Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Indonesian tech giant GoTo Gojek Tokopedia PT (IDX:GOTO) has released its first quarter 2025 results, showcasing significant improvements in profitability while maintaining strong growth across its business segments. The company, which operates ride-hailing, e-commerce, and financial technology services, reported a substantial turnaround in its Adjusted EBITDA figures, with all major business units now operating in positive territory.

The results come as Indonesia’s digital economy continues to expand, with increased adoption of digital payment solutions and on-demand services. GoTo’s stock has responded positively to the improved performance, with shares up 3.66% to IDR 82 following the presentation.

Quarterly Performance Highlights

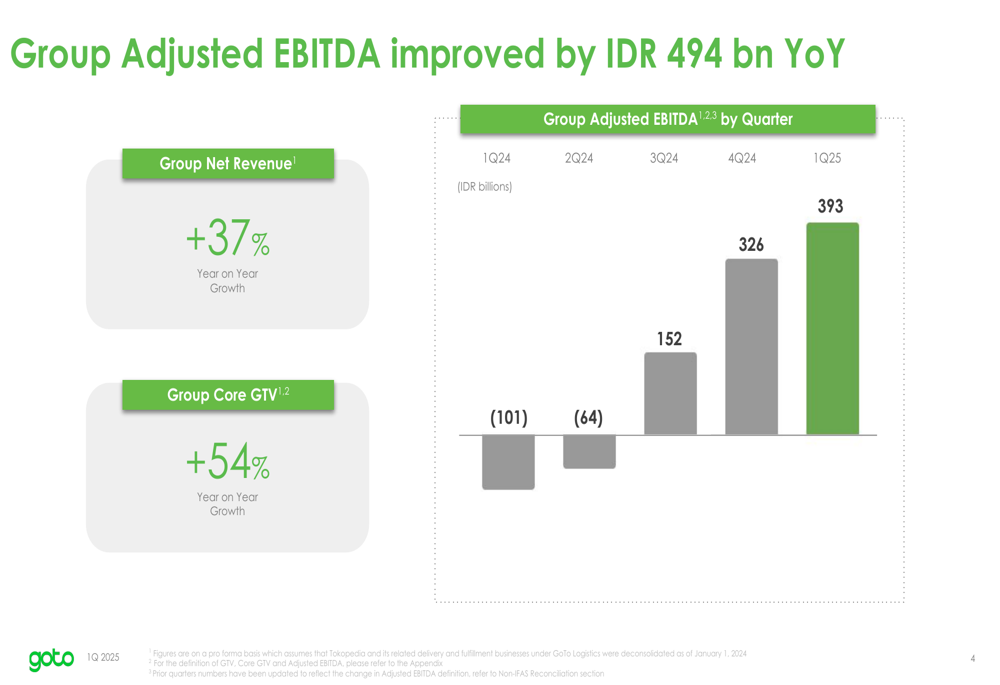

GoTo reported a Group Adjusted EBITDA improvement of IDR 494 billion year-over-year, reaching IDR 393 billion in Q1 2025. This marks a significant turnaround from the IDR 101 billion loss in the same period last year. The company achieved this while growing Group Net Revenue by 37% and Group Core GTV (Gross Transaction (JO:NTUJ) Value) by 54% year-over-year.

As shown in the following chart of quarterly Group Adjusted EBITDA progression:

The company’s overall financial position remains strong, with a cash balance of IDR 21 trillion (USD 1.3 billion) as of March 2025. GoTo has also continued its share buyback program, with IDR 1.6 trillion (USD 99 million) in repurchases completed by the end of the quarter, out of a total approved program of USD 200 million.

