U.S. stocks edge higher after weekly jobless claims; Salesforce gains

Introduction & Market Context

General Dynamics Corporation (NYSE:GD) released its second-quarter 2025 financial results on July 23, showcasing strong performance across all business segments. The defense and aerospace giant reported an 8.9% increase in revenue and a 14.7% jump in earnings per share, continuing the momentum from its strong first quarter.

The company’s stock responded positively to the results, rising 2.91% to $306.25 in premarket trading, building on its previous close of $297.60. This performance places the stock closer to its 52-week high of $316.90 than its low of $239.20, reflecting investor confidence in the company’s execution and growth trajectory.

Quarterly Performance Highlights

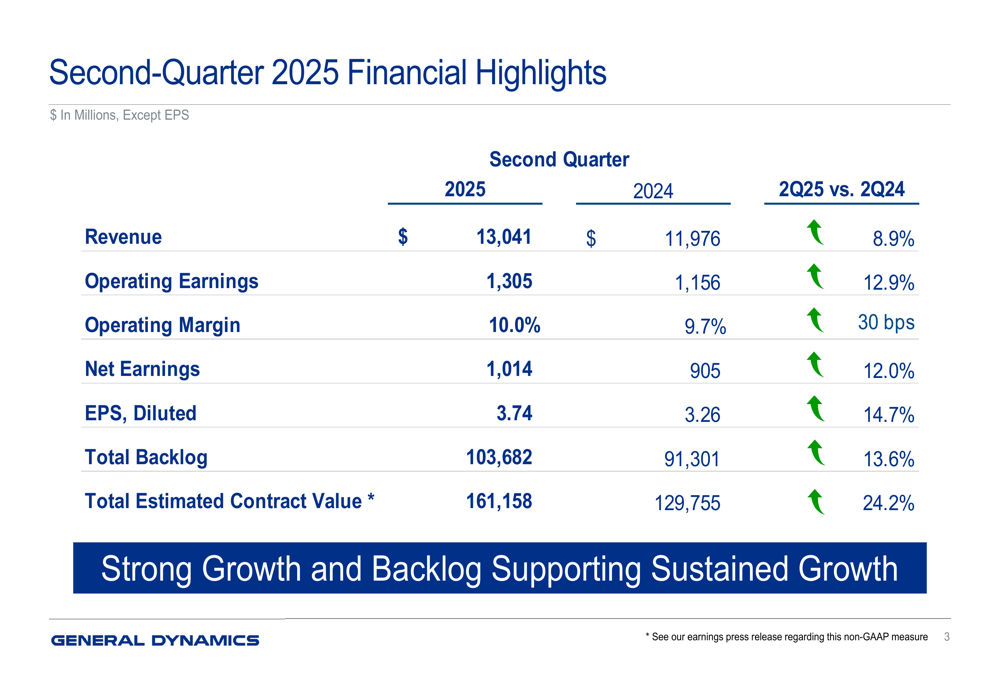

General Dynamics reported second-quarter revenue of $13.04 billion, an 8.9% increase from the $11.98 billion reported in the same period last year. Operating earnings rose 12.9% to $1.31 billion, while net earnings increased 12.0% to $1.01 billion. Diluted earnings per share reached $3.74, a 14.7% improvement over Q2 2024.

The company’s operating margin expanded to 10.0%, up 30 basis points from 9.7% in the prior-year quarter, demonstrating improved operational efficiency across the business.

As shown in the following comprehensive financial summary:

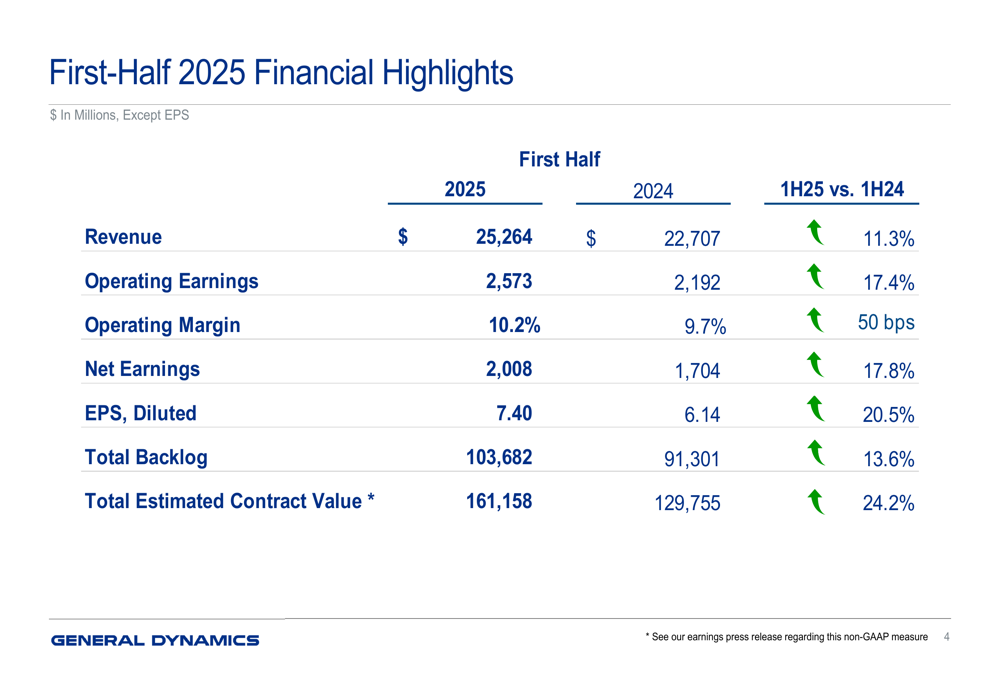

For the first half of 2025, General Dynamics reported even stronger results, with revenue up 11.3% to $25.26 billion and operating earnings increasing 17.4% to $2.57 billion. The six-month operating margin improved by 50 basis points to 10.2%, while diluted EPS grew 20.5% to $7.40.

The first-half performance builds on the company’s strong Q1 results, when it exceeded analyst expectations with EPS of $3.66 against a forecast of $3.45.

Segment Analysis

General Dynamics’ performance was driven by growth across its four major business segments, with particularly strong showings in Aerospace and Marine Systems.

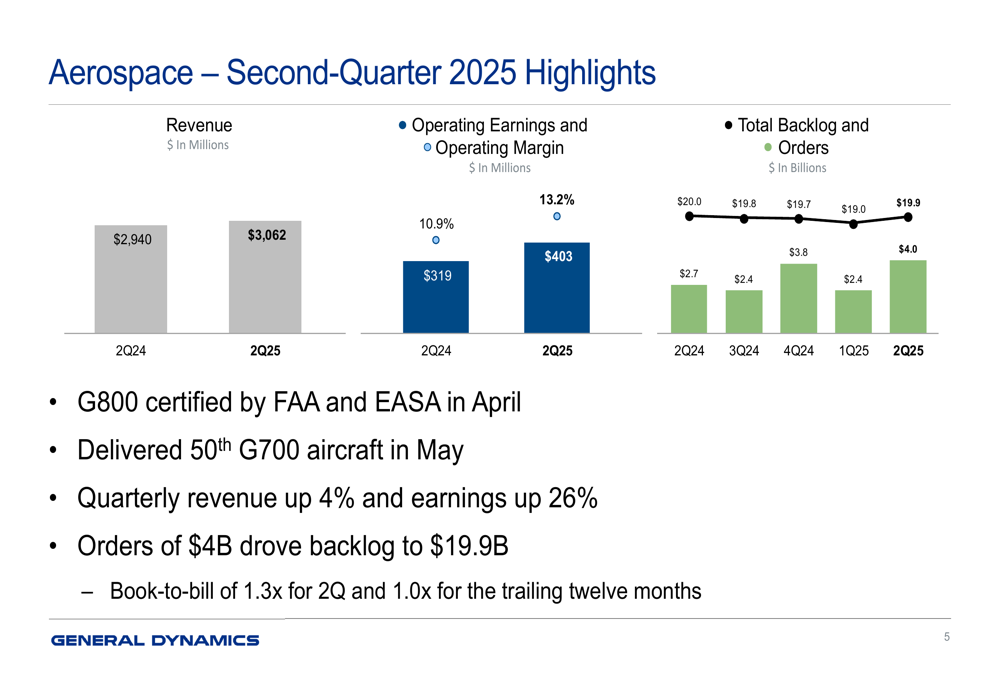

The Aerospace segment, which includes Gulfstream business jets, posted a 4% revenue increase to $3.06 billion, while operating earnings surged 26% year-over-year. The segment’s operating margin expanded significantly to 13.2% from 10.9% in Q2 2024. Key milestones included FAA and EASA certification of the G800 in April and delivery of the 50th G700 aircraft in May. Strong orders of $4 billion drove the segment’s backlog to $19.9 billion.

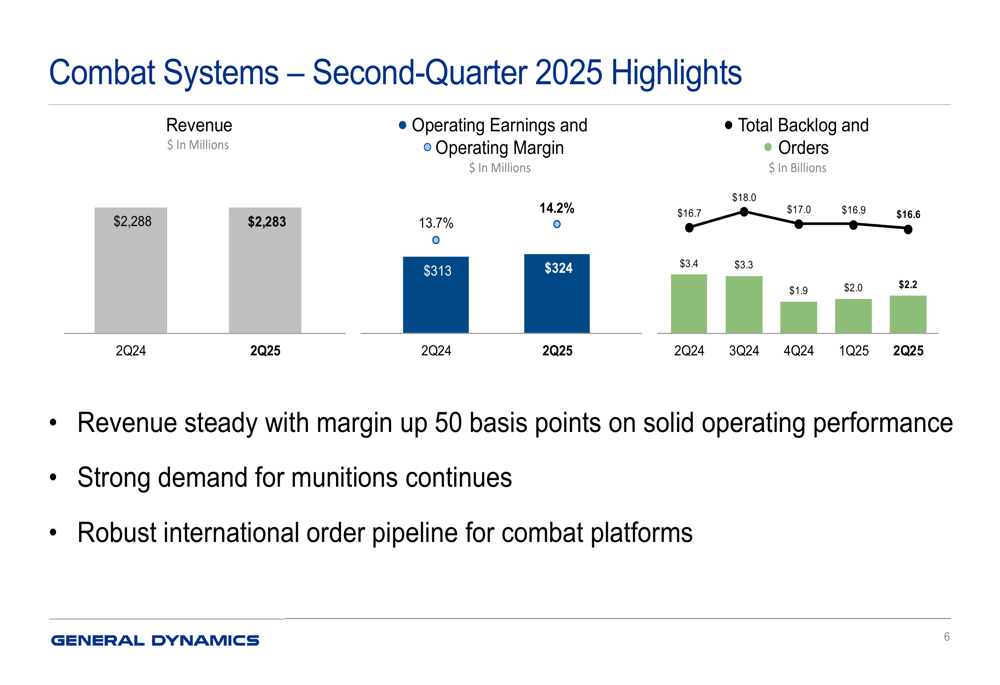

Combat Systems revenue remained essentially flat at $2.28 billion, but the segment improved its operating margin by 50 basis points to 14.2%. Management highlighted continued strong demand for munitions and a robust international order pipeline for combat platforms.

