Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

General Dynamics Corporation (NYSE:GD) has reported a strong start to 2025, with its first-quarter presentation showing substantial growth across all business segments. The defense and aerospace giant revealed impressive financial results on April 23, 2025, continuing the positive momentum seen in the previous quarter.

The company’s stock, which closed at $274.80 on April 22, showed a positive reaction in pre-market trading, rising 1.16% to $278.00 following the presentation. This performance comes after General Dynamics’ Q4 2024 results, which saw revenue rise 14.3% year-over-year but with EPS slightly missing analyst expectations.

Quarterly Performance Highlights

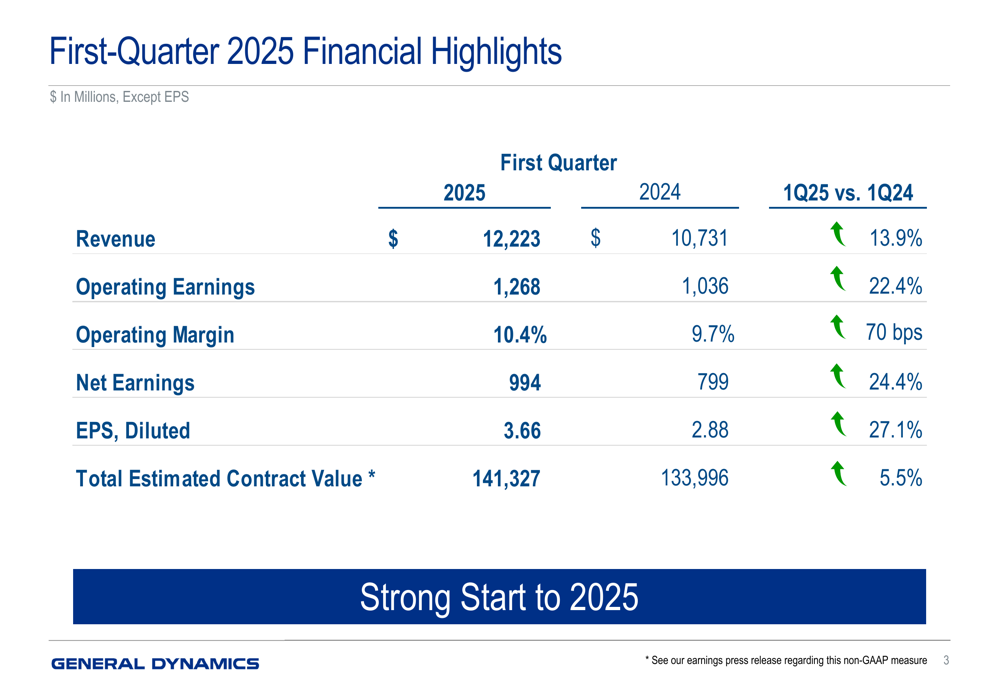

General Dynamics reported robust financial performance for Q1 2025, with significant improvements across all key metrics compared to the same period last year. The company’s presentation highlighted "Strong Start to 2025" with double-digit growth in revenue, earnings, and EPS.

As shown in the following financial highlights slide, the company achieved $12.22 billion in revenue, representing a 13.9% increase from Q1 2024:

The financial highlights reveal:

- Operating earnings of $1,268 million, up 22.4% year-over-year

- Operating margin of 10.4%, an increase of 70 basis points

- Net earnings of $994 million, up 24.4% from Q1 2024

- Diluted EPS of $3.66, representing a 27.1% increase

- Total (EPA:TTEF) estimated contract value of $141.33 billion, up 5.5%

These results demonstrate a significant improvement over the company’s Q4 2024 performance, where General Dynamics reported EPS of $4.15 on revenue of $13.34 billion.

