Street Calls of the Week

Introduction & Market Context

GN Store Nord (CPH:GN) reported challenging first-quarter results on May 1, 2025, with organic revenue declining 3% excluding wind-down effects. The Danish audio and hearing aid company faced headwinds from market uncertainty and challenging economic conditions, particularly in Europe, leading to a significant drop in its EBITA margin to 7.5% from 12.5% in the same period last year.

The company’s stock reacted negatively to the results, falling 6.9% to 98.60 DKK during the presentation, reflecting investor concerns about the weaker-than-expected performance and the impact of the changing trade environment on GN’s operations.

As shown in the following overview of key financial metrics:

Quarterly Performance Highlights

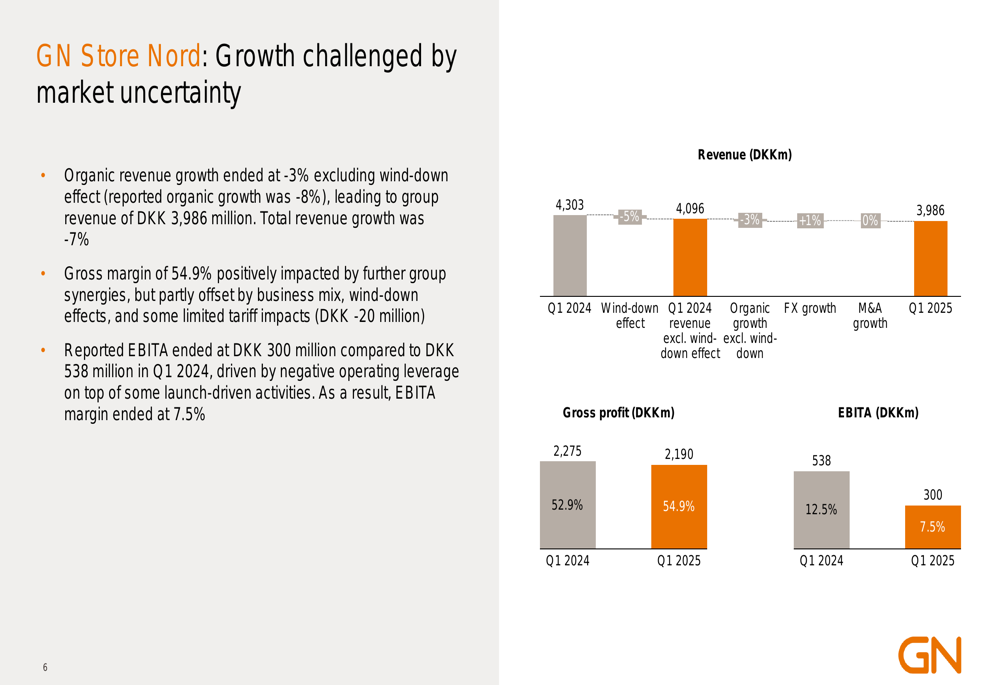

GN Store Nord reported Q1 2025 revenue of 3,986 million DKK, representing a 7% decline compared to Q1 2024. Organic revenue growth was -8% on a reported basis, or -3% when excluding the wind-down effect of the consumer business. The gross margin improved to 54.9% from 52.9% in the prior year, but EBITA fell to 300 million DKK from 538 million DKK, resulting in an EBITA margin of 7.5%.

The detailed financial breakdown reveals the extent of the challenges facing the company:

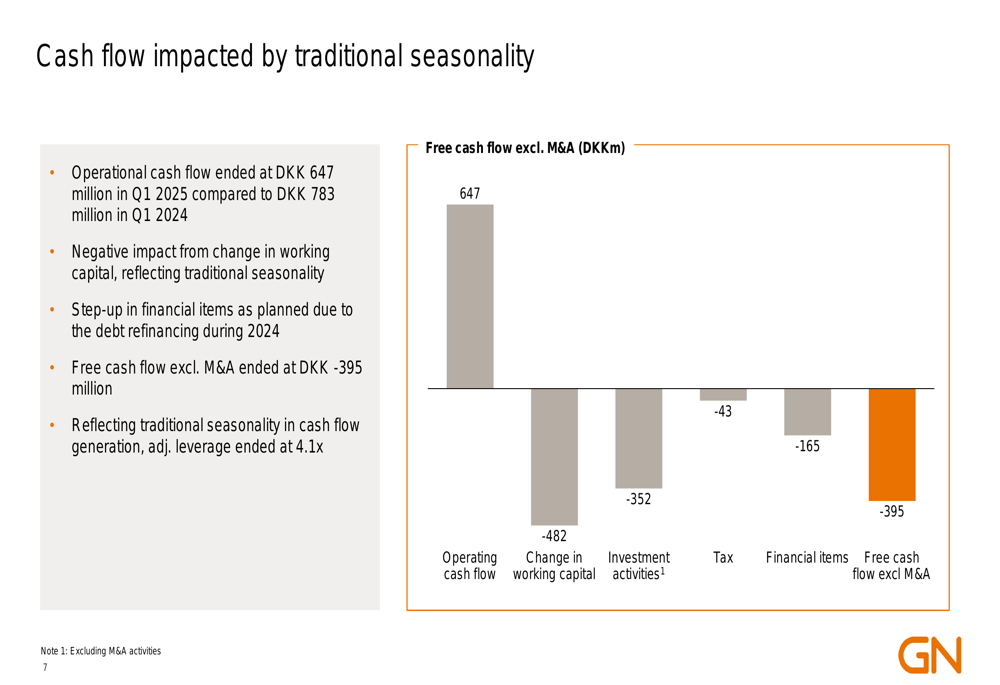

Cash flow was also impacted by seasonality, with free cash flow excluding M&A at -395 million DKK. The company noted that operational cash flow ended at 647 million DKK, but was offset by negative impacts from changes in working capital, investment activities, tax, and financial items related to debt refinancing.

As illustrated in this cash flow breakdown:

Divisional Performance Analysis

GN’s three divisions delivered markedly different performances in Q1 2025, with Gaming showing strong growth while Hearing and Enterprise faced challenges.

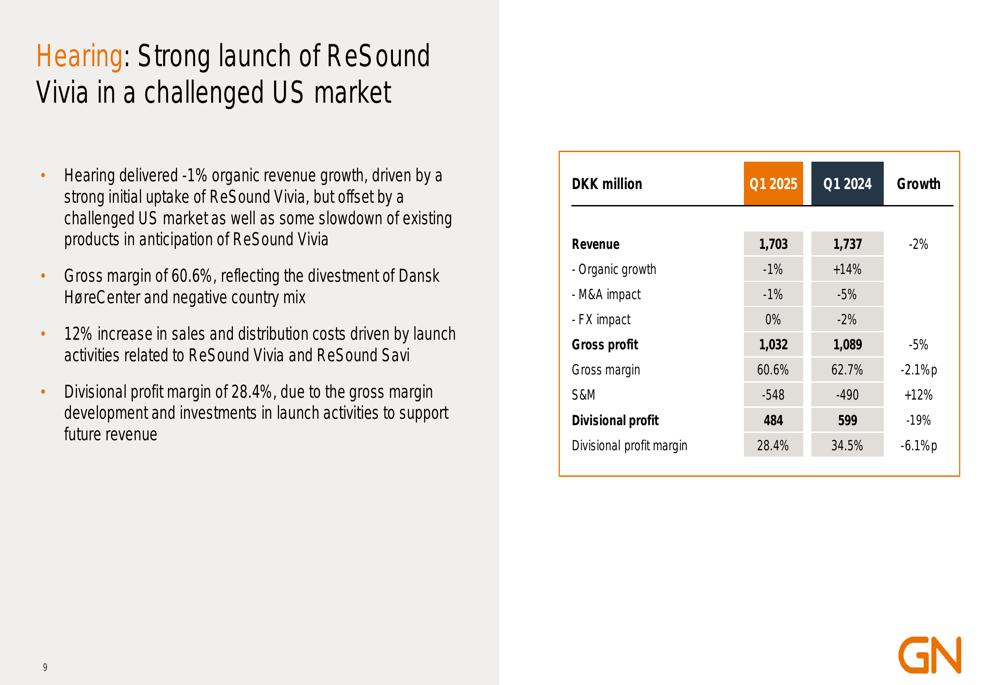

The Hearing division reported a modest 1% organic revenue decline, with revenue of 1,703 million DKK. Despite challenges in the US market, the division benefited from the strong initial uptake of ReSound Vivia and Savi products. Gross margin was 60.6%, down from 62.7% in Q1 2024, while divisional profit margin decreased to 28.4% from 34.5%, partly due to a 12% increase in sales and distribution costs.

