BofA warns Fed risks policy mistake with early rate cuts

Introduction & Market Context

General Mills (NYSE:GIS) presented its fourth-quarter and full-year fiscal 2025 earnings results on June 25, 2025, highlighting met guidance but continued sales challenges. The consumer packaged goods giant is down 2.08% in pre-market trading, extending the negative trend seen after its Q3 report when the stock fell 2.97%.

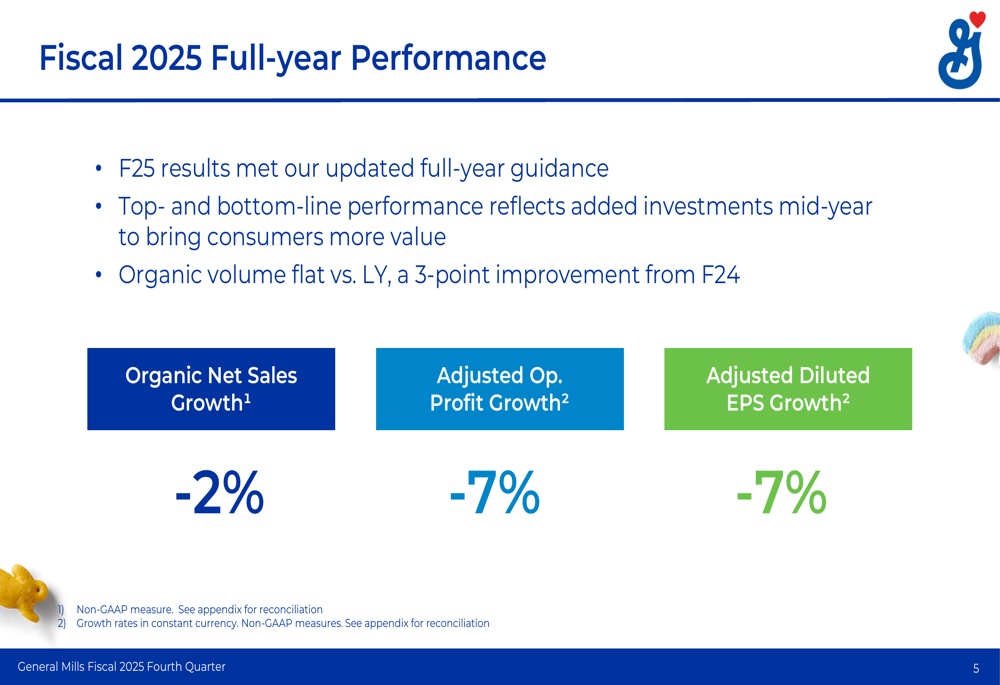

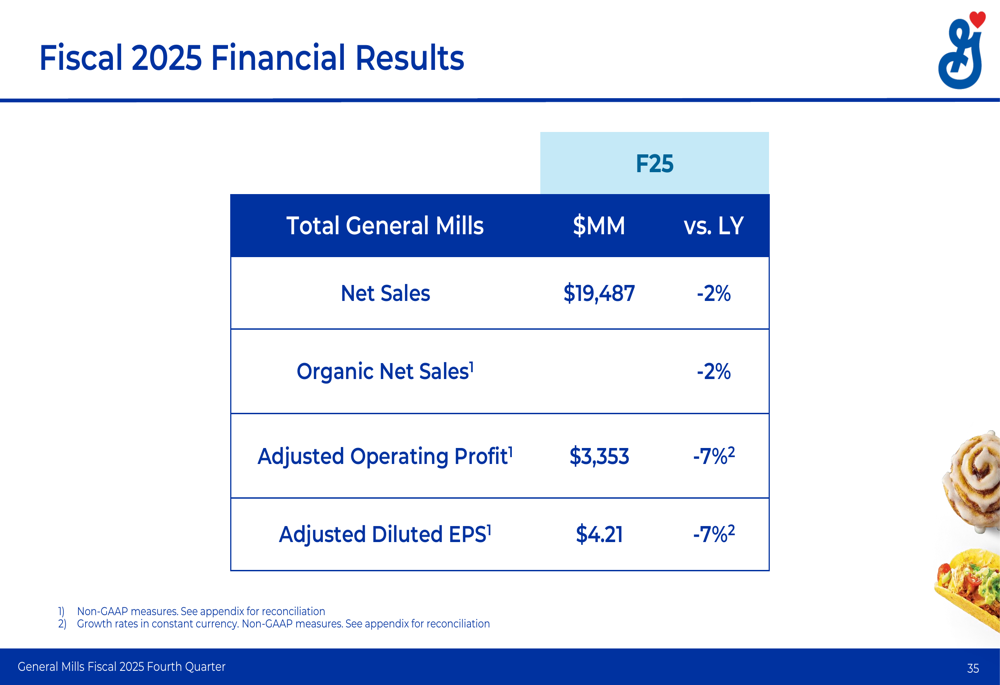

The company reported Q4 organic net sales decline of 3% while maintaining flat organic volume, emphasizing its progress in volume trends despite continued price/mix headwinds. For the full fiscal year 2025, organic net sales declined 2%, with adjusted operating profit and diluted EPS both down 7%.

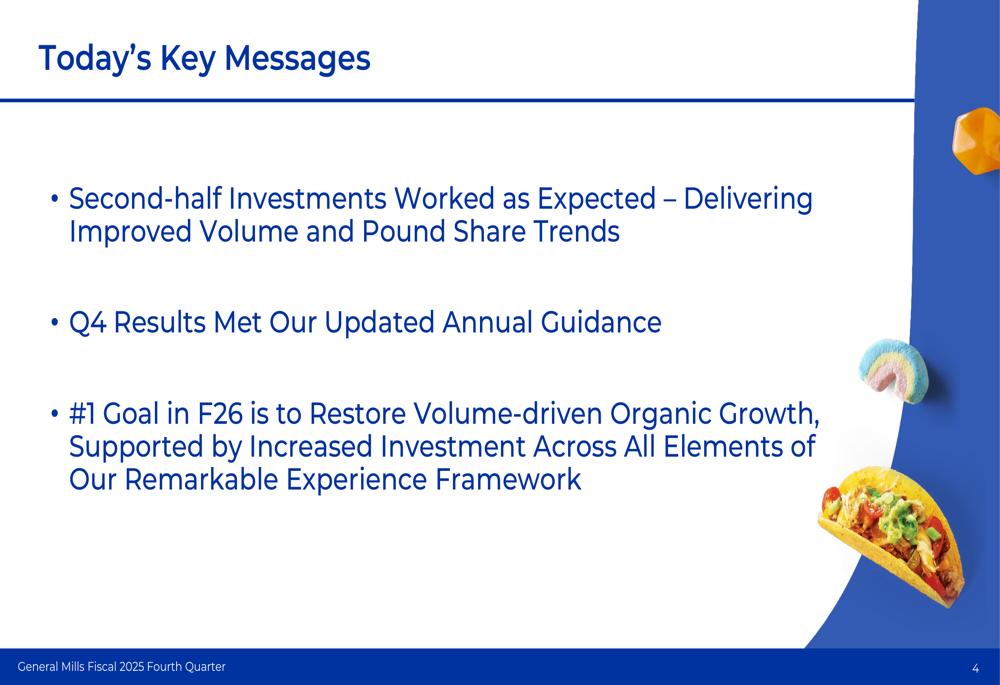

As shown in the following key messages slide, General Mills is focusing on volume-driven growth after investments in the second half of fiscal 2025:

Quarterly Performance Highlights

General Mills met its updated annual guidance for fiscal 2025, with results reflecting the company’s mid-year pivot to invest more heavily in bringing consumers greater value. The company highlighted that organic volume was flat versus last year, representing a 3-point improvement from fiscal 2024.

The fourth quarter showed mixed segment performance. North America Retail, the company’s largest segment, saw organic net sales decline 7% in Q4, with segment operating profit down 29%. North America Pet delivered 3% organic net sales growth in Q4, though segment operating profit decreased 3%. International was the standout performer with 9% organic net sales growth and 42% increase in segment operating profit for the quarter.

The following slide summarizes the company’s full-year fiscal 2025 performance:

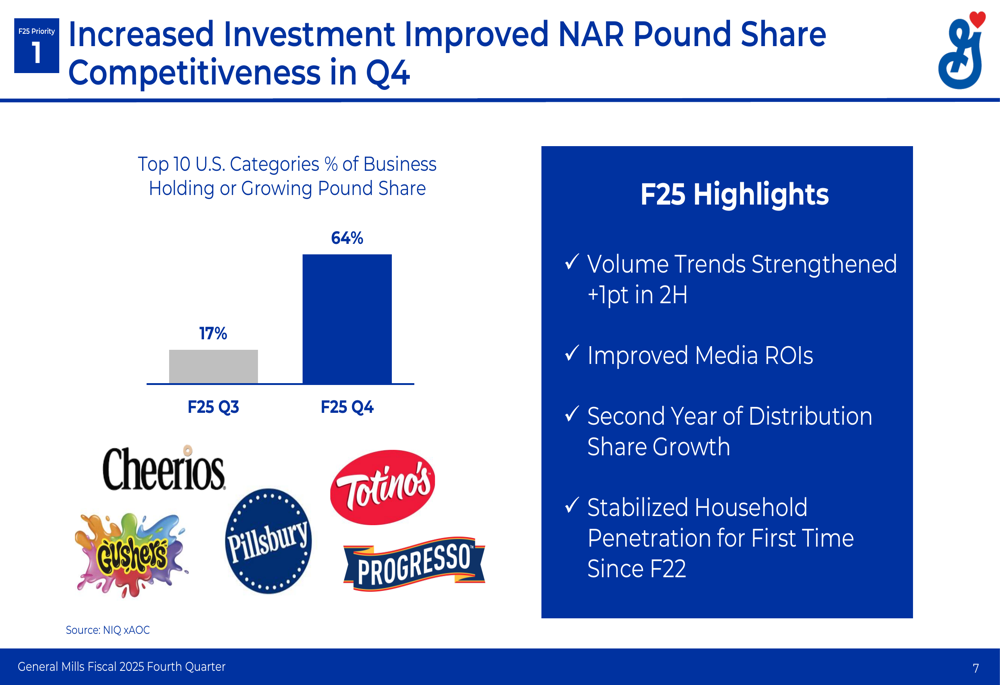

A key achievement highlighted in the presentation was the significant improvement in market share metrics. In North America Retail, the percentage of top 10 U.S. categories holding or growing pound share jumped from 17% in Q3 to 64% in Q4, demonstrating the effectiveness of the company’s increased investments.

As illustrated in this competitive performance slide:

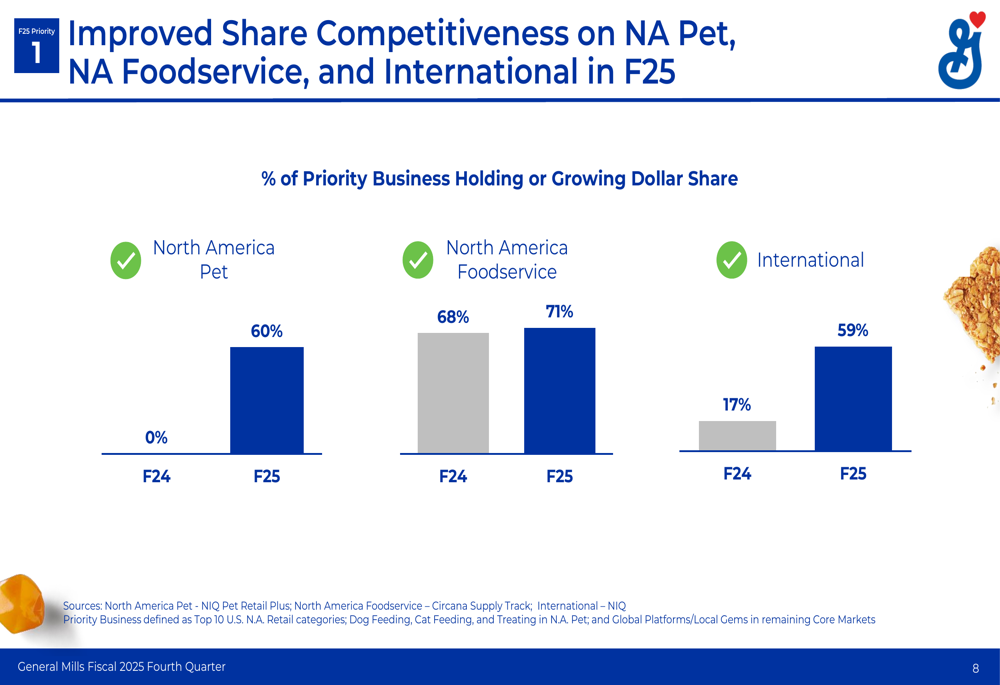

Similar share improvements were seen across other segments, with North America Pet increasing from 0% in fiscal 2024 to 60% in fiscal 2025, and International improving from 17% to 59%:

Strategic Initiatives

General Mills outlined its "remarkability" framework as the cornerstone of its strategy to restore volume-driven organic growth in fiscal 2026. This approach focuses on five key elements: superior product, package design, brand communication, omnichannel execution, and compelling value.

The company is investing significantly across these areas, with particular emphasis on product innovation and value. Management highlighted a 25% increase in new product sales versus last year and plans for significant product news across all top 10 U.S. categories.

The following slide details the company’s investment approach to drive North America Retail back to volume growth:

Product innovation is a central pillar of the strategy, with new offerings spanning multiple categories and consumer needs. The company showcased innovations across its portfolio, organized around consumer trends like protein, bold flavors, and familiar favorites:

In the pet food segment, General Mills is expanding its portfolio beyond the core Blue Buffalo brand. A major initiative is the national launch of "Love Made Fresh," a fresh pet food line coming to stores later this year. This expansion will make Blue Buffalo the largest U.S. pet food brand offering solutions across dry, wet, and fresh feeding formats.

As shown in the following slide detailing the Love Made Fresh launch:

Detailed Financial Analysis

General Mills’ fiscal 2025 financial results showed pressure on both top and bottom lines. The company’s adjusted gross margin decreased slightly from 34.8% in fiscal 2024 to 34.5% in fiscal 2025, while adjusted operating profit margin declined more significantly from 18.1% to 17.2%.

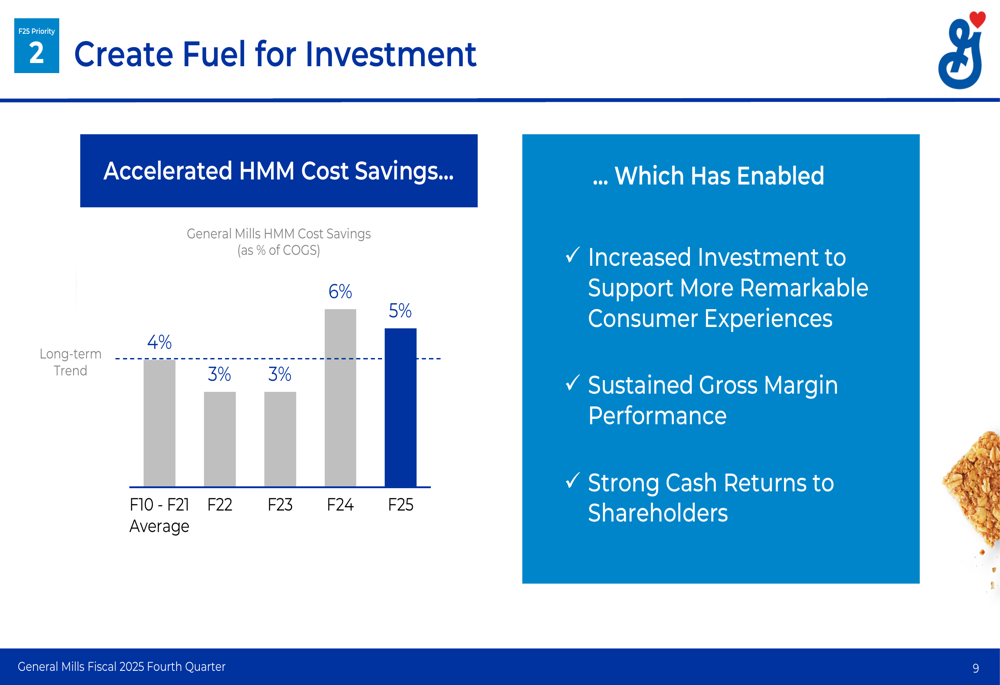

The company attributed the margin decline to input cost inflation, unfavorable price/mix, and volume deleverage, partially offset by Holistic Margin Management (HMM) cost savings. These cost savings reached 5% of cost of goods sold in fiscal 2025, slightly down from 6% in fiscal 2024 but still above the long-term trend of 4%.

The following slide illustrates the company’s HMM cost savings trend:

Despite margin pressure, General Mills maintained strong cash generation with free cash flow conversion of 97%, exceeding its long-term target of 95%+. The company returned $2.5 billion to shareholders through dividends and share repurchases during fiscal 2025.

The comprehensive fiscal 2025 financial results are presented in this slide:

Forward-Looking Statements

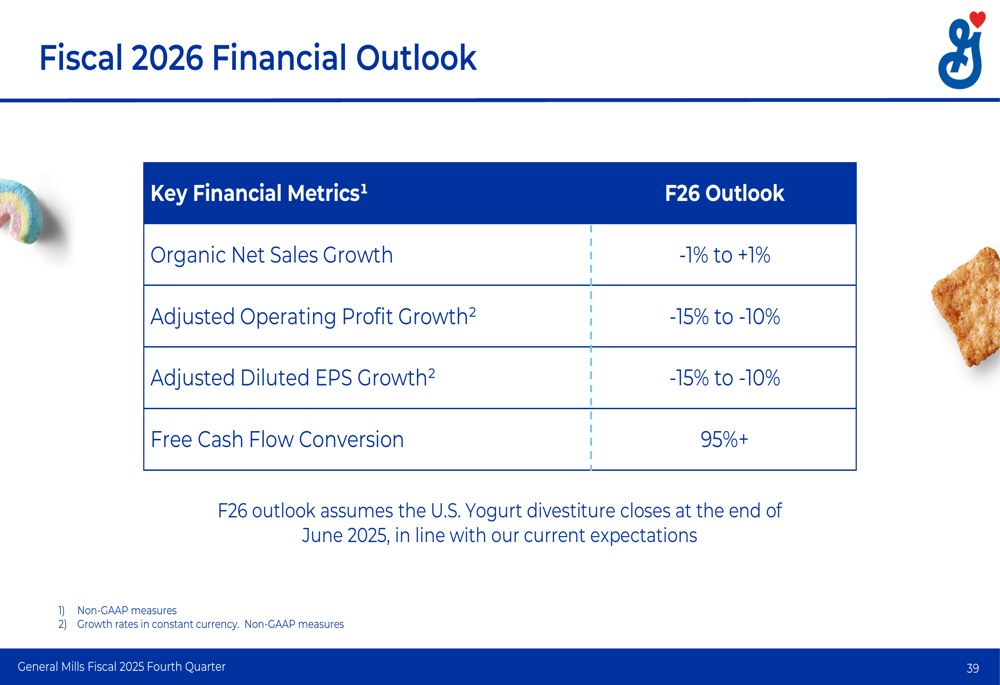

Looking ahead to fiscal 2026, General Mills outlined a challenging but strategic year focused on restoring volume-driven organic growth. The company’s financial outlook projects organic net sales growth between -1% and +1%, with adjusted operating profit and adjusted diluted EPS both expected to decline between 15% and 10%.

This significant projected profit decline reflects substantial investments in remarkability, including the national launch of fresh pet food, as well as the net impact of yogurt divestitures and pet acquisitions (approximately 5 percentage points) and incentive compensation reset (approximately 3 percentage points).

CFO Kofi Bruce noted that the company expects to offset some of these pressures through HMM cost savings of approximately 5% of COGS and an additional $100 million in cost savings from a new global transformation initiative.

The fiscal 2026 outlook is summarized in the following slide:

Chairman and CEO Jeff Harmening emphasized that the company’s "#1 goal in F26 is to restore volume-driven organic growth," supported by increased investment across all elements of the remarkability framework. This pivot comes as General Mills navigates a challenging consumer environment where value-seeking behavior continues to pressure sales.

The company’s strategic focus on volume growth represents a shift from recent years’ emphasis on price/mix, reflecting the changing consumer landscape and competitive dynamics in the packaged food industry. With category growth expected to remain below long-term expectations, General Mills is betting that its investments in product innovation and value will strengthen its competitive position and drive sustainable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.