Street Calls of the Week

Introduction & Market Context

Gentian Diagnostics AS (OB:GENT) presented its Q1 2025 results on May 7, 2025, highlighting record sales and significant margin expansion. The company, which specializes in developing and manufacturing high-quality diagnostic tests, reported continued momentum following its strong Q4 2024 performance. Gentian’s stock closed at NOK 49.6 on May 6, representing a 0.4% increase on the day and continuing the positive trend seen after the previous quarter’s results.

The company operates in a diagnostic market estimated at $1.8 billion with annual growth of 5-10%. Gentian’s business model focuses on converting clinically relevant diagnostic biomarkers from slow platforms to high-throughput analyzers, offering up to 10x improved efficiency and cost savings for healthcare providers.

Quarterly Performance Highlights

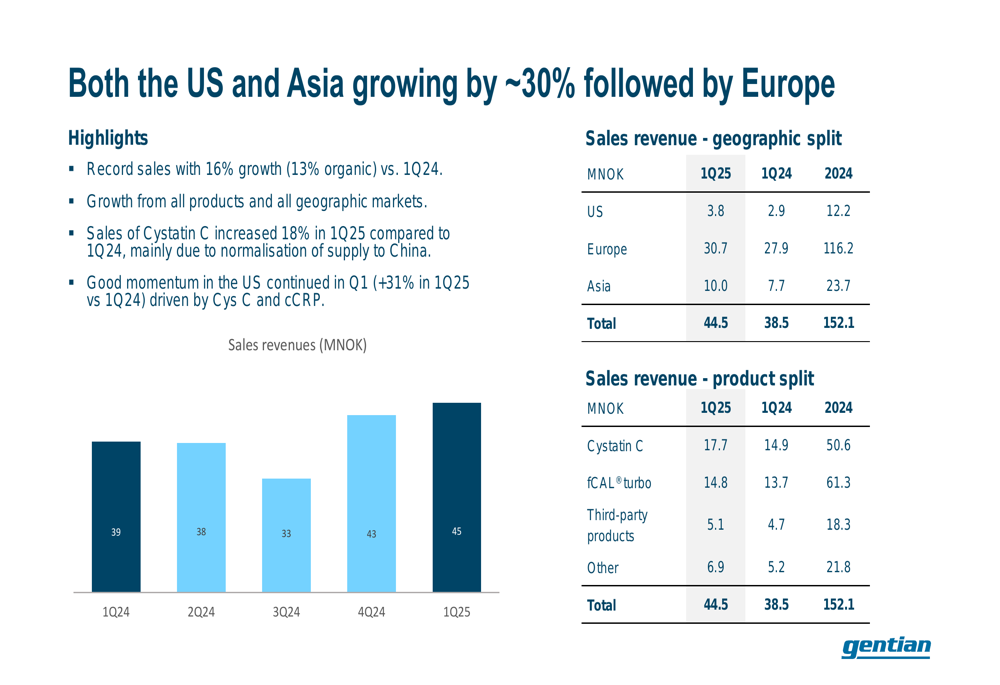

Gentian reported Q1 2025 sales of NOK 44.5 million, representing a 16% increase compared to Q1 2024. The company achieved a record gross margin of 64%, up significantly from 53% in the same period last year. This margin expansion, combined with stable operating expenses, drove EBITDA to NOK 14.0 million, nearly tripling from NOK 4.8 million in Q1 2024.