Segment Analysis

Aerospace

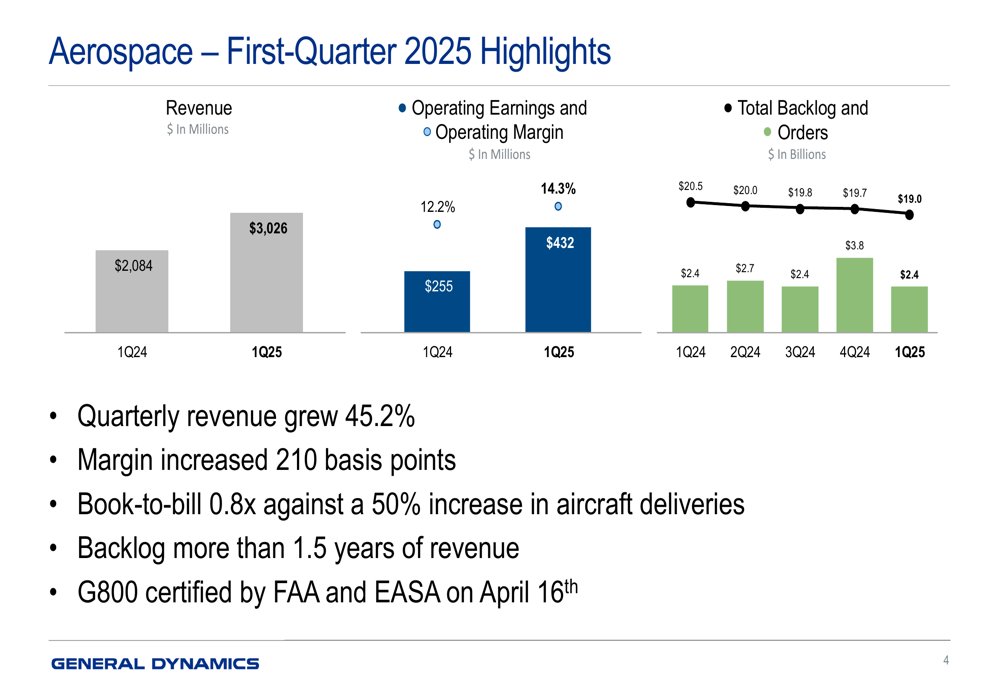

The Aerospace segment emerged as the standout performer in Q1 2025, showing exceptional growth in both revenue and profitability. The segment’s revenue surged by 45.2% year-over-year to $3.03 billion, while operating margins expanded by 210 basis points to 14.3%.

The following slide illustrates the segment’s impressive performance:

Key achievements in the Aerospace segment include:

- A 50% increase in aircraft deliveries despite a book-to-bill ratio of 0.8x

- Backlog representing more than 1.5 years of revenue

- FAA and EASA certification of the G800 on April 16, 2025

This performance is particularly noteworthy given the challenges the company faced with G700 deliveries in late 2024, as mentioned in their previous earnings call.

