Gold bars to be exempt from tariffs, White House clarifies

Introduction & Market Context

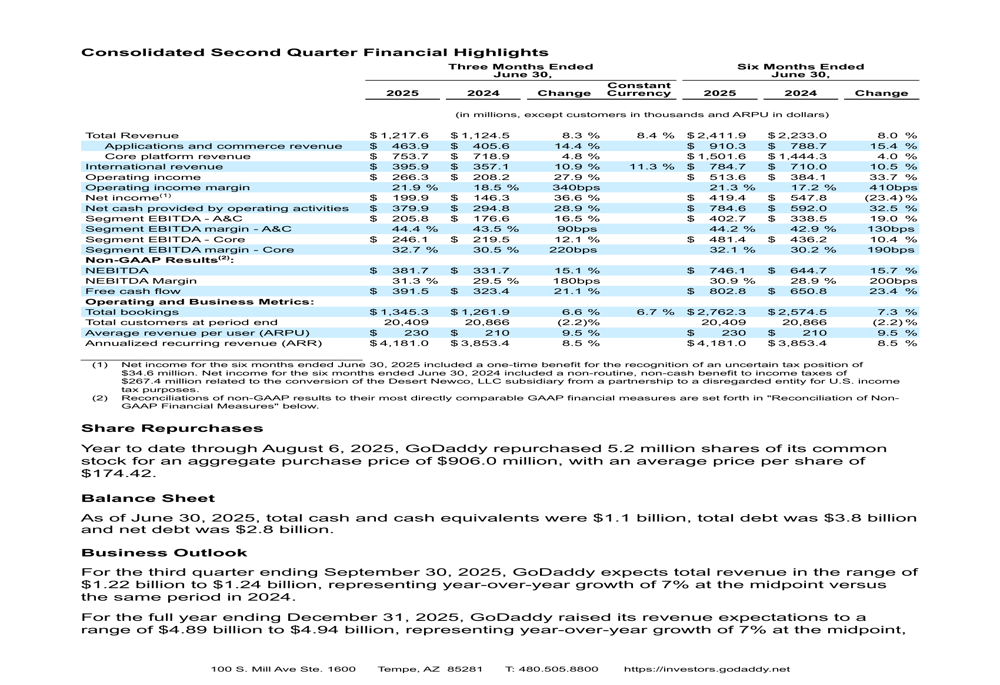

GoDaddy Inc. (NYSE:GDDY) reported strong second-quarter 2025 financial results on August 7, demonstrating continued growth across key metrics despite broader economic uncertainty. The domain registrar and web hosting company posted an 8.3% year-over-year revenue increase, with particularly strong performance in its Applications and Commerce segment.

The company’s results come amid mixed economic sentiment among small businesses, with GoDaddy’s own research indicating that 72% of U.S. customers expect their revenue to increase or remain stable, while only 45% anticipate similar stability in the broader U.S. economy.

GoDaddy shares closed at $150.25 on August 7, down 2.95% for the day, reflecting a significant decline from the $180.56 price following its Q1 2025 earnings report. This suggests investors may be responding to factors beyond the company’s operational performance, as the stock has fallen approximately 16.8% since the previous quarter despite consistently strong results.

Quarterly Performance Highlights

GoDaddy reported total revenue of $1.22 billion for Q2 2025, representing an 8.3% increase compared to the same period in 2024. The company’s Applications and Commerce segment was the standout performer, growing 14.4% year-over-year to reach $463.9 million, while Core Platform revenue rose 4.8% to $753.7 million.

As shown in the consolidated financial highlights:

Operating income saw substantial improvement, rising 27.9% year-over-year to $266.3 million, representing a 22% margin. Net income grew even more impressively, increasing 37% to $199.9 million compared to $146.3 million in Q2 2024.

Normalized EBITDA, a key profitability metric for the company, reached $381.7 million, up 15.1% year-over-year, with a margin of 31%. Free cash flow also showed strong growth, increasing 21.1% to $391.5 million.

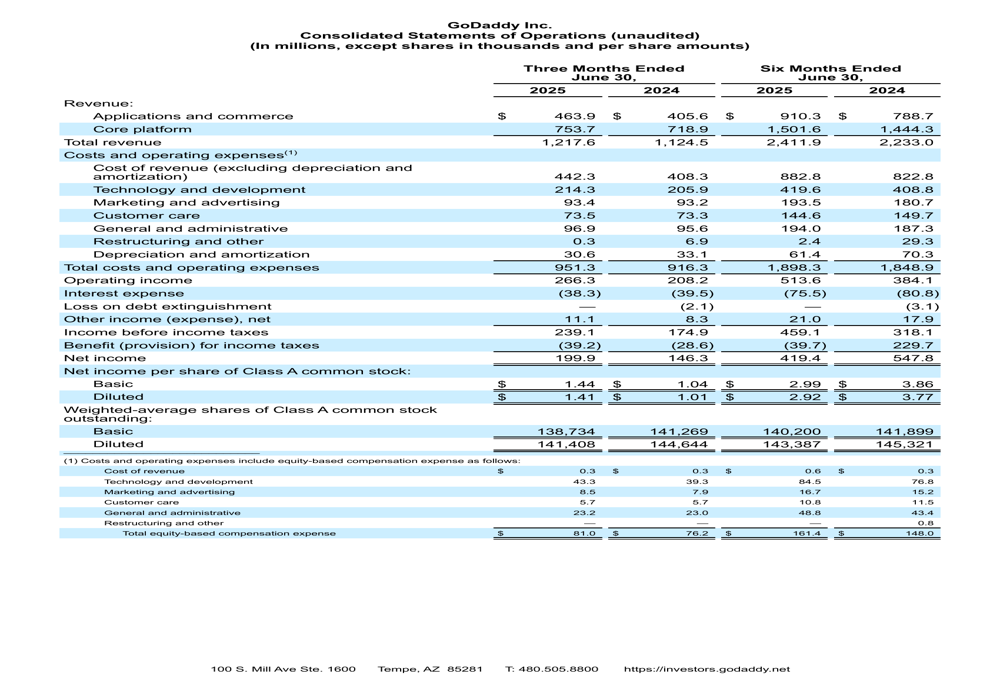

The company’s detailed statements of operations provide further insight into its financial performance:

Detailed Financial Analysis

GoDaddy’s bookings, which represent the total value of customer contracts entered during the period, grew 6.6% year-over-year to $1.35 billion. This metric is particularly important as it provides visibility into future revenue recognition.

Average Revenue Per User (ARPU) continued its upward trajectory, reaching $230, a 9.5% increase compared to Q2 2024. This growth suggests the company’s strategy of focusing on high-value customers and expanding its service offerings is yielding positive results.

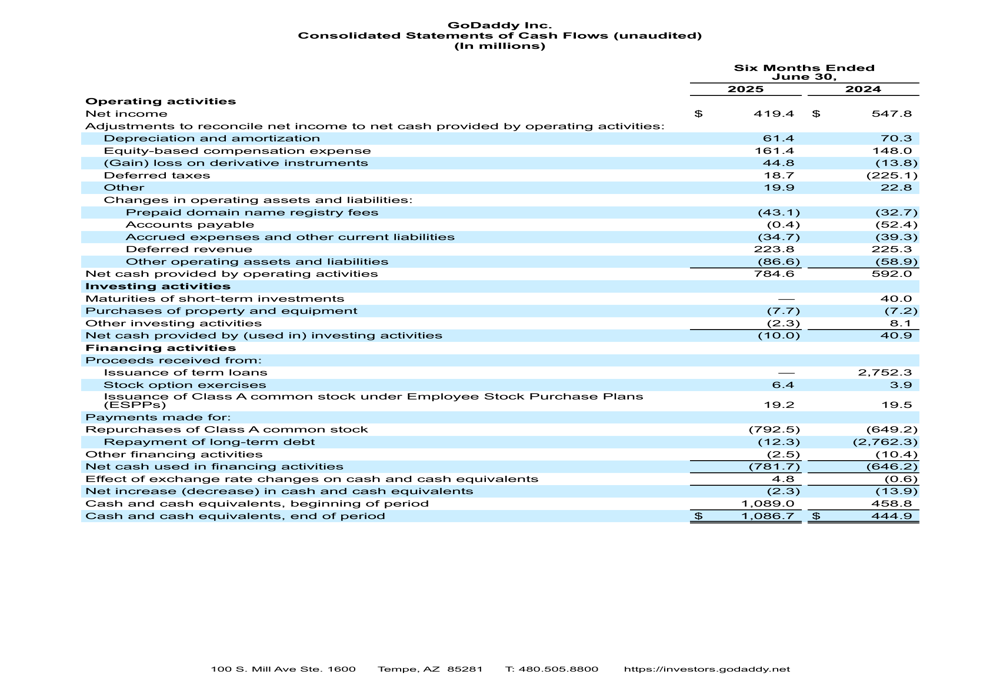

The company’s cash flow generation remained robust, as demonstrated in its consolidated statements of cash flows:

GoDaddy maintained a strong balance sheet with $1.1 billion in cash and cash equivalents as of June 30, 2025. Total (EPA:TTEF) debt stood at $3.8 billion, resulting in net debt of $2.8 billion. The company’s capital allocation strategy continued to prioritize share repurchases, with 5.2 million shares bought back year-to-date through August 6, 2025, for an aggregate purchase price of $906 million at an average price of $174.42 per share.

