Still betting on Nvidia? Our AI picked this stock instead; it’s up 96%+ THIS MONTH

Introduction & Market Context

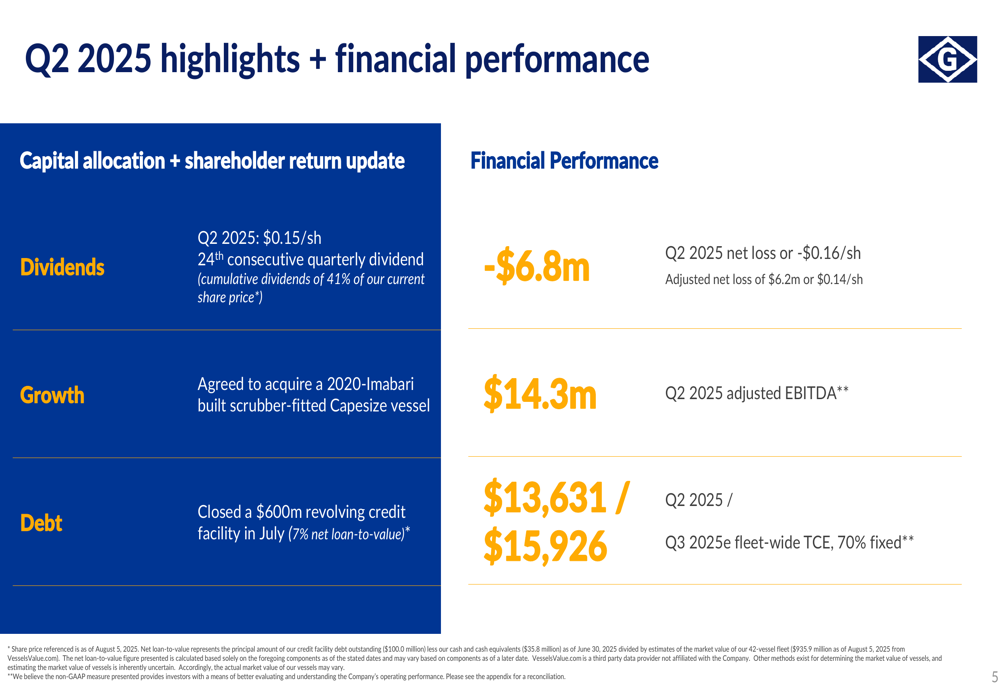

Genco Shipping & Trading Limited (NYSE:GNK) reported a net loss of $6.8 million for Q2 2025, an improvement from the $11.9 million loss in the previous quarter, according to the company’s earnings presentation released on August 7, 2025. Despite the continued losses, the company maintained its dividend at $0.15 per share, marking its 24th consecutive quarterly dividend.

The stock closed at $16.77 on the day of the announcement, down 3.64% from the previous close, reflecting investor concerns about the continued challenges in the drybulk shipping market despite the quarter-over-quarter improvement in financial performance.

