5 big analyst AI moves: Nvidia guidance warning; Snowflake, Palo Alto upgraded

Goodyear Tire & Rubber Co. (NYSE:NASDAQ:GT) presented its first quarter 2025 earnings results on May 8, showing declining sales and operating income amid challenging market conditions, while making progress on its transformation initiatives. The company’s stock closed at $11.01 on May 7, up 0.46% for the day, but was trading down 4% in the aftermarket following the release.

Quarterly Performance Highlights

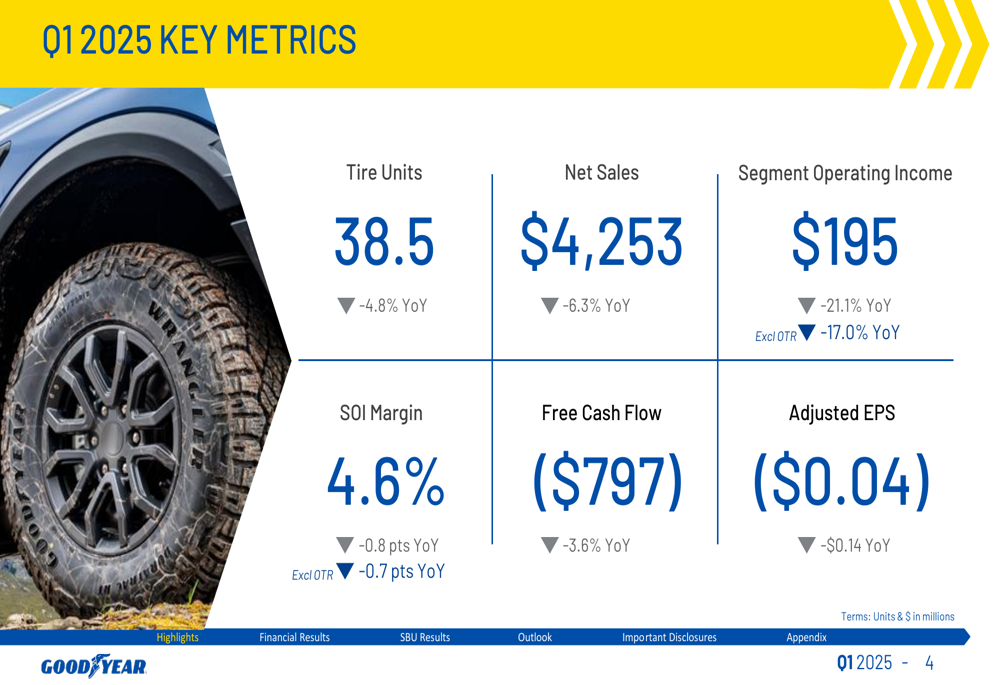

Goodyear reported first quarter net sales of $4,253 million, down 6.3% year-over-year, with tire unit volume declining 4.8% to 38.5 million units. Segment operating income fell 21.1% to $195 million, resulting in a segment operating margin of 4.6%, down 0.8 percentage points from the prior year.

As shown in the following comprehensive metrics overview:

Despite the operating income decline, Goodyear reported net income of $115 million for the quarter, a significant improvement from a net loss of $57 million in Q1 2024. However, adjusted earnings per share came in at negative $0.04, compared to positive $0.10 in the prior-year period.

The company’s free cash flow was negative $797 million, slightly worse than the negative $769 million reported in the same period last year, reflecting typical first quarter seasonal patterns.

