Asia FX dithers as dollar steadies before Powell speech; yen muted after CPI data

Introduction & Market Context

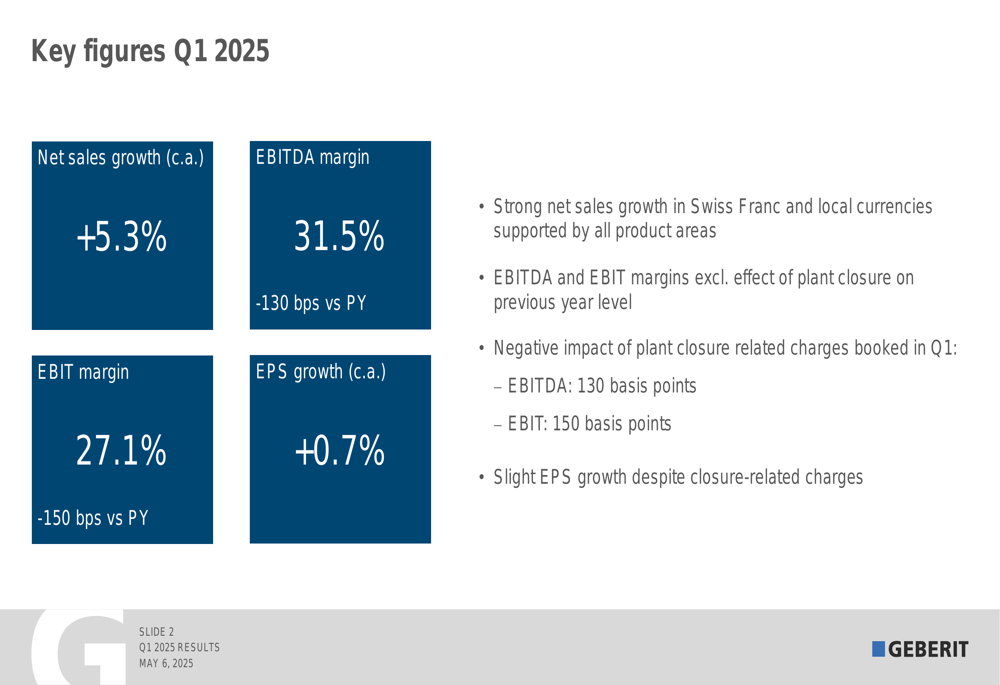

Geberit AG (SWX:SIX:GEBN) reported solid sales growth for the first quarter of 2025, with a 5.3% increase in local currencies, according to the company’s presentation delivered on May 6, 2025. The Swiss sanitary products manufacturer achieved net sales of CHF 878 million, representing a 4.9% increase in Swiss francs compared to the same period last year.

Despite the positive sales development, Geberit’s profitability metrics were impacted by one-time charges related to a plant closure, which affected both EBITDA and EBIT margins. The company’s results reflect a mixed global market environment with strong performance in most regions offset by challenges in Western Europe and China.

Quarterly Performance Highlights

Geberit’s Q1 2025 results showed strength in sales growth across all product areas, supported by new product developments and pre-buying by wholesalers ahead of a planned price increase in April.

As shown in the following key figures chart, Geberit achieved solid growth while maintaining profitability despite restructuring costs:

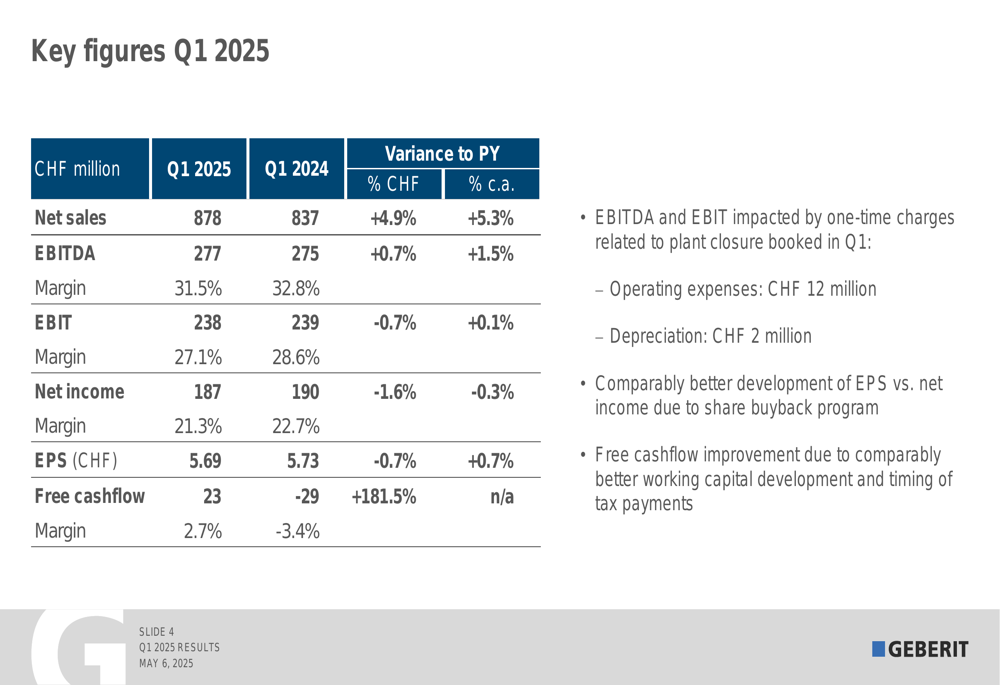

The company’s EBITDA reached CHF 277 million, a modest increase of 0.7% in Swiss francs and 1.5% in local currencies compared to Q1 2024. However, the EBITDA margin decreased by 130 basis points to 31.5%, primarily due to one-time charges related to a plant closure.

Similarly, EBIT stood at CHF 238 million, representing a slight decrease of 0.7% in Swiss francs but a marginal increase of 0.1% in local currencies. The EBIT margin declined by 150 basis points to 27.1%.

A more detailed breakdown of the financial figures shows the impact of one-time charges on the company’s performance:

Net income decreased by 1.6% to CHF 187 million, with a margin of 21.3% compared to 22.7% in the previous year. Earnings per share (EPS) reached CHF 5.69, down 0.7% in Swiss francs but up 0.7% in local currencies. According to the earnings call transcript, adjusted EPS excluding one-time costs would have been CHF 6.50, marking a 6% increase.

Free cash flow showed significant improvement, reaching CHF 23 million compared to negative CHF 29 million in Q1 2024, primarily due to better working capital management and the timing of tax payments.

Regional and Product Performance

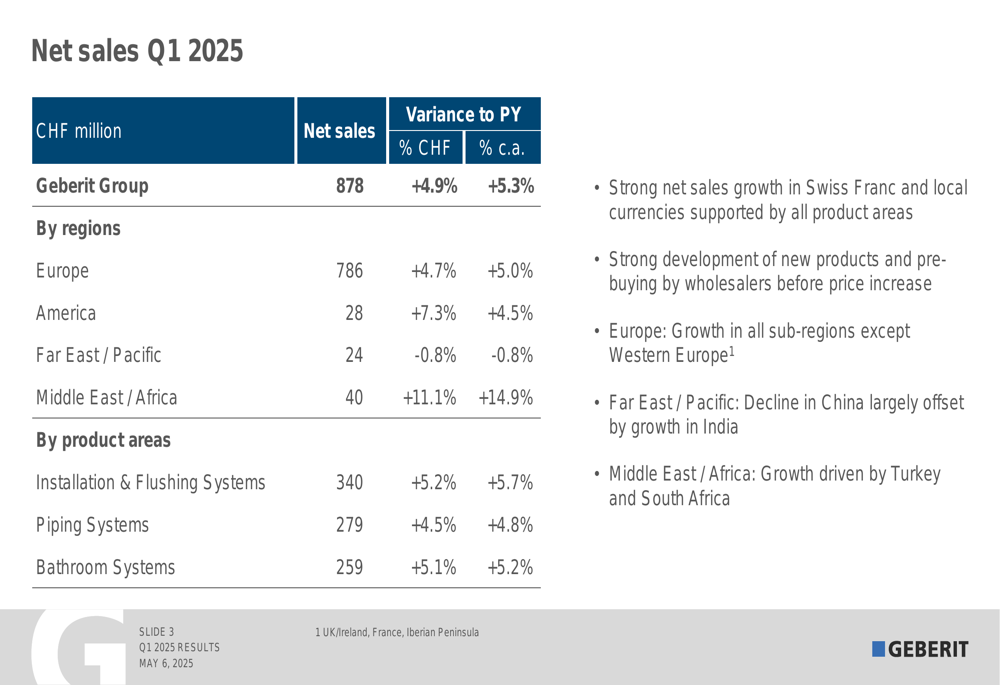

Geberit’s sales performance varied across different regions, with particularly strong growth in the Middle East/Africa and America, while the Far East/Pacific region experienced a slight decline.

