JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

goeasy Ltd (TSX:GSY) presented its Q2 2025 earnings results on August 7, 2025, showcasing a strong recovery from its disappointing Q1 performance. The company’s stock has rebounded significantly since the Q1 earnings miss, currently trading at $186, up from the post-Q1 low of $145.10, though down slightly by 0.26% in the most recent session.

The non-prime lender delivered record loan growth and revenue in Q2, successfully navigating challenges from interest rate caps through an increased focus on secured lending and operational efficiency improvements. This quarter’s results mark a substantial improvement over Q1 2025, when the company missed analyst expectations with an adjusted EPS of $3.53 against a forecasted $4.53.

Quarterly Performance Highlights

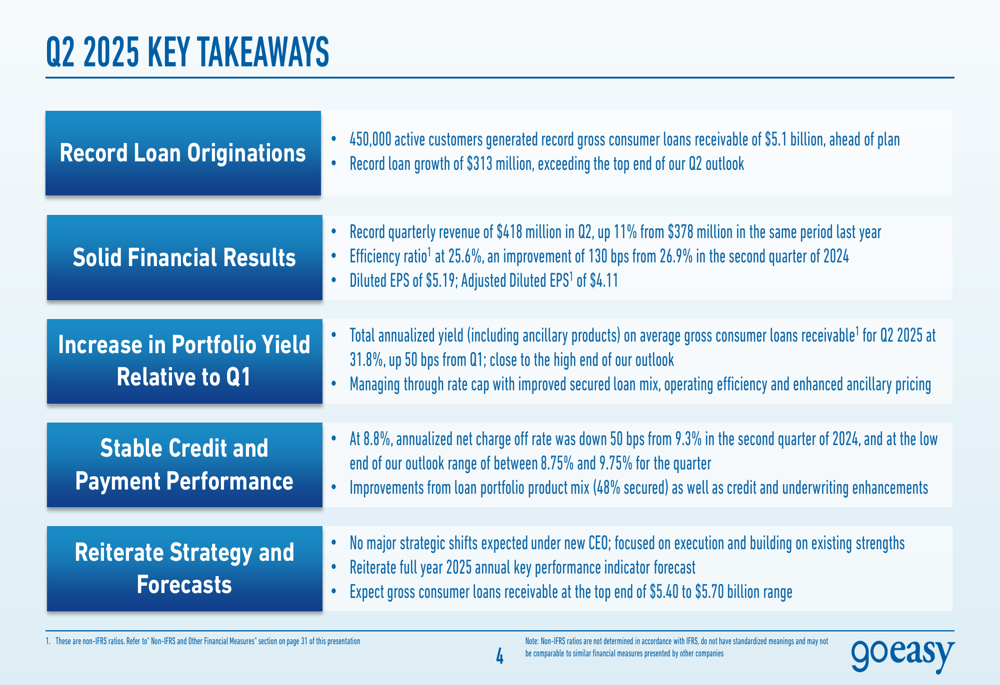

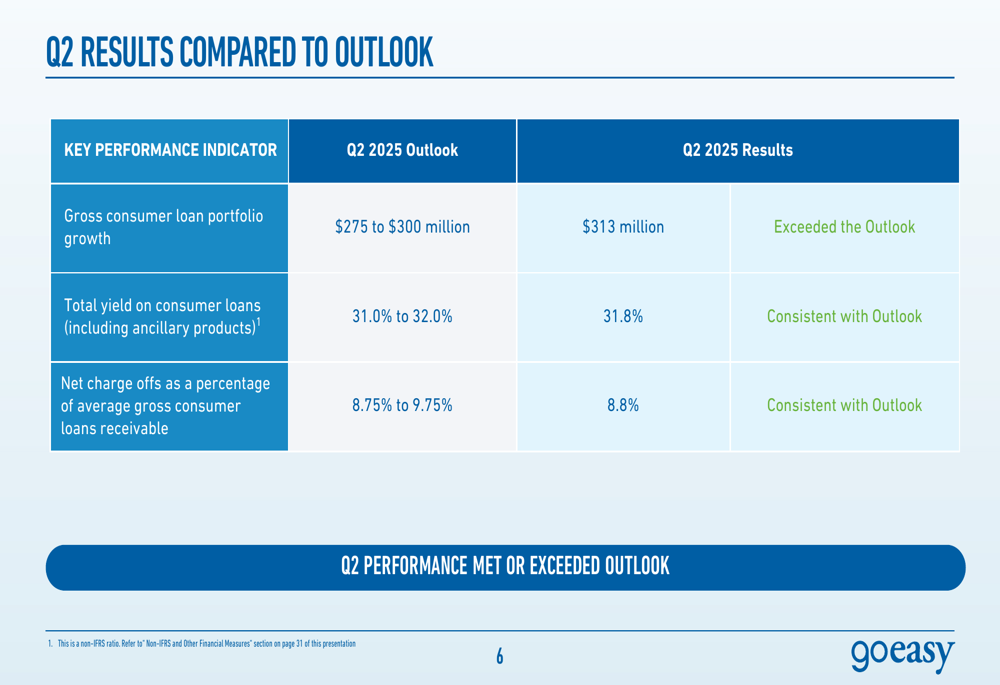

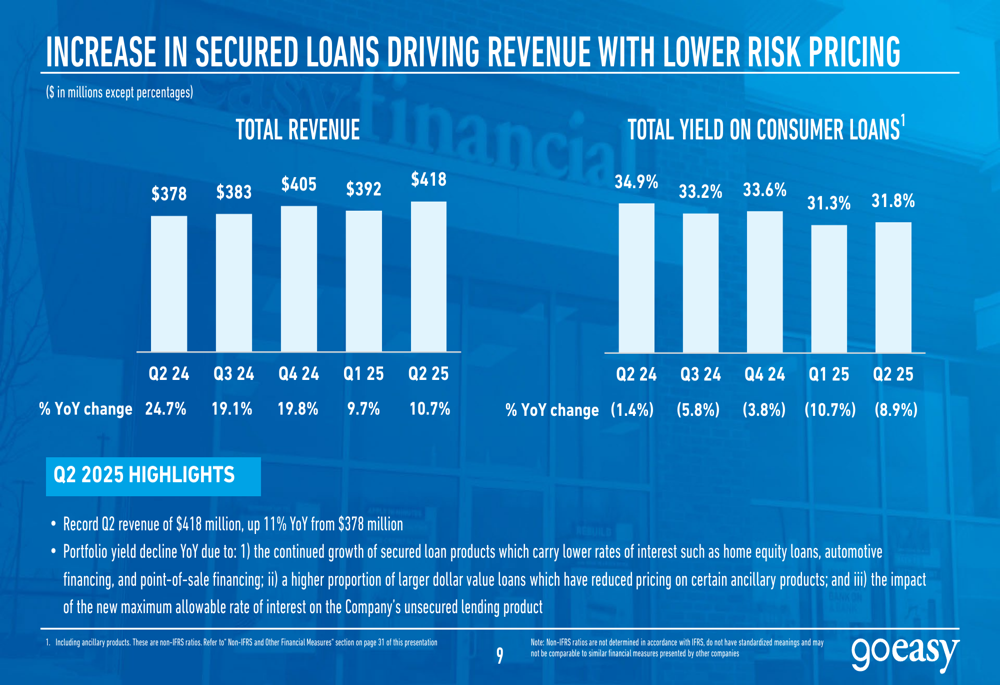

goeasy reported record gross consumer loans receivable of $5.1 billion in Q2 2025, with exceptional loan growth of $313 million that exceeded the company’s own guidance range of $275-300 million. The company achieved record quarterly revenue of $418 million, representing an 11% increase from $378 million in Q2 2024.

As shown in the following key takeaways from the presentation, the company delivered solid financial results while maintaining stable credit performance:

Efficiency improvements were a standout feature of the quarter, with the efficiency ratio improving to 25.6%, representing a 130 basis point enhancement year-over-year. This operational leverage helped offset the impact of regulatory interest rate caps on the company’s unsecured lending products.

The company’s Q2 results consistently met or exceeded its previously stated outlook across all key metrics:

Detailed Financial Analysis

goeasy’s strong performance was driven by record loan originations of $904 million in Q2 2025, a 9% increase compared to $827 million in the same period last year. The company added 50,300 new customers, up 3% year-over-year, with applications for credit increasing by 23%.

The following chart illustrates the consistent growth in both loan originations and gross consumer loans receivable over the past five quarters:

Revenue growth remained robust at 11% year-over-year, reaching $418 million for the quarter. While the total yield on consumer loans decreased year-over-year from 34.9% to 31.8% due to the growing proportion of secured loans and regulatory interest rate caps, it showed a 50 basis point improvement from Q1 2025’s 31.3%.

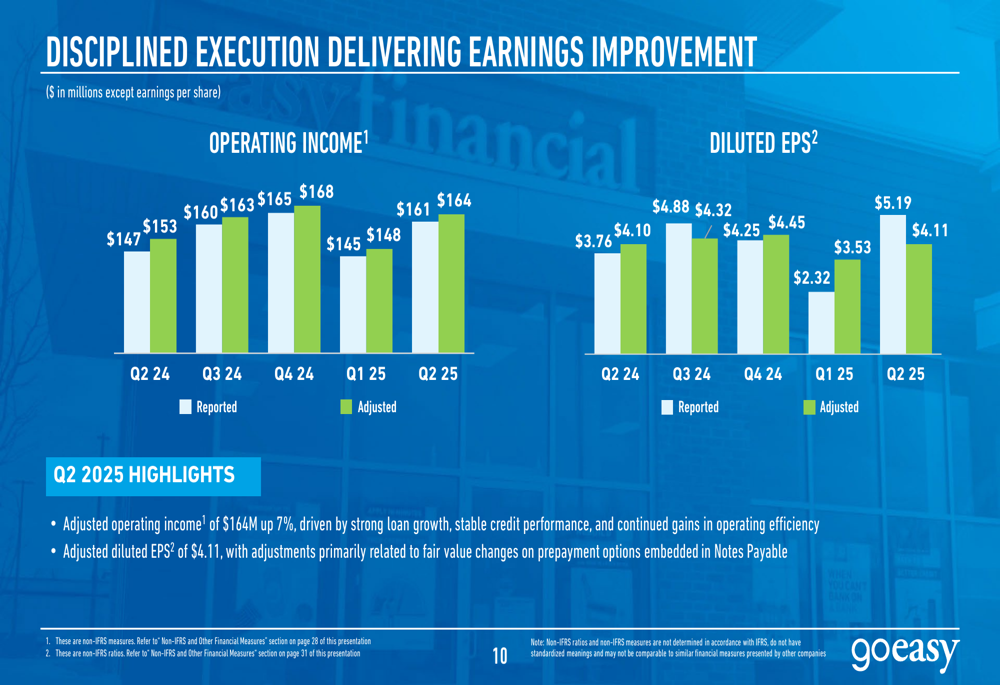

Profitability metrics showed mixed results, with reported net income of $86.5 million and diluted earnings per share of $5.19. Adjusted net income was $68.5 million, down 4% year-over-year, while adjusted diluted EPS remained relatively flat at $4.11 compared to $4.10 in Q2 2024. The adjusted figures primarily reflect fair value changes on prepayment options embedded in notes payable.

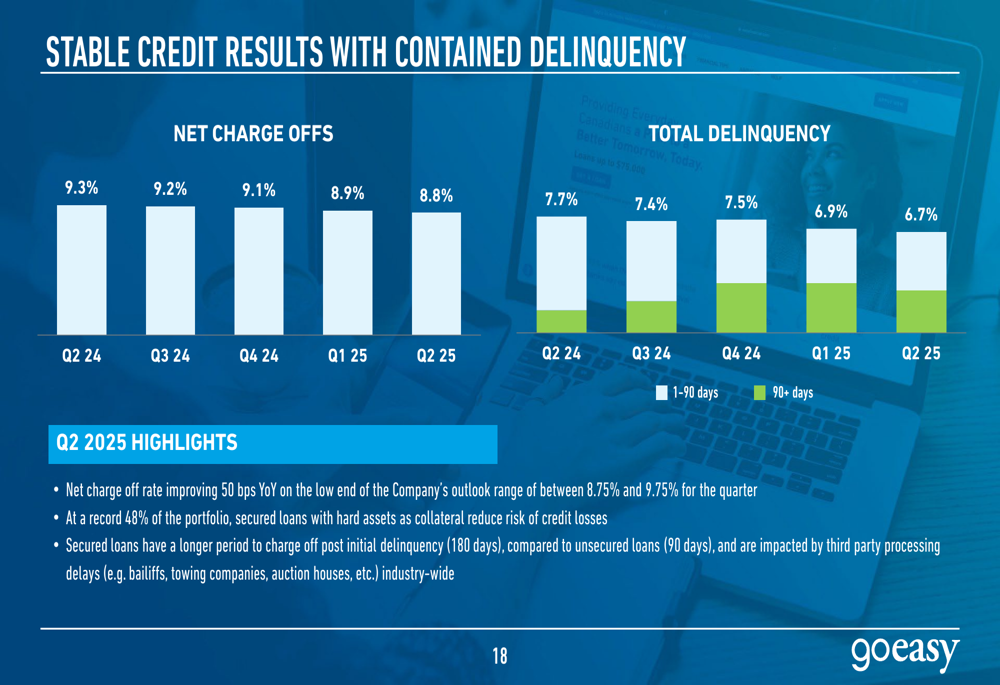

Credit performance remained stable, with the net charge-off rate improving to 8.8%, down 50 basis points year-over-year and at the low end of the company’s outlook range. This improvement reflects the company’s strategic shift toward secured lending, with secured loans now comprising 48% of the portfolio.

Strategic Initiatives

goeasy’s strategic focus on increasing the proportion of secured loans has been instrumental in managing credit risk while maintaining growth. The company has implemented targeted credit and underwriting enhancements, including selective reductions in loan-to-value ratios for home equity loans and adjustments to align with the new interest rate cap regulations.

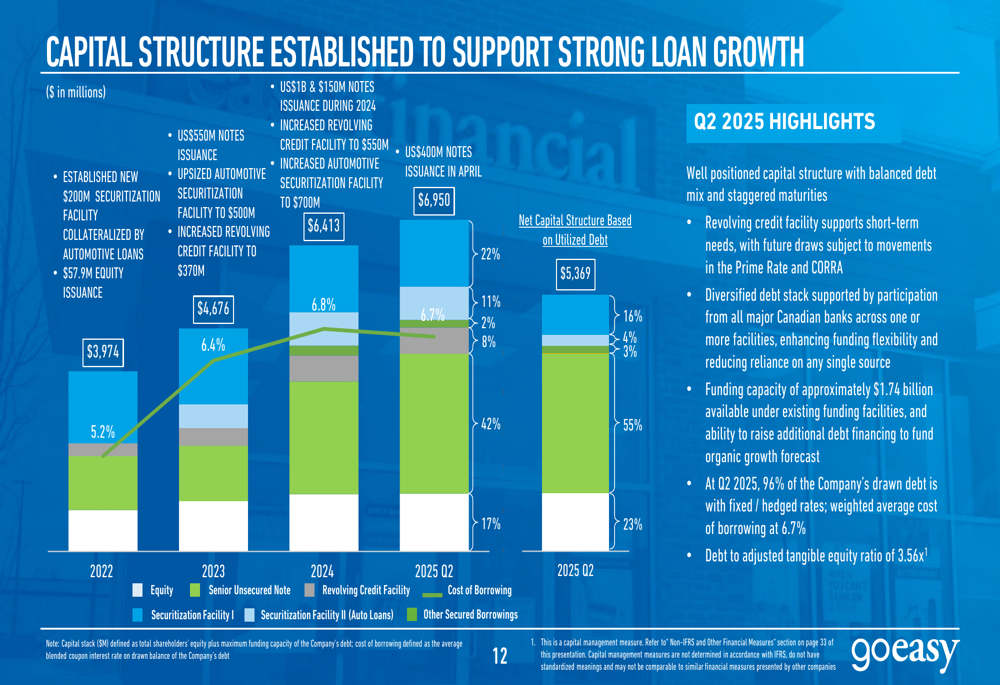

During the quarter, goeasy strengthened its liquidity position by issuing US$400 million of senior unsecured notes due October 2030, bringing its total funding capacity to approximately $1.74 billion. This robust capital structure positions the company well for continued growth.

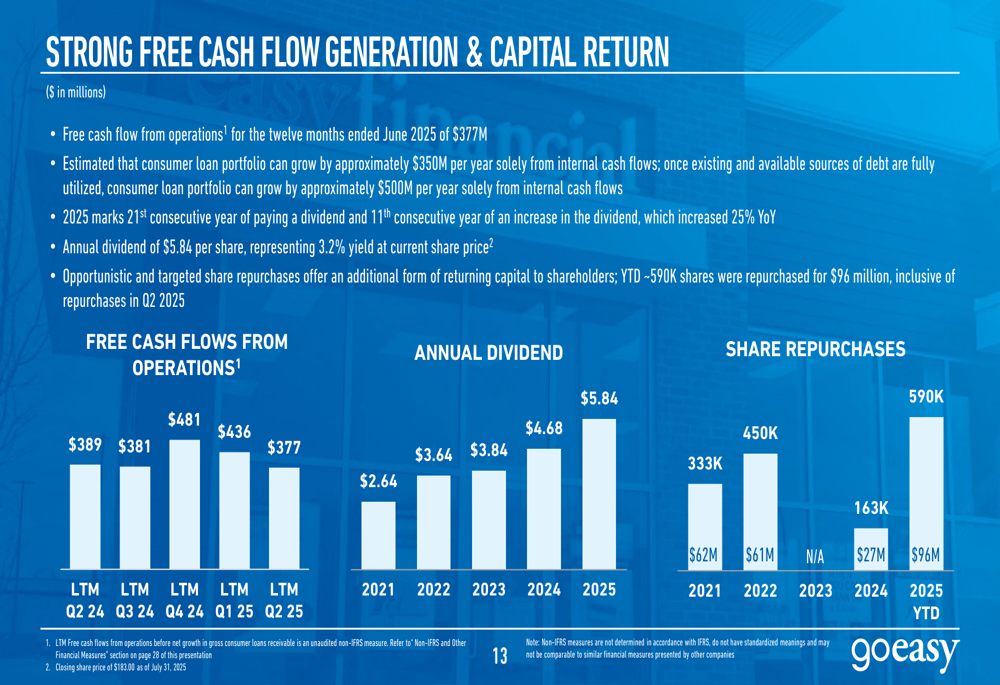

The company continues to generate strong free cash flow, which supports its capital return strategy. goeasy has increased its annual dividend to $5.84 per share, representing a 3.2% yield at the current share price. Additionally, the company has been active in share repurchases, buying back 590,000 shares for $96 million year-to-date.

Forward-Looking Statements

Looking ahead to Q3 2025, goeasy expects continued strong performance with gross consumer loan portfolio growth similar to Q2. The company anticipates maintaining a total yield on consumer loans between 31% and 32%, with net charge-offs between 8.75% and 9.75%.

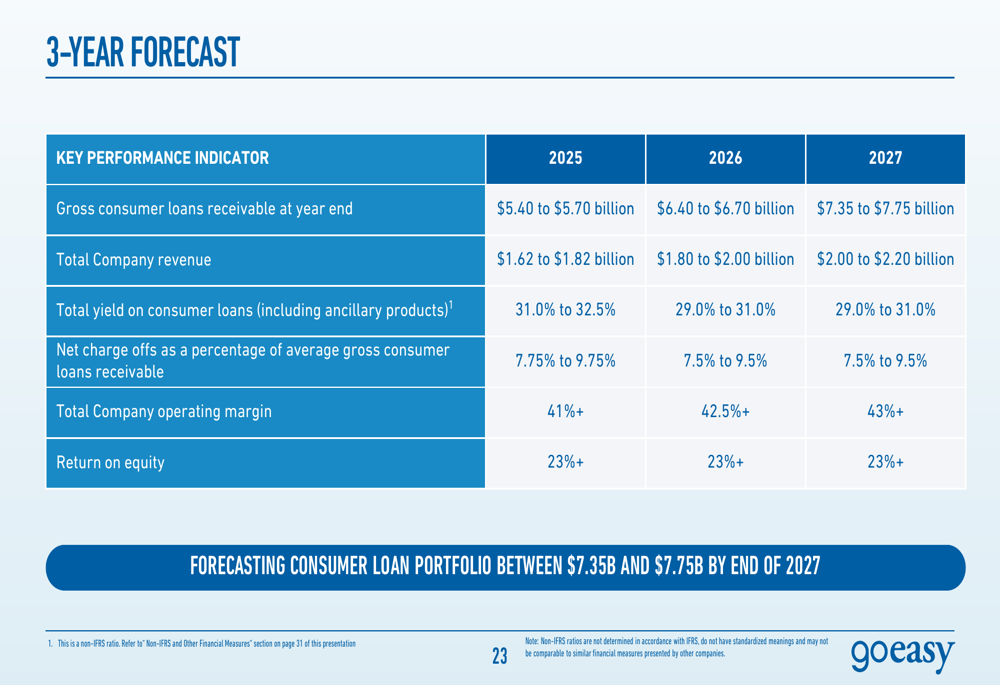

For the longer term, goeasy has reiterated its three-year forecast, projecting gross consumer loans receivable to reach between $7.35 billion and $7.75 billion by the end of 2027. This represents a compound annual growth rate of approximately 15% from current levels.

The company’s management indicated no major strategic shifts are expected under the new CEO, maintaining confidence in the current business model and growth trajectory. goeasy expects its gross consumer loans receivable for full-year 2025 to be at the top end of the $5.40 to $5.70 billion range.

Overall, goeasy’s Q2 2025 results demonstrate a strong recovery from Q1’s disappointing performance, with record loan growth and revenue highlighting the effectiveness of the company’s strategic focus on secured lending and operational efficiency. The company appears well-positioned to continue its growth trajectory while managing credit risk in the non-prime lending market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.