Buy gold, crypto and China, tread carefully on rich U.S. tech: BofA’s Hartnett

Introduction & Market Context

GE Aerospace (NYSE:GE) reported strong first-quarter 2025 results on April 22, showcasing significant growth in earnings and revenue despite ongoing supply chain challenges. The company’s shares were up 1.08% in premarket trading, reflecting positive investor sentiment about the results.

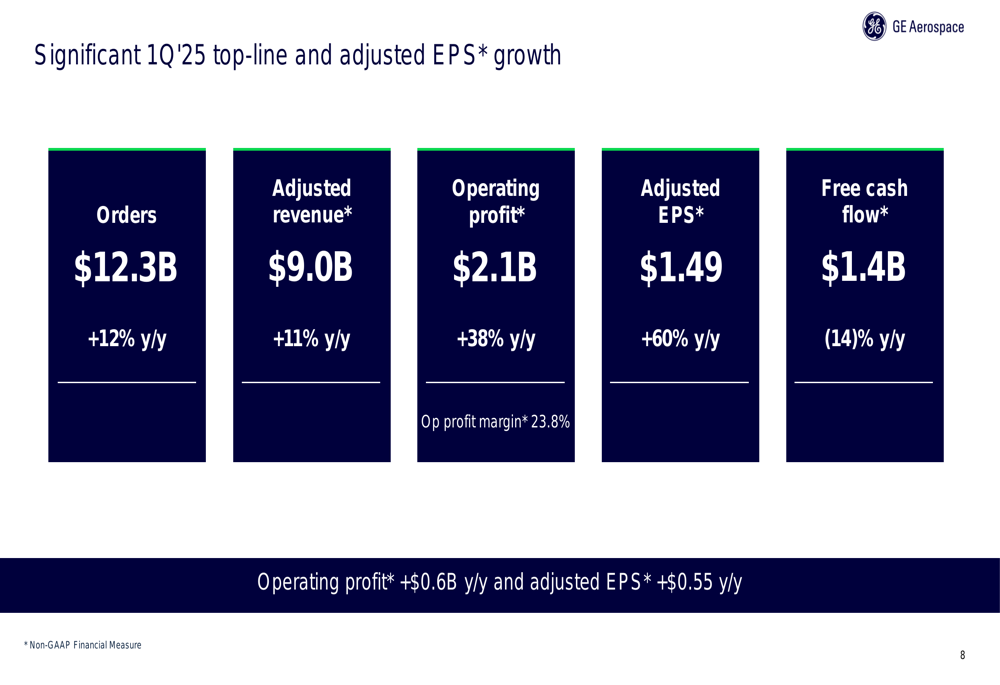

The aerospace giant delivered impressive year-over-year growth metrics, with orders up 12%, adjusted revenue increasing 11%, and adjusted earnings per share surging 60%. This performance builds on the momentum seen in previous quarters, including the strong Q3 2024 results when the company exceeded analyst expectations.

