Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

Geox SpA (BIT:GEO) presented its first quarter 2025 financial results on May 13, 2025, highlighting the ongoing implementation of its business plan amid challenging market conditions. The Italian footwear and apparel company reported mixed results, with overall sales declining slightly while its web channel continued to demonstrate strong growth. The presentation emphasized Geox’s focus on strengthening its financial profile through improved working capital management and debt restructuring, even as it navigates persistent market volatility.

Executive Summary

Geox reported Q1 2025 net sales of €189.0 million, representing a 2.4% decrease compared to the same period last year (or -2.6% at constant exchange rates). This performance aligns with the company’s expectations as it continues to implement Phase One of its business plan, which includes geographic rationalization in markets like China and the USA.

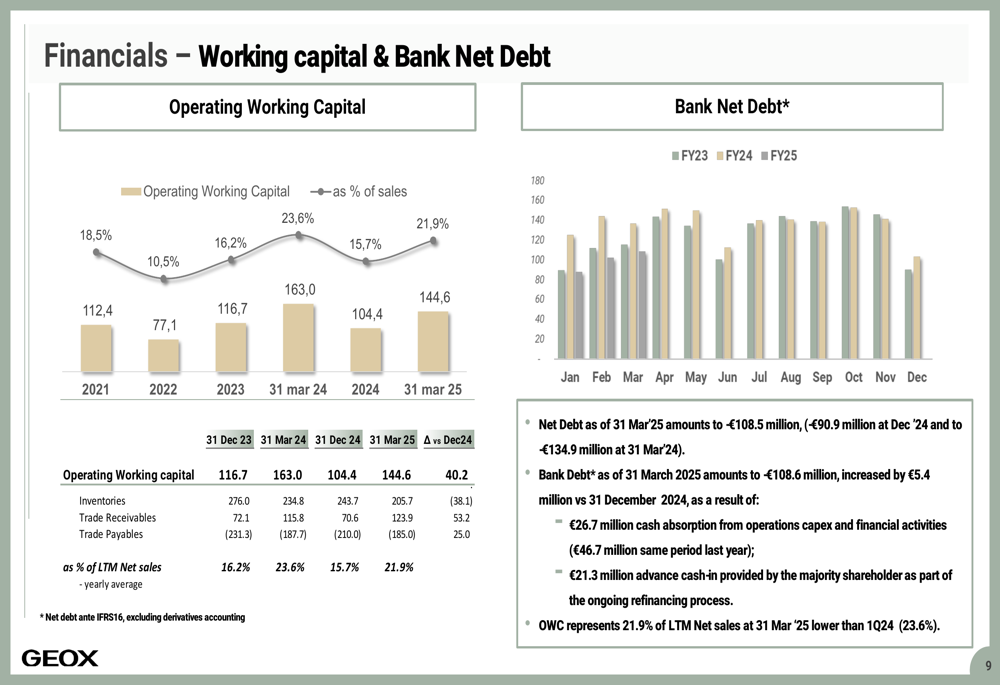

The company’s net financial position (pre-IFRS16) improved to -€108.5 million as of March 2025, compared to -€134.9 million in March 2024, reflecting enhanced working capital management. Bank debt stood at -€108.6 million, slightly higher than the -€103.2 million reported at the end of December 2024, but significantly better than the €136.8 million recorded in March 2024.

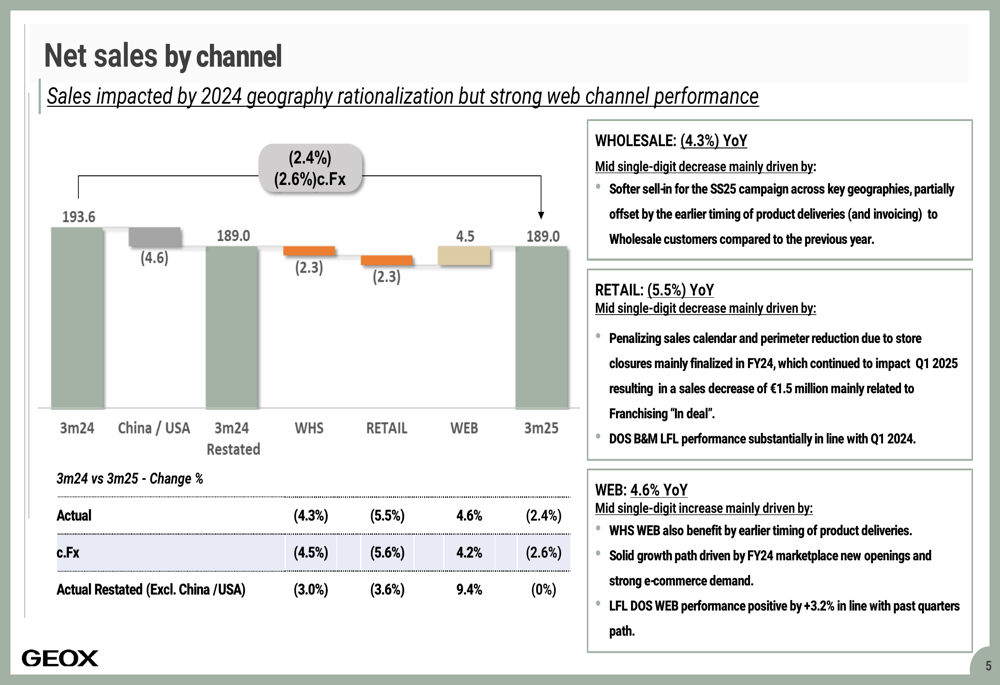

As shown in the following chart of sales performance by channel, Geox’s web segment was the only channel to deliver growth in Q1:

Quarterly Performance Highlights

Geox’s performance varied significantly across channels, regions, and product categories. The web channel emerged as the bright spot, growing 4.6% year-over-year, while traditional wholesale and retail channels declined by 4.3% and 5.5%, respectively. When excluding China and USA operations (which are undergoing rationalization), the web channel’s growth was even more impressive at 9.4%.

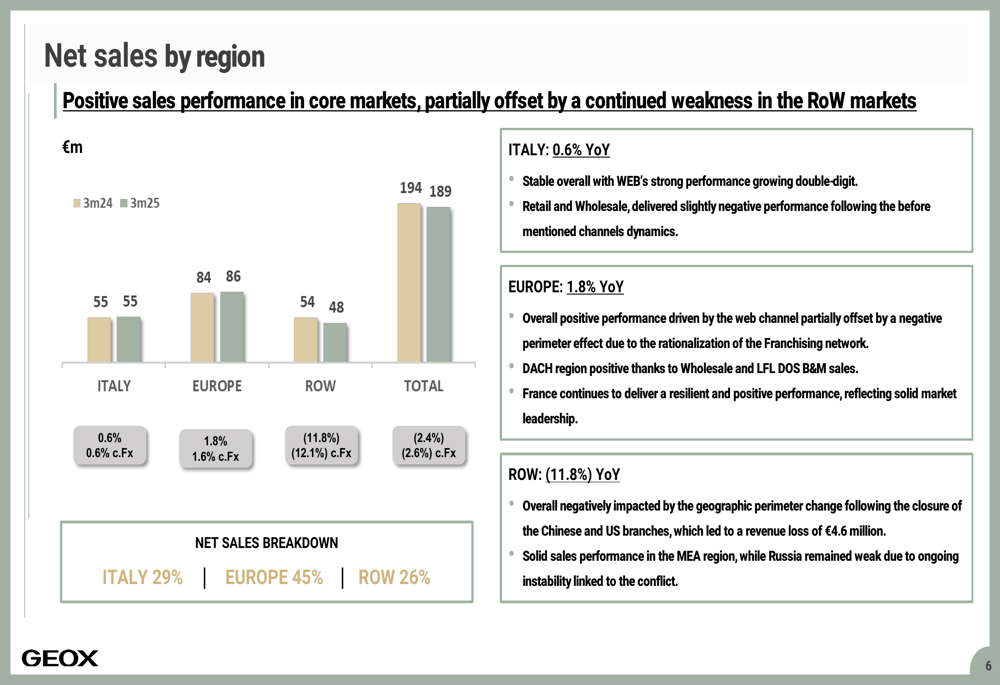

Regional performance showed divergence between core and peripheral markets. Italy remained stable with 0.6% growth, while Europe delivered a solid 1.8% increase, primarily driven by web channel performance. However, Rest of World markets declined by 11.8%, largely due to the company’s strategic geographic rationalization.

The following regional breakdown illustrates these performance differences:

In terms of product categories, footwear continues to dominate Geox’s sales mix, accounting for 90% of revenue. Footwear sales decreased by 1.9% compared to Q1 2024, while apparel experienced a more significant decline of 6.9%.

Detailed Financial Analysis

Geox’s working capital management showed improvement, with net working capital representing 21.9% of last twelve months’ net sales as of March 2025, down from 23.6% in March 2024. This improvement came despite the typical seasonal increase in working capital during the first quarter.