The detailed Hearing division results show:

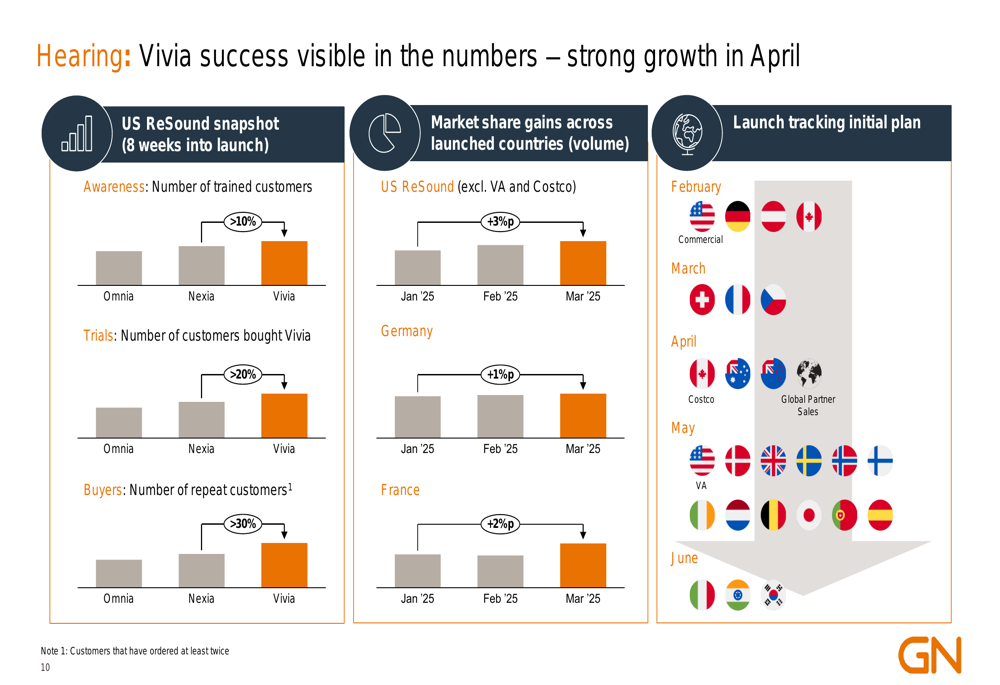

The company highlighted the success of its Vivia product launch, noting market share gains across several countries, with particularly strong performance in the US (+3 percentage points), Germany (+1 percentage point), and France (+2 percentage points).