Combat Systems

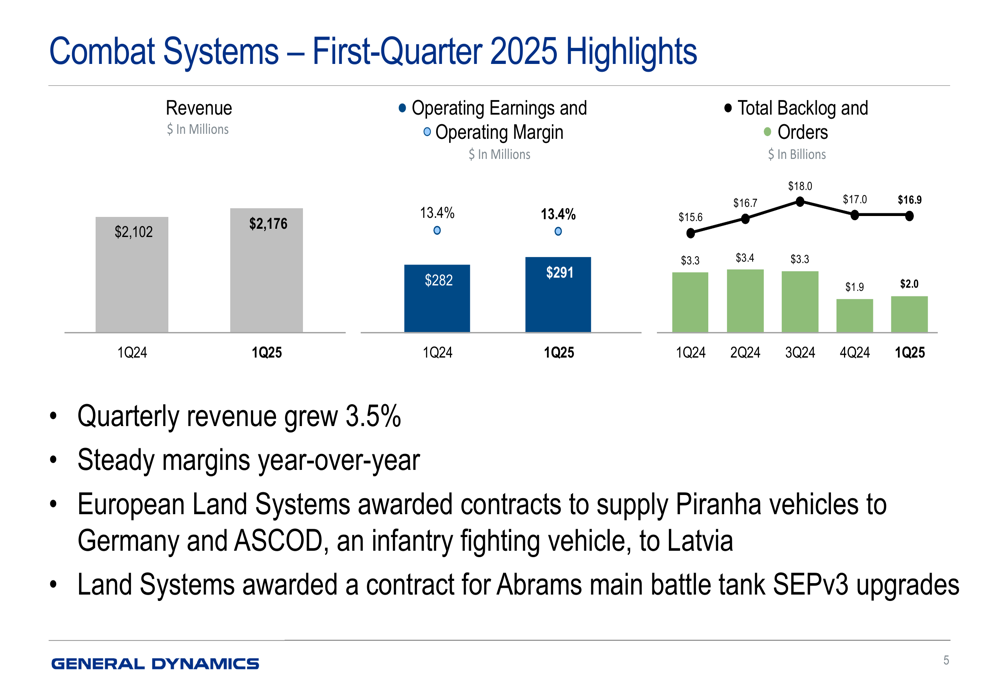

The Combat Systems segment reported modest but steady growth in Q1 2025, with revenue increasing by 3.5% to $2.18 billion while maintaining a strong operating margin of 13.4%.

As shown in the following slide, the segment secured important contract wins:

Notable developments in Combat Systems include:

- European Land Systems awarded contracts to supply Piranha vehicles to Germany

- Contract for ASCOD infantry fighting vehicles to Latvia

- New contract for Abrams main battle tank SEPv3 upgrades

The segment’s total backlog stood at $16.9 billion, providing visibility for future revenue growth.

Marine Systems

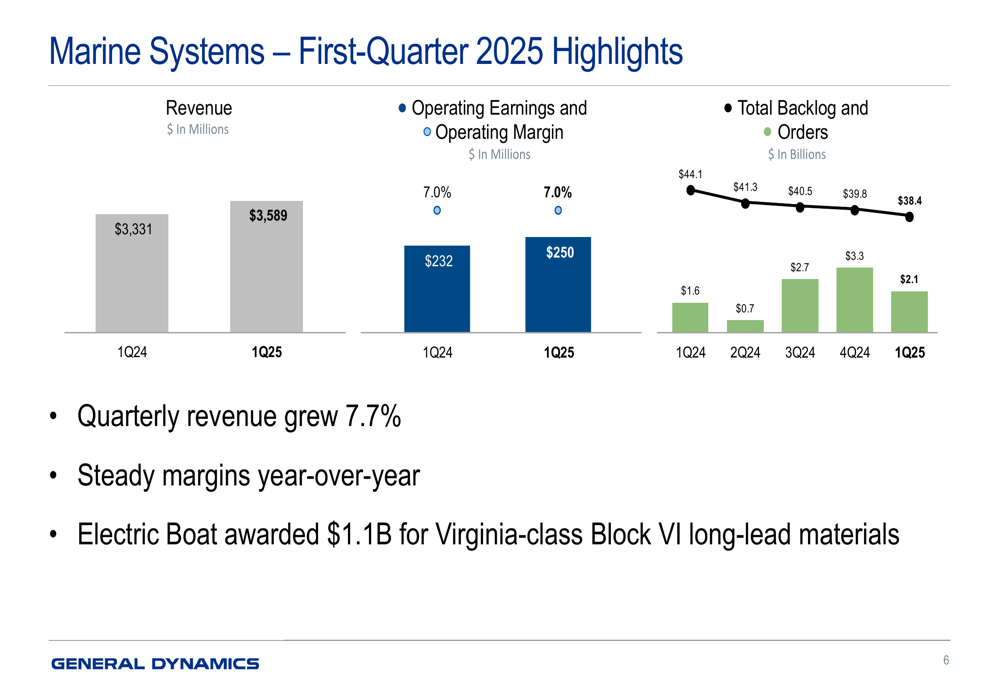

The Marine Systems segment continued its growth trajectory with revenue increasing by 7.7% to $3.59 billion, while maintaining a steady operating margin of 7.0%.

The following slide details the segment’s performance:

A significant highlight for Marine Systems was Electric Boat being awarded $1.1 billion for Virginia-class Block VI long-lead materials. The segment’s backlog remained substantial at $38.4 billion, though it has decreased from $44.1 billion in Q1 2024.