As shown in the following chart of quarterly highlights, the company demonstrated strong performance across all key metrics:

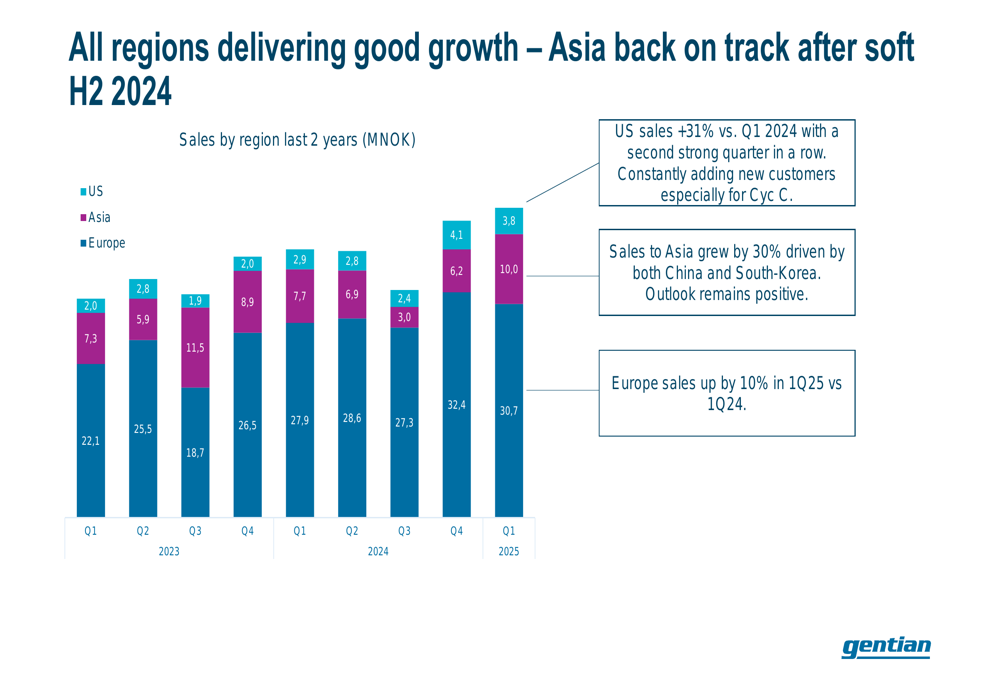

The sales growth was broad-based across all products and geographic markets. Notably, sales to Asia increased by 30% compared to Q1 2024, while US sales grew by 31%, and European sales rose by 10%. This regional diversification highlights the company’s successful expansion strategy beyond its European base.

The following chart illustrates the sales breakdown by region and product:

Detailed Financial Analysis

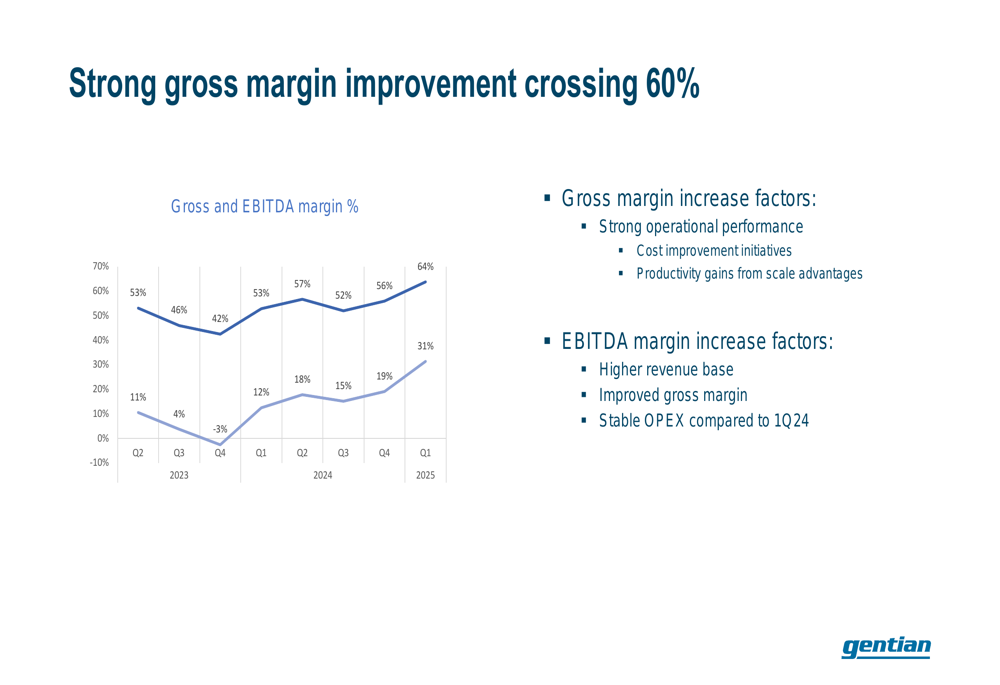

Gentian’s gross margin has shown consistent improvement over recent quarters, reaching 64% in Q1 2025. This represents a significant increase from 52% in Q1 2024 and 57% in Q4 2024. The company attributes this improvement to strong operational performance, cost improvement initiatives, and productivity gains from scale advantages.

The progression of gross and EBITDA margins over the past quarters is illustrated in the following chart:

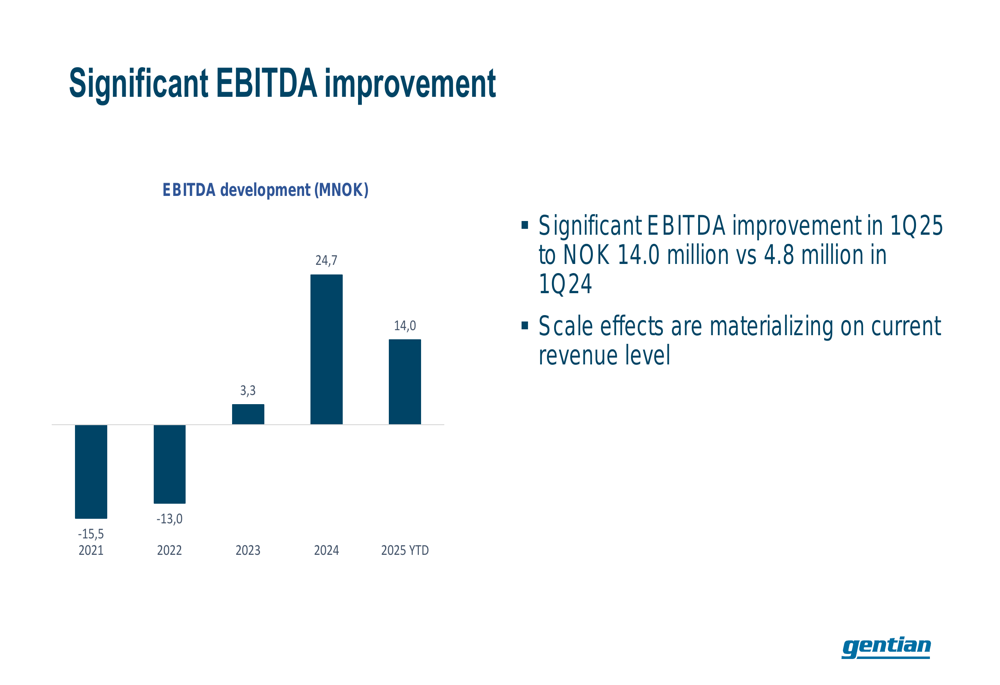

The EBITDA improvement has been particularly notable, with Q1 2025 contributing NOK 14.0 million to the total. This continues the positive trend seen in 2024, when the company achieved full-year EBITDA of NOK 24.7 million, a substantial improvement from NOK 3.3 million in 2023.

The following chart shows Gentian’s EBITDA development over recent years:

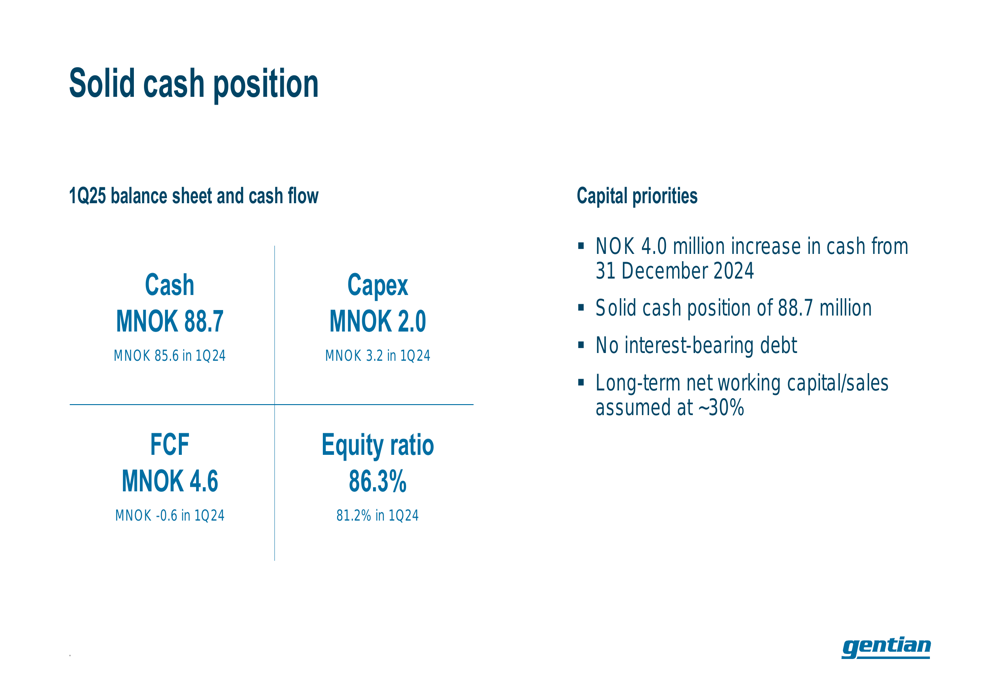

Gentian maintained a solid financial position with cash of NOK 88.7 million at the end of Q1 2025, up from NOK 85.6 million in Q1 2024 and NOK 84.7 million at the end of 2024. The company generated free cash flow of NOK 4.6 million in the quarter, compared to negative NOK 0.6 million in Q1 2024. With no interest-bearing debt and an equity ratio of 86.3%, Gentian has a strong foundation for future growth.