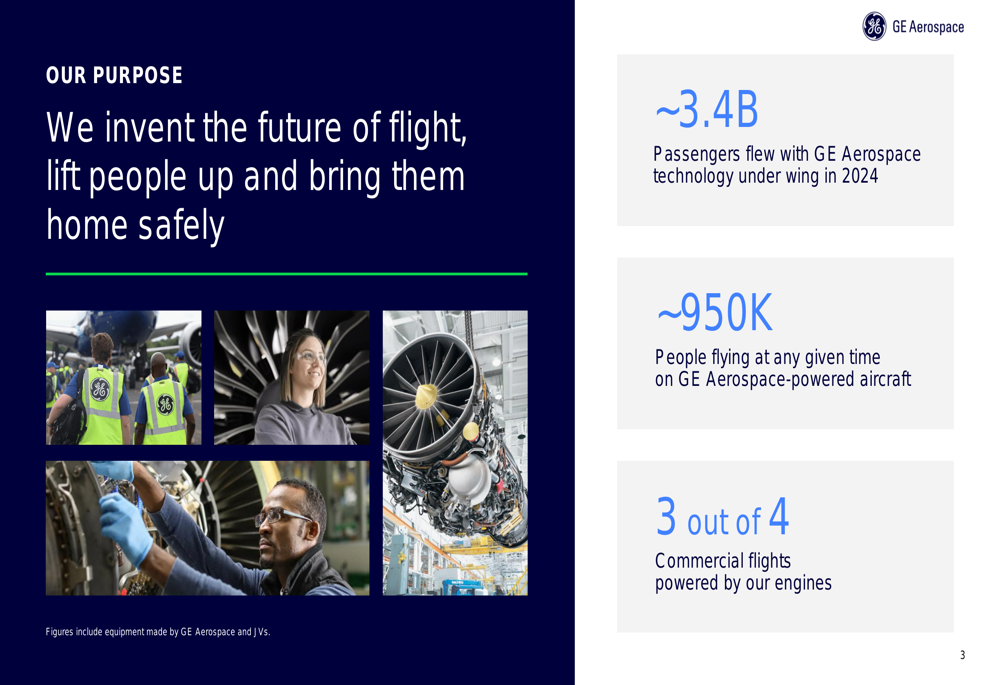

As shown in the following slide highlighting GE Aerospace’s purpose and market position, the company maintains a dominant position in the commercial aviation market:

Quarterly Performance Highlights

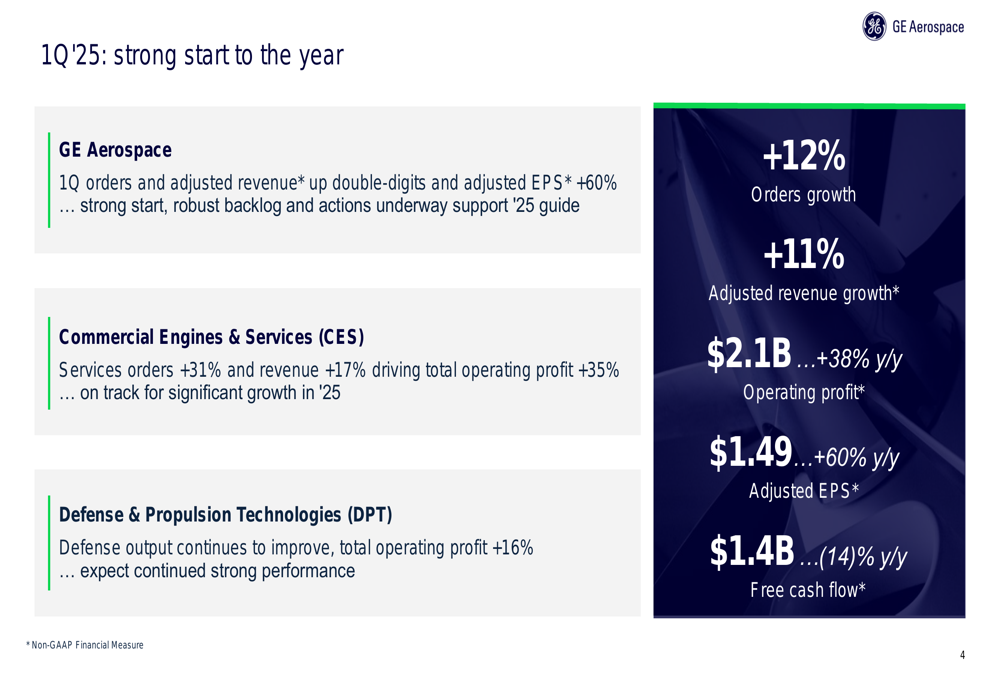

GE Aerospace reported robust financial results for Q1 2025, with adjusted revenue reaching $9.0 billion (up 11% year-over-year) and operating profit increasing 38% to $2.1 billion. The company’s adjusted earnings per share jumped 60% to $1.49, while free cash flow was $1.4 billion, down 14% compared to the same period last year.

The following slide summarizes the key financial metrics for the quarter:

Operating profit margin expanded to 23.8%, reflecting the company’s ability to drive profitability improvements despite challenges. Total (EPA:TTEF) orders for the quarter reached $12.3 billion, demonstrating continued strong demand for GE Aerospace’s products and services.

