S&P 500 jumps as tech rallies as investors eye end of government shutdown

Introduction & Market Context

Gestamp Automocion SA (BME:GEST) released its third-quarter and nine-month 2025 results on November 4, showing improved profitability despite a significant revenue decline. Following the earnings announcement, Gestamp’s stock fell 1.43% to close at €3.31, reflecting investor concerns over top-line performance despite margin improvements.

The Spanish auto parts manufacturer faced challenging market conditions, with global auto production growing 4.3% year-over-year while Gestamp’s revenue underperformed the market by 1.3 percentage points. The company’s results highlight its focus on operational efficiency and balance sheet strength amid uneven regional performance and significant currency headwinds.

Quarterly Performance Highlights

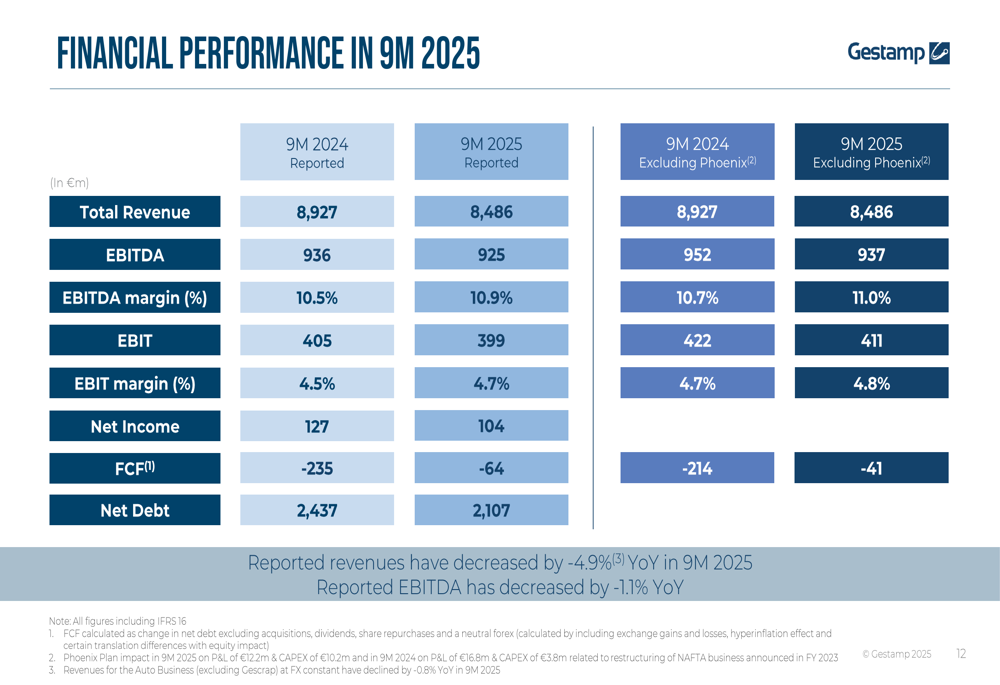

Gestamp reported revenue of €8.486 billion for the first nine months of 2025, representing a 4.9% decrease compared to the same period in 2024. Despite this revenue decline, the company improved its EBITDA margin to 11.0%, up 38 basis points year-over-year, demonstrating operational resilience in challenging conditions.

As shown in the following financial performance overview:

Net income fell 18% year-over-year to €104 million, while free cash flow improved significantly to -€64 million from -€235 million in the same period last year. The company maintained its focus on deleveraging, with net debt decreasing to €2.107 billion and a leverage ratio of 1.6x Net Debt to EBITDA, down from 1.9x in the comparable period.