Product and Regional Performance

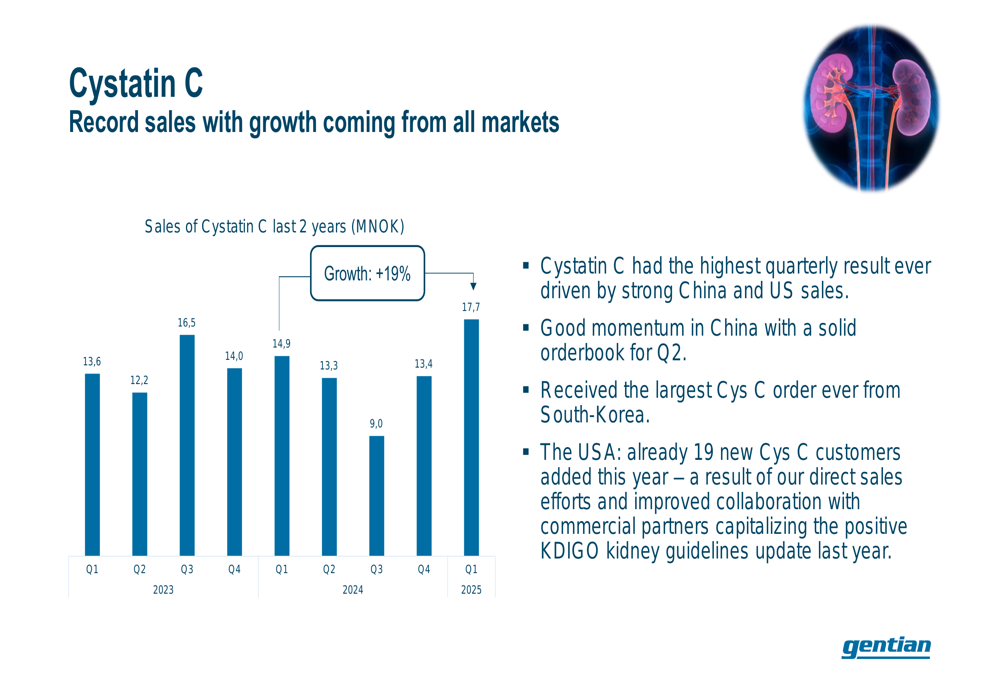

Cystatin C, Gentian’s kidney disease diagnostic product, achieved its highest quarterly sales ever at NOK 17.7 million, a 19% increase compared to Q1 2024. The growth was driven by strong performance in China and the US, with the company noting it had received its largest Cystatin C order ever from South Korea. In the US market, Gentian added 19 new Cystatin C customers in the first quarter alone.

The following chart shows Cystatin C’s sales performance over the past two years:

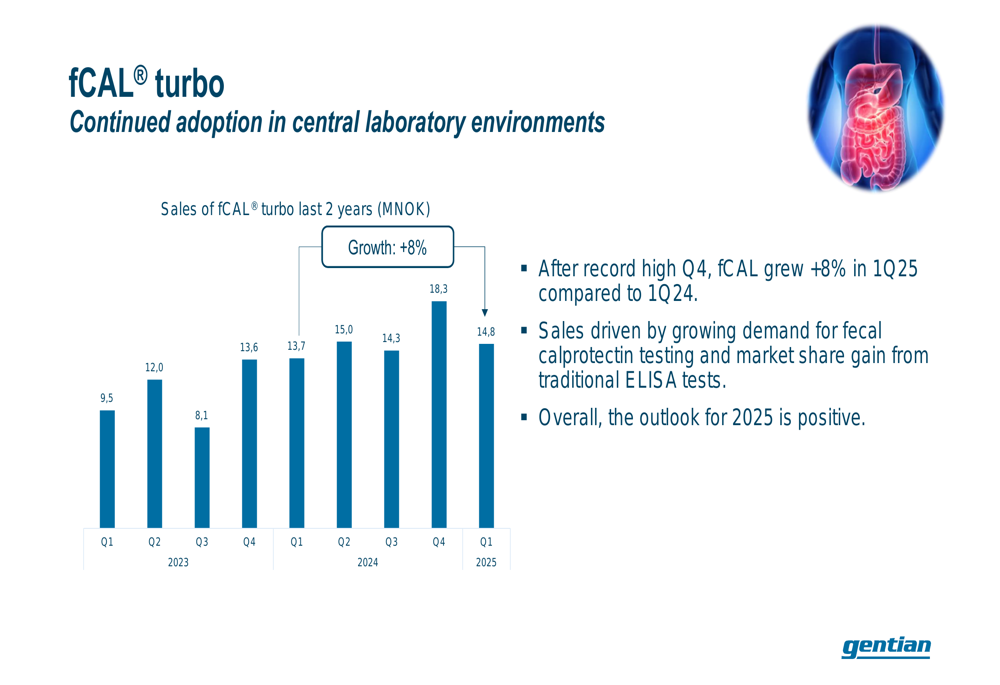

The company’s fCAL turbo product, used for inflammation testing, grew 8% to NOK 14.8 million in Q1 2025 compared to Q1 2024. This follows a record high Q4 2024, with growth driven by increasing demand for fecal calprotectin testing.

