Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

Gentian Diagnostics (OB:GENT) presented its second quarter 2025 results on July 10, revealing a quarter of strong revenue growth overshadowed by production challenges that significantly impacted margins. The Norwegian diagnostics company, which specializes in high-throughput clinical testing solutions, reported 14% year-over-year revenue growth while experiencing a substantial decline in gross margin.

The company’s stock closed at 63.4 NOK on July 9, up 1.93% ahead of the earnings presentation, reflecting investor optimism following the company’s strong first quarter performance when it achieved a record 64% gross margin.

Quarterly Performance Highlights

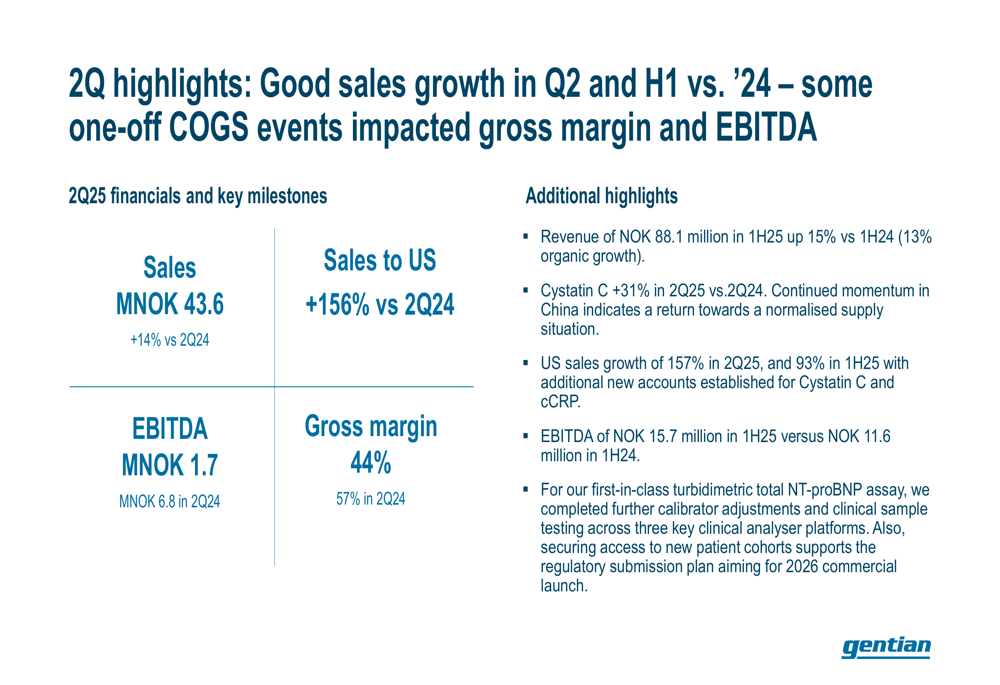

Gentian reported Q2 2025 sales of 43.6 million NOK, representing a 14% increase compared to the same period last year. This contributed to first-half 2025 revenue of 88.1 million NOK, up 15% year-over-year with 13% organic growth. The company’s EBITDA for the quarter came in at 1.7 million NOK, significantly lower than the 6.8 million NOK achieved in Q2 2024 and the 14 million NOK reported in Q1 2025.

As shown in the following quarterly highlights summary:

The most notable challenge in the quarter was the sharp decline in gross margin to 44%, compared to 57% in the same quarter last year. This decline was attributed to production issues and increased raw material costs, which the company indicated had stabilized by June. Despite these challenges, Gentian maintained its long-term gross margin target in the 55-60% range.

