Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

GE Vernova (NYSE:GEV) reported strong first-quarter 2025 financial results on April 23, showing significant improvements across key metrics. The company’s shares jumped 8.2% in premarket trading to $352.80, reflecting positive investor sentiment following the release.

The energy technology company demonstrated robust growth amid what it describes as an "electricity supercycle," with accelerating demand for products and services that electrify and decarbonize the global economy. The company also highlighted its ability to navigate global supply chain volatility through nimble operations.

Quarterly Performance Highlights

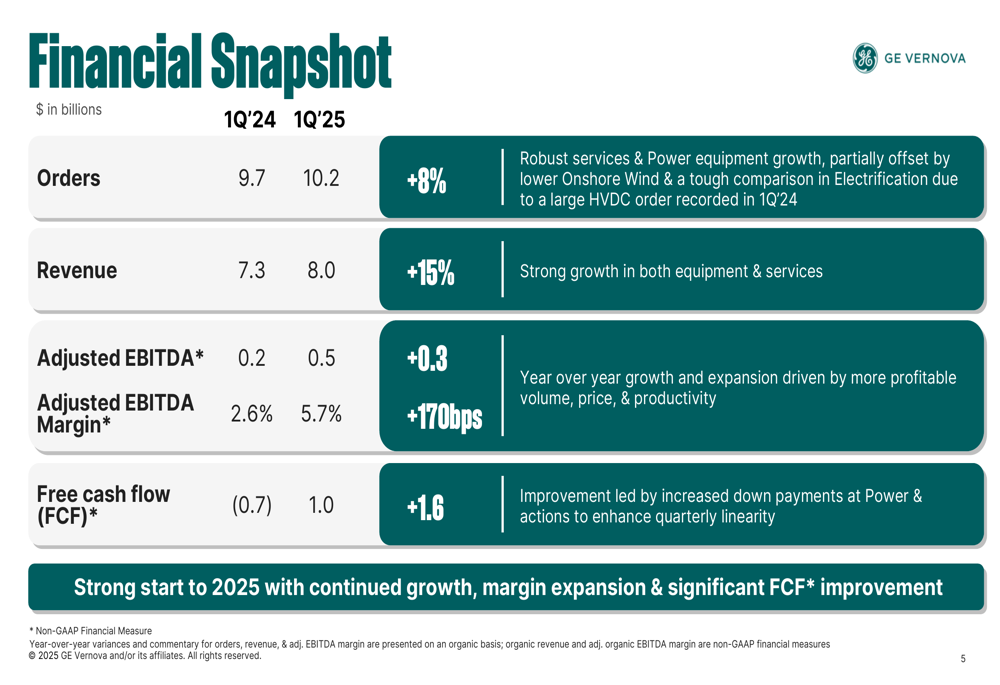

GE Vernova delivered impressive financial results in Q1 2025, with revenue growing 15% year-over-year to $8.0 billion. Orders increased 8% to $10.2 billion, while adjusted EBITDA more than doubled to $0.5 billion, representing a margin expansion of 170 basis points to 5.7%.