Revenue Challenges

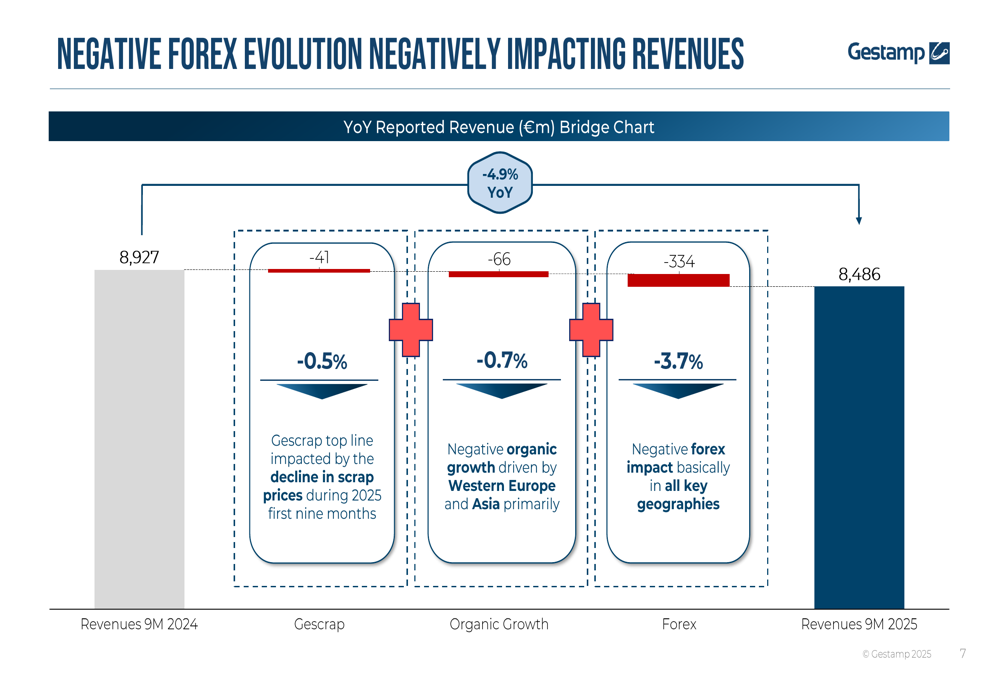

The primary driver behind Gestamp’s revenue decline was a substantial negative impact from foreign exchange movements, which reduced revenue by €334 million or 3.7%. Organic growth also declined by 0.7%, while the company’s Gescrap recycling business contributed a 0.5% negative impact due to falling scrap prices.

This revenue bridge clearly illustrates these impacts:

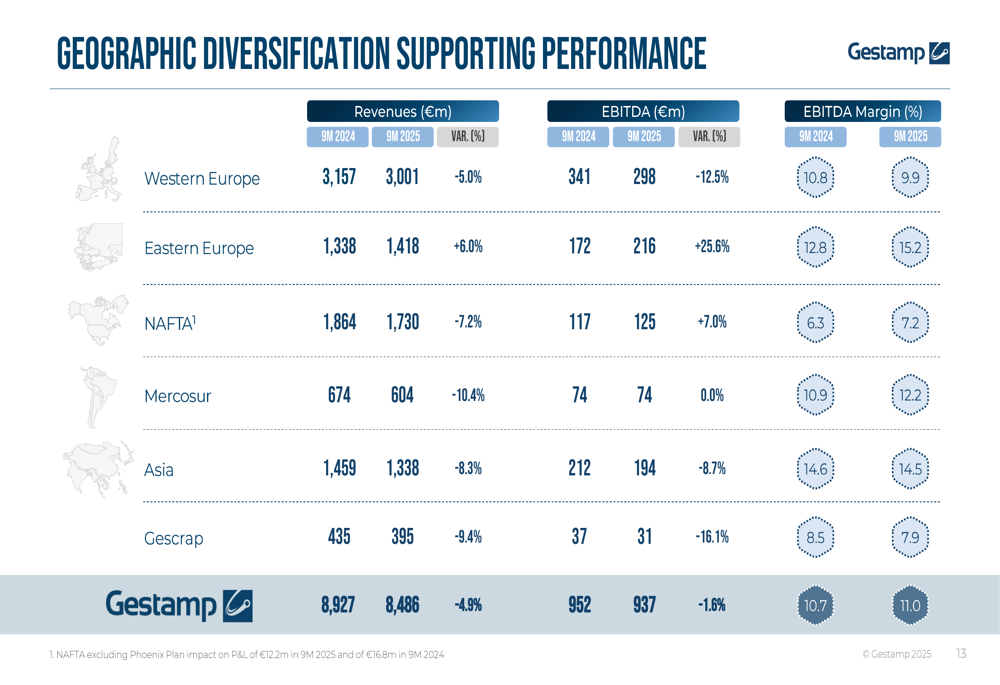

Regional performance varied significantly, with Eastern Europe showing strong growth (+6.0% revenue, +25.6% EBITDA) while other regions experienced declines. Western Europe revenue fell 5.0%, NAFTA declined 7.2%, Mercosur dropped 10.4%, and Asia decreased 8.3%. This geographic diversification provided some buffer against market volatility:

Profitability Resilience

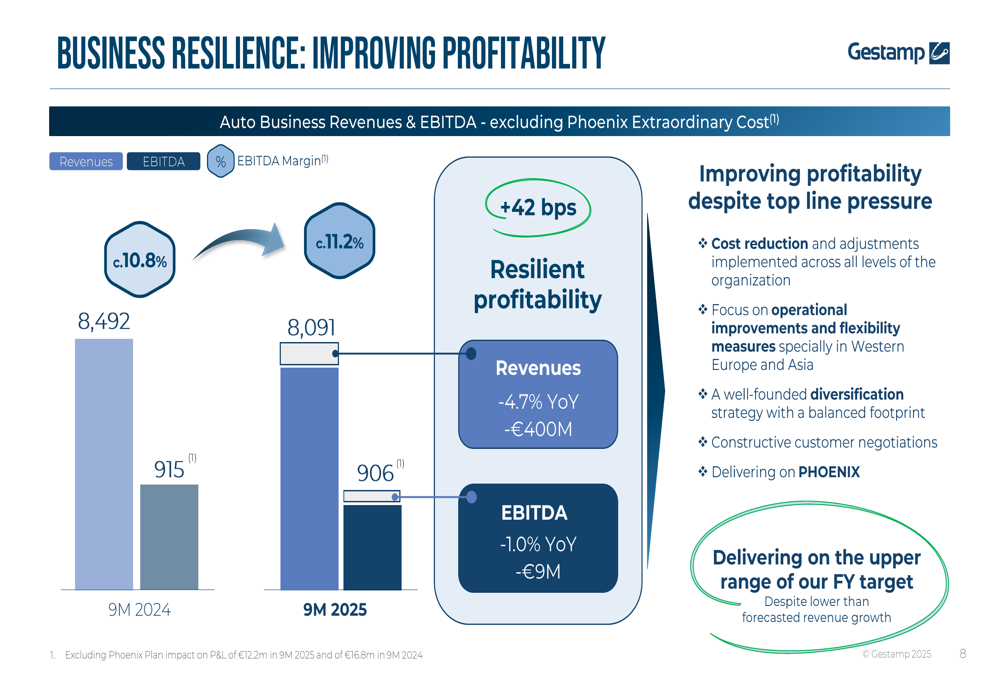

Despite revenue challenges, Gestamp demonstrated resilience in its core business profitability. The company’s auto business EBITDA margin improved by 42 basis points to 11.2%, reflecting successful cost reduction measures and operational improvements.

The following chart illustrates this profitability improvement despite revenue pressure:

During the earnings call, Executive Chairman Francisco Riberas emphasized, "We are focused on profitability and to preserve our financial health," underscoring the company’s strategic shift toward margin protection over growth in the current market environment.