Quarterly Performance Highlights

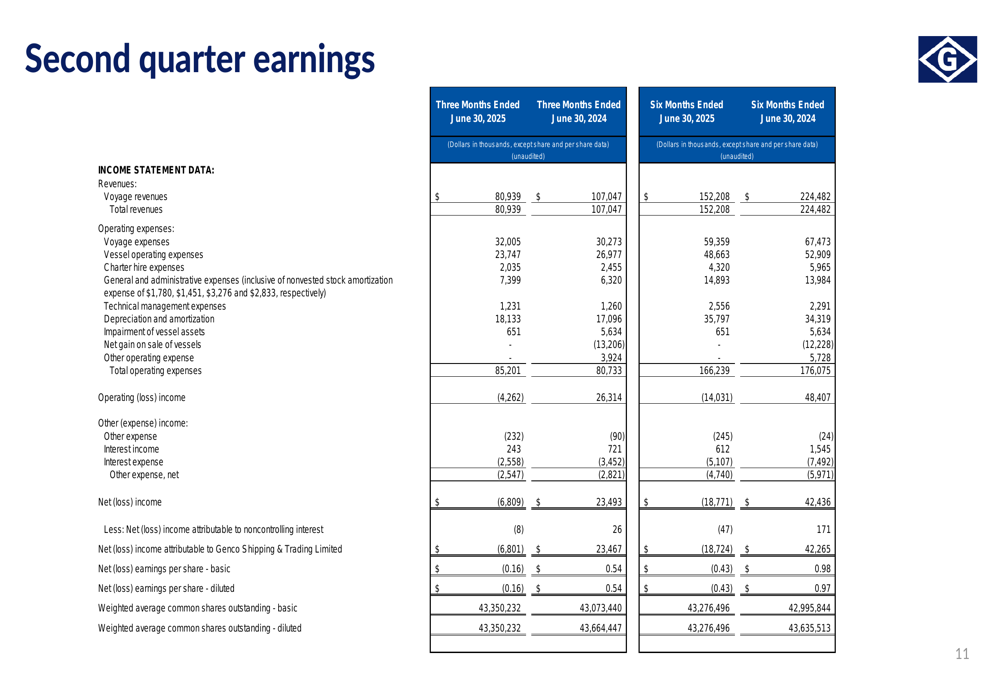

Genco reported a Q2 2025 net loss of $6.8 million ($0.16 per share), compared to a net income of $23.5 million ($0.54 per share) in the same quarter of 2024. On an adjusted basis, the net loss was $6.2 million ($0.14 per share). The company generated $14.3 million in adjusted EBITDA for the quarter.

As shown in the following financial performance summary, Genco maintained its dividend despite the challenging market conditions:

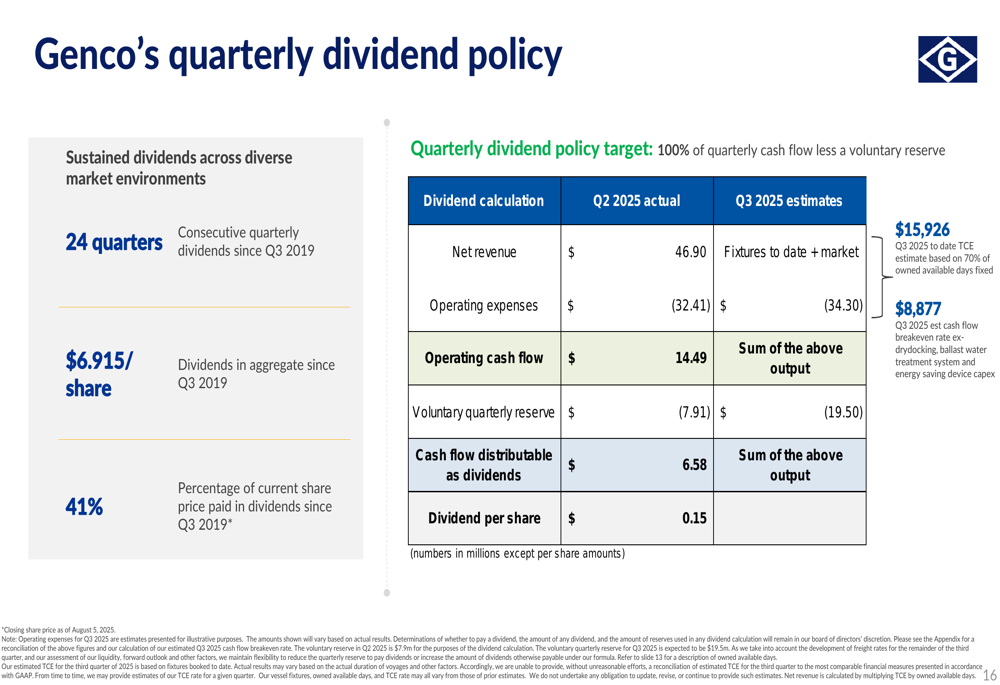

Revenue for the quarter came in at $80.9 million, down from $107.0 million in Q2 2024. The company’s Time Charter Equivalent (TCE) rate was $13,631 for Q2 2025, significantly lower than the $19,938 achieved in Q2 2024, reflecting the weaker market conditions. For Q3 2025, Genco has already fixed 70% of its available days at an estimated TCE of $15,926, suggesting a modest improvement in rates.