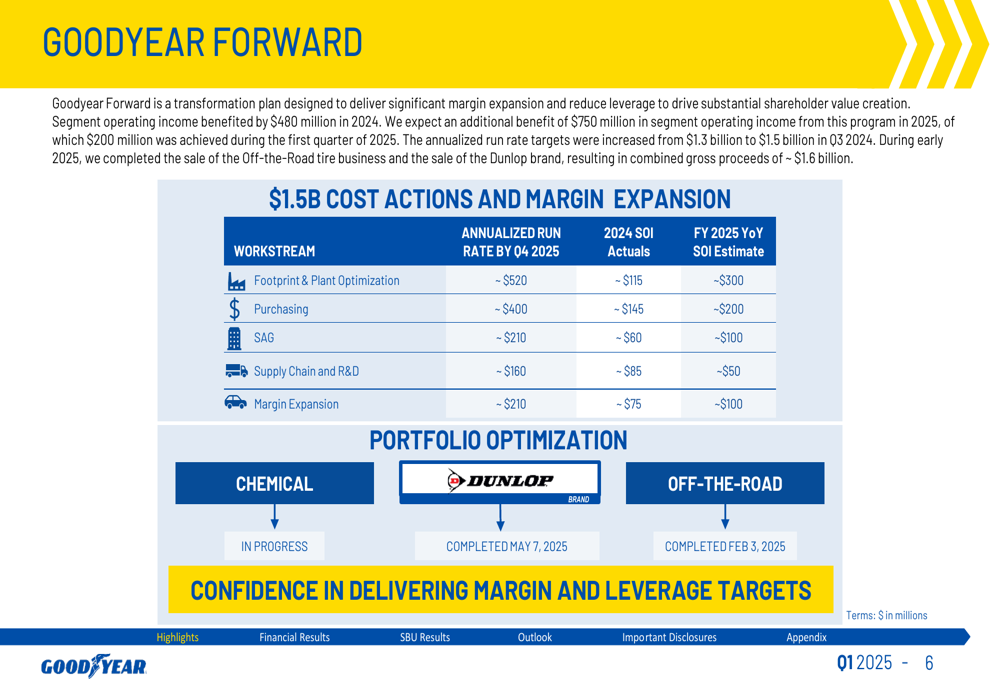

Goodyear Forward Transformation Progress

A key highlight of the quarter was the completion of the Dunlop brand sale, which generated $735 million in gross proceeds. This transaction, along with the previously completed Off-the-Road business sale, represents significant progress in Goodyear’s transformation strategy.

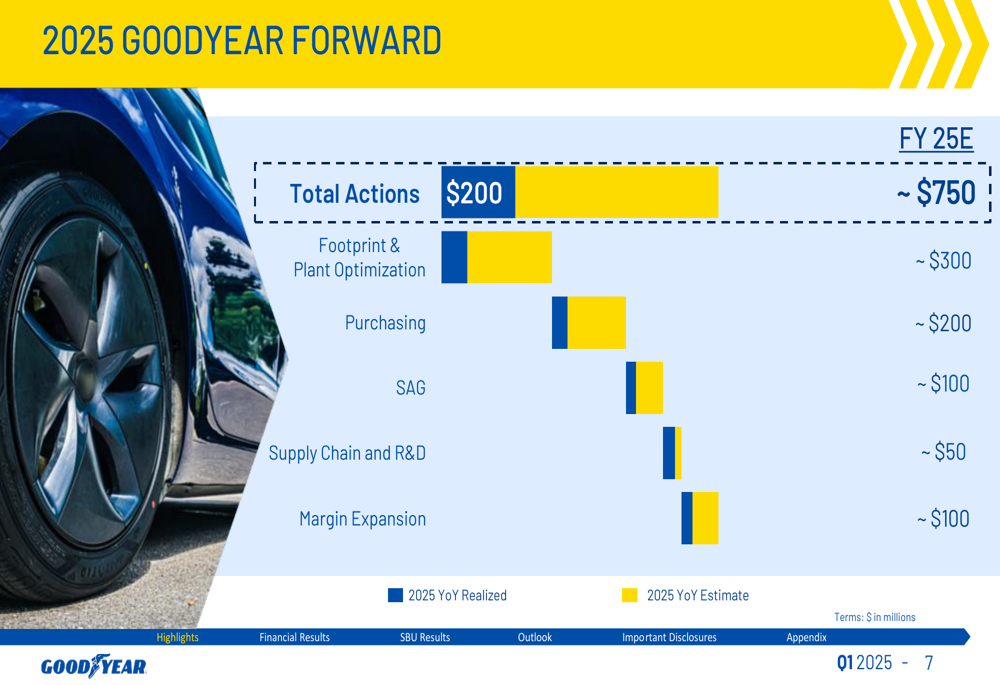

The company’s Goodyear Forward program delivered $200 million in benefits during the quarter, helping to offset headwinds from raw material costs, inflation, and lower volumes. The program encompasses multiple workstreams targeting cost reduction and margin expansion:

The company reaffirmed its targets for the Goodyear Forward initiative, which aims to deliver approximately $750 million in benefits for the full year 2025:

Regional Performance Analysis

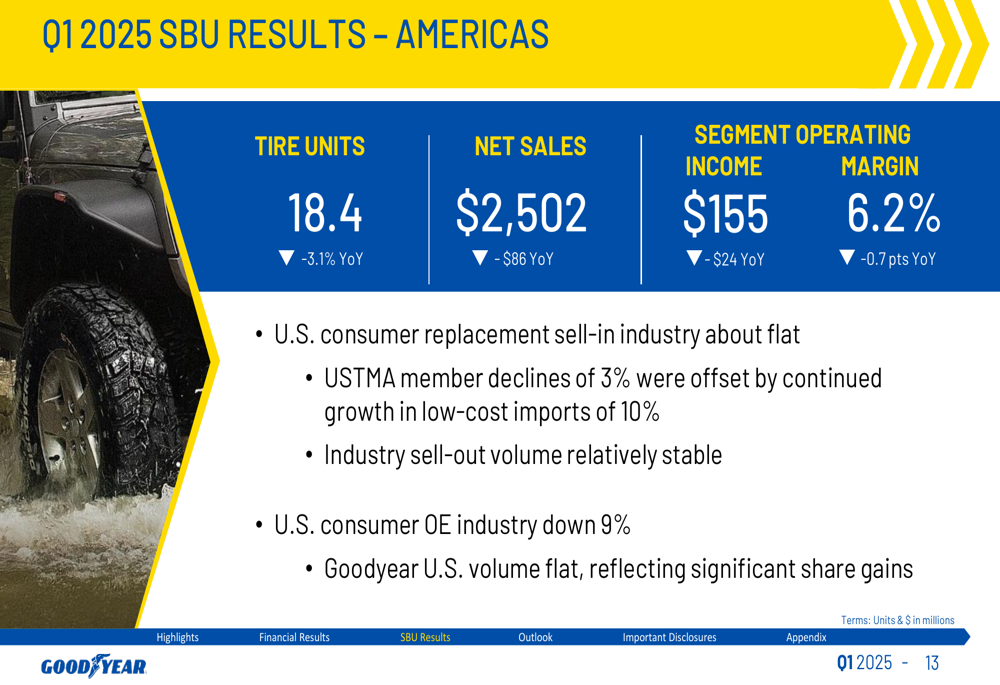

Goodyear’s performance varied significantly across regions, with the Americas delivering the strongest results despite challenging conditions.

The Americas segment reported net sales of $2,502 million, down $86 million year-over-year, with segment operating income of $155 million and a margin of 6.2%, down 0.7 percentage points. The U.S. consumer replacement market was approximately flat, while the OE industry declined 9%:

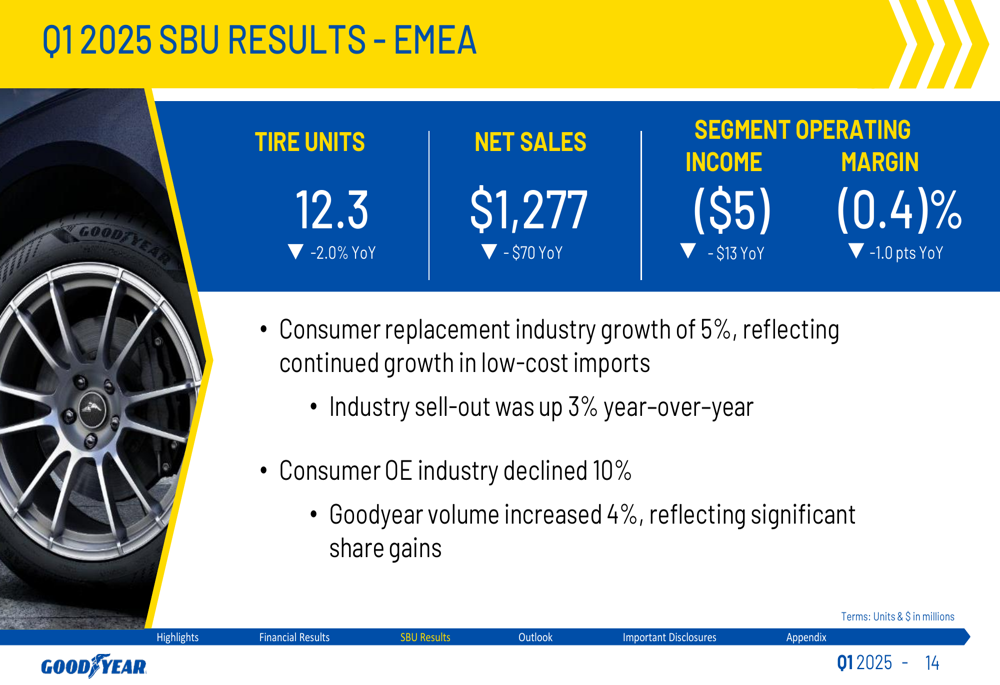

EMEA (Europe, Middle East, and Africa) faced more significant challenges, reporting a segment operating loss of $5 million and a negative margin of 0.4%, despite consumer replacement industry growth of 5%:

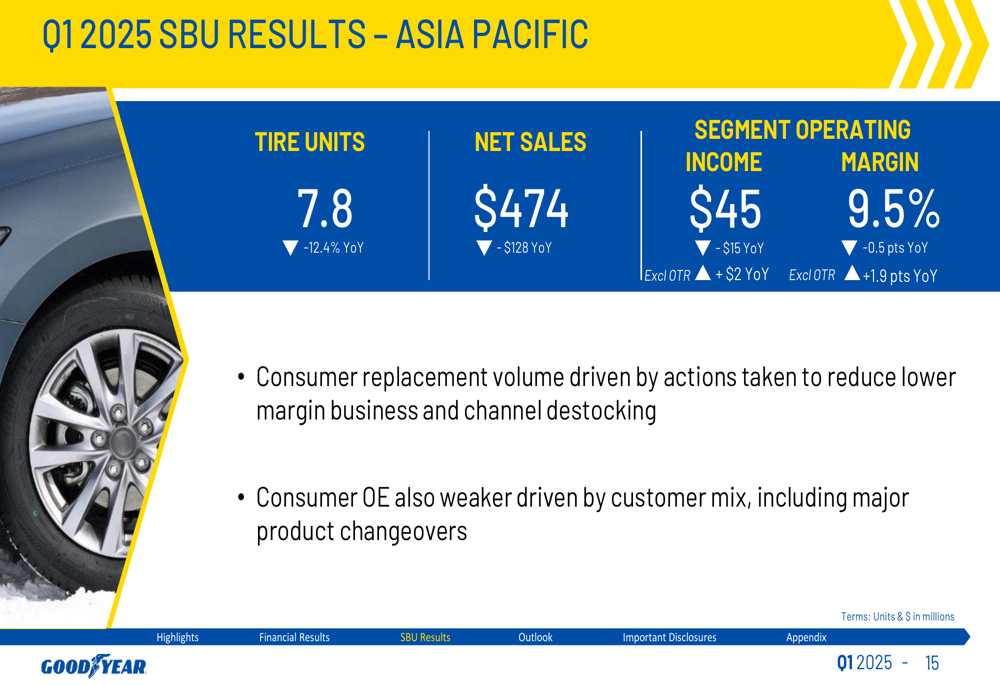

Asia Pacific reported net sales of $474 million, down $128 million year-over-year, with segment operating income of $45 million and a margin of 9.5%. The region was impacted by actions to reduce lower-margin business and channel destocking:

Financial Position and Debt Management

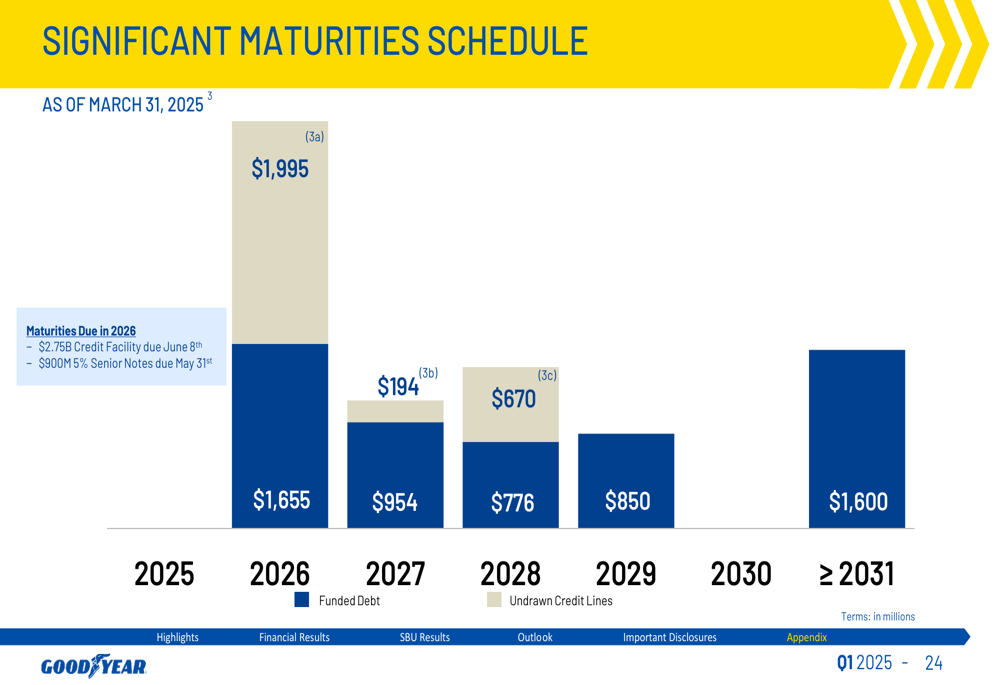

Goodyear has made progress in reducing its debt burden, with pro forma total debt of $7,363 million as of March 31, 2025, down 10.9% year-over-year. Net debt decreased 12.4% to $6,461 million on a pro forma basis, reflecting the planned repayment of $675 million of third-party debt following the Dunlop brand sale.

The company’s debt maturity schedule shows significant obligations coming due in the next few years, highlighting the importance of continued focus on debt reduction:

Outlook and Forward-Looking Statements

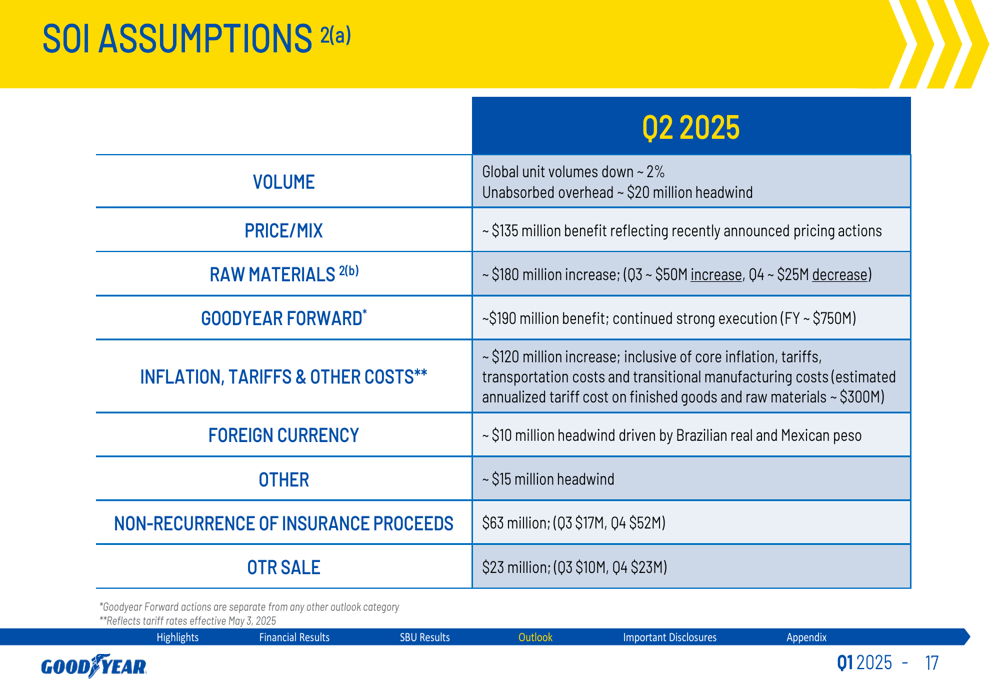

For the second quarter of 2025, Goodyear expects continued challenges, with global unit volumes projected to decline approximately 2%. Raw material costs are expected to increase by approximately $180 million, while the Goodyear Forward program is anticipated to deliver approximately $190 million in benefits:

For the full year 2025, the company provided industry assumptions of -2% to 2% for both consumer and commercial tire markets. Goodyear noted that U.S. volatility related to imports/prebuy and trade uncertainty is impacting global demand, with commercial demand recovery expected later in the second half of the year.

The company expects to generate approximately $50 million in working capital inflow for the year and plans capital expenditures of $950 million. Additionally, Goodyear anticipates approximately $70 million of gross proceeds from land sales and other real estate transactions.

Despite the challenging start to the year, Goodyear’s transformation initiatives and strategic actions position the company to navigate the current market environment while working toward its longer-term financial objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.