Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Executive Summary

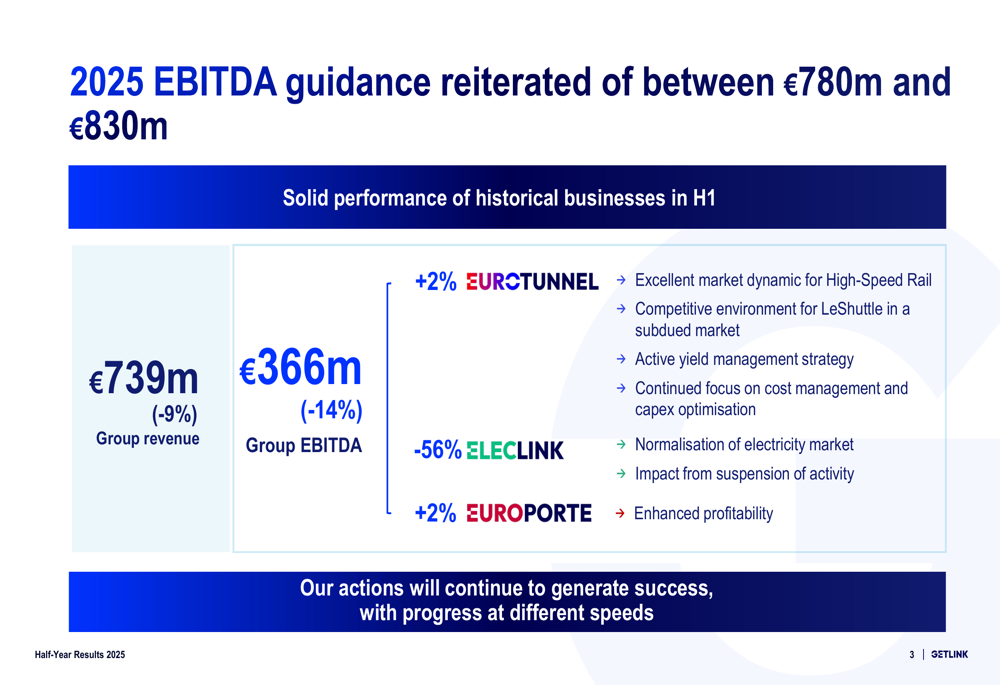

Getlink SE (ENXTPA:GET) presented its half-year 2025 results on July 24, showing mixed performance across its business units. The company reported a 9% decline in group revenue to €739 million and a 14% drop in EBITDA to €366 million, primarily due to the normalization of electricity markets affecting its Eleclink business. Despite these challenges, Getlink maintained its full-year EBITDA guidance of €780-830 million, highlighting resilience in its core Eurotunnel operations.

As shown in the following financial highlights chart, the performance varied significantly across business segments:

Quarterly Performance Highlights

Getlink's performance was characterized by contrasting results across its three main business units. Eurotunnel, the company's core business, showed modest growth with a 2% increase in EBITDA to €298 million. This was supported by strong passenger services and high-speed rail traffic. Meanwhile, Eleclink experienced a significant 56% decline in EBITDA due to electricity market normalization and operational suspensions. Europorte maintained stable performance with a 2% EBITDA increase.