The following chart breaks down the company’s net sales by region and product area:

Europe, which accounts for approximately 89% of Geberit’s total sales, grew by 4.7% in Swiss francs and 5.0% in local currencies to CHF 786 million. The company noted growth across all European sub-regions except Western Europe.

The Middle East/Africa region showed the strongest performance with growth of 11.1% in Swiss francs and 14.9% in local currencies, driven primarily by Turkey and South Africa. America also performed well with 7.3% growth in Swiss francs and 4.5% in local currencies.

The Far East/Pacific region was the only one to experience a decline, with sales decreasing by 0.8% in both Swiss francs and local currencies. According to the presentation, the decline in China was largely offset by growth in India.

All product areas contributed to the overall sales growth, with Installation & Flushing Systems leading at 5.2% growth in Swiss francs (5.7% in local currencies), followed by Bathroom Systems at 5.1% (5.2% in local currencies) and Piping Systems at 4.5% (4.8% in local currencies).

Detailed Financial Analysis

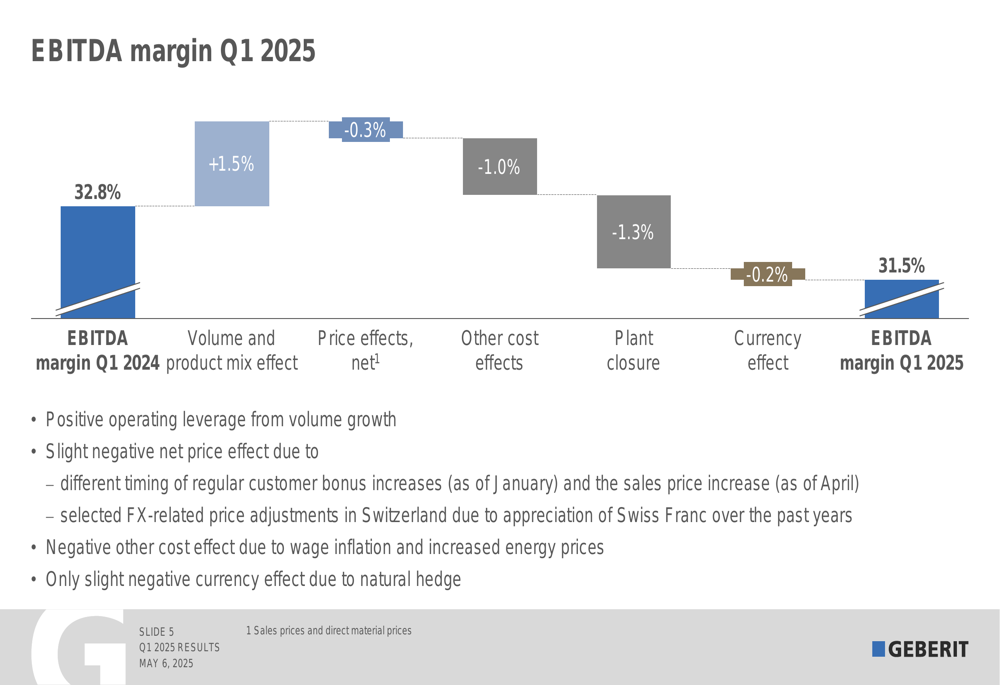

A closer examination of Geberit’s EBITDA margin reveals the various factors that influenced the company’s profitability in Q1 2025.

The following waterfall chart illustrates the changes in EBITDA margin from Q1 2024 to Q1 2025:

The EBITDA margin decreased from 32.8% in Q1 2024 to 31.5% in Q1 2025. This decline was primarily due to a 1.3 percentage point negative impact from the plant closure. Without this one-time effect, the EBITDA margin would have been on par with the previous year’s level.