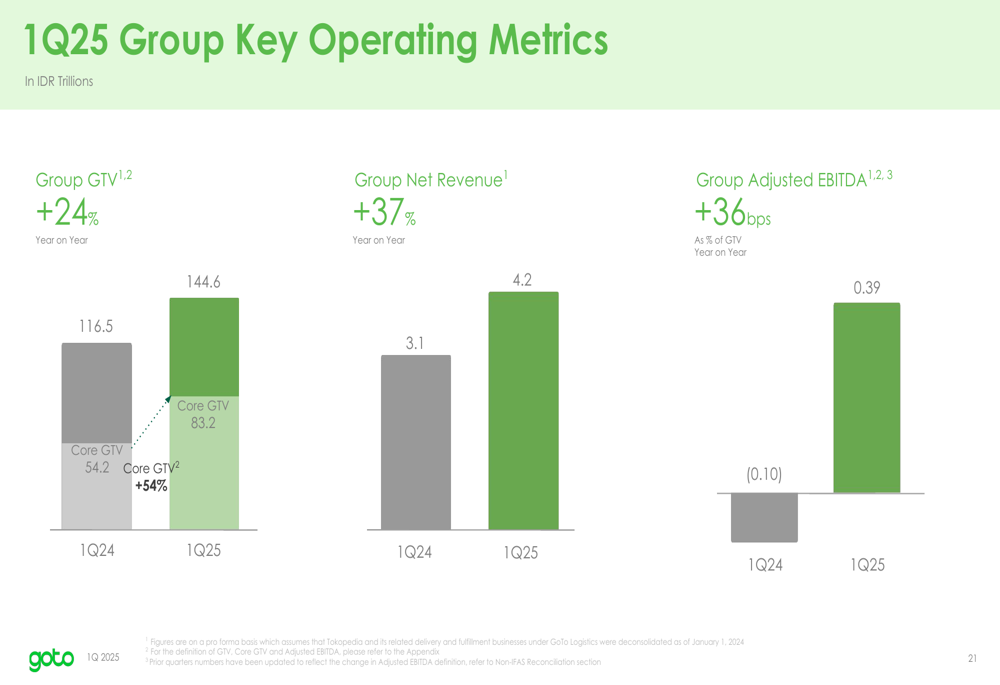

The following slide summarizes the key operating metrics for the Group in Q1 2025:

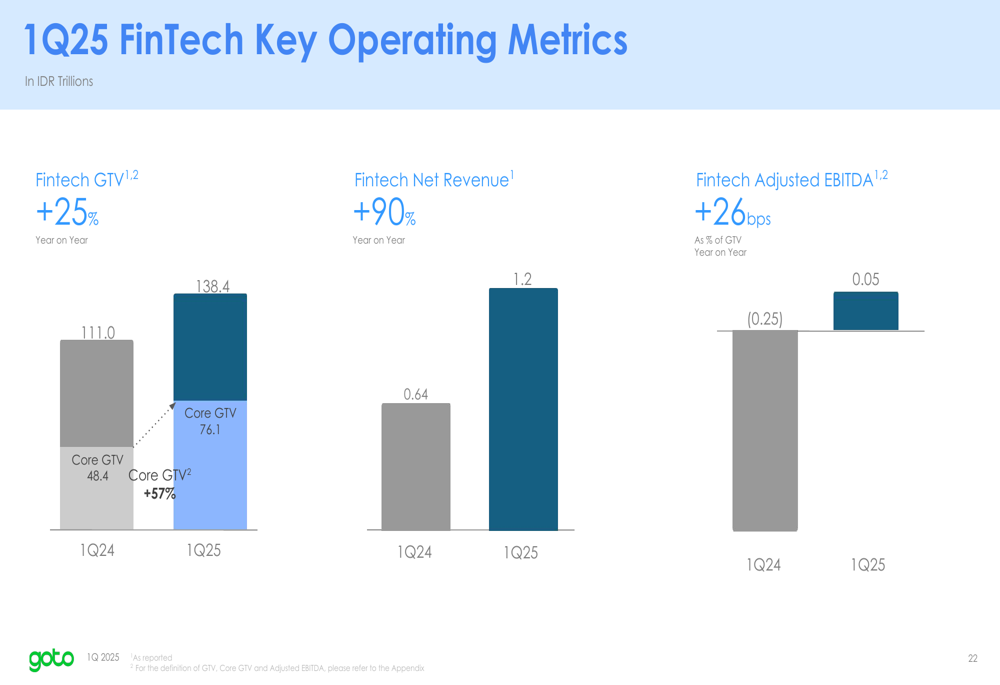

FinTech Segment Growth

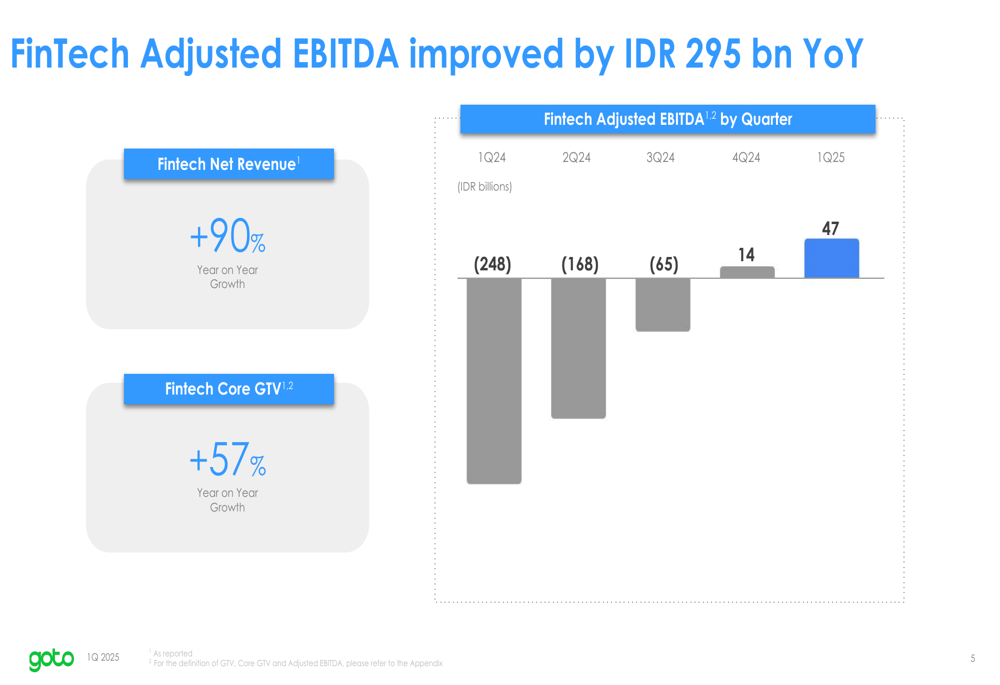

The FinTech segment emerged as a standout performer, with Net Revenue surging 90% year-over-year and Core GTV growing by 57%. The segment achieved positive Adjusted EBITDA of IDR 47 billion in Q1 2025, a remarkable improvement from the IDR 248 billion loss recorded in Q1 2024.

The company’s FinTech performance is illustrated in this progression chart:

GoTo’s lending business has shown particularly strong growth, with total consumer loans outstanding reaching IDR 5.7 trillion, representing a 108% increase year-over-year. The company emphasized its focus on prudent risk management through a tech-driven operating model, integrated ecosystem, and robust data-driven framework.

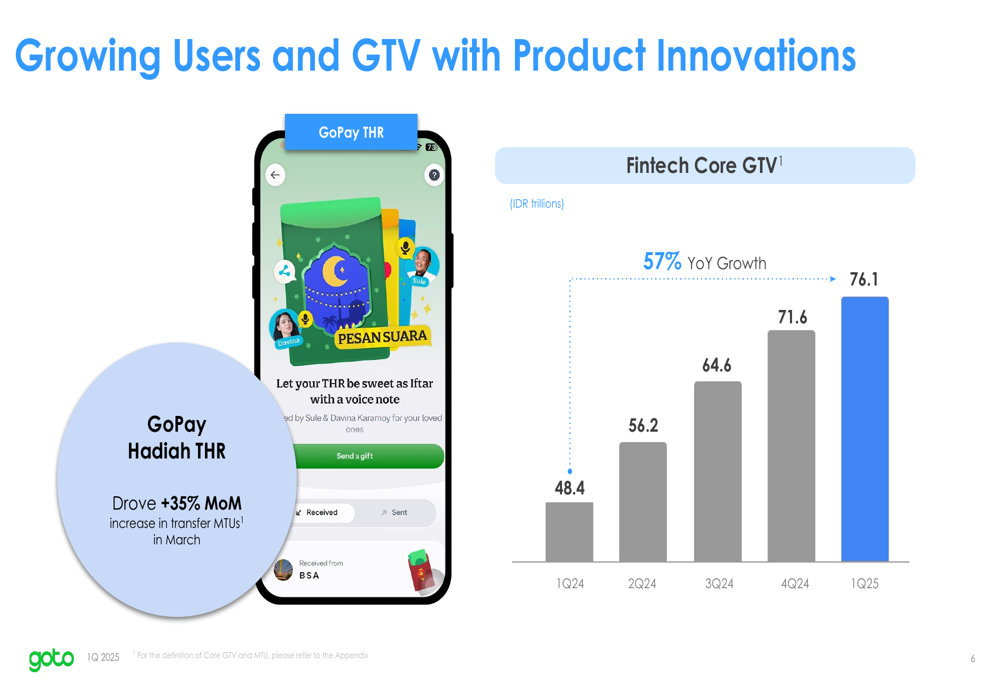

As shown in the following chart of FinTech GTV growth:

Monthly Transacting Users (MTUs) in the FinTech segment reached 20.6 million in Q1 2025, growing 30% year-over-year. Product innovations like GoPay Hadiah THR (festive bonus transfer) drove a 35% month-on-month increase in transfer MTUs in March.

The key operating metrics for the FinTech segment are summarized in this slide:

