AngloGold Ashanti’s shares rise nearly 3% as profit soars on higher gold prices

Global Net Lease Inc. (NYSE:GNL) shares climbed 6.09% to $7.55 on November 6, 2025, as investors responded positively to the company’s third-quarter investor presentation despite an earnings miss. The real estate investment trust highlighted significant progress in its strategic transformation, including substantial debt reduction and a credit rating upgrade.

Strategic Transformation Highlights

GNL’s presentation emphasized its successful execution of strategic initiatives since the internalization in 2023. Most notably, the company achieved an investment-grade credit rating of BBB- from Fitch Ratings, an upgrade from its previous BB+ rating. This milestone reflects GNL’s improved financial position and opens doors to potentially lower borrowing costs.

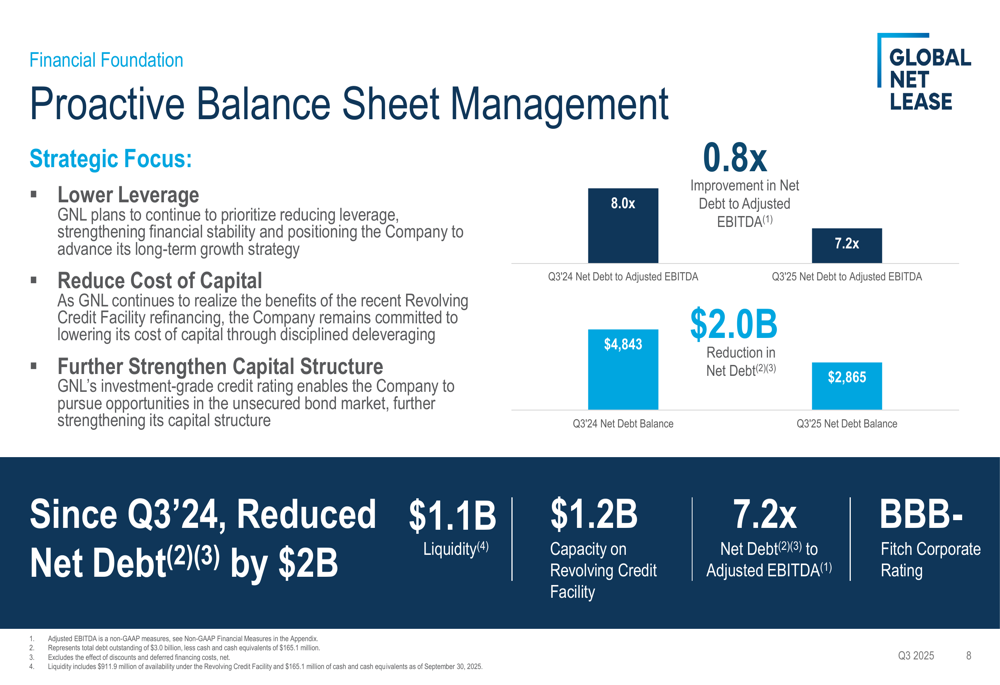

The company has dramatically reduced its leverage, cutting net debt by $2 billion since Q3 2024 to $2.87 billion. This reduction helped improve the net debt to adjusted EBITDA ratio from 8.0x to 7.2x year-over-year.

As shown in the following balance sheet management overview:

A cornerstone of GNL’s transformation strategy has been its disciplined disposition program. The company has closed on 273 property sales totaling $2.08 billion, with an additional 28 properties under contract for $121.5 million. These dispositions have achieved a cash cap rate of 8.4%, allowing GNL to streamline its portfolio while generating significant proceeds for debt reduction.

The completion of a $1.8 billion multi-tenant retail portfolio sale marked a pivotal transaction in the company’s strategic shift toward a pure-play single-tenant focus. This move aligns with GNL’s goal of reducing capital expenditures and G&A costs while simplifying operations.

Portfolio Composition and Performance

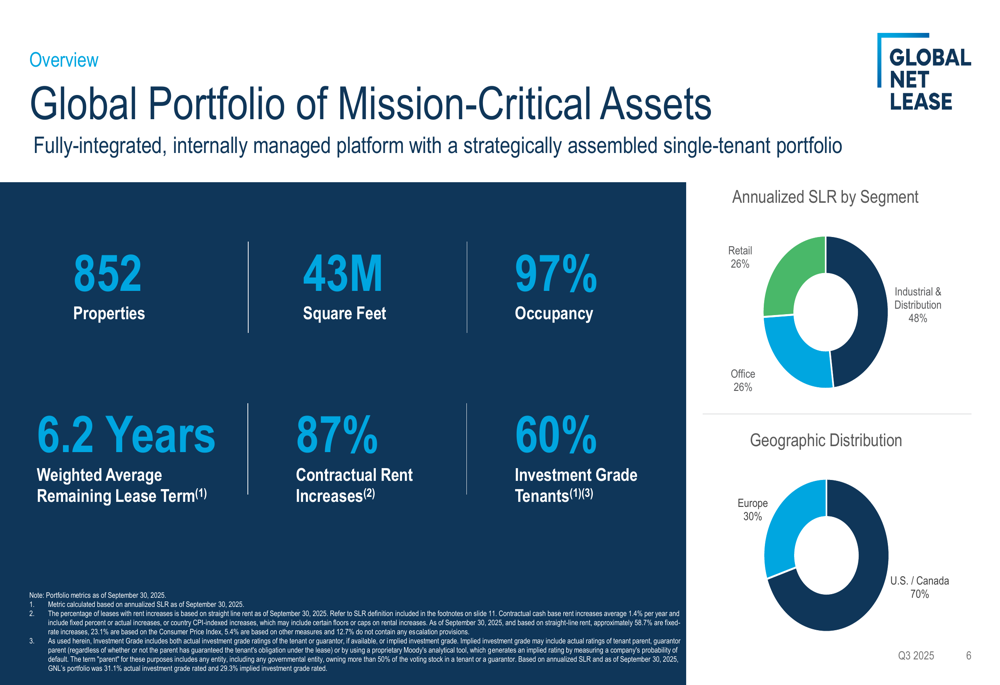

GNL’s portfolio now consists of 852 properties spanning 43 million square feet, maintaining a strong 97% occupancy rate. The portfolio features a weighted average remaining lease term of 6.2 years, with 87% of leases containing contractual rent increases and 60% of tenants holding investment-grade ratings.

The company’s property mix is well-balanced across three segments: industrial and distribution (48%), retail (26%), and office (26%). This diversification helps mitigate sector-specific risks while allowing GNL to optimize its holdings.

The following chart illustrates GNL’s global portfolio characteristics:

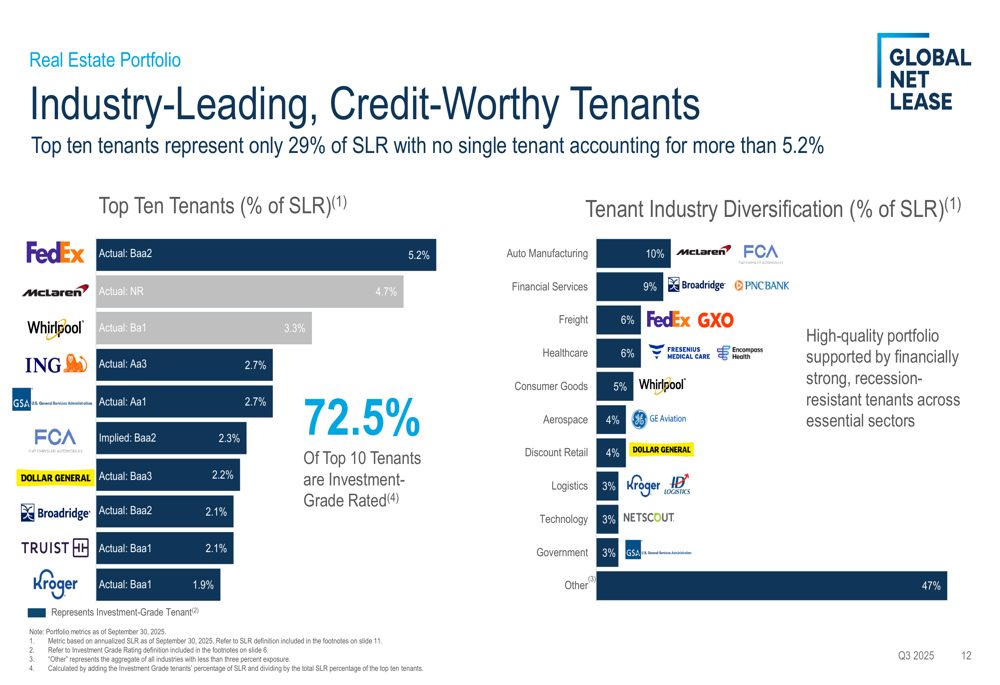

GNL’s tenant base represents another strength, with the top ten tenants accounting for only 29% of straight-line rent (SLR), indicating limited concentration risk. The portfolio is further diversified across industries, with auto manufacturing (10%), financial services (9%), and freight (6%) representing the largest sectors.

As shown in the tenant overview:

The company’s geographic footprint spans the United States (70.5%) and Europe (29.5%), providing exposure to multiple markets while maintaining a focus on stable, developed economies.

Leasing Activity and Property Segments

GNL reported strong leasing momentum in Q3 2025, completing 12 new leases and renewals covering over 1 million square feet. The company achieved an impressive 26.4% renewal leasing spread, demonstrating its ability to capture higher rents in the current market environment.

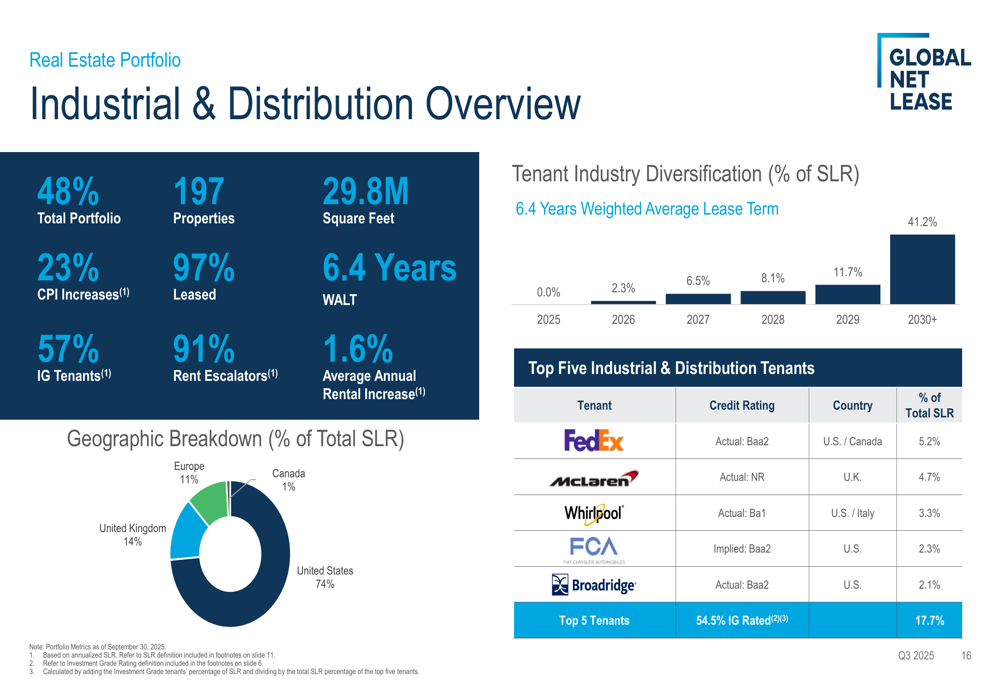

The industrial and distribution segment, which represents 48% of GNL’s portfolio, features 197 properties spanning 29.8 million square feet. This segment maintains a weighted average lease term of 6.4 years, with 57% of tenants holding investment-grade ratings and 91% of leases containing rent escalators.

The following industrial and distribution portfolio overview provides additional details:

The retail segment comprises 596 properties totaling 6.7 million square feet, with key tenants including Dollar General, Truist, and Fresenius Medical Care. This segment maintains a strong 6.9-year weighted average lease term and 80% of leases include rent escalators.

The office portfolio, while representing 26% of the total, maintains strong fundamentals with 94% occupancy and 77% investment-grade tenants. Notably, 64% of these properties are considered "mission critical" to their tenants, potentially reducing tenant turnover risk.

Financial Results and Debt Profile

Despite the positive strategic developments, GNL’s Q3 2025 financial results were mixed. The company reported AFFO per share of $0.24, but posted a net loss with EPS of -$0.33, significantly below analyst expectations of -$0.075. Revenue came in at $121 million, slightly under the anticipated $123.51 million.

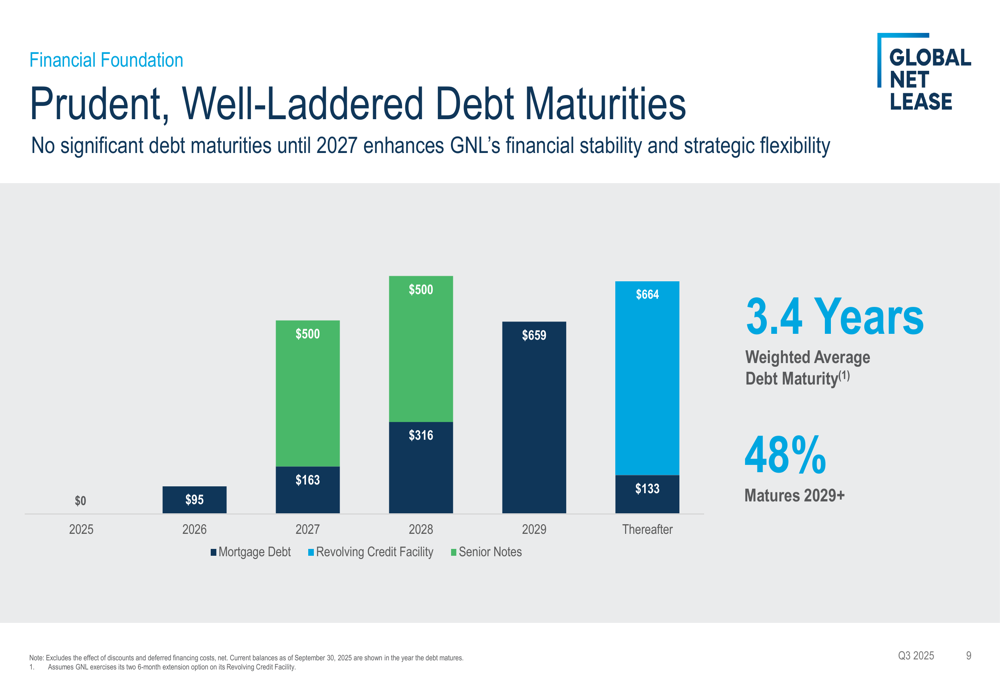

The company’s debt profile has improved substantially, with total debt reduced to $3.03 billion. GNL maintains a weighted average interest rate of 4.2% and an interest coverage ratio of 2.9x. Importantly, the company has no significant debt maturities until 2027, providing financial flexibility in the near term.

The debt maturity schedule shows a well-laddered approach:

GNL’s liquidity position remains strong at $1.1 billion, including capacity on its revolving credit facility of $1.2 billion. This provides ample resources for potential share repurchases and strategic investments.

Forward Outlook

In a sign of management’s confidence, GNL raised its full-year 2025 AFFO per share guidance to $0.95-$0.97. The company reaffirmed its 2025 net debt to adjusted EBITDA guidance range of 6.5x to 7.1x, indicating continued focus on deleveraging.

During the earnings call, CEO Michael Weil emphasized the company’s focus on maximizing shareholder value, noting that share repurchases offer significant immediate accretion. Management also indicated they are preparing for GNL’s next growth phase, though they acknowledged that current high cap rates and debt costs make acquisitions less attractive.

The company anticipates potential Federal Reserve rate cuts in spring 2026, which could create more favorable conditions for acquisitions and refinancing. In the meantime, GNL plans to continue its disposition program, focus on debt reduction, and make opportunistic share repurchases.

Investors appear to be looking past the earnings miss to focus on the company’s strategic progress and improved financial position, as evidenced by the stock’s positive performance following the presentation. With its strengthened balance sheet, upgraded credit rating, and streamlined portfolio, GNL is positioning itself for potentially improved performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.