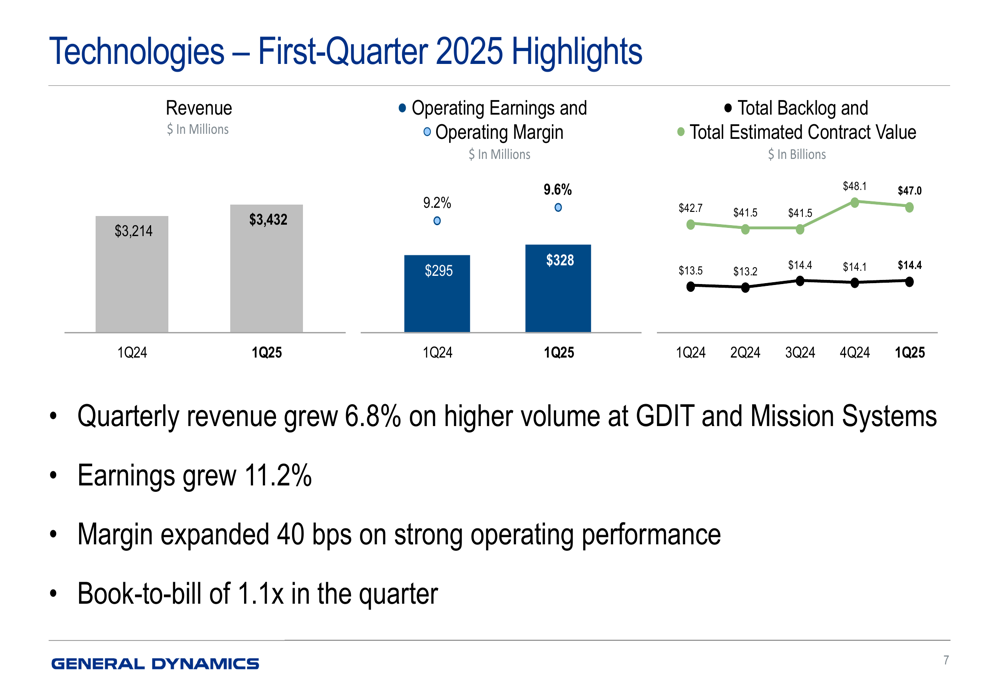

Technologies

The Technologies segment delivered solid performance with revenue growing 6.8% to $3.43 billion and operating earnings increasing by 11.2%. The segment’s operating margin expanded by 40 basis points to 9.6%.

As illustrated in the following slide, the segment achieved a book-to-bill ratio of 1.1x:

The segment’s total estimated contract value increased to $47.0 billion, up from $42.7 billion in Q1 2024, providing a strong foundation for future growth.

Financial Analysis

General Dynamics’ Q1 2025 results demonstrate a company firing on all cylinders, with all business segments contributing to overall growth. The 13.9% increase in revenue and 27.1% increase in EPS reflect both volume growth and improved operational efficiency.

The company’s operating margin expansion of 70 basis points to 10.4% is particularly impressive given the scale of its operations. This margin improvement was driven primarily by the Aerospace segment, which saw margins increase by 210 basis points, and the Technologies segment, which improved margins by 40 basis points.

The total estimated contract value of $141.33 billion provides substantial visibility for future revenue, representing a 5.5% increase from the prior year. This growth in backlog, coupled with strong book-to-bill ratios in key segments, suggests continued momentum throughout 2025.

Forward-Looking Statements

While the presentation did not provide explicit guidance for the remainder of 2025, the strong Q1 results position General Dynamics well to meet or exceed the expectations set during their Q4 2024 earnings call. At that time, the company forecasted a 5.5% increase in revenue for 2025, expecting to reach $50.3 billion, with an EPS projection of $14.80.

The certification of the G800 by both FAA and EASA on April 16th represents a significant milestone that should support continued growth in the Aerospace segment. Additionally, the robust order activity across defense segments, particularly in Combat Systems and Technologies, provides a solid foundation for sustained performance.

Given the current geopolitical environment and increased defense spending by the U.S. and its allies, General Dynamics appears well-positioned to capitalize on growing demand for its products and services across all business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.