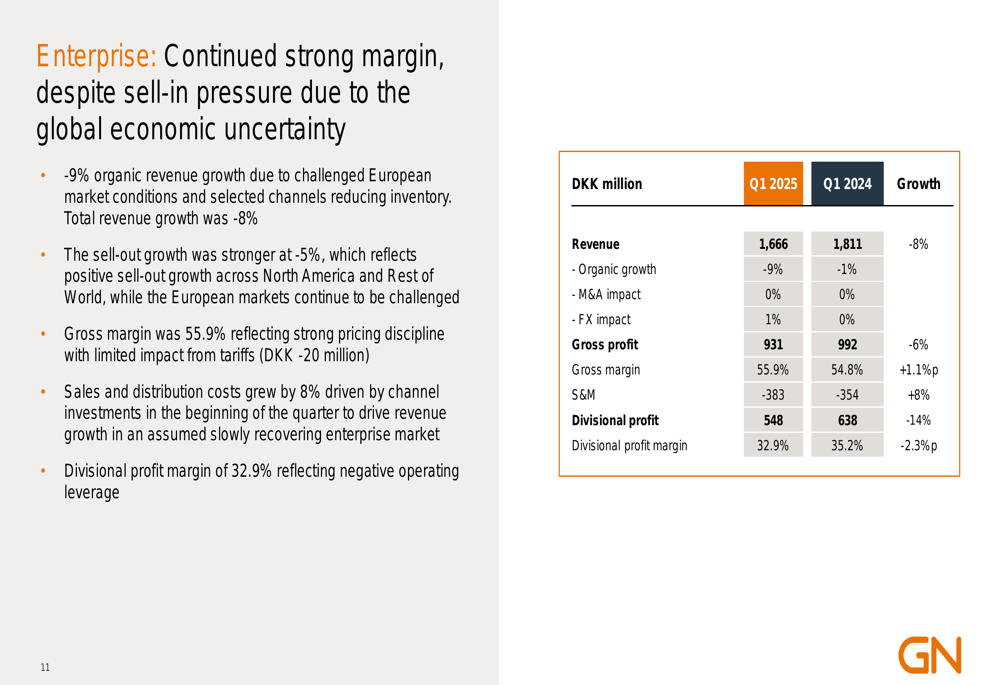

The Enterprise division faced the most significant challenges, with organic revenue declining 9% to 1,666 million DKK. The division was particularly affected by difficult economic conditions in Europe, although sell-out growth was stronger at -5%. Despite these challenges, gross margin improved to 55.9% from 54.8%, though divisional profit margin fell to 32.9% from 35.2%.

The Enterprise division’s financial performance is detailed here:

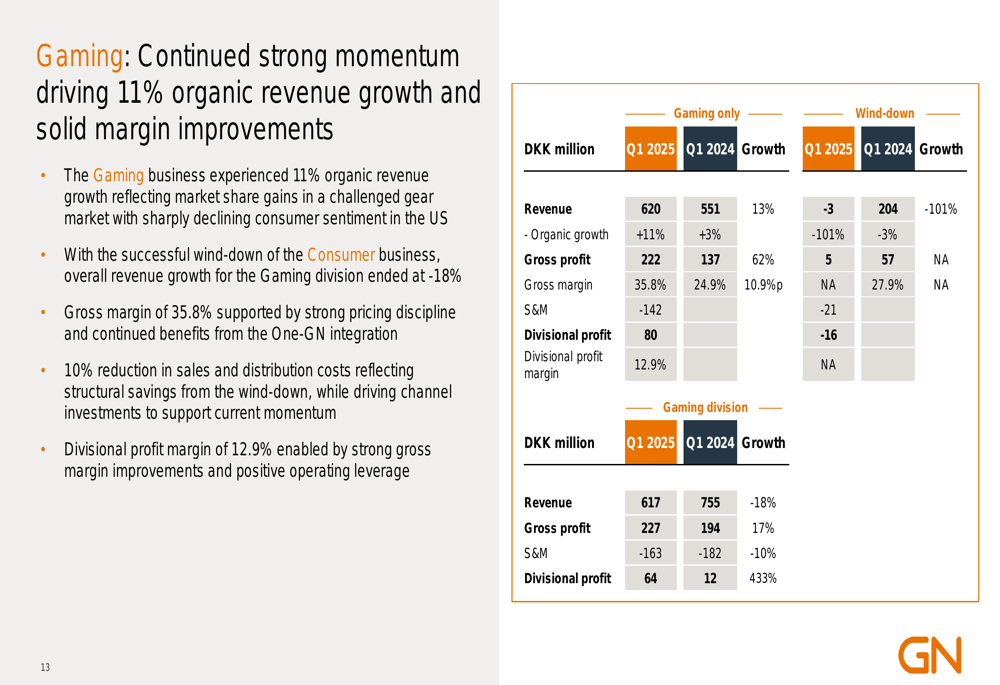

In contrast, the Gaming division was a bright spot, delivering 11% organic revenue growth (excluding wind-down effects). With the successful wind-down of the Consumer business, overall revenue for the Gaming division ended at 617 million DKK, representing an 18% decline from Q1 2024. However, gross margin improved significantly to 35.8% from 24.9%, and divisional profit surged to 64 million DKK from 12 million DKK, representing a 433% increase.

The Gaming division’s impressive performance metrics:

Strategic Initiatives

In response to the challenging trade environment, GN Store Nord outlined several strategic initiatives to protect its financial performance:

1. Accelerating the diversification of its manufacturing footprint

2. Implementing price increases in the Enterprise and Gaming divisions

3. Launching cost and cash flow initiatives to protect financials

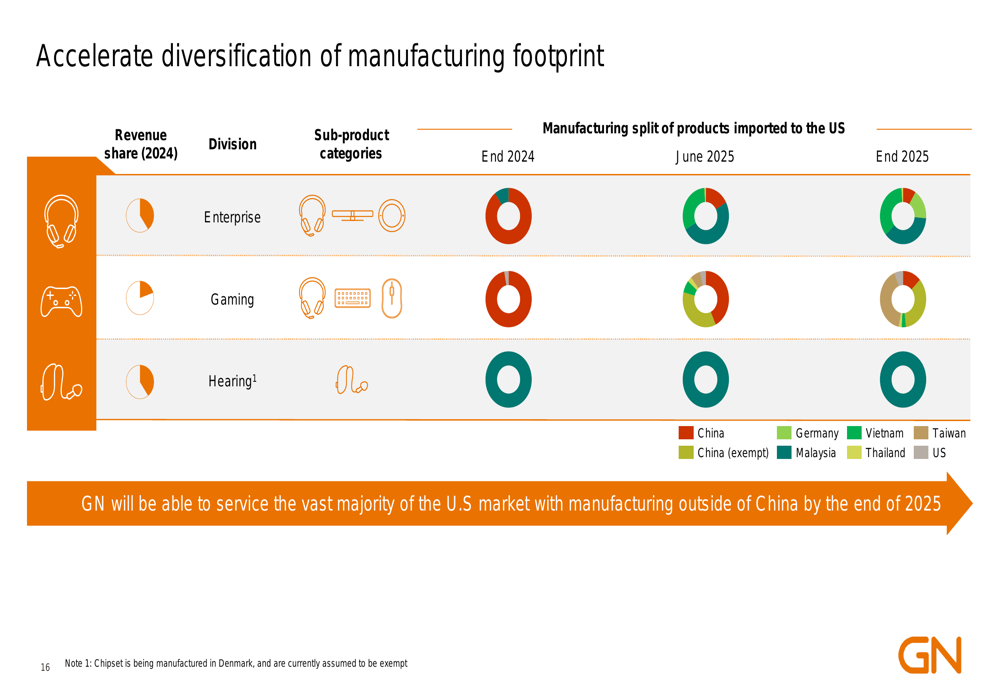

The company presented a detailed plan for manufacturing diversification, showing how it will reduce dependence on China for products imported to the US:

GN Store Nord stated that by the end of 2025, it will be able to service the vast majority of the US market with manufacturing outside of China, significantly reducing exposure to potential tariff increases.

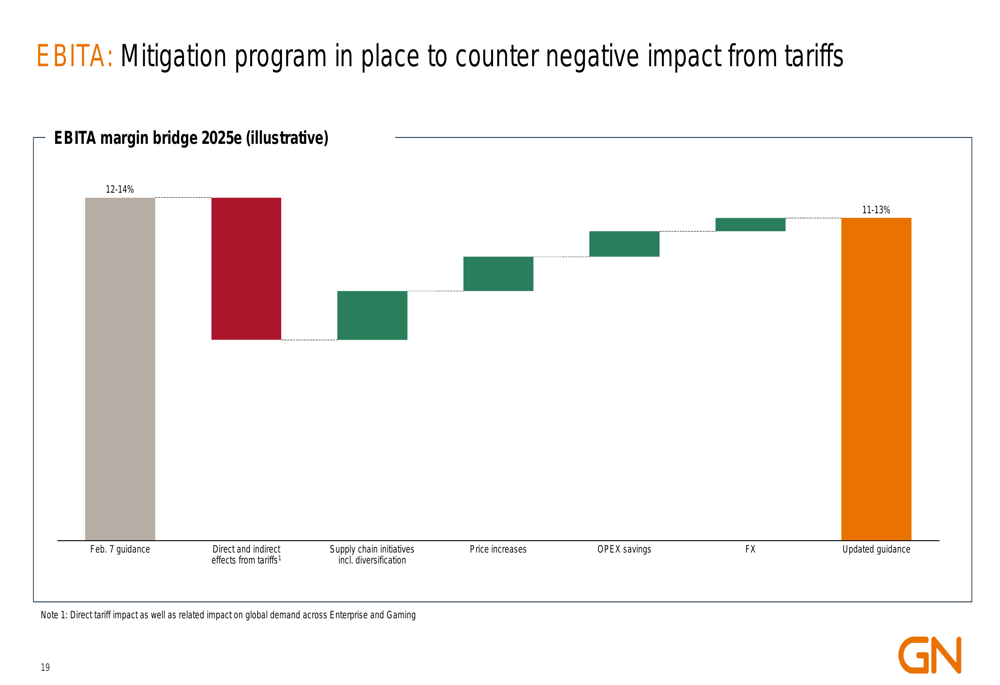

To mitigate the impact on EBITA margins, the company has implemented a comprehensive program that includes supply chain initiatives, price increases, and OPEX savings:

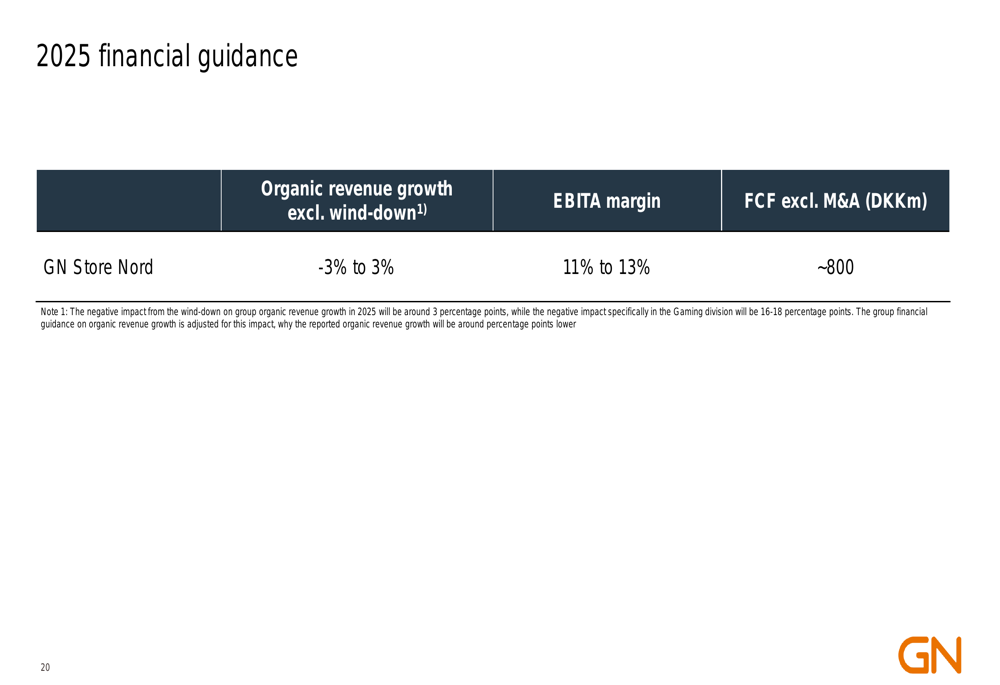

Financial Guidance & Outlook

Despite the challenging Q1 results, GN Store Nord maintained a cautiously optimistic outlook for the remainder of 2025, though it adjusted its financial guidance. The company now expects:

- Organic revenue growth (excluding wind-down) of -3% to 3%

- EBITA margin of 11% to 13%

- Free cash flow excluding M&A of approximately 800 million DKK

The updated guidance reflects the company’s assessment of the current market environment:

For the Hearing division, GN expects the market to grow in line with historical rates of 3-5% in value, with ReSound Vivia and Savi driving market share gains. The division’s revenue growth is projected at 5% to 9%.

The Enterprise division faces continued global macroeconomic uncertainty, with revenue growth expected between -8% and 0%. Meanwhile, the Gaming division is projected to deliver between -6% and +2% revenue growth (excluding wind-down effects), as it navigates global economic uncertainty and declining consumer sentiment.

GN Store Nord’s Q1 2025 results highlight the challenges facing the company in an uncertain global economic environment. While the Gaming division shows promising growth and margin expansion, the Hearing and Enterprise divisions face headwinds that have led to an overall decline in organic revenue. The company’s strategic initiatives to diversify manufacturing, implement price increases, and control costs will be crucial in navigating these challenges and achieving its updated financial guidance for the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.