The detailed financial performance slide below provides a comprehensive view of the company’s Q1 results:

Detailed Financial Analysis

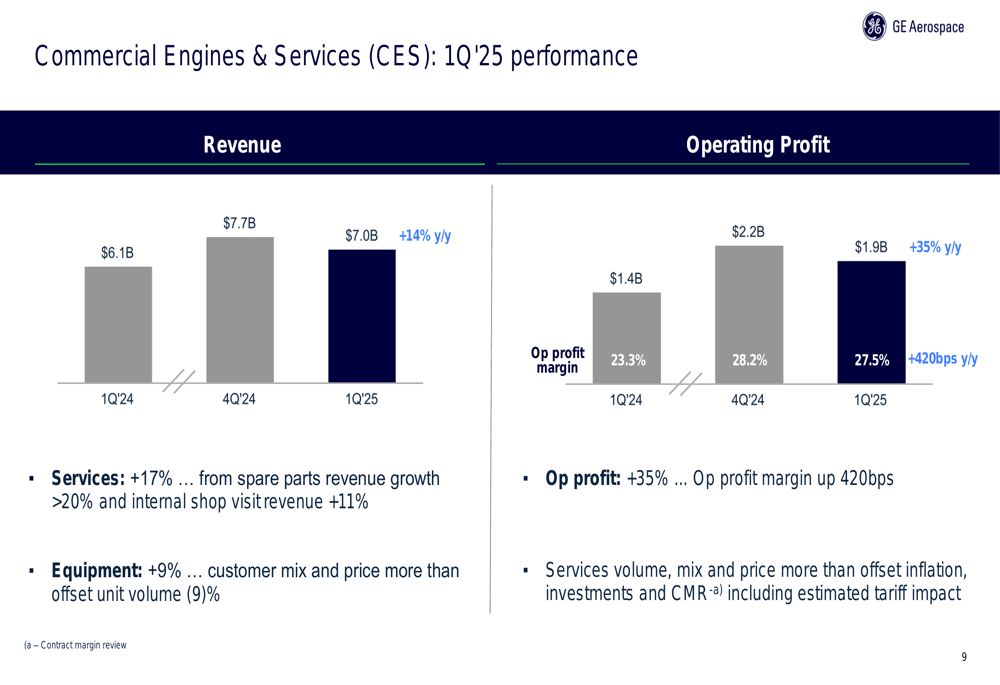

GE Aerospace’s performance was driven primarily by its Commercial Engines & Services (CES) segment, which saw revenue increase by 14% year-over-year to $7.0 billion. Services revenue within this segment grew 17%, fueled by spare parts revenue growth exceeding 20% and internal shop visit revenue increasing 11%. Equipment revenue rose 9%, with customer mix and price more than offsetting a 9% decline in unit volume.

The CES segment’s operating profit surged 35% to $1.9 billion, with margins expanding 420 basis points to 27.5%. This substantial improvement was attributed to services volume, mix, and price, which more than offset inflation, investments, and estimated tariff impacts.

The following slide details the CES segment’s performance:

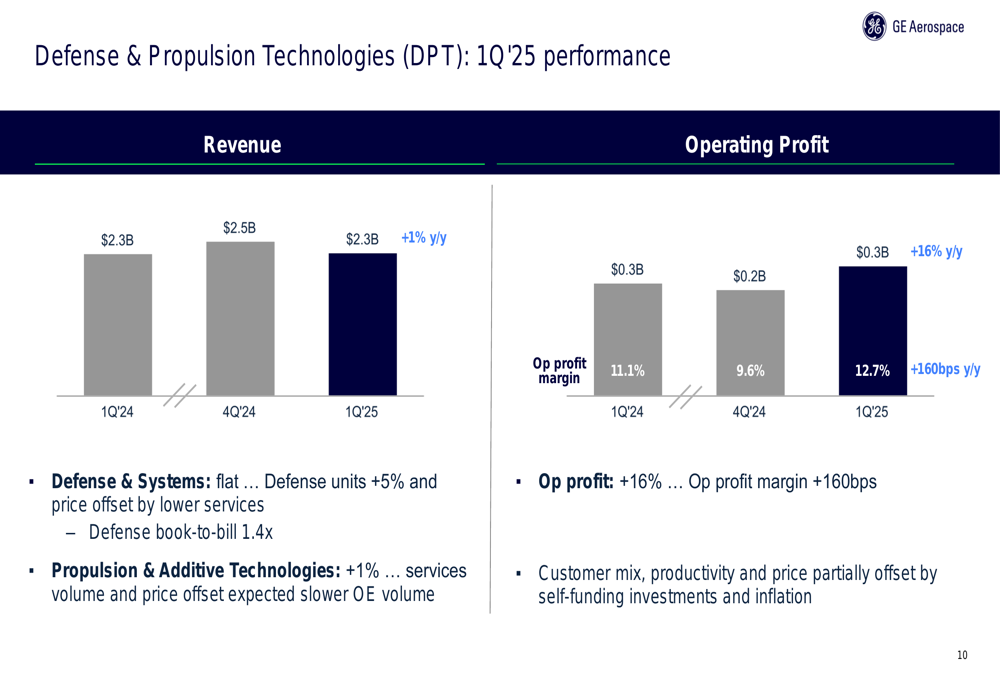

The Defense & Propulsion Technologies (DPT) segment reported more modest growth, with revenue increasing 1% year-over-year to $2.3 billion. Defense units grew 5%, and the segment maintained a strong book-to-bill ratio of 1.4x. Operating profit in this segment increased 16% to $0.3 billion, with margins expanding 160 basis points to 12.7%.

The DPT segment’s performance is illustrated in the following slide:

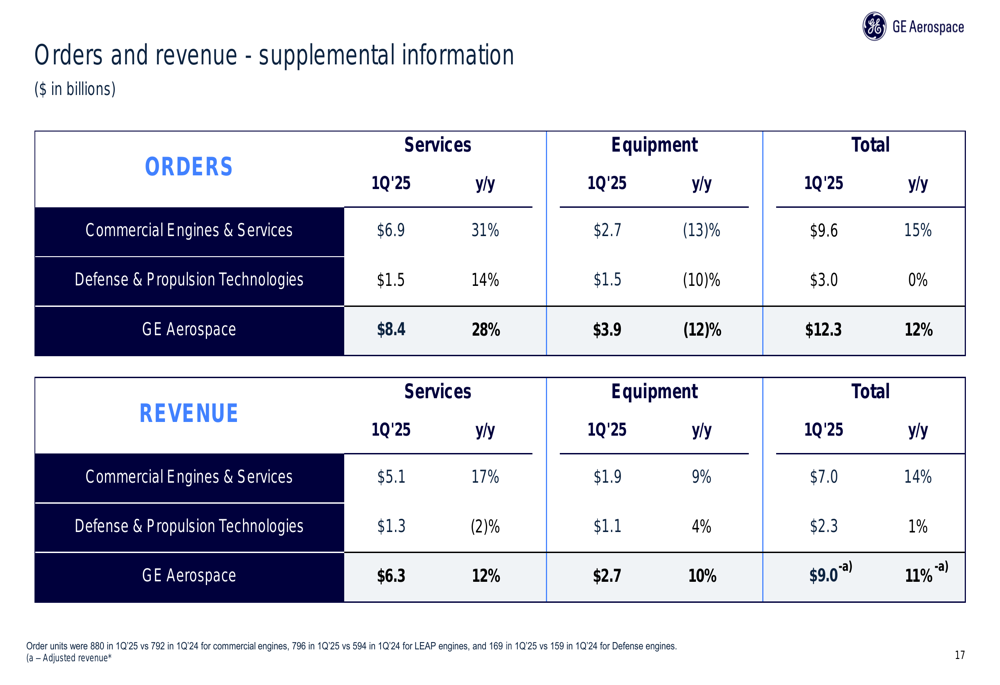

A more detailed breakdown of orders and revenue by segment and category (services vs. equipment) is provided in the supplemental information slide:

Strategic Initiatives

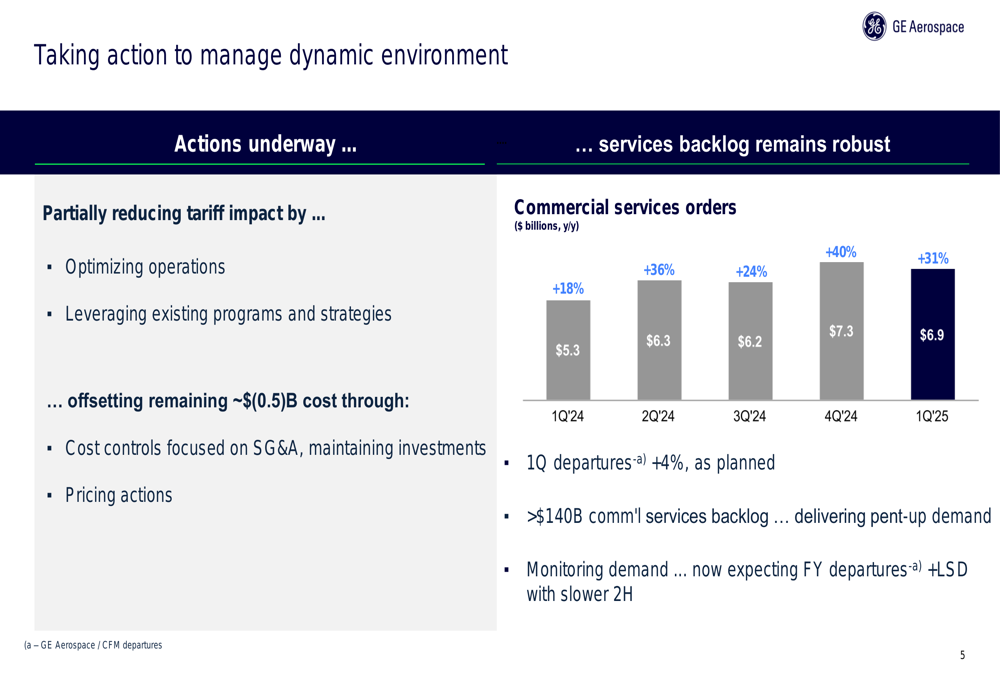

GE Aerospace is actively addressing the dynamic business environment, including managing the impact of tariffs and supply chain challenges. The company outlined actions to partially reduce tariff impact by optimizing operations and leveraging existing programs, while offsetting the remaining approximately $0.5 billion cost through SG&A controls, maintaining investments, and pricing actions.

As shown in the following slide, commercial services orders have demonstrated consistent growth over five consecutive quarters, with Q1 2025 showing a 31% increase:

The company is also focused on accelerating aftermarket and original equipment (OE) output. Priority supplier material input improved 8% quarter-over-quarter from Q4 2024 to Q1 2025, with February and March both showing double-digit growth versus January, supporting improved output expectations for Q2 and beyond.

GE Aerospace continues to secure significant new business, including engine commitments with All Nippon Airways (ANA) for LEAP and GEnx engines to power 13 A321neo, up to 22 737MAX, and 18 787-9 aircraft. The company also completed the Detailed Design Review of the XA102 adaptive cycle engine, a key milestone in the U.S. Air Force’s next-generation propulsion program.