Regional Performance Analysis

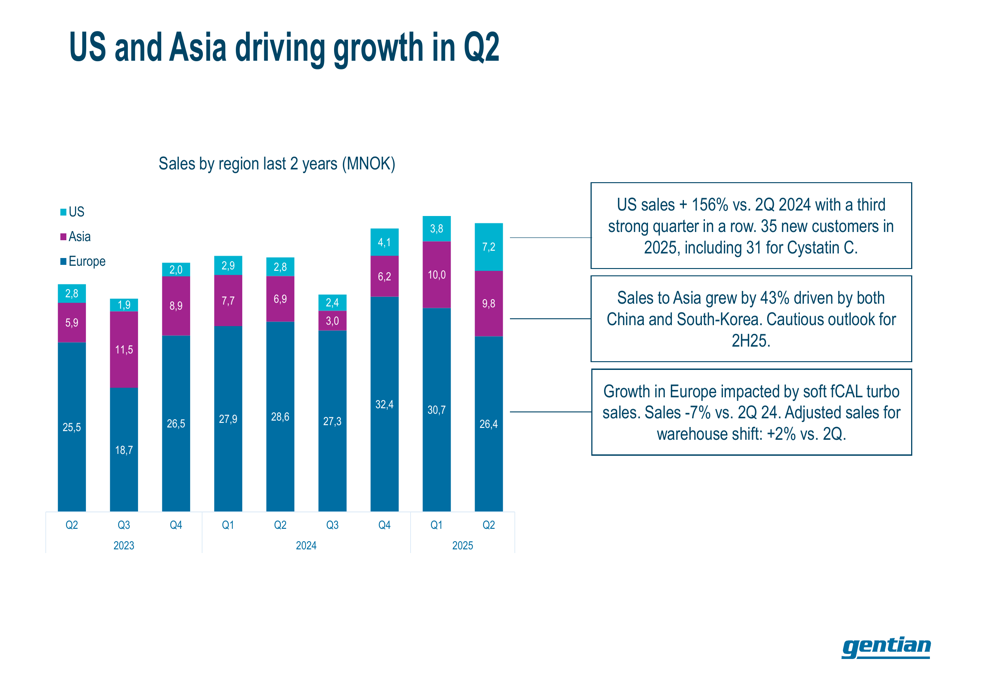

Gentian’s regional performance showed striking divergence, with exceptional growth in the US and Asia contrasting with softness in Europe. US sales surged by 156% compared to Q2 2024, marking the third consecutive quarter of strong performance in this market. The company added 35 new customers in the US during 2025, including 31 for its Cystatin C product.

Sales to Asia grew by 43%, driven by both China and South Korea, though the company expressed a cautious outlook for the second half of 2025. European sales declined by 7% year-over-year, primarily due to soft fCAL turbo sales, though the company noted that adjusting for warehouse shifts would show a modest 2% growth.

The following chart illustrates this regional sales performance:

Product Performance

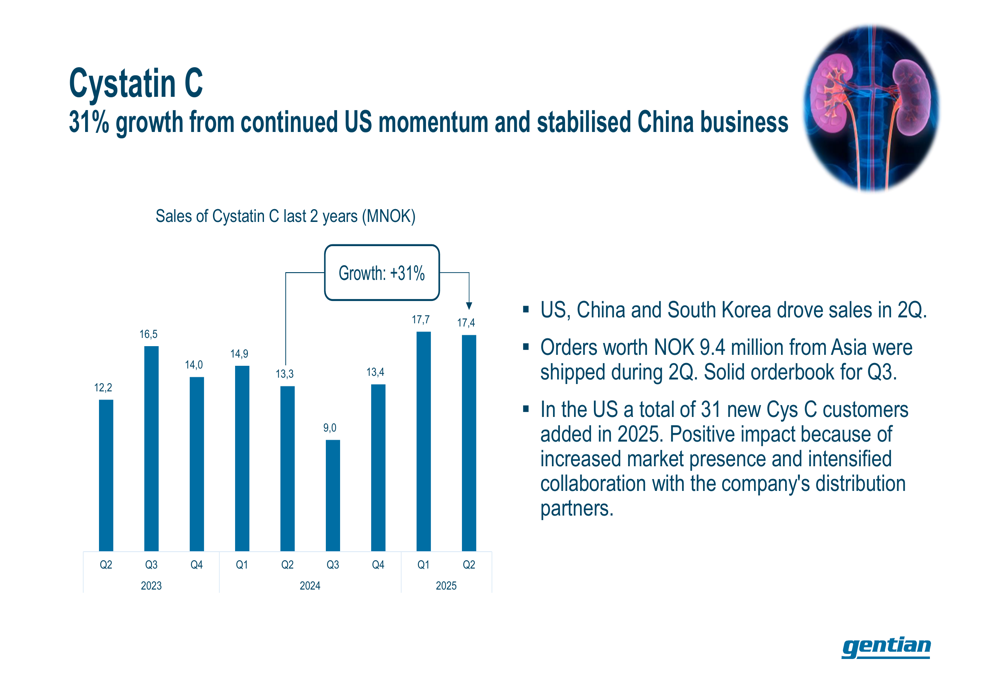

Cystatin C emerged as the standout performer in Gentian’s product portfolio, with sales increasing 31% year-over-year. This growth was driven by continued momentum in the US market and stabilized business in China. The company reported that orders worth 9.4 million NOK from Asia were shipped during Q2, with a solid order book for Q3.

The performance of Cystatin C over the past two years is illustrated in the following chart:

In contrast, fCAL turbo sales declined by 15% year-over-year to 12.8 million NOK, which the company attributed to stocking during previous quarters and order phasing. Gentian maintained its outlook for fCAL turbo for the full year 2025, expecting additional distribution agreements to contribute to sales during the second half.