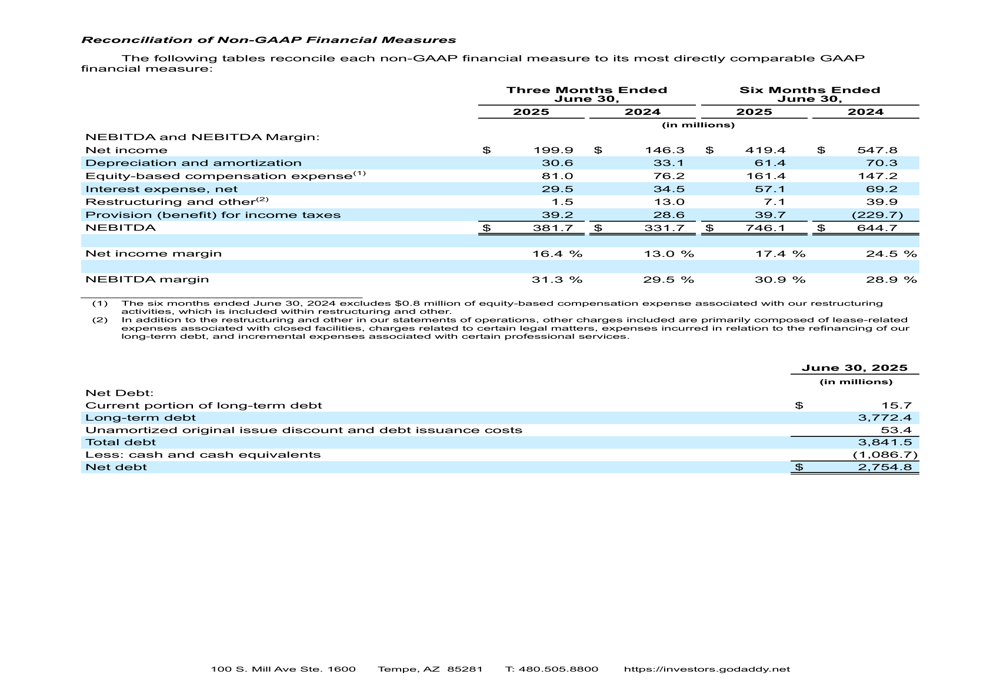

The reconciliation of non-GAAP financial measures provides additional context for understanding GoDaddy’s performance:

Forward-Looking Statements & Guidance

Based on its strong first-half performance, GoDaddy raised its full-year 2025 revenue guidance to between $4.89 billion and $4.94 billion. For the third quarter of 2025, the company expects revenue in the range of $1.22 billion to $1.24 billion.

GoDaddy anticipates continued divergence in segment performance, with Applications and Commerce revenue projected to grow in the mid-teens, while Core Platform revenue is expected to increase at a low single-digit rate. The company noted that beginning in Q4 2025, it will no longer be the registry service provider for the .CO top-level domain, which will result in a 50 basis point headwind.

On the profitability front, GoDaddy expects a Normalized EBITDA margin of approximately 32% for Q3 2025 and is targeting approximately 33% by the end of 2025. The company also raised its free cash flow target to $1.6 billion, reflecting confidence in its operational efficiency and cash generation capabilities.

Strategic Initiatives

CEO Aman Bhutani highlighted the company’s strategy and the potential of agentic AI in his comments, suggesting GoDaddy continues to invest in technological innovation to maintain its competitive edge. This aligns with the company’s previous quarter emphasis on AI-driven products like GoDaddy Airo.

CFO Mark McCaffrey emphasized the company’s focus on high-intent customers and maximizing free cash flow, a strategy that appears to be delivering results as evidenced by the improved margins and increased cash generation.

GoDaddy’s continued investment in its Applications and Commerce segment is paying dividends, with this higher-margin business growing at nearly three times the rate of the Core Platform segment. This shift in revenue mix toward higher-value services is likely contributing to the overall margin improvement.

The company remains committed to its share repurchase program, which has been a consistent element of its capital allocation strategy. With $906 million spent on buybacks year-to-date at an average price significantly higher than the current trading level, GoDaddy’s management appears to see the stock as undervalued at current prices.

As GoDaddy continues to execute on its strategic initiatives while delivering strong financial results, the disconnect between operational performance and stock price movement suggests investors may be factoring in broader economic concerns or competitive pressures not immediately evident in the company’s financial statements.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.