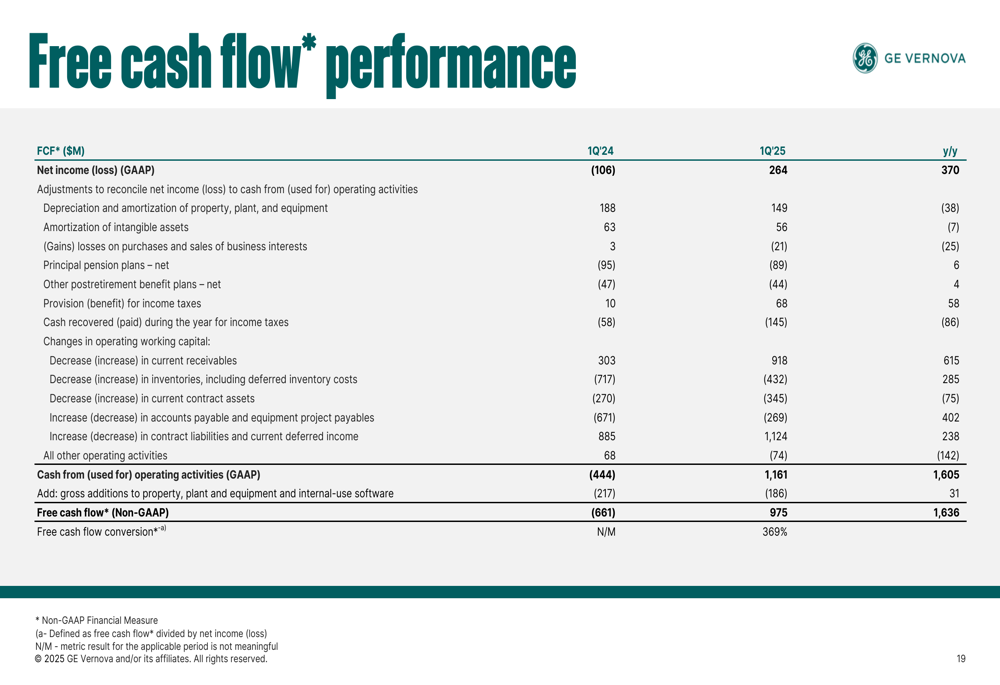

One of the most notable achievements was the significant improvement in free cash flow, which reached $1.0 billion—a $1.6 billion increase compared to the same period last year. The company also returned $1.3 billion to shareholders during the quarter.

As shown in the following financial snapshot comparing Q1 2024 to Q1 2025:

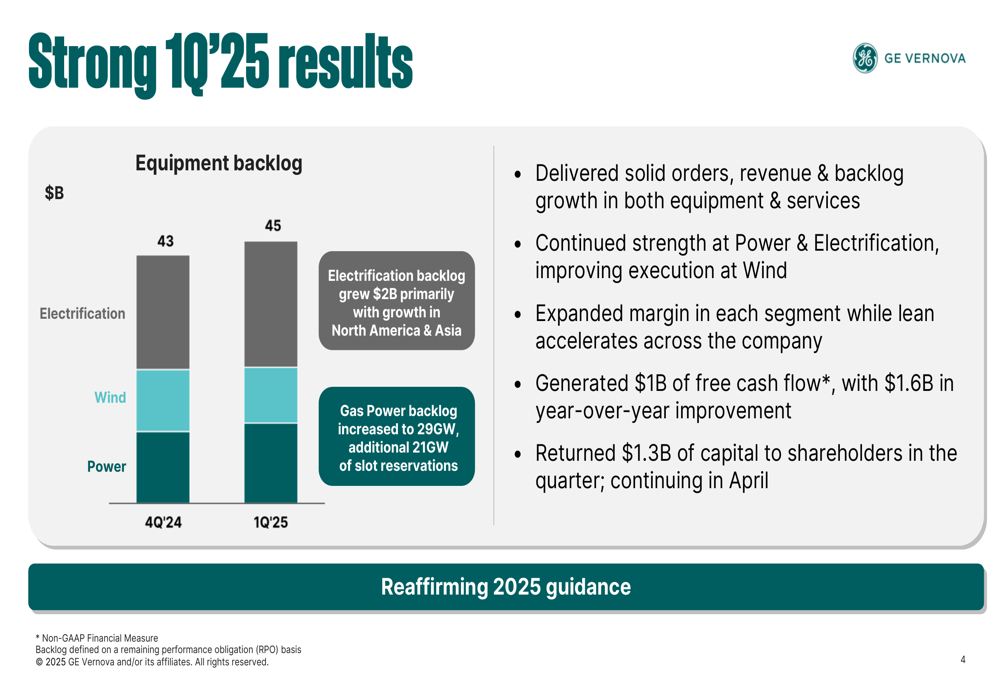

The company’s equipment backlog continued to grow, with particular strength in the Electrification segment, which increased by $2 billion primarily due to growth in North America and Asia. The Gas Power backlog increased to 29GW, with an additional 21GW of slot reservations.

Segment Analysis

Power Segment

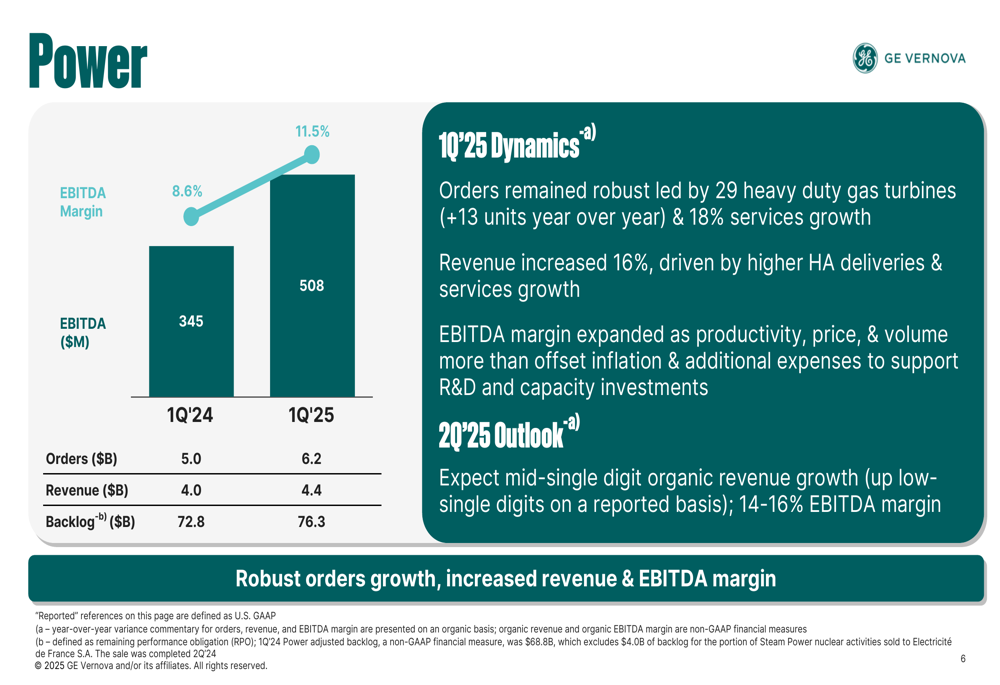

The Power segment delivered strong performance with orders of $6.2 billion, up from $5.0 billion in Q1 2024. Revenue increased 16% to $4.4 billion, driven by higher HA gas turbine deliveries and 18% services growth. The segment’s EBITDA margin expanded from 8.6% to 11.5% as productivity, price, and volume more than offset inflation and additional expenses related to R&D and capacity investments.

The following chart illustrates the Power segment’s performance improvements:

Wind Segment

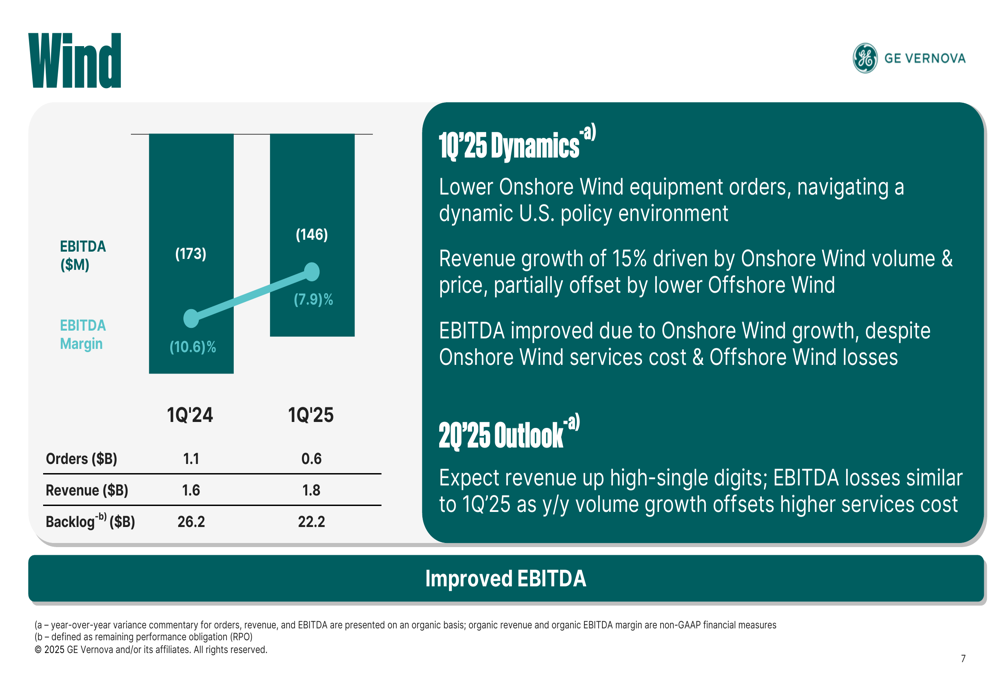

The Wind segment faced challenges but showed signs of improving execution. While orders decreased from $1.1 billion to $0.6 billion due to a dynamic U.S. policy environment, revenue grew 15% to $1.8 billion, driven by Onshore Wind volume and price improvements. EBITDA losses narrowed from $173 million to $146 million, with margin improving from -10.6% to -7.9%.

The Wind segment’s performance metrics are illustrated below:

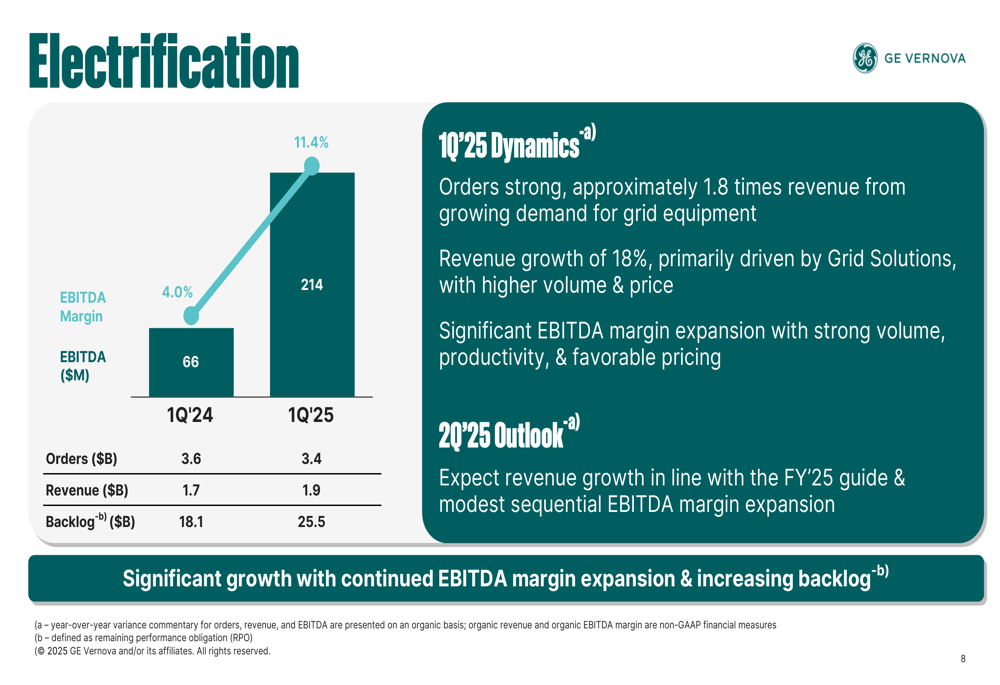

Electrification Segment

The Electrification segment demonstrated particularly strong results, with orders at approximately 1.8 times revenue, reflecting growing demand for grid equipment. Revenue increased 18% to $1.9 billion, primarily driven by Grid Solutions with higher volume and price. The segment achieved significant EBITDA margin expansion from 4.0% to 11.4%, thanks to strong volume, productivity, and favorable pricing.

