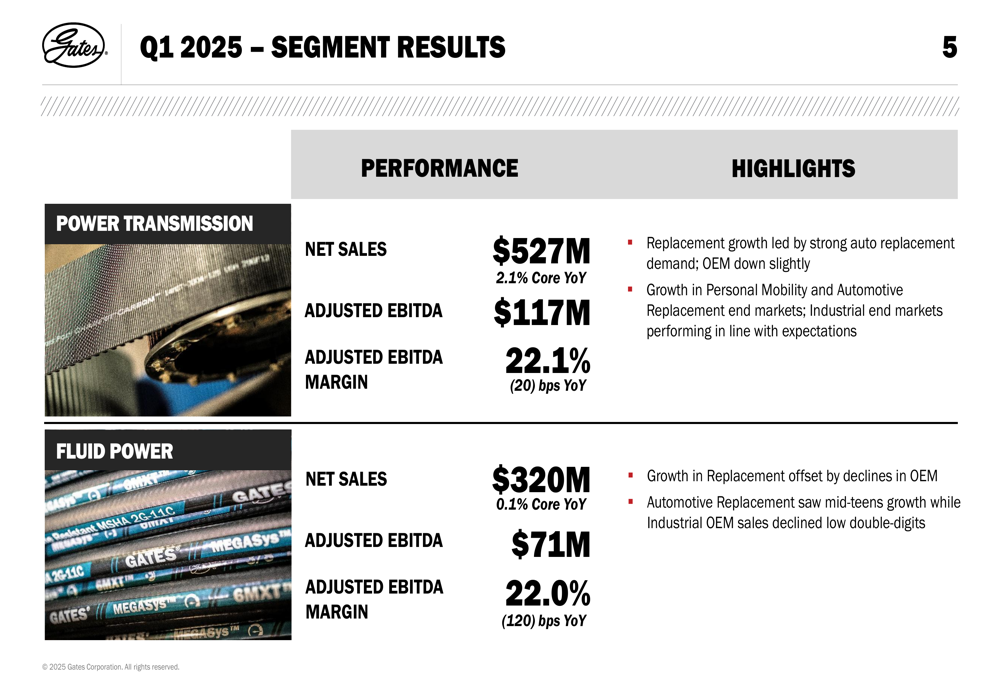

Gates operates through two primary segments: Power Transmission and Fluid Power. The Power Transmission segment generated $527 million in net sales, representing a 2.1% core growth year-over-year, with an adjusted EBITDA of $117 million and a 22.1% margin. Meanwhile, the Fluid Power segment recorded $320 million in net sales with 0.1% core growth, generating $71 million in adjusted EBITDA with a 22.0% margin.

The segment breakdown reveals that replacement channel growth was led by strong automotive replacement demand, while OEM sales declined:

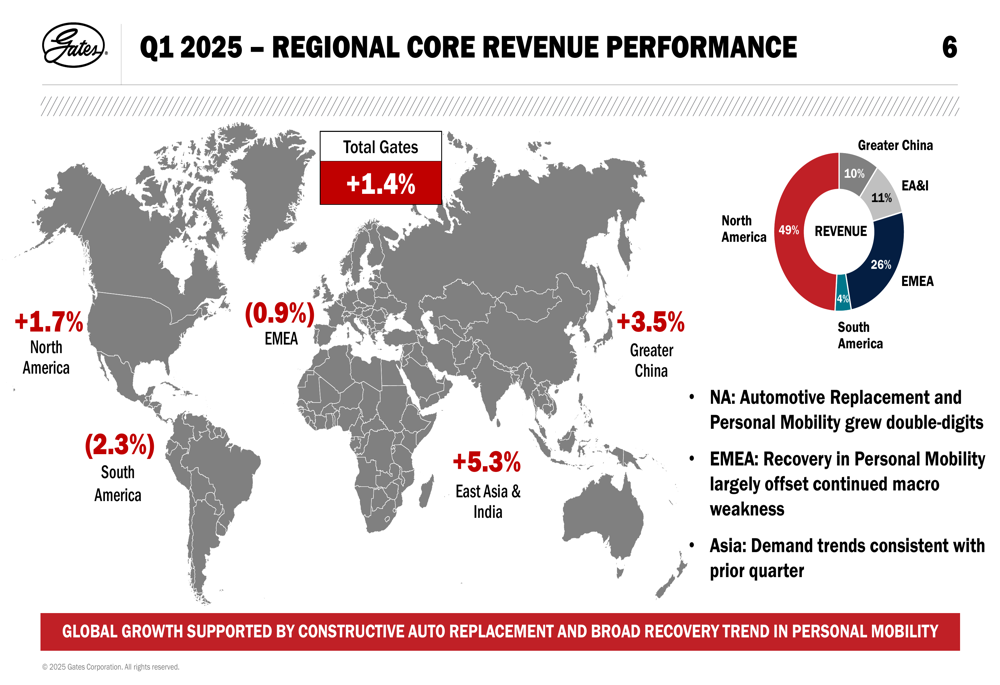

From a regional perspective, Gates experienced varied performance across its global operations. North America grew by 1.7%, East Asia & India by 5.3%, and Greater China by 3.5%, while EMEA declined by 0.9%. The company noted that automotive replacement and personal mobility in North America grew by double digits, while recovery in personal mobility in EMEA largely offset continued macroeconomic weakness in the region.