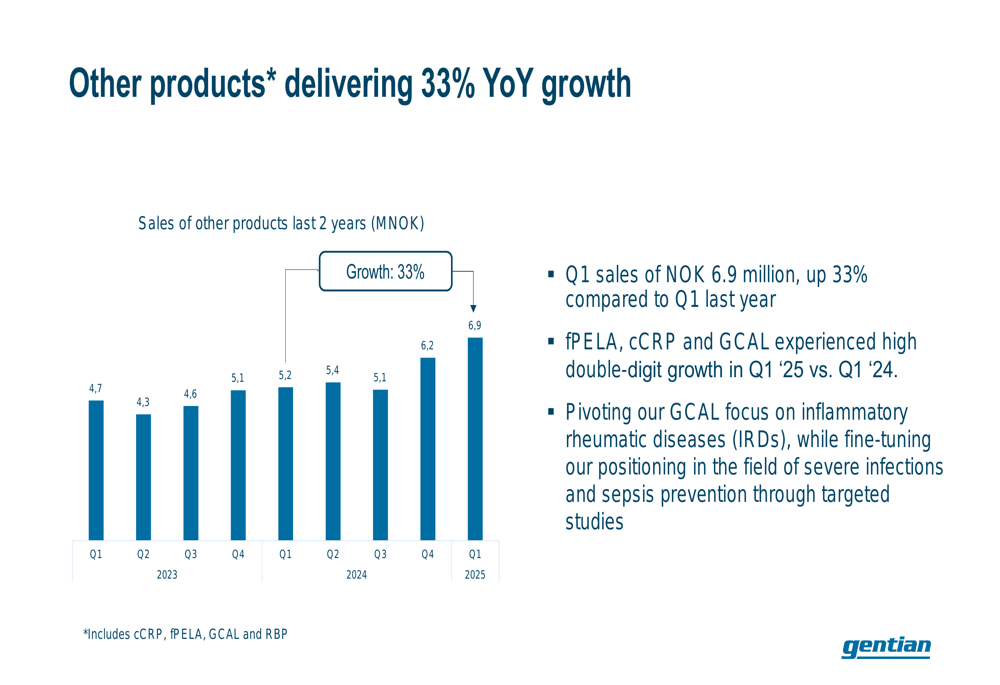

Other products, including fPELA, cCRP, and GCAL, experienced high double-digit growth, with total sales reaching NOK 6.9 million, up 33% from Q1 2024. The company is pivoting its GCAL focus toward inflammatory rheumatic diseases.

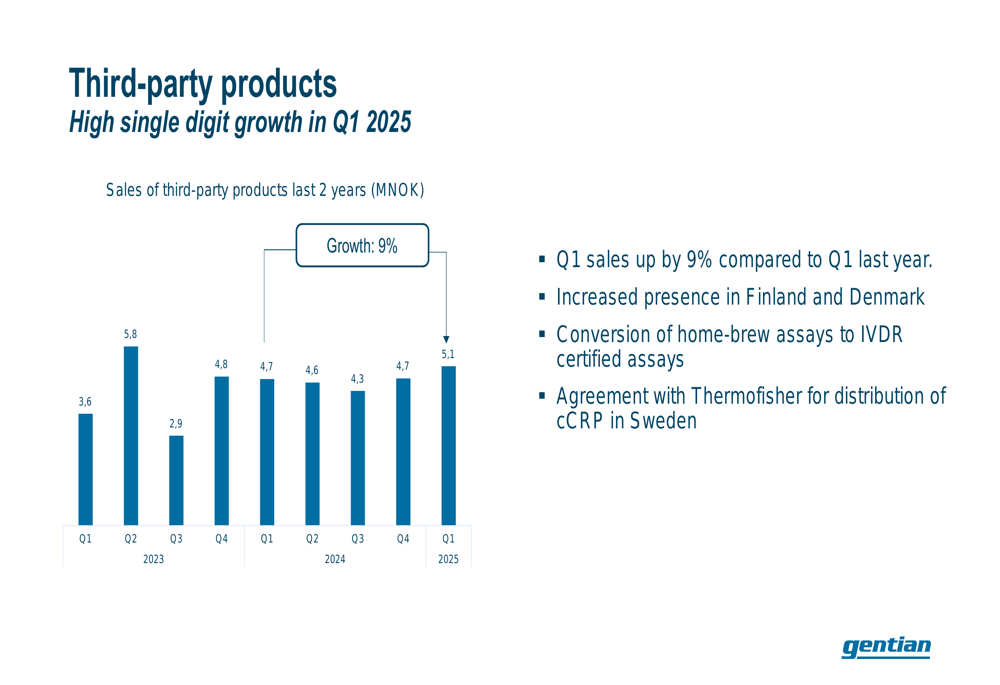

Third-party product sales grew 9% to NOK 5.1 million, supported by increased presence in Finland and Denmark and a new agreement with Thermofisher for distribution of CCRP in Sweden.