Phoenix Plan Progress

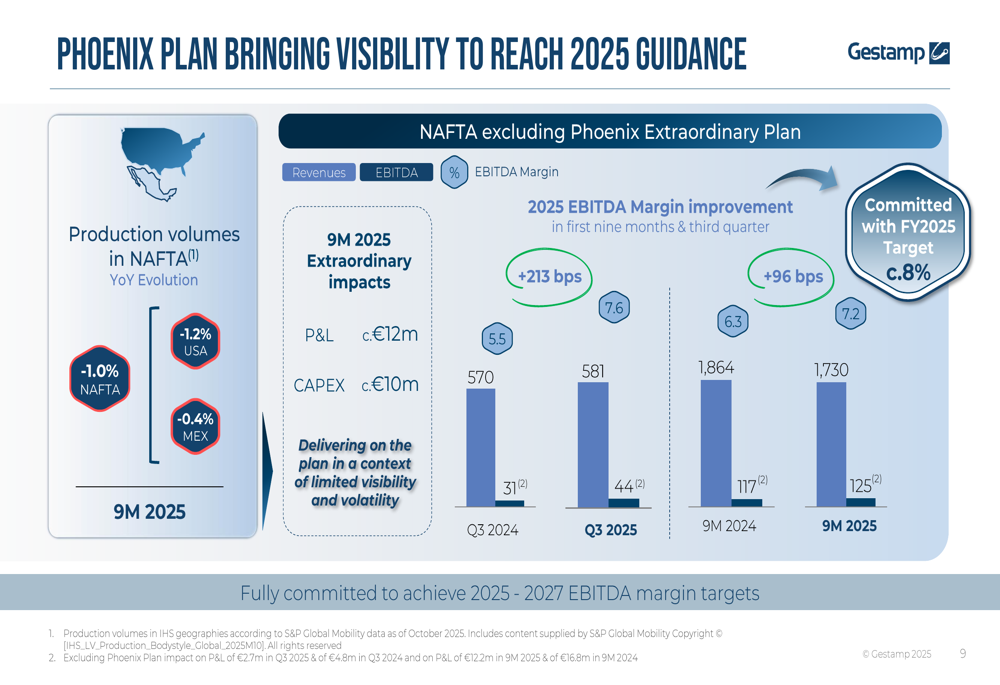

A key highlight of Gestamp’s presentation was the progress of its Phoenix plan in the NAFTA region, where the company achieved an EBITDA margin of 7.2% for the first nine months of 2025, representing a 96 basis point improvement year-over-year. The third quarter showed even stronger improvement, with EBITDA margin reaching 7.6%, up 213 basis points from Q3 2024.

The Phoenix plan’s impact on NAFTA profitability is clearly demonstrated in this chart:

The company remains committed to achieving its target of 8% EBITDA margin in NAFTA for 2025 and double-digit margins by the end of 2026, despite challenging production volumes in the region (USA:-1.2%, Mexico: -0.4%).

Balance Sheet Strength

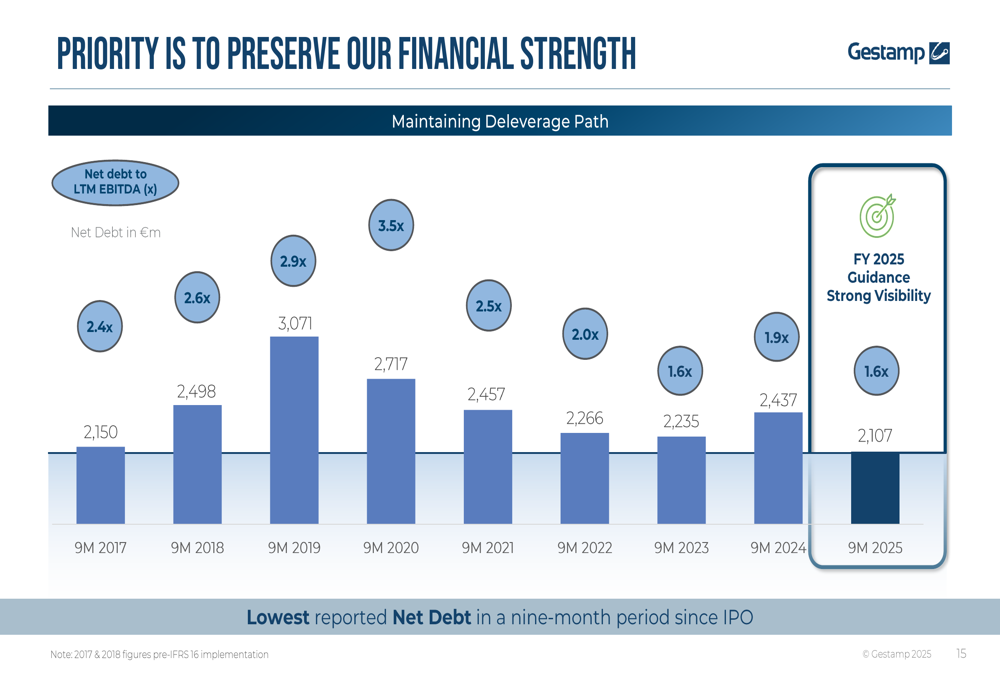

Gestamp continued its focus on financial strength and deleveraging, achieving its lowest reported net debt in a nine-month period since its IPO. The company’s leverage ratio improved to 1.6x, down from 1.9x in the comparable period last year, reflecting disciplined balance sheet management.

This chart shows Gestamp’s consistent deleveraging trend:

To further enhance financial flexibility, Gestamp issued €500 million in senior secured bonds maturing in 2030 with a 4.375% coupon and executed a partial real estate sale and leaseback agreement for assets in Spain valued at €246 million. These actions have provided the company with a more balanced debt maturity profile and additional liquidity.

Forward-Looking Statements

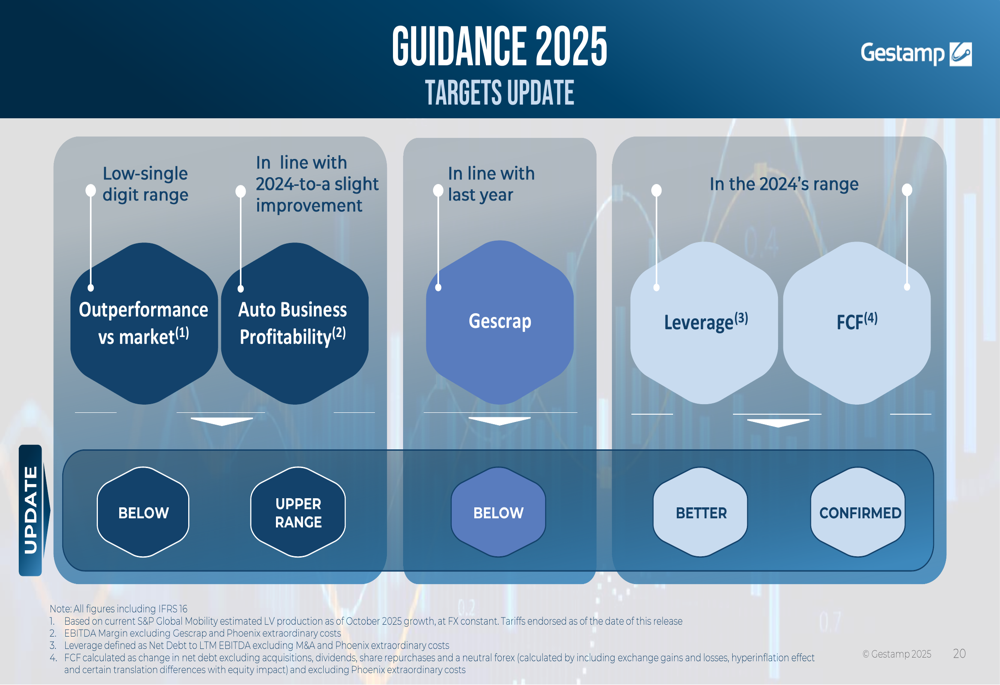

Gestamp updated its 2025 guidance, maintaining a cautious outlook while emphasizing profitability and balance sheet strength. The company expects to underperform the market in revenue growth but aims to achieve the upper range of its auto business profitability targets. Leverage is projected to be better than initially guided, while free cash flow targets are confirmed.

The company’s updated guidance is summarized in this overview:

Looking ahead, Gestamp anticipates a steady recovery in 2025 despite complex macroeconomic conditions. The company has revised its volume forecast upward to 1.90 million vehicles (+2.0% year-over-year), primarily due to stronger performance in Asia, while Western Europe (-3.6%) and NAFTA (-2.0%) are expected to remain challenging.

During the earnings call, Riberas noted, "We see a good trend. We have a very good position with [Chinese OEMs]," highlighting the company’s strategic positioning with emerging automakers despite current regional challenges.

Gestamp continues to face risks from forex fluctuations, regional underperformance, potential steel tariffs, and broader macroeconomic pressures, but its focus on profitability and balance sheet strength positions the company to navigate these challenges while maintaining financial health.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.