The following map illustrates the regional core revenue performance:

Capital Efficiency and Cash Flow

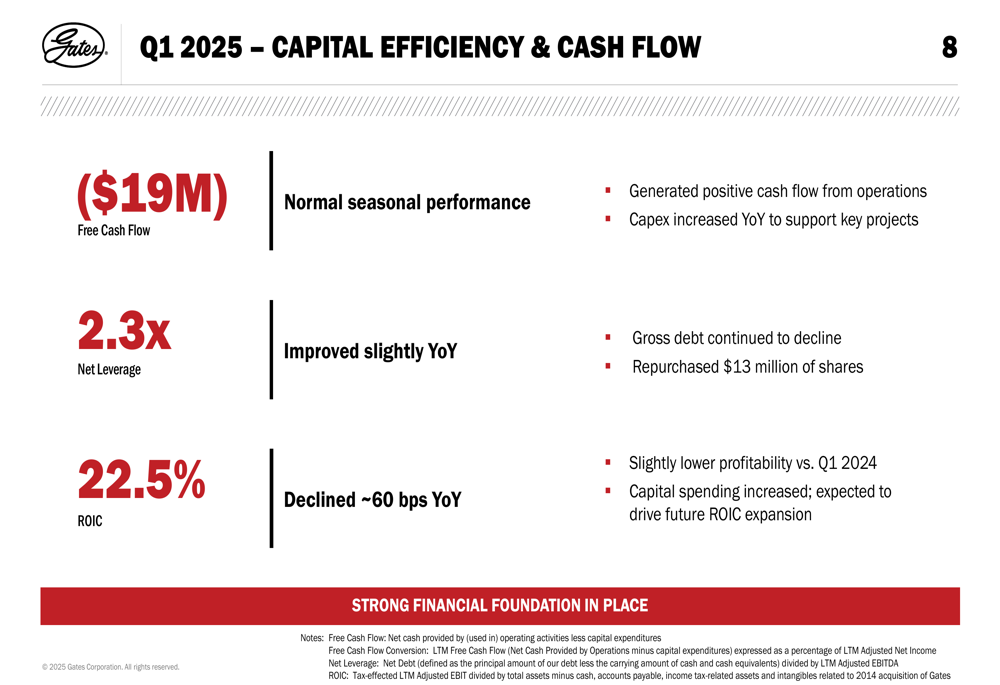

Gates reported negative free cash flow of $19 million for the quarter, which the company described as normal seasonal performance. Return on invested capital (ROIC) was 22.5%, reflecting a decline of approximately 60 basis points year-over-year.

The company continued its share repurchase program, buying back $13 million of stock during the quarter, with over $100 million remaining under the existing authorization. Capital expenditures increased year-over-year to support key projects, which the company expects will drive future ROIC expansion.

The following chart details the company’s capital efficiency and cash flow metrics:

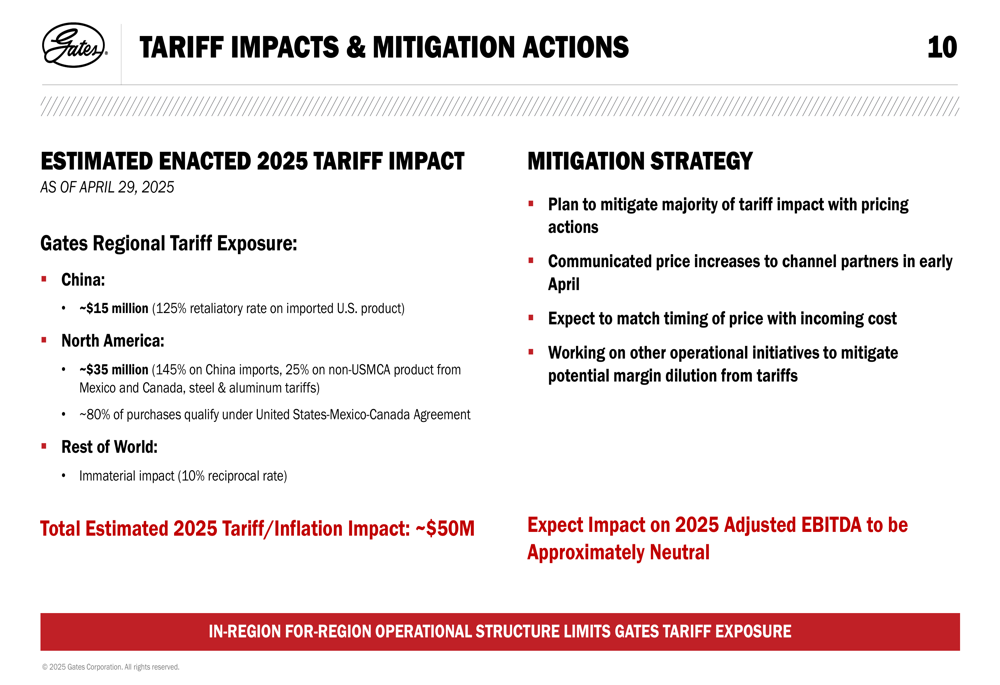

Tariff Impacts and Mitigation Strategy

A significant focus of Gates’ presentation was its strategy for addressing tariff impacts. The company estimates a total tariff and inflation impact of approximately $50 million for 2025, with regional breakdowns of approximately $15 million for China and $35 million for North America.

Gates outlined its mitigation strategy, which includes implementing pricing actions to offset the majority of the tariff impact. The company is actively communicating price increases and working to match the timing of price adjustments with incoming costs, while also pursuing other operational initiatives. Overall, Gates expects the impact on 2025 adjusted EBITDA to be approximately neutral.

Forward-Looking Statements

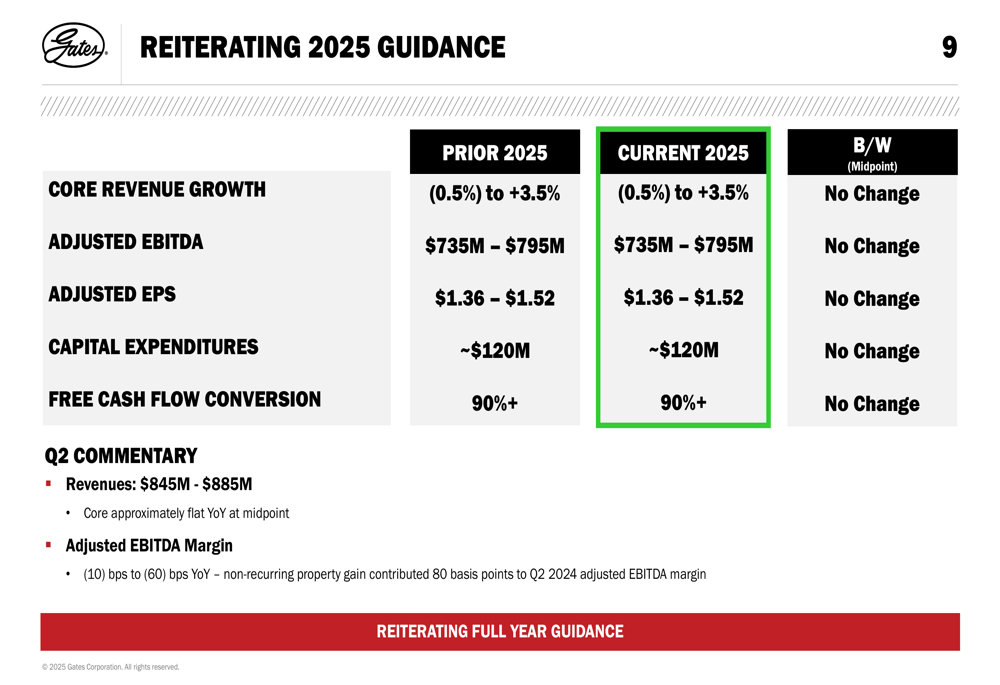

Gates reaffirmed its full-year 2025 guidance, maintaining its previous projections for core revenue growth of -0.5% to +3.5%, adjusted EBITDA of $735-$795 million, and adjusted EPS of $1.36-$1.52. The company also provided specific guidance for Q2 2025, projecting revenues of $845-$885 million, with core growth approximately flat year-over-year at the midpoint.

The following table details the company’s unchanged 2025 guidance:

For the second quarter, Gates noted that adjusted EBITDA margin is expected to be 10 to 60 basis points lower year-over-year, primarily due to a non-recurring property gain that contributed 80 basis points to Q2 2024’s adjusted EBITDA margin.

In its summary thoughts, Gates emphasized that it is well-equipped to manage business uncertainty, with commercial and operating teams prepared to mitigate tariff costs and a solid balance sheet providing financial flexibility. While acknowledging near-term uncertainty, the company expressed confidence in its ability to implement additional efficiency actions if needed.

This Q1 2025 performance represents a positive shift from the company’s Q3 2024 results, when Gates reported a 3.8% decrease in core sales. The return to positive growth suggests that the company’s strategic focus on replacement channels and mobility segments is beginning to yield results, though challenges remain in certain industrial OEM markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.