Volume and product mix had a positive effect of 1.5 percentage points, reflecting the operating leverage from increased sales volumes. However, this was offset by a slight negative net price effect of 0.3 percentage points, which the company attributed to different timing of regular customer bonus increases (implemented in January) and the sales price increase (scheduled for April).

Other cost effects had a negative impact of 1.0 percentage point, mainly due to wage inflation and increased energy prices. Currency effects had a minimal negative impact of 0.2 percentage points, which the company noted was due to its natural hedge position.

Forward-Looking Statements

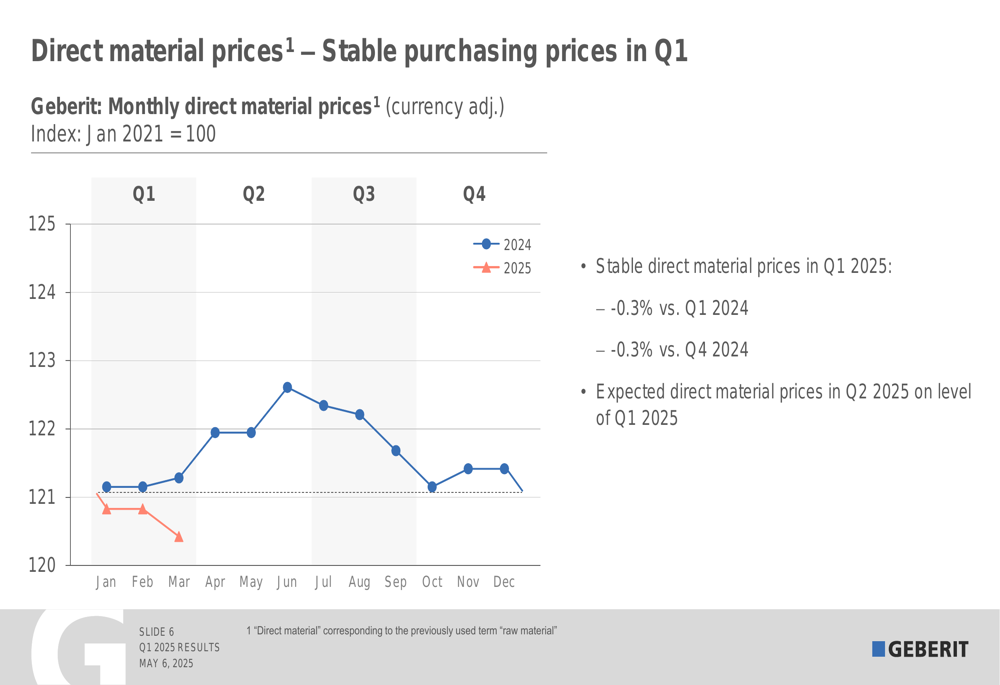

Regarding raw material costs, Geberit reported stable direct material prices in Q1 2025, with a slight decrease of 0.3% compared to both Q1 2024 and Q4 2024. The company expects direct material prices in Q2 2025 to remain at the same level as Q1 2025.

The following chart shows the trend of direct material prices:

According to the earnings call transcript, Geberit anticipates wage inflation of 3-4% for the full year, with energy prices expected to exert downward pressure. The company remains committed to new product development and expanding sales initiatives in emerging markets.

Market stabilization in Europe is expected by 2025, with a positive renovation market offsetting declines in new build activity. The company also noted strong performance in product innovation, particularly in its FlowFit and MalPress TERM piping systems and the ALBA shower toilet line.

Strategic Initiatives

Geberit’s Q1 2025 results reflect its ongoing strategic focus on product innovation and market expansion. The company’s plant closure, while impacting short-term profitability, appears to be part of its operational optimization efforts.

The share buyback program mentioned in the earnings call transcript (71,000 shares for CHF 37 million) indicates the company’s confidence in its financial position and commitment to returning value to shareholders.

With a market capitalization of approximately $24.1 billion and a gross profit margin of 72.85%, Geberit maintains its position as a market leader in the sanitary products industry. The company’s ability to achieve solid sales growth across all product areas, despite challenging market conditions in some regions, demonstrates the strength of its business model and product portfolio.

As Geberit moves forward in 2025, investors will be watching to see if the company can maintain its sales momentum while recovering from the one-time costs that impacted its Q1 margins.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.