Other products achieved their highest quarterly sales ever at 7.1 million NOK, representing 32% year-over-year growth. This category was driven by strong performance from fPELA turbo and cCRP products. Third-party products also posted record quarterly sales of 6.4 million NOK, up 38% from Q2 2024.

Operational Challenges

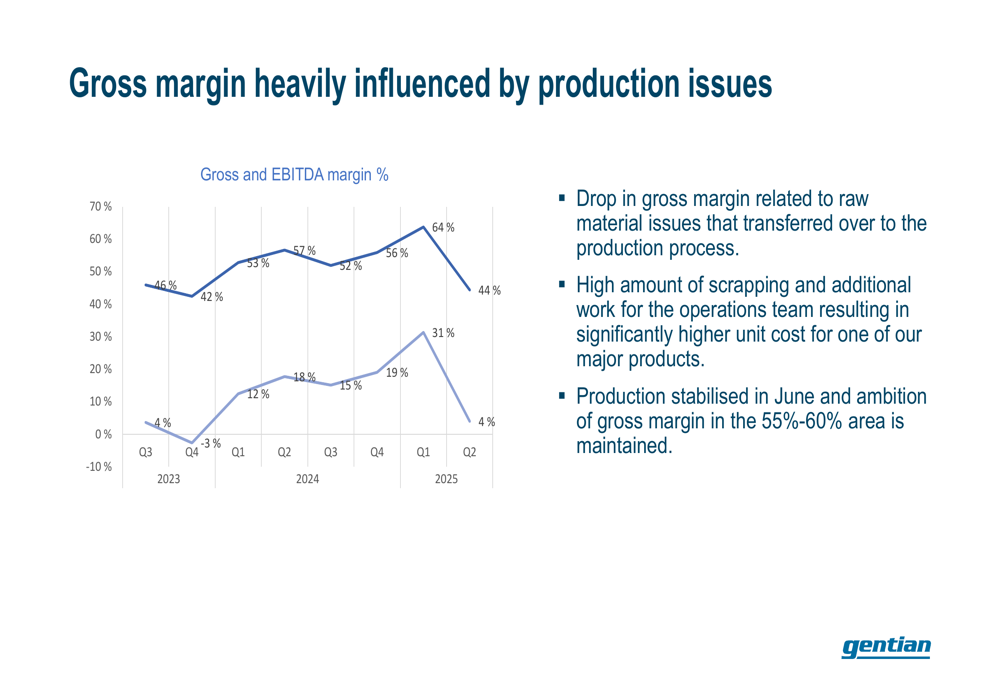

The significant decline in gross margin was the primary operational challenge in Q2. Gentian attributed this to raw material issues and increased scrapping, which elevated unit costs. The company indicated that production had stabilized in June and reaffirmed its ambition to achieve gross margins in the 55-60% range.

This margin pressure is clearly visible in the following chart:

Despite these challenges, Gentian maintained a solid cash position of 80.2 million NOK, compared to 81.0 million NOK in Q2 2024. The company’s equity ratio improved slightly to 85.4% from 84.2% a year earlier, and it continues to operate with no interest-bearing debt.