The detailed income statement shows the extent of the year-over-year decline in performance:

Strategic Initiatives

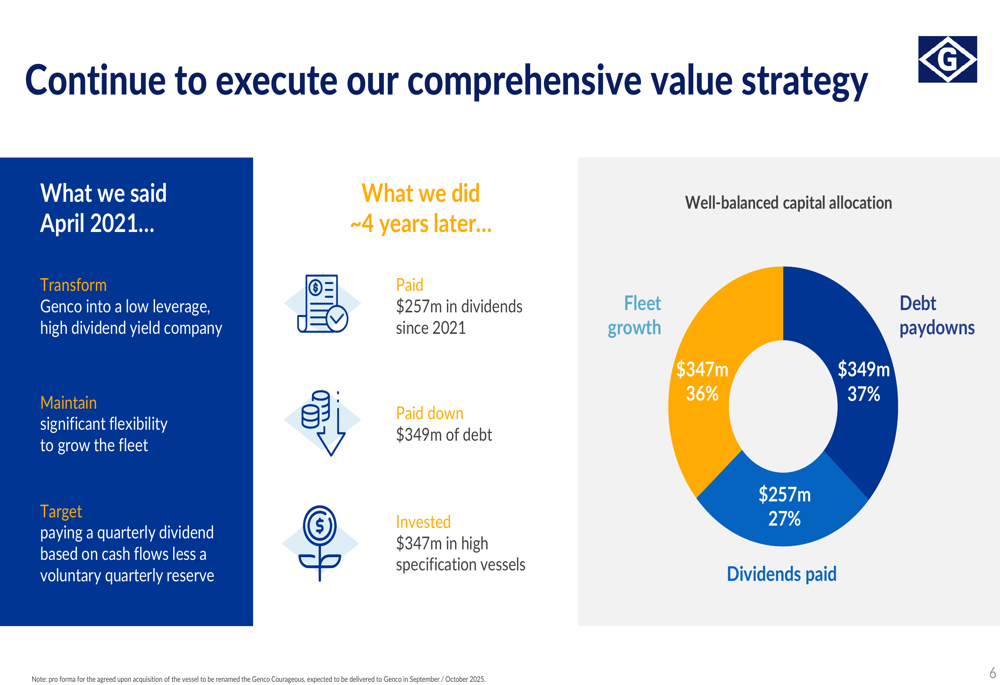

Genco continues to execute its comprehensive value strategy initiated in April 2021, focusing on three key areas: dividend payments, debt reduction, and fleet growth. As illustrated in the following chart, the company has maintained a balanced approach to capital allocation:

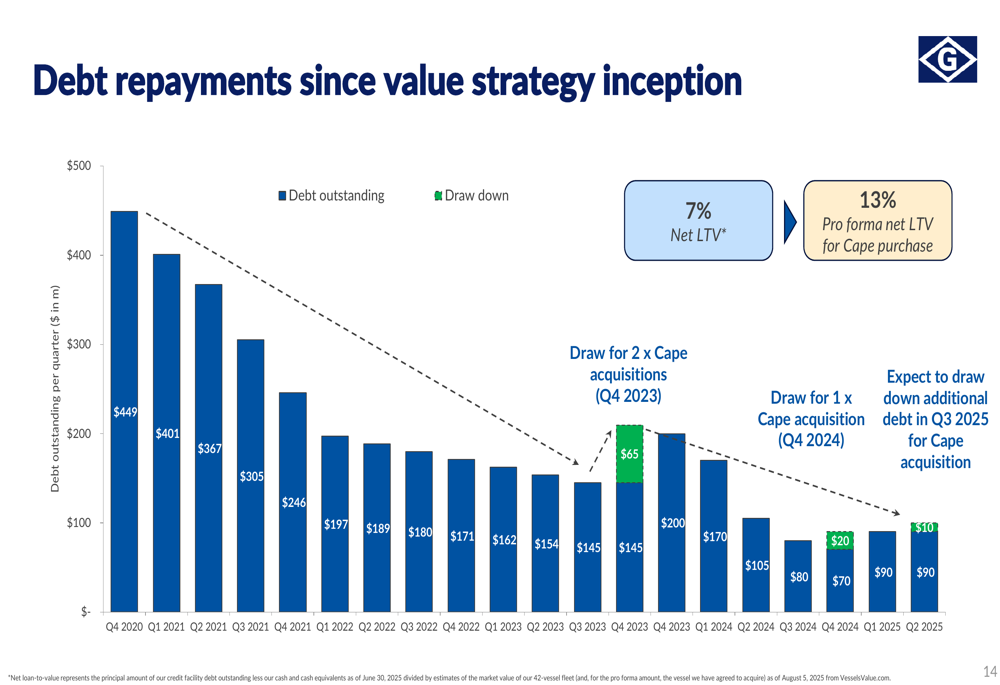

Since 2021, Genco has paid $257 million in dividends, paid down $349 million of debt, and invested $347 million in high-specification vessels. This balanced approach has positioned the company with one of the lowest leverage profiles in the industry, with a net loan-to-value ratio of just 7%.

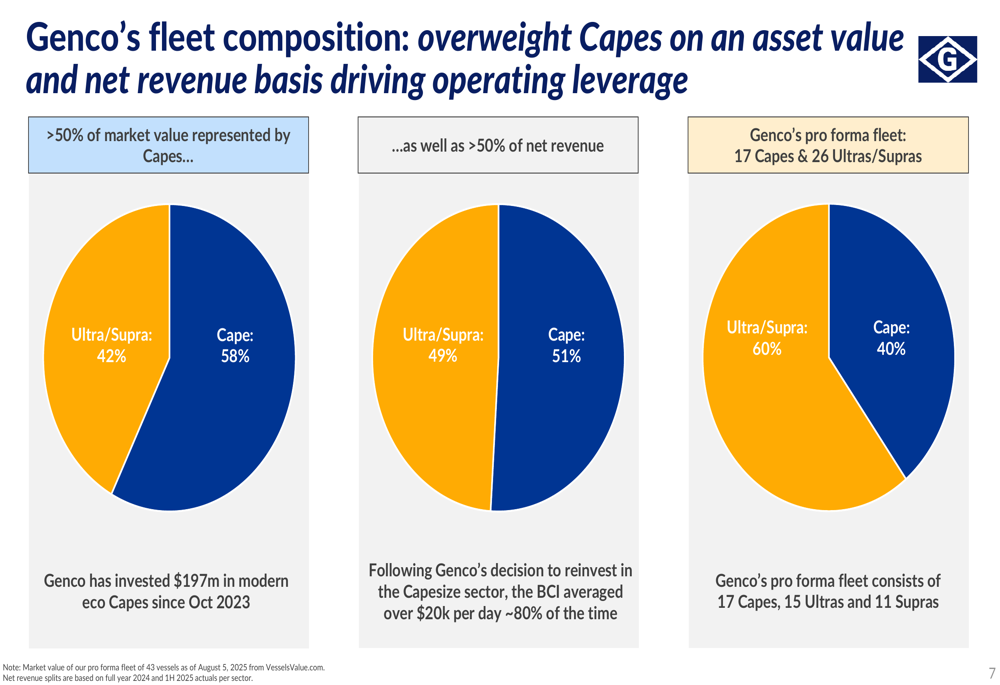

The company’s fleet strategy emphasizes Capesize vessels, which represent over 50% of its market value and net revenue despite constituting only 40% of its fleet by vessel count. This strategic overweighting provides Genco with greater operating leverage in improving market conditions.

