Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

GigaCloud Technology Inc (NASDAQ:GCT), an online global B2B solutions provider for large parcel merchandise, presented strong third-quarter results in its November 2024 earnings presentation. The company, which joined the Russell 2000 index in 2024, demonstrated significant growth across key metrics while continuing to expand its marketplace ecosystem.

The presentation highlighted GigaCloud’s evolution since its 2010 launch on Rakuten in Japan, through its 2022 NASDAQ IPO, to its current position as a comprehensive B2B marketplace connecting suppliers and resellers globally. However, this Q3 performance would later be followed by a Q4 deceleration and earnings miss that sent shares tumbling nearly 15%.

Quarterly Performance Highlights

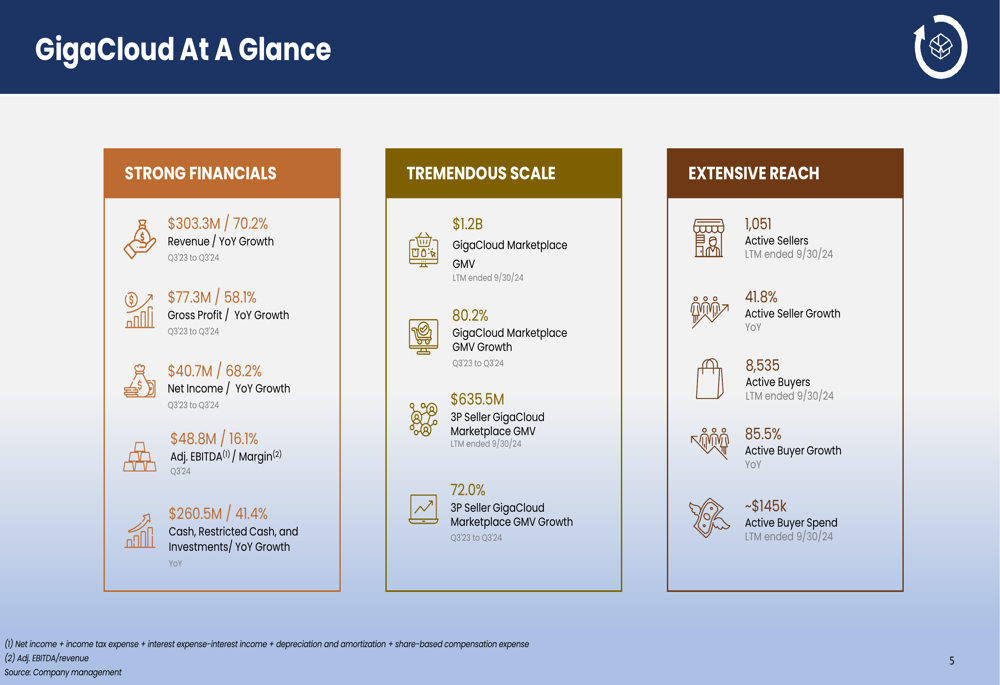

GigaCloud reported exceptional year-over-year growth in Q3 2024, with total revenues reaching $303.3 million, representing a 70.2% increase from Q3 2023. This growth was driven by both product revenue ($203.0 million) and service revenue ($100.3 million).

As shown in the following financial performance chart:

The company’s marketplace GMV (Gross Merchandise Value) showed even stronger growth, increasing 80.2% year-over-year to $1.23 billion. This growth was balanced across both first-party (1P) sales, which grew to $598.1 million, and third-party (3P) seller GMV, which reached $635.5 million.

Gross profit increased 58.1% year-over-year to $77.3 million, though gross margin contracted slightly from 27.4% to 25.5%. Similarly, Adjusted EBITDA grew to $48.8 million with a 16.1% margin, compared to $29.8 million and a 16.7% margin in the prior year period.

Detailed Financial Analysis

GigaCloud’s business model combines product-based revenue (1P), service-based revenue (3P), and logistics infrastructure, all supported by an algorithm-enabled technology stack. This integrated approach has fueled the company’s rapid expansion.