The company’s financial structure benefited from significant inventory reduction, with inventories decreasing by €38.1 million compared to December 2024. However, this was partially offset by a €53.2 million increase in trade receivables and a €25.0 million decrease in trade payables during the same period.

The following chart illustrates Geox’s working capital and bank net debt trends:

Cash flow dynamics showed improvement compared to the previous year. The company reported €26.7 million in cash absorption from operations, capital expenditures, and financial activities during Q1 2025, significantly better than the €46.7 million absorbed in the same period last year. Additionally, Geox received a €21.3 million advance cash infusion from its majority shareholder (LIR, which holds 71% of shares) as part of the ongoing refinancing process.

Strategic Initiatives

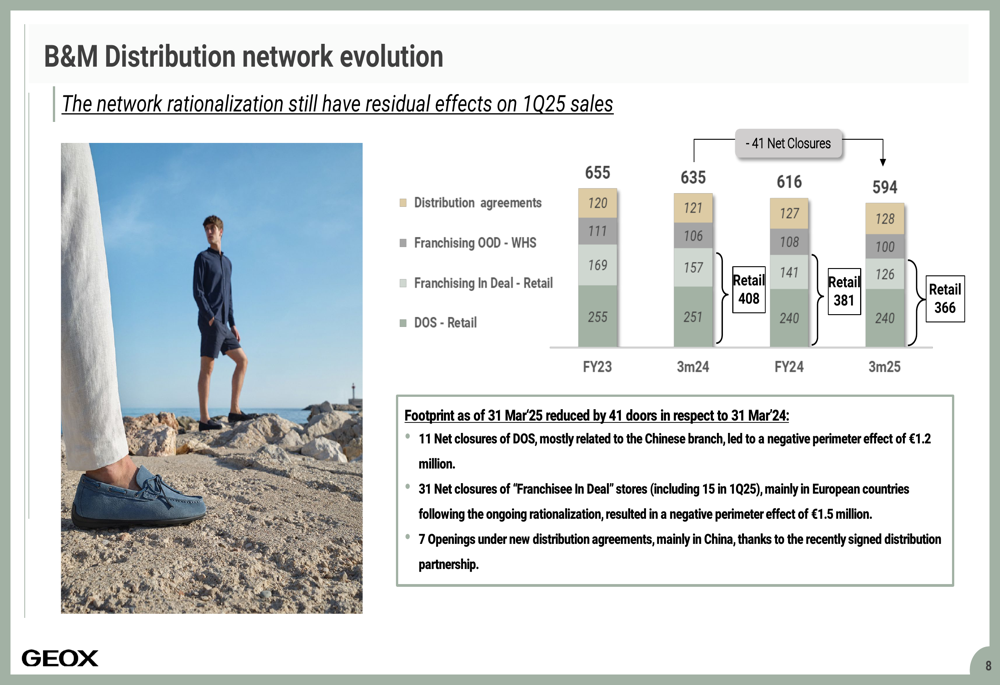

Geox continued its distribution network optimization strategy, reducing its brick-and-mortar footprint by 41 doors compared to March 2024. This included 11 net closures of directly operated stores (DOS), primarily related to the Chinese branch, and 31 net closures of "Franchisee In Deal" stores, mainly in European countries. These closures resulted in a negative perimeter effect of €2.7 million on sales.

The company’s distribution network evolution is detailed in the following chart:

Simultaneously, Geox opened seven new locations under distribution agreements, primarily in China, leveraging a recently signed distribution partnership. This strategic shift reflects the company’s focus on more capital-efficient growth models while maintaining market presence.

Forward-Looking Statements

Despite the persistent uncertainty in the international environment, Geox substantially confirmed its consolidated 2025 guidance as outlined in its recently approved Industrial Plan. The company prudently anticipates a slightly lower than expected sales figure, though it characterized this deviation as "not material." Profitability expectations remain unchanged, with the Group’s plan forecasting a modest year-on-year decline in both sales and margins for full-year 2025.

Current trading indicators show mixed signals. Forward season (FW25) in-season reorders are in line with the previous year, while retail (DOS B&M) performance through week 19 of 2025 is slightly positive year-to-date compared to the previous year. The web channel is expected to continue delivering positive performance throughout 2025.

The company’s outlook acknowledges ongoing challenges:

Geox emphasized that all forward-looking statements remain subject to the instability of the current geopolitical, economic, and inflationary environment, highlighting the cautious approach management is taking toward forecasting in uncertain market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.