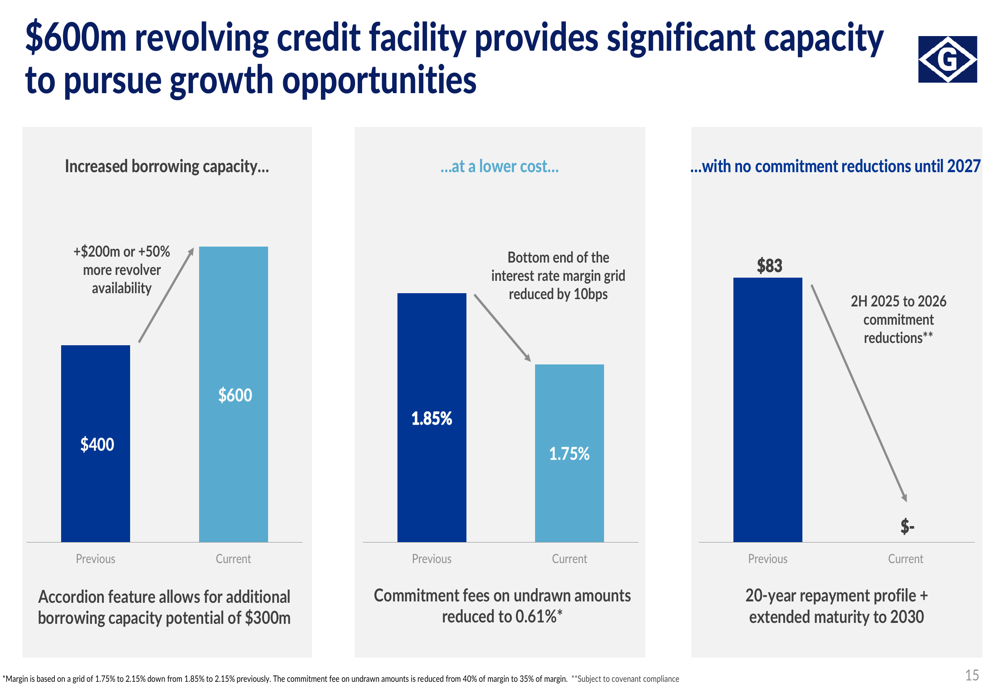

Genco’s financial flexibility is further enhanced by its recently closed $600 million revolving credit facility, which increases its borrowing capacity by 50% at a lower cost and with no commitment reductions until 2027:

Detailed Financial Analysis

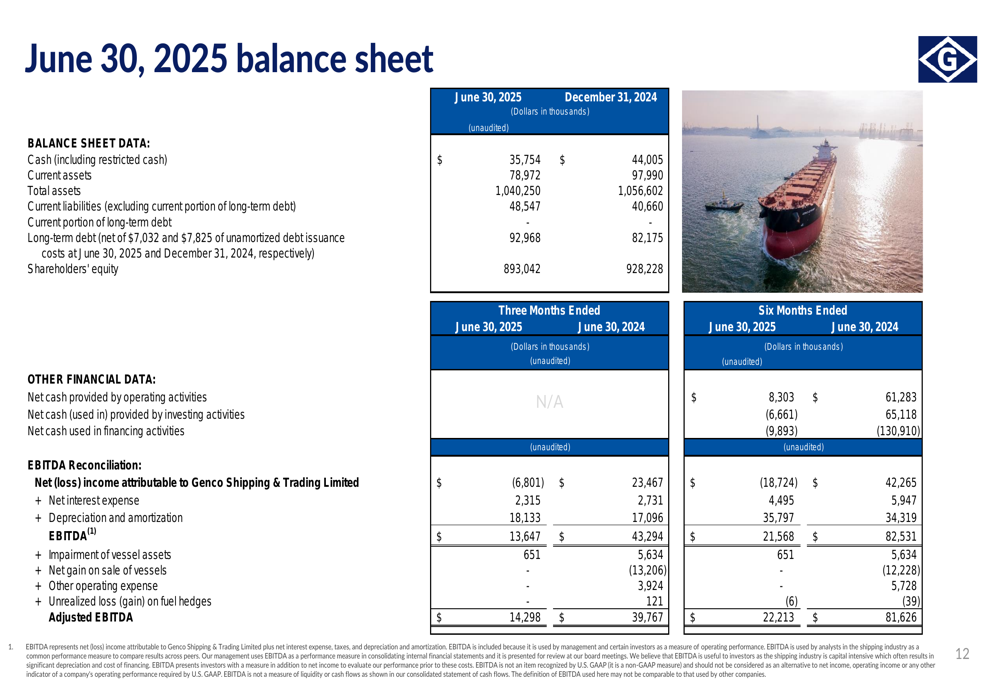

The company’s balance sheet remains strong despite the challenging market conditions. As of June 30, 2025, Genco reported cash (including restricted cash) of $35.8 million, down from $44.0 million at the end of 2024. Long-term debt stood at $93.0 million, up from $82.2 million at the end of 2024, reflecting recent vessel acquisitions.

Genco’s debt reduction strategy has been a key focus since the inception of its value strategy in late 2020. The company has significantly reduced its debt from $449 million in Q4 2020 to current levels, with selective drawdowns for strategic vessel acquisitions:

The company’s quarterly dividend policy targets 100% of quarterly cash flow less a voluntary reserve. For Q2 2025, this resulted in a dividend of $0.15 per share. Since Q3 2019, Genco has paid cumulative dividends of $6.915 per share, representing 41% of the current share price.

Industry Outlook

Genco’s presentation highlighted several positive long-term industry trends that could support future growth. One significant factor is the aging global drybulk fleet, with approximately 30% of the current fleet expected to be 20 years or older by 2030, representing about 4,200 ships. This aging fleet, combined with reduced shipyard capacity (down 60% versus 2008), could constrain supply growth.

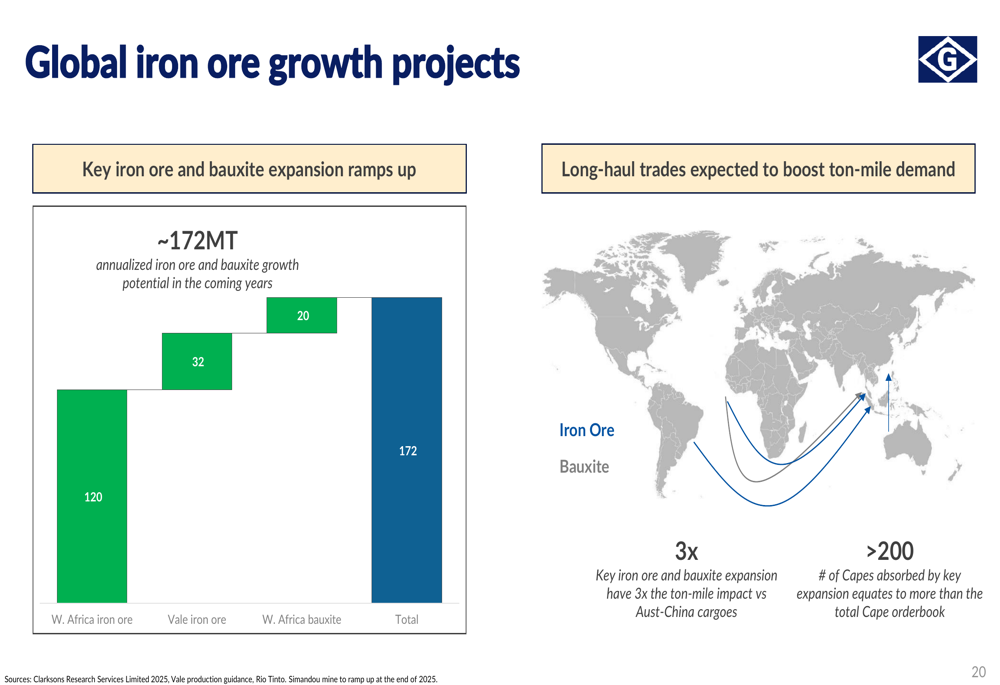

On the demand side, Genco highlighted the potential impact of global iron ore and bauxite growth projects, which could significantly boost ton-mile demand:

The company also noted the strong growth in Guinean bauxite exports, which have increased by 35% year-over-year to 93 million tons in the first half of 2025. Capesize vessels handle approximately 90% of these shipments, with over 80% of volumes heading to China.

Forward-Looking Statements

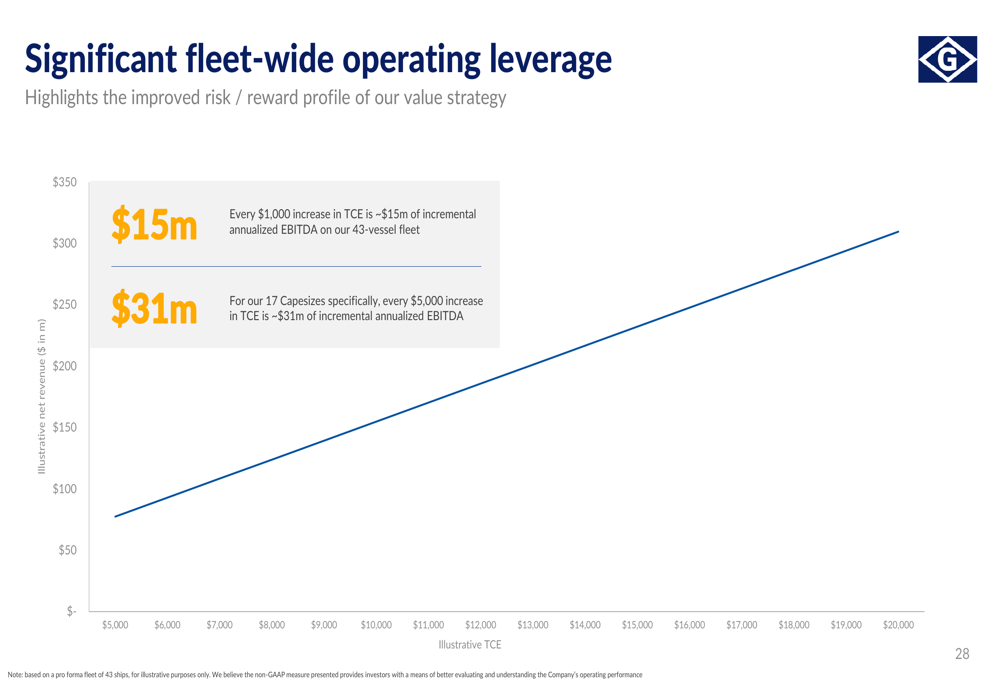

Looking ahead, Genco’s management expressed confidence in the company’s strategic positioning despite the current market challenges. The company’s low financial leverage provides significant operating leverage in an improving market environment, with every $1,000 increase in TCE rates generating approximately $15 million in incremental annualized EBITDA across its 43-vessel fleet.

The company continues to focus on its balanced capital allocation strategy, maintaining its dividend policy while selectively growing its fleet with modern, fuel-efficient vessels. The recent acquisition of a 2020-built scrubber-fitted Capesize vessel aligns with this strategy.

Genco’s management highlighted the potential positive impact of increasing long-haul iron ore and bauxite trades, which could significantly boost ton-mile demand. The company’s strategic overweighting of Capesize vessels positions it to benefit from these trends.

Despite the current market challenges reflected in the Q2 2025 results, Genco’s management remains confident in the company’s long-term prospects, supported by its strong balance sheet, low financial leverage, and strategic fleet positioning.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.