Forward-Looking Statements

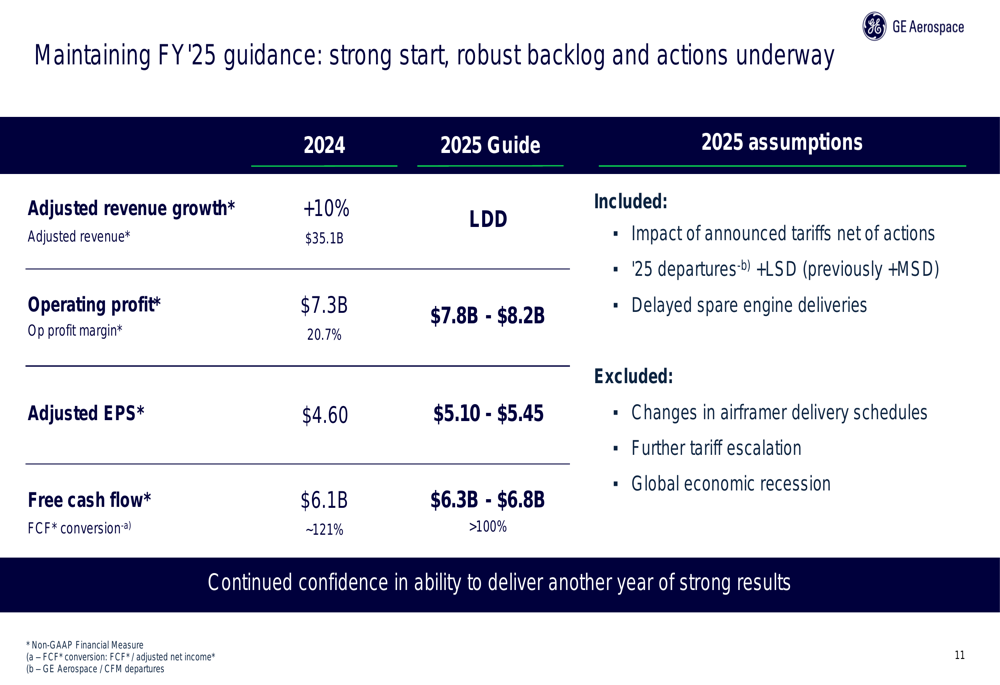

Despite the challenges in the operating environment, GE Aerospace is maintaining its full-year 2025 guidance, citing a strong start to the year, robust backlog, and ongoing strategic actions. The company expects low double-digit adjusted revenue growth, with operating profit projected to be between $7.8 billion and $8.2 billion, representing an operating profit margin of approximately 21-23%.

Adjusted EPS is expected to be in the range of $5.10 to $5.45, while free cash flow is projected at $6.3 billion to $6.8 billion, exceeding 100% conversion rate.

The following slide outlines the company’s FY 2025 guidance compared to 2024 results:

The guidance includes the impact of announced tariffs (net of mitigating actions) and assumes lower-than-previously-expected flight departures growth of low single digits for 2025, compared to the mid-single-digit growth previously anticipated. It excludes potential changes in airframer delivery schedules, further tariff escalation, or a global economic recession.

Competitive Industry Position

GE Aerospace continues to strengthen its leadership position in both commercial and defense aerospace markets. The company highlighted that approximately 3.4 billion passengers flew with GE Aerospace technology in 2024, with about 950,000 people flying at any given time on GE Aerospace-powered aircraft. Impressively, three out of four commercial flights are powered by GE engines.

The company is growing its backlog, which now exceeds $170 billion, with the services backlog alone surpassing $140 billion. This substantial backlog provides visibility and stability for future revenue streams.

GE Aerospace is also investing in breakthrough innovation to maintain its competitive edge, including the RISE (Revolutionary Innovation for Sustainable Engines) program and advanced military propulsion systems like the XA102 adaptive cycle engine.

Executive Summary

GE Aerospace’s Q1 2025 results demonstrate the company’s ability to drive significant profit growth despite operational challenges. The strong performance was primarily driven by the commercial services business, which continues to benefit from robust demand and pricing power.

The company’s strategic actions to address supply chain constraints and mitigate tariff impacts appear to be yielding positive results, with sequential improvements in material inputs and engine output. While equipment volumes remain below desired levels, the company is offsetting this through favorable mix, pricing, and continued services growth.

Looking ahead, GE Aerospace remains confident in its full-year outlook, maintaining its guidance for low double-digit revenue growth and raising its profit and cash flow expectations. The company’s substantial backlog, dominant market position, and ongoing investments in next-generation technologies position it well for continued success in both commercial and defense aerospace markets.

As the aerospace industry continues to recover and grow, GE Aerospace appears well-positioned to capitalize on increasing air travel demand while navigating the complex supply chain and geopolitical challenges that affect the broader market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.