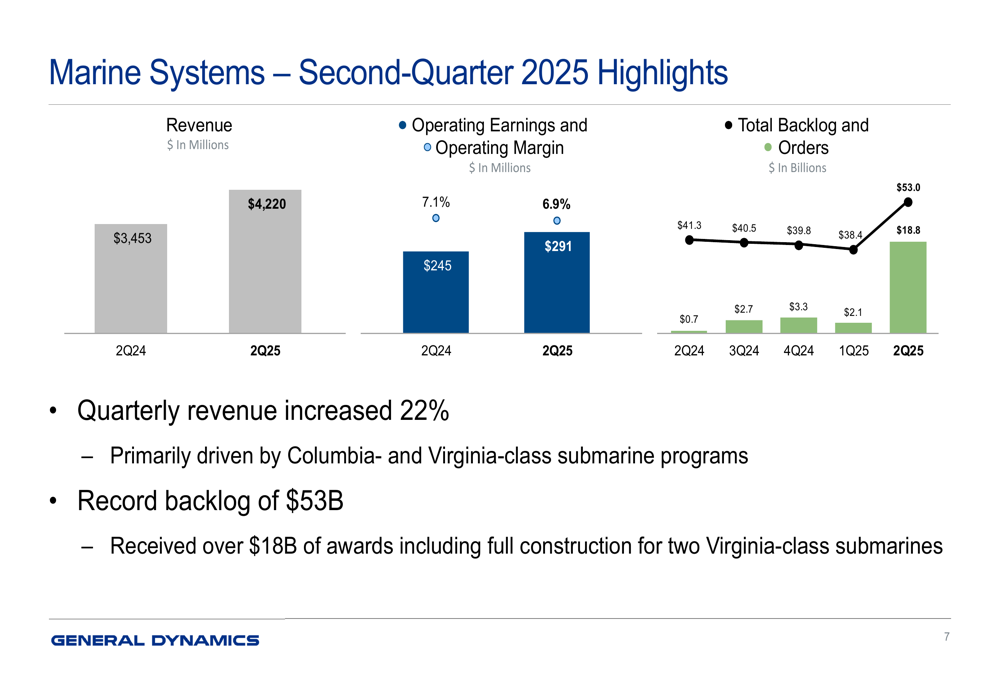

The Marine Systems segment delivered the strongest revenue growth, jumping 22% to $4.22 billion, primarily driven by Columbia- and Virginia-class submarine programs. Operating earnings increased to $291 million from $245 million, though operating margin contracted slightly to 6.9% from 7.1%. The segment secured over $18 billion in new awards, including full construction contracts for two Virginia-class submarines, pushing its backlog to a record $53 billion.

The Technologies segment, which encompasses IT services and mission systems, grew revenue by over 5% to $3.48 billion. Operating earnings increased slightly to $332 million, with margins holding relatively steady at 9.6% compared to 9.7% in the prior year. The segment maintained a book-to-bill ratio of 1.1x for the trailing twelve months.

Backlog and Future Outlook

One of the most significant highlights from the presentation was the substantial growth in General Dynamics’ backlog, which increased 13.6% year-over-year to $103.7 billion. The total estimated contract value, which includes options and indefinite delivery, indefinite quantity contracts, grew even more impressively, up 24.2% to $161.2 billion.

This robust backlog provides General Dynamics with significant revenue visibility for the coming years, particularly in the Marine Systems segment, where submarine construction programs offer long-term stability. The Aerospace segment’s book-to-bill ratio of 1.3x for the quarter indicates continued strong demand for business jets, despite economic uncertainties.

The company’s performance in the first half of 2025 positions it well to meet or exceed the full-year guidance established in January. This outlook aligns with the company’s statement during its Q1 earnings call, where management anticipated continued revenue growth and modestly positive cash flow in Q2 2025.

Stock Performance and Investor Implications

General Dynamics’ stock has shown resilience in 2025, trading near its 52-week high despite broader market volatility. The premarket gain of 2.91% following the Q2 results contrasts with the market’s reaction to Q1 earnings, when the stock fell 2.15% despite beating expectations.

The company’s consistent performance, expanding margins, and growing backlog provide a solid foundation for investors seeking stability in the defense sector. With 47 consecutive years of dividend payments and a yield of approximately 2.18% (based on Q1 data), General Dynamics continues to offer an attractive combination of growth and income.

The presentation reinforces the company’s strong competitive position across its diverse business segments, with particular strength in submarine construction and business aviation. As global defense spending increases in response to geopolitical tensions, and as the business jet market continues its post-pandemic recovery, General Dynamics appears well-positioned to capitalize on these trends through the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.