Regionally, Gentian saw growth across all markets. The US market grew 31% to NOK 3.8 million, while Asia increased 30% to NOK 10.0 million, driven by both China and South Korea. European sales rose 10% to NOK 30.7 million.

Strategic Initiatives and Outlook

Gentian continues to advance its product pipeline, with notable progress on its NT-proBNP cardiac marker test. The company has decided on a calibration strategy and will proceed with developing an assay detecting total NT-proBNP not affected by glycosylation. The company also reported that its patent application in Japan has been accepted.

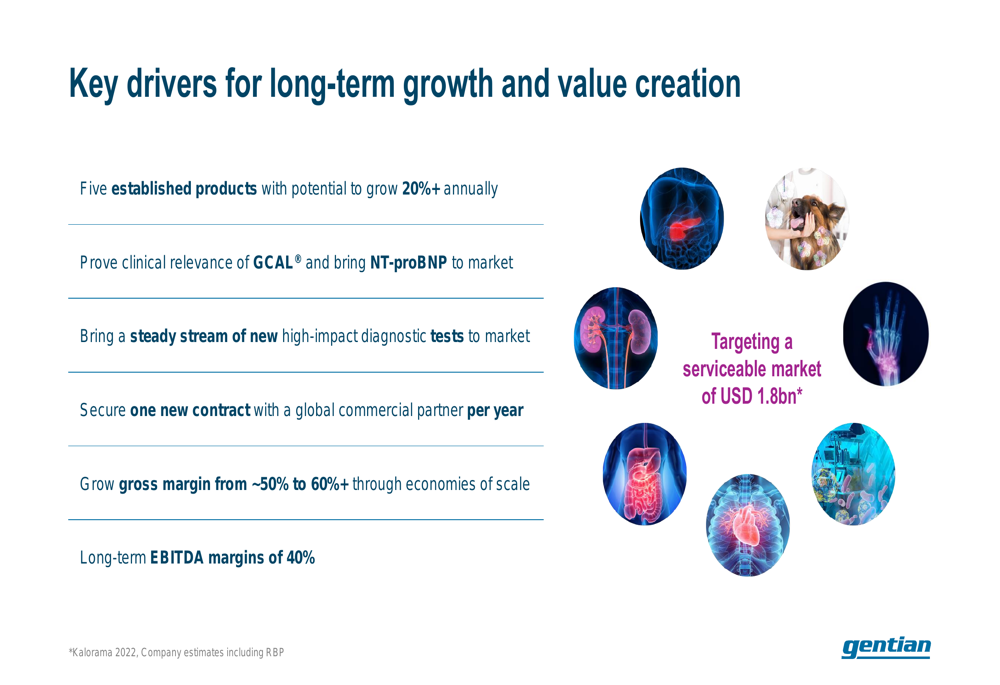

Looking ahead, Gentian aims to grow its established products by over 20% annually and achieve a gross margin of 60% or more through economies of scale. The company targets long-term EBITDA margins of 40% and plans to secure one new contract with a global commercial partner per year.

The company’s long-term growth strategy is built on five established products with potential to grow 20%+ annually, proving clinical relevance of GCAL and bringing NT-proBNP to market, introducing new high-impact diagnostic tests, securing new commercial partnerships, and improving margins through economies of scale.

With its strong Q1 2025 performance, Gentian Diagnostics has demonstrated that its business model is delivering results, with scale effects materializing at current revenue levels. The company’s focus on operational efficiency and geographic expansion, particularly in the US and Asian markets, positions it well for continued growth in the expanding diagnostic market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.