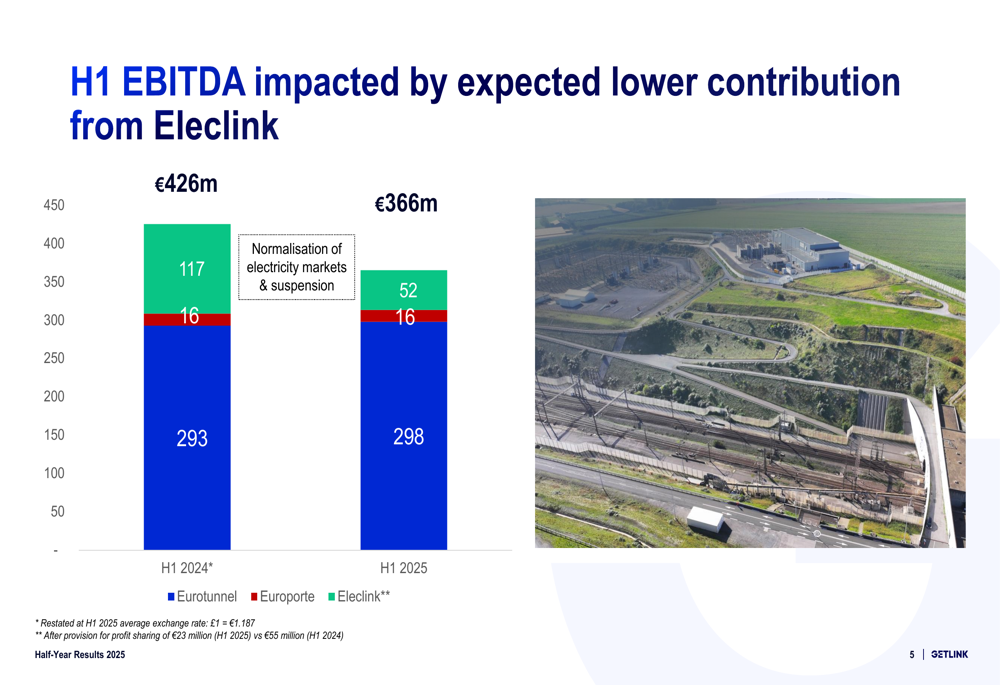

The EBITDA bridge below clearly illustrates how Eleclink's decline offset the gains from other business units:

Eurotunnel's traffic statistics demonstrated resilience in a challenging market environment. LeShuttle Passenger services carried 985,847 vehicles, up 2% year-over-year, while maintaining a dominant market share of 59.9% (+60 basis points). LeShuttle Freight transported 591,746 trucks, representing a 2% decline but with an improved market share of 35.7% (+30 basis points). The company's yield management strategy proved effective, with average shuttle yield increasing by 3%.

The following chart details these traffic and market share metrics:

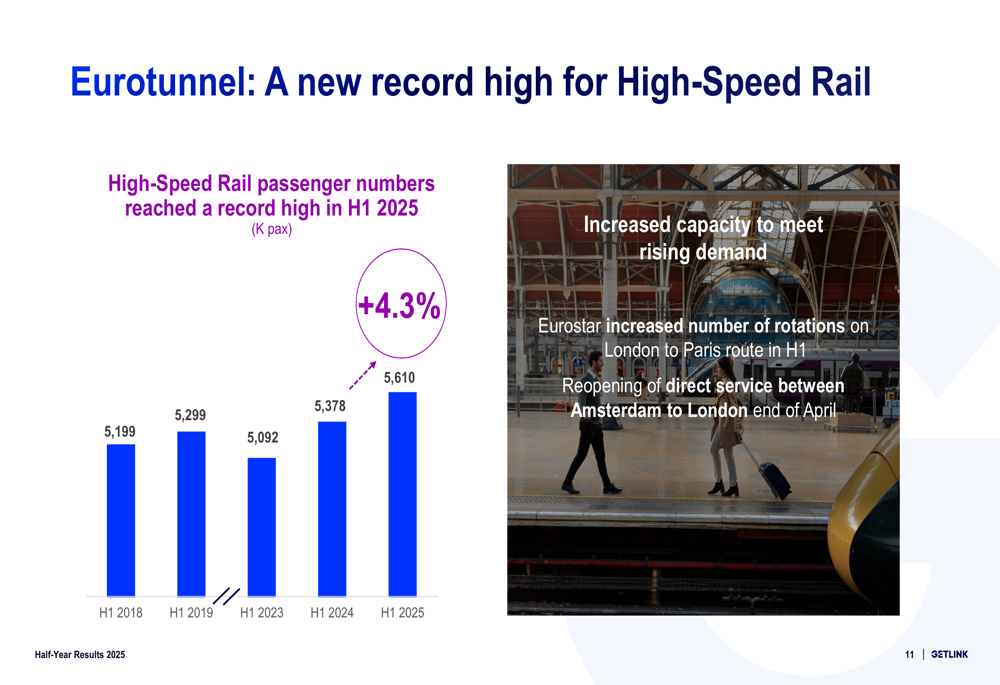

High-speed rail services through the Channel Tunnel achieved record passenger numbers in H1 2025, reaching 5.61 million passengers, a 4.3% increase compared to H1 2024. This growth was supported by increased capacity, including more Eurostar rotations on the London-Paris route and the reopening of direct service between Amsterdam and London in late April.

The following graph illustrates the strong growth trend in high-speed rail passenger numbers:

Detailed Financial Analysis

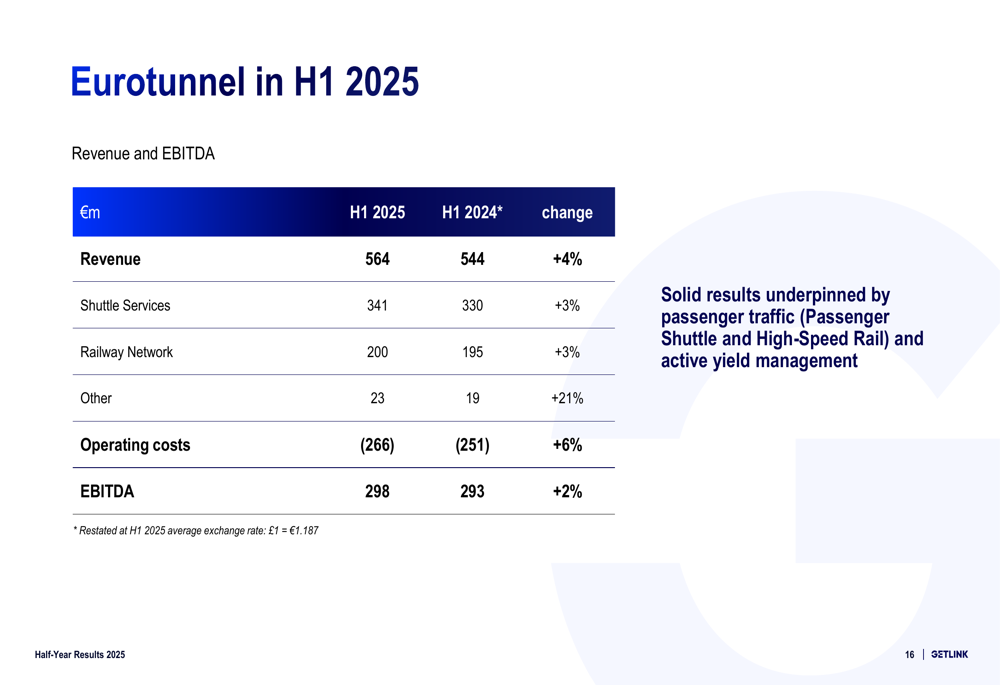

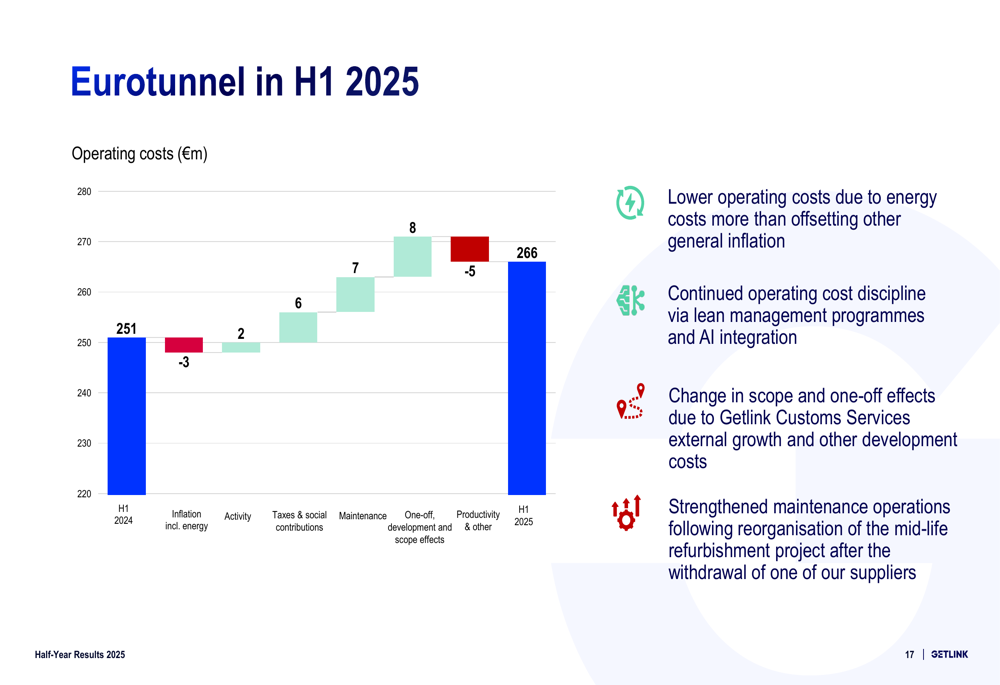

Eurotunnel, Getlink's largest business unit, reported revenue of €564 million, up 4% from the previous year. This growth was driven by a 3% increase in shuttle services revenue (€341 million) and a 3% increase in railway network revenue (€200 million). Despite a 6% increase in operating costs to €266 million, EBITDA improved by 2% to €298 million, underscoring the strength of passenger shuttle and high-speed rail services.

The financial breakdown for Eurotunnel is shown below:

Eurotunnel's operating costs increased by €15 million compared to H1 2024, with the main drivers being taxes (+€6 million) and maintenance (+€7 million). These increases were partially offset by productivity improvements and lower energy costs, as illustrated in the following cost bridge:

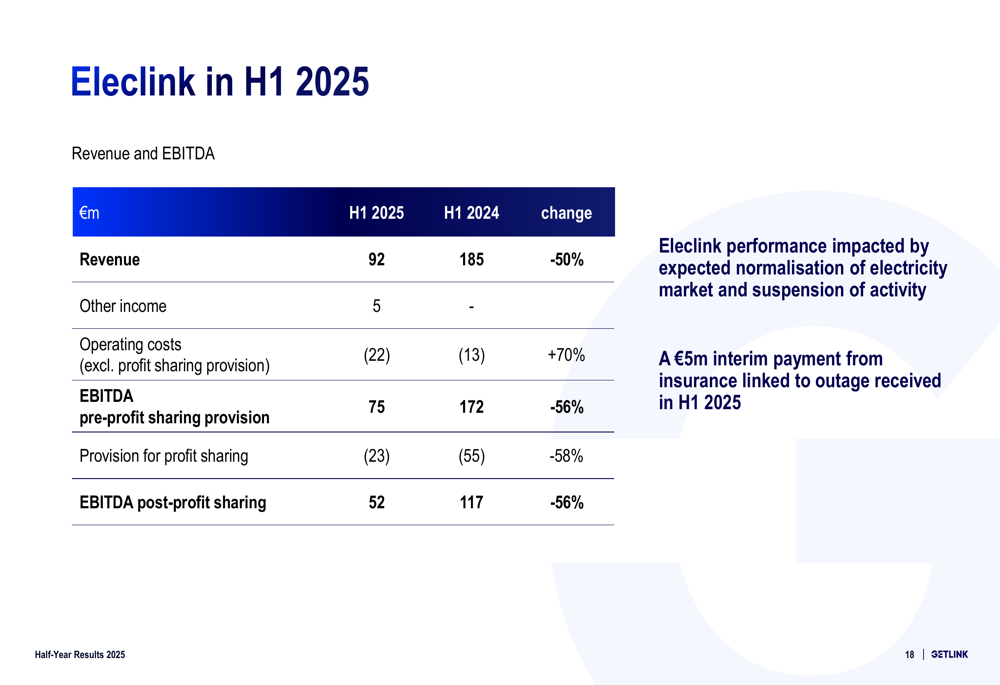

Eleclink, which had been a significant contributor to group profits in previous periods, saw its revenue halve to €92 million in H1 2025. EBITDA after profit-sharing provisions fell to €52 million, heavily impacted by the normalization of electricity market conditions and operational suspensions. The company did receive a €5 million interim insurance payment related to the outages.

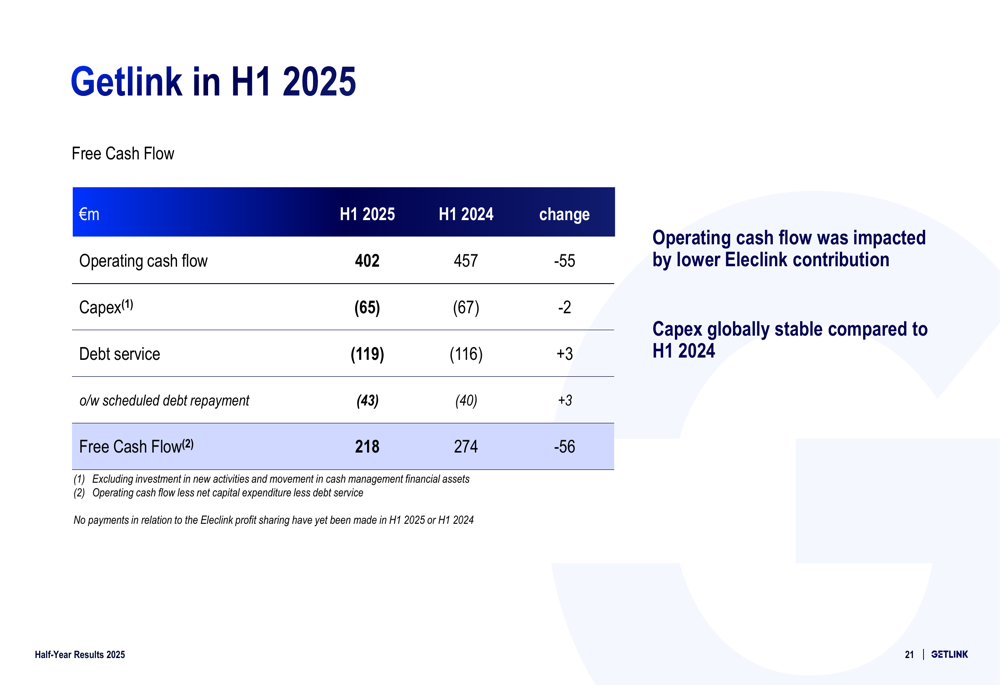

At the consolidated level, Getlink reported a net profit of €113 million, down 35% from the previous year. Free cash flow decreased to €218 million from €274 million, primarily due to Eleclink's lower contribution. The company maintained a strong cash position of €1,355 million and successfully issued €600 million in Green Bonds during the period.

Strategic Initiatives

Getlink highlighted several strategic initiatives aimed at enhancing operational efficiency and customer experience. The company implemented an optimized pricing structure for Eurotunnel with Standard, Standard Plus, and Flexiplus options to support its yield management strategy. This approach has contributed to improved customer satisfaction, with Net Promoter Scores increasing for both freight (62 vs. 52) and passenger (48 vs. 40) services compared to the previous year.

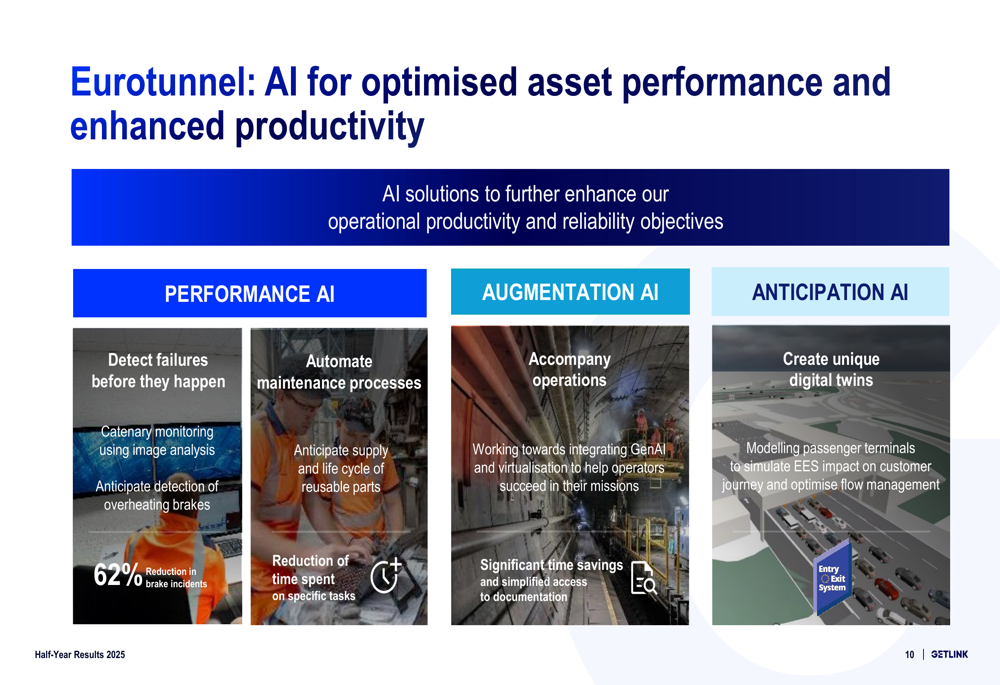

The company invested €60 million in H1 2025 as part of its lifecycle and attractivity reinforcement program. A notable innovation is the application of artificial intelligence to optimize asset performance, which has led to a 62% reduction in brake incidents through image analysis and improved maintenance productivity.

The following slide illustrates how AI is being leveraged across operations:

Forward-Looking Statements

Despite the challenges in H1, Getlink maintained its full-year 2025 EBITDA guidance of €780-830 million. The company expects continued growth in Eurotunnel, with implementation of Entry/Exit System (EES) formalities from October potentially impacting operations. For Eleclink, the outlook remains cautiously optimistic with UK-France electricity spreads remaining attractive and 46% of 2025 capacity already sold.

Looking further ahead, Getlink identified significant growth potential in railway expansion, with new operators like Trenitalia and Evolyn potentially entering the market. The company estimates potential new revenue of approximately €8.5 million from expansion to new destinations, based on airline market estimates.

Getlink also emphasized its ESG leadership position, noting that while ferry operators are charging additional costs to customers due to EU carbon regulations (€6-8 per ticket in 2025), the company is well-positioned with its lower-emission transport alternatives. This advantage could become more pronounced as carbon costs for ferries are expected to increase further in 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.