The company’s marketplace metrics demonstrate strong ecosystem growth:

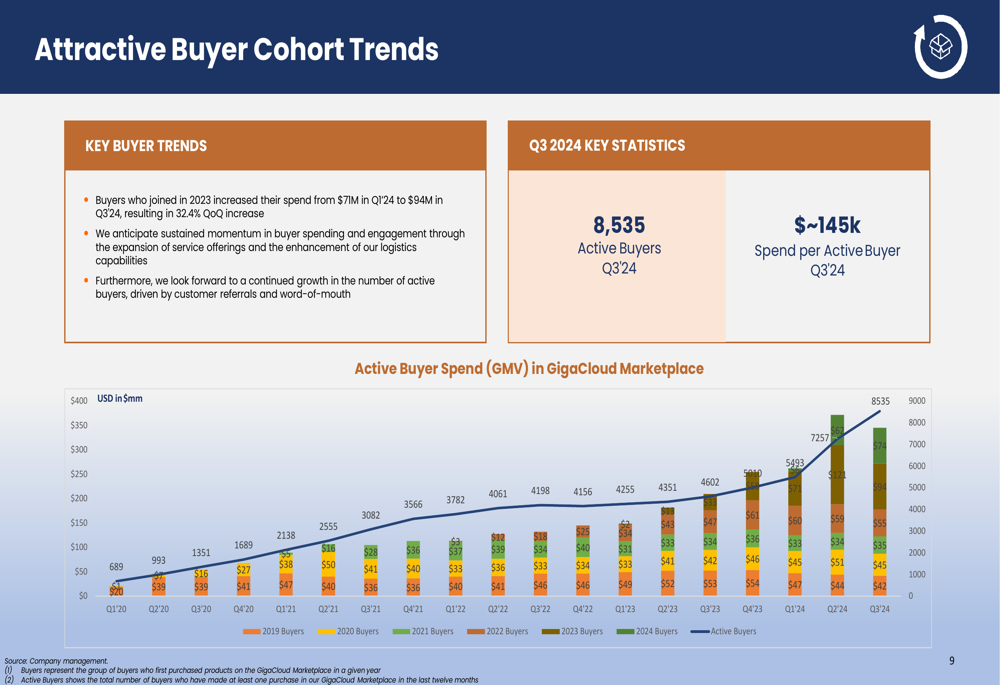

Active sellers on the platform increased 41.8% year-over-year to 1,051, while active buyers surged 85.5% to 8,535. The average spend per active buyer reached approximately $145,000 over the trailing twelve months ended September 30, 2024.

Buyer cohort analysis reveals increasing engagement over time, with buyers who joined in 2023 increasing their spend from $71 million in Q1 2024 to $94 million in Q3 2024, representing a 32.4% quarter-over-quarter increase.

The company’s seller and GMV growth has been particularly impressive, with 3P seller GMV on the GigaCloud Marketplace increasing 72.0% year-over-year to $635.5 million for the trailing twelve months ended September 30, 2024.

Strategic Initiatives

GigaCloud’s growth strategy focuses on four key areas: core business optimization, service offerings elevation, business reach acceleration, and technology enhancement. These initiatives leverage the company’s recent acquisitions of Noble House and Wondersign.