The following chart shows the substantial improvement in the Electrification segment’s profitability:

Strategic Positioning

GE Vernova emphasized its strategic positioning to benefit from what it calls the "electricity supercycle," with accelerating demand for products and services that electrify and decarbonize the world. The company noted that global supply chain volatility presents an opportunity to differentiate through nimble operations and accelerated actions to offset increased costs.

Management highlighted that its solid balance sheet, growing free cash flow, and strong backlog enable investment in the business while returning capital to shareholders. The company’s free cash flow performance showed remarkable improvement:

Forward Guidance

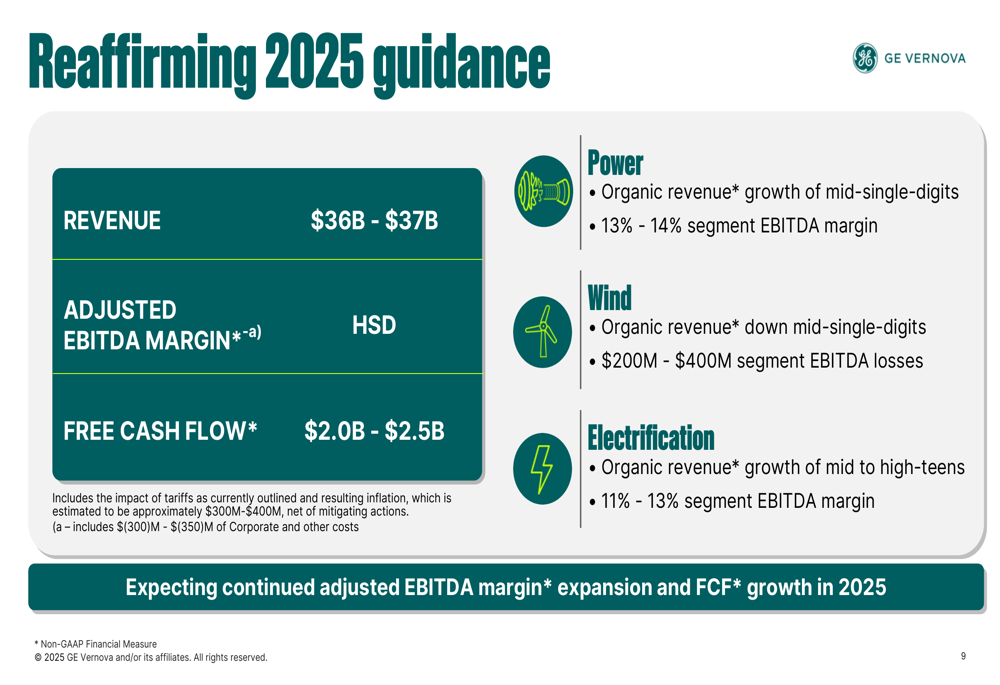

GE Vernova reaffirmed its 2025 guidance, projecting revenue of $36-37 billion, adjusted EBITDA margin in the high single digits, and free cash flow of $2.0-2.5 billion. The guidance includes the impact of tariffs as currently outlined and resulting inflation, estimated at approximately $300-400 million, net of mitigating actions.

Segment-specific guidance includes:

- Power: Mid-single-digit organic revenue growth with 13-14% EBITDA margin

- Wind: Organic revenue down mid-single-digits with $200-400 million EBITDA losses

- Electrification: Mid to high-teens organic revenue growth with 11-13% EBITDA margin

The company expects continued adjusted EBITDA margin expansion and free cash flow growth throughout 2025, emphasizing that it is "well-positioned to meet growing demand with disciplined execution" and is "just getting started" on its growth journey.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.