Strategic Initiatives

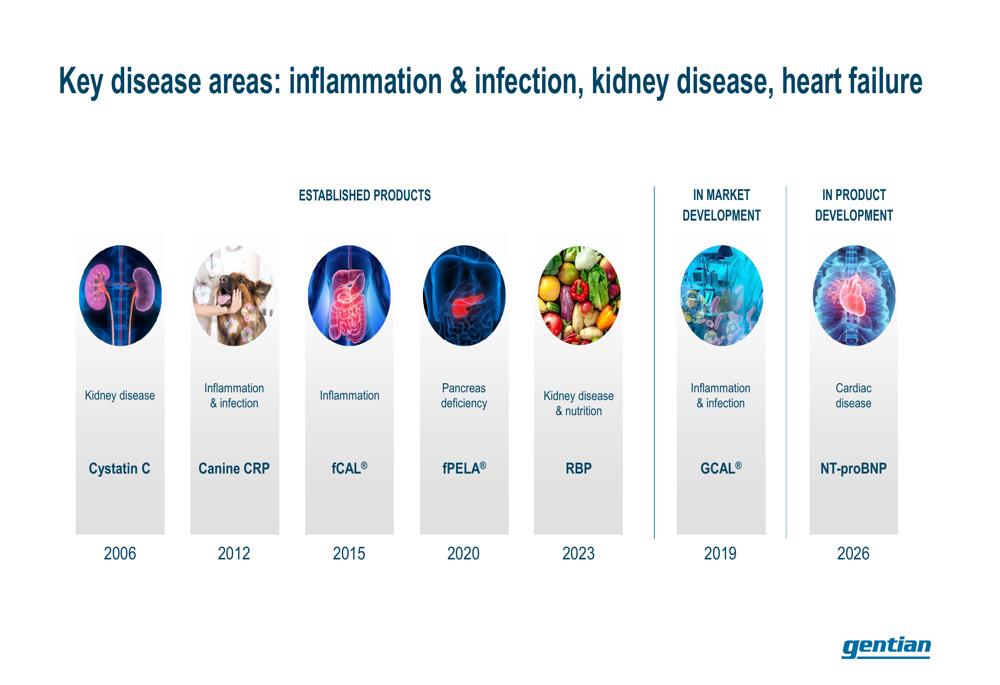

Gentian continues to make progress on its strategic initiatives, particularly the development of its NT-proBNP assay. The company reported that it is advancing toward the final validation phase for this product, having resolved some instrument alignment challenges and demonstrated long-term stability for key reagent and calibrator components.

The company remains on track to introduce NT-proBNP as a research-use-only product in the second half of 2025, with full commercial launch planned for 2026. This aligns with the company’s long-term growth strategy, which targets a serviceable market of $1.8 billion with annual growth of 5-10%.

Gentian’s overall strategy and key disease focus areas are illustrated in the following slide:

The company’s R&D activities also include an early-stage development project in partnership with a global IVD player, which is progressing toward the end of the proof-of-concept phase. Additionally, Gentian has begun exploring a next-generation technology platform and plans to make decisions on its next product development targets during the second half of 2025.

Forward-Looking Statements

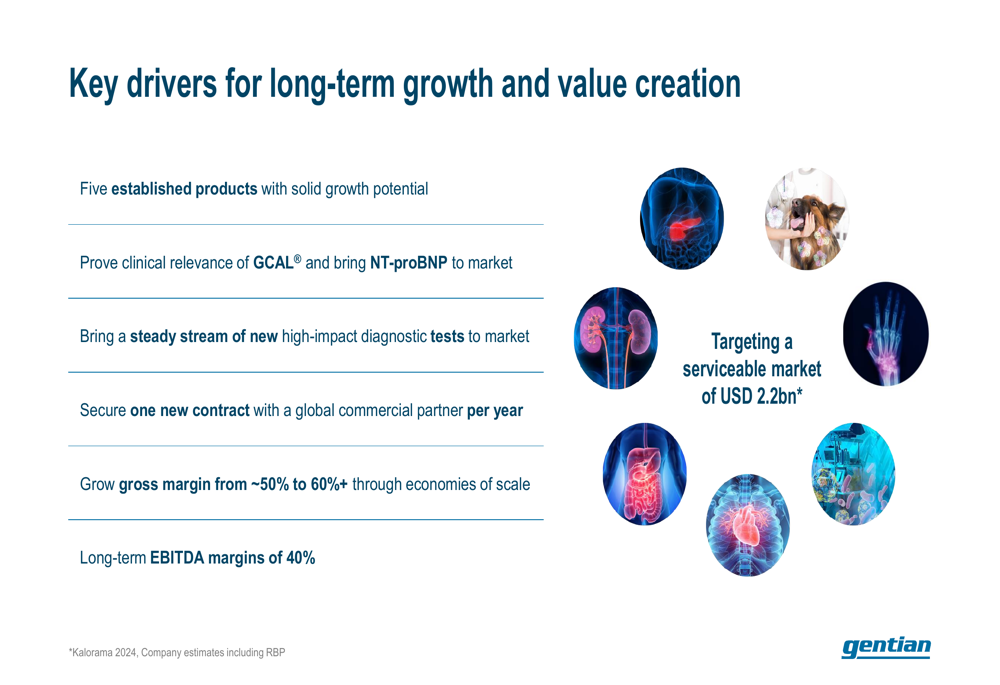

Looking ahead, Gentian outlined several key drivers for long-term growth and value creation:

The company aims to grow its gross margin from around 50% to over 60% through economies of scale and targets long-term EBITDA margins of 40%. These objectives are supported by Gentian’s partnerships with major industry players, including Siemens (ETR:SIEGn) Healthineers, Beckman Coulter, and Roche, which validate its go-to-market model.

While the Q2 results presented some challenges, particularly in gross margin, the company’s continued revenue growth and strategic progress suggest that its long-term trajectory remains intact. The stabilization of production issues in June provides a basis for potential margin improvement in the second half of 2025.

For investors, the key question will be whether Gentian can successfully navigate the transition from its strong Q1 performance to address the operational challenges that emerged in Q2, while maintaining its growth momentum in key markets like the US and Asia.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.