Intellia presents positive data for hereditary angioedema treatment

Gibraltar Industries (NASDAQ:ROCK) reported strong second-quarter 2025 results during its earnings call on August 6, showcasing the success of its portfolio simplification strategy despite challenging market conditions in some segments. The company delivered double-digit growth in both revenue and earnings per share while maintaining a robust order backlog.

Quarterly Performance Highlights

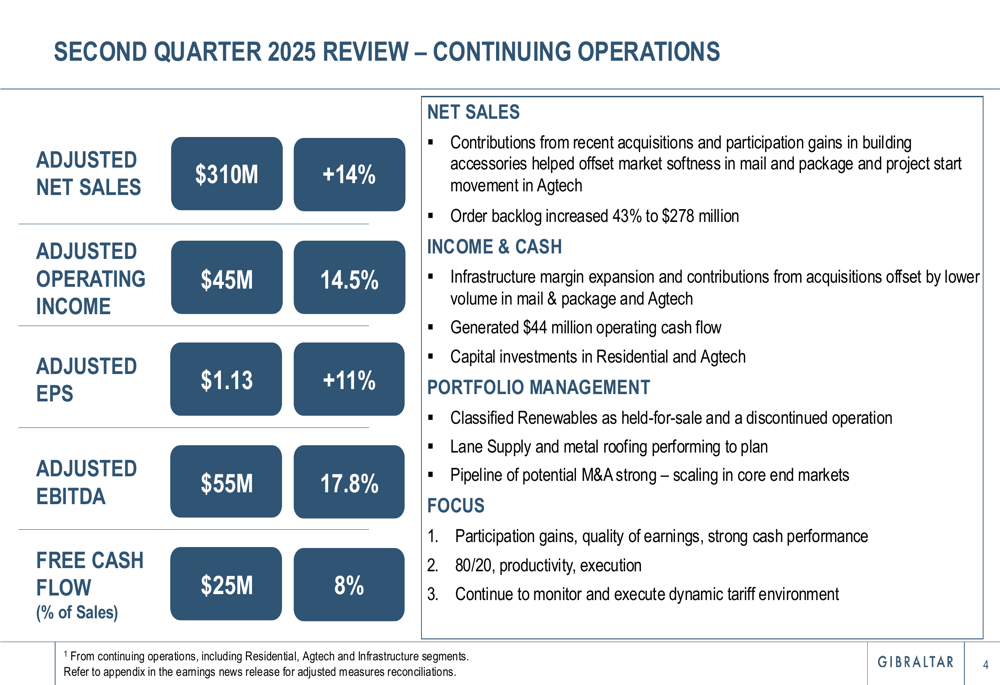

Gibraltar reported adjusted net sales of $310 million in Q2 2025, representing a 14% increase year-over-year. Adjusted operating income reached $45 million with a margin of 14.5%, while adjusted earnings per share grew 11% to $1.13. The company’s adjusted EBITDA increased to $55 million with a margin of 17.8%.

As shown in the following chart of Gibraltar’s Q2 2025 performance metrics:

Particularly noteworthy was the 43% increase in order backlog to $278 million, indicating strong future revenue potential. This growth comes despite headwinds in the residential construction market, demonstrating Gibraltar’s ability to gain market share in challenging conditions.

Portfolio Simplification Strategy

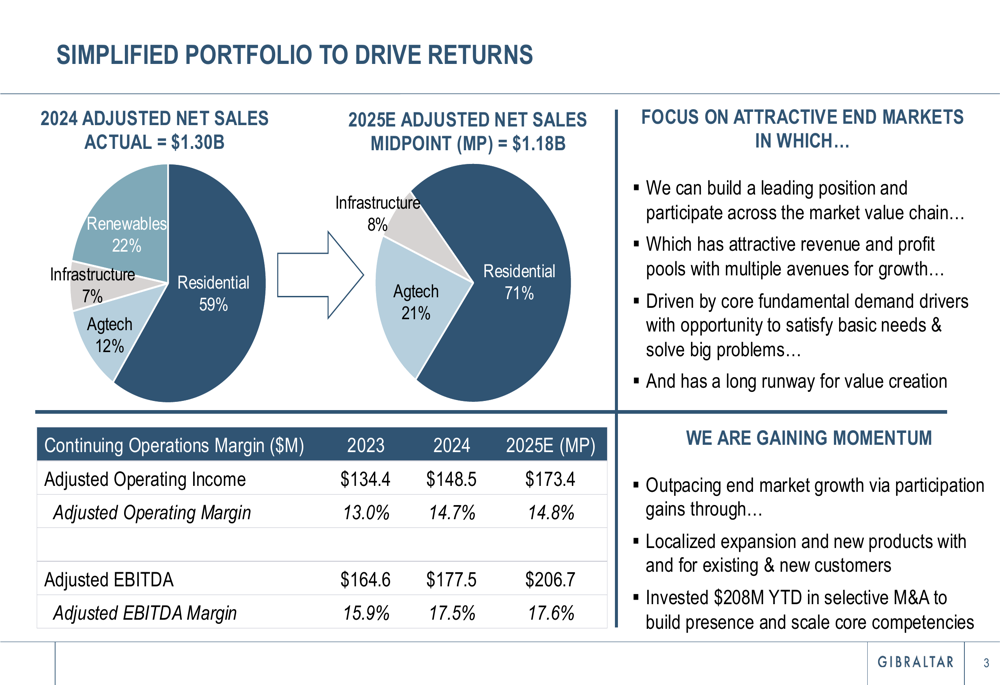

Gibraltar’s strategic realignment toward higher-margin businesses appears to be yielding positive results. The company has simplified its portfolio to focus primarily on Residential and Agtech segments while divesting its Infrastructure and Renewables operations.

The following chart illustrates Gibraltar’s portfolio transformation and improving profitability metrics:

This strategic shift has contributed to improving profitability metrics, with adjusted operating income projected to reach $173.4 million in 2025, up from $148.5 million in 2024 and $134.4 million in 2023. Similarly, adjusted EBITDA is expected to grow to $206.7 million in 2025 from $177.5 million in 2024.

Segment Analysis

Residential Segment

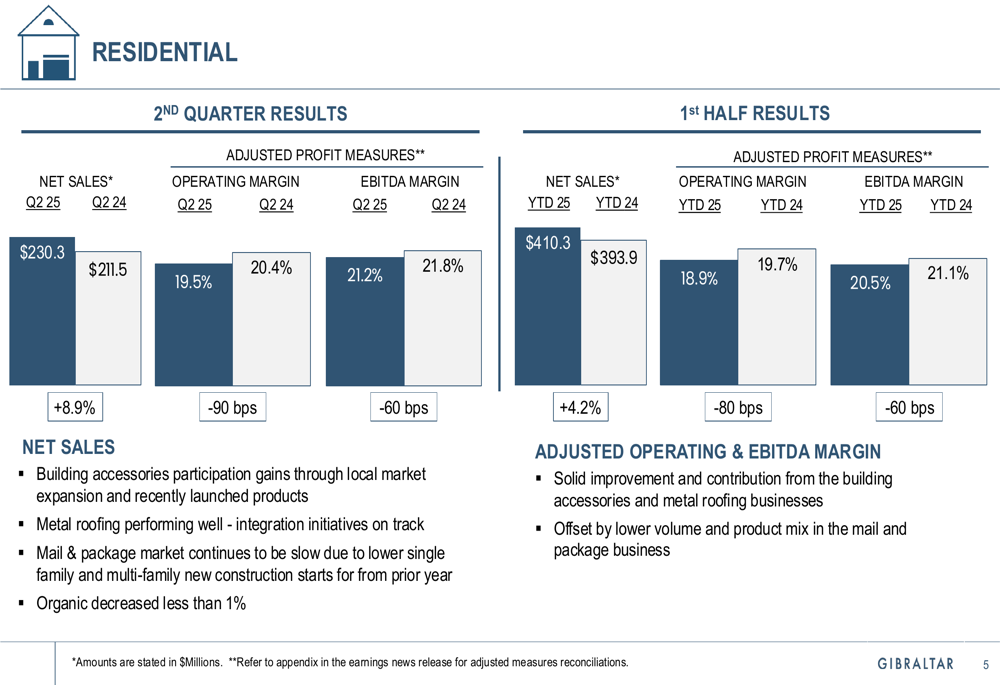

The Residential segment, Gibraltar’s largest business unit, delivered net sales of $230.3 million in Q2 2025, an 8.9% increase from the prior year. However, adjusted operating margin decreased slightly to 19.5% from 20.4% in Q2 2024.

The segment’s performance is illustrated in the following chart:

Despite challenging market conditions, including affordability issues and high interest rates impacting demand, Gibraltar achieved solid growth in this segment. The company noted that retailer point-of-sale results were down 5-6%, and ARMA shingle shipments declined 4.3% in Q2, suggesting Gibraltar is outperforming the broader market.

The company continues to expand its residential footprint, adding new locations including Oklahoma City, with plans for 3-4 more locations in the second half of 2025.

Agtech Segment

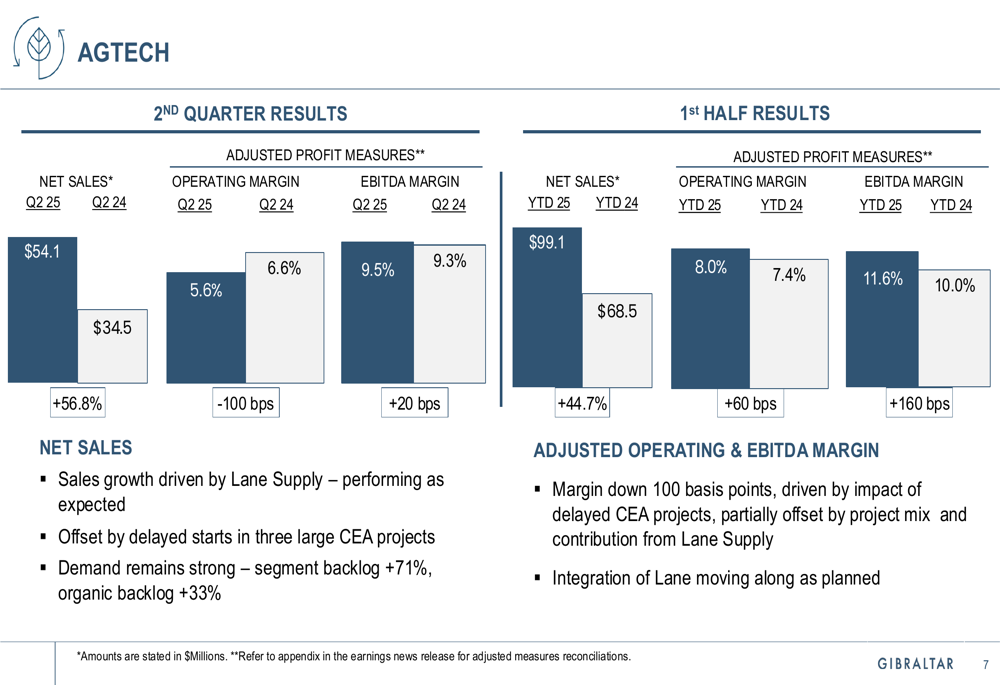

The Agtech segment delivered exceptional growth, with Q2 2025 net sales of $54.1 million, a 56.8% increase from $34.5 million in Q2 2024. Operating margin was 5.6%, and EBITDA margin reached 9.5%.

The following chart details the Agtech segment’s performance:

Growth was primarily driven by the Lane Supply acquisition, though the company noted some project delays. Despite these delays, the segment’s backlog increased by 71%, indicating strong future revenue potential.

Gibraltar highlighted several significant Agtech projects, including a $90 million major retrofit for Houwelings and two Pomas Farms projects totaling $13.6 million. The company is also expanding into institutional and commercial segments with projects like the Lewis-Ginter Botanical Garden Conservatory Expansion.

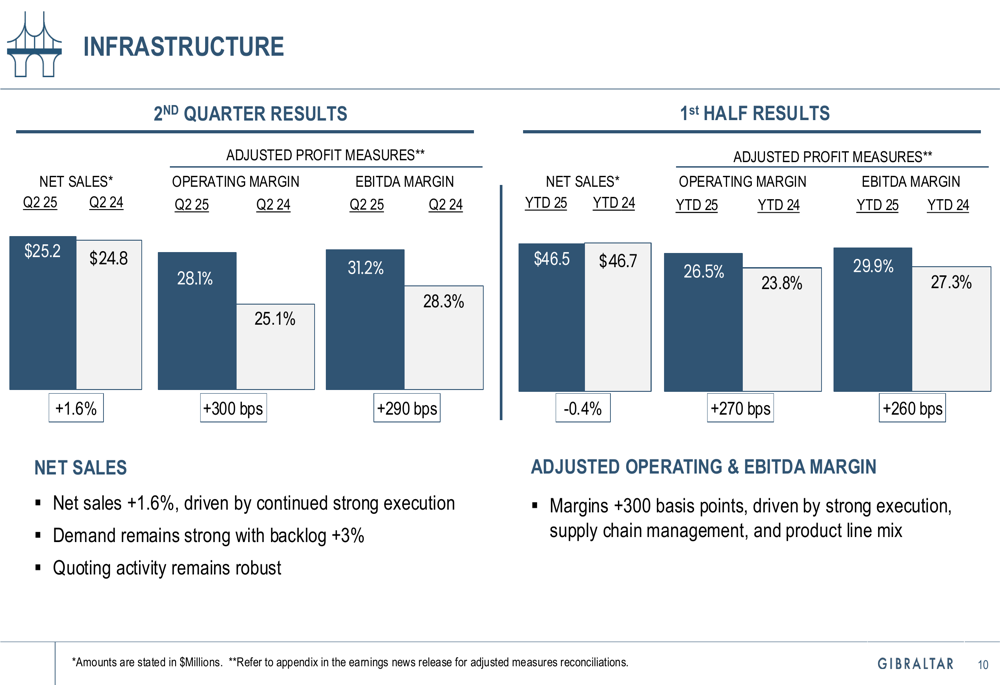

Infrastructure Segment

The Infrastructure segment, though a smaller portion of Gibraltar’s portfolio, delivered solid results with Q2 2025 net sales of $25.2 million, a 1.6% increase from Q2 2024. The segment achieved impressive profitability with an operating margin of 28.1% and EBITDA margin of 31.2%.

The segment’s performance is shown in the following chart:

The company noted that demand remains strong in this segment, with backlog increasing by 3%.

Financial Position & Outlook

Gibraltar maintains a strong balance sheet with ample liquidity and solid free cash flow. In Q2 2025, the company generated operating cash flow of $44 million and free cash flow of $25 million. Management expects 2025 free cash flow to be approximately 10% of net sales.

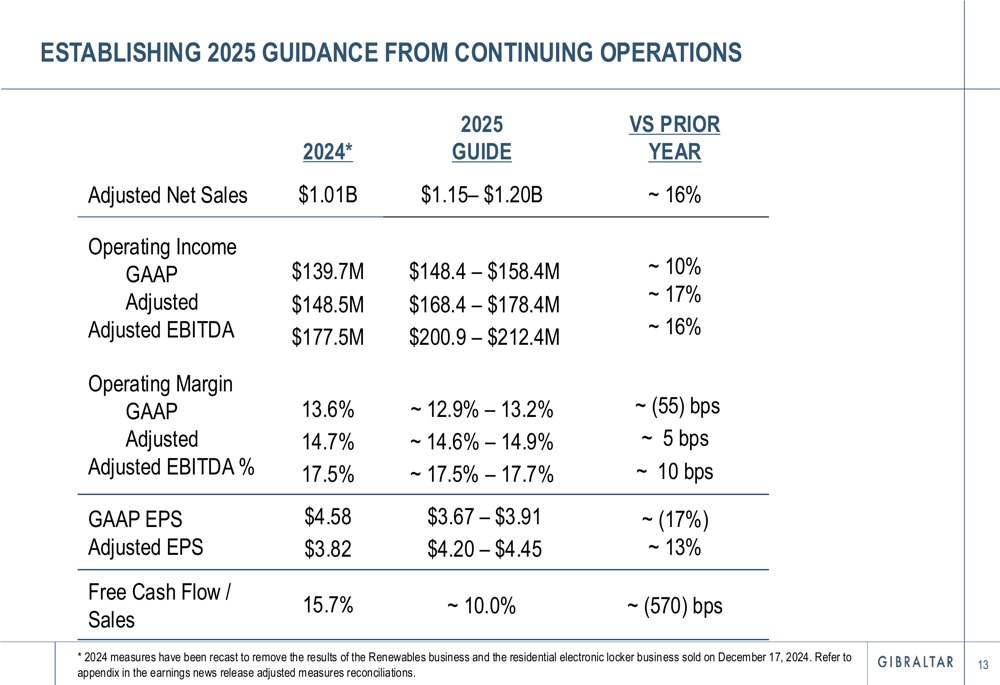

For the full year 2025, Gibraltar established guidance for continuing operations with adjusted net sales projected between $1.15 billion and $1.20 billion, representing approximately 16% growth versus the prior year. Adjusted operating income is expected to range from $168.4 million to $178.4 million, with adjusted EPS of $4.20 to $4.45.

The company’s 2025 guidance is detailed in the following table:

Management highlighted three key drivers supporting this guidance: current demand trends, successful integration of acquisitions (Lane Supply and metal roofing), and effective tariff mitigation through the company’s established playbook.

Gibraltar’s stock closed at $64.42 on August 5, 2025, virtually unchanged from the previous day. The company’s shares have traded between $48.96 and $74.97 over the past 52 weeks, suggesting potential upside if the company continues to execute on its strategic initiatives and deliver on its 2025 guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.