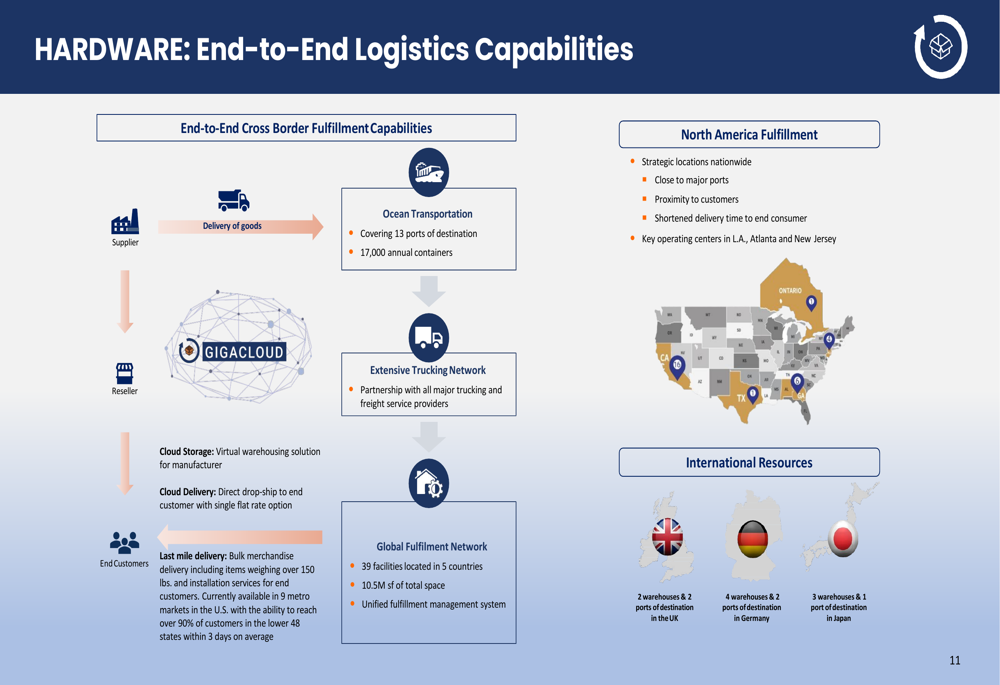

The company’s extensive logistics network serves as a competitive advantage, with 39 facilities across five countries totaling 10.5 million square feet of space. This infrastructure supports ocean transportation covering 13 destination ports and handling 17,000 annual containers.

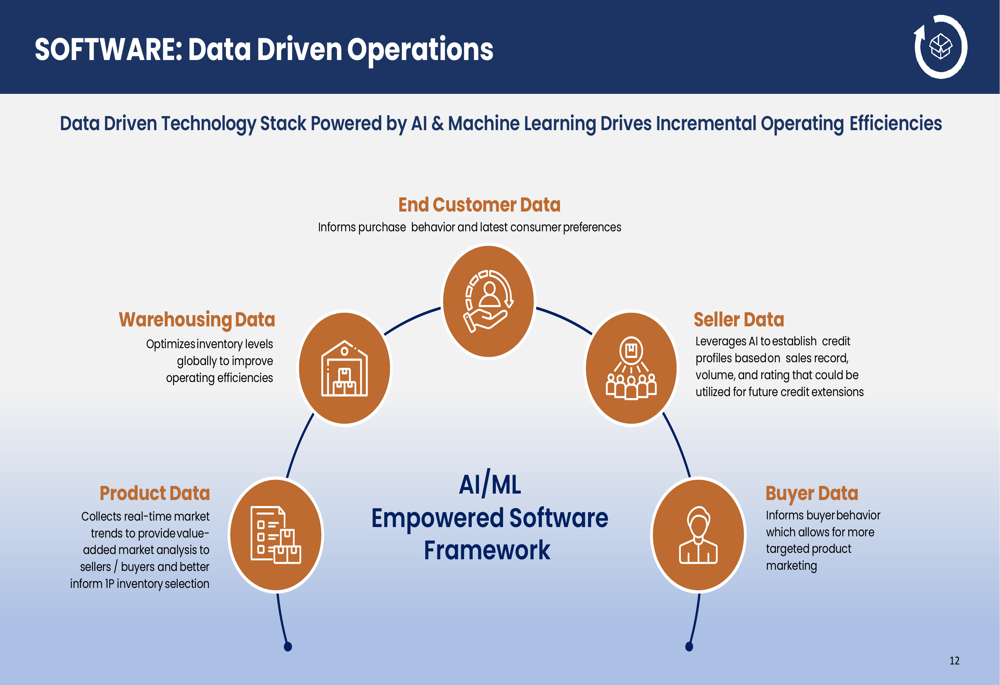

GigaCloud’s data-driven approach to operations leverages AI and machine learning to optimize various aspects of the business, from warehousing and inventory management to seller credit profiles and market trend analysis.

Forward-Looking Statements

Despite the strong Q3 2024 performance highlighted in the presentation, subsequent developments revealed challenges. According to recent earnings reports, GigaCloud’s Q4 2024 showed a significant deceleration, with revenue growing only 21% year-over-year to $296 million – a sequential decline from Q3. The company also missed earnings expectations with EPS of $0.75 versus the forecasted $0.82.

Looking ahead, GigaCloud has set Q1 2025 revenue guidance between $250 million and $265 million, suggesting continued sequential decline. Management anticipates temporary softening in Q2 but remains focused on profitable growth and further integration of Noble House operations.

The company faces several challenges, including potential macroeconomic headwinds affecting consumer spending, a 9% year-over-year decline in new furniture orders across the industry, margin pressures from inventory and freight costs, and ongoing integration of acquisitions.

Despite these challenges, GigaCloud maintains strong fundamentals with a gross profit margin of 26.13% and a return on equity of 40%. The company’s stock, which closed at $12.81 on May 1, 2025, remains well below its 52-week high of $41.31, potentially reflecting investor concerns about the growth slowdown following the impressive Q3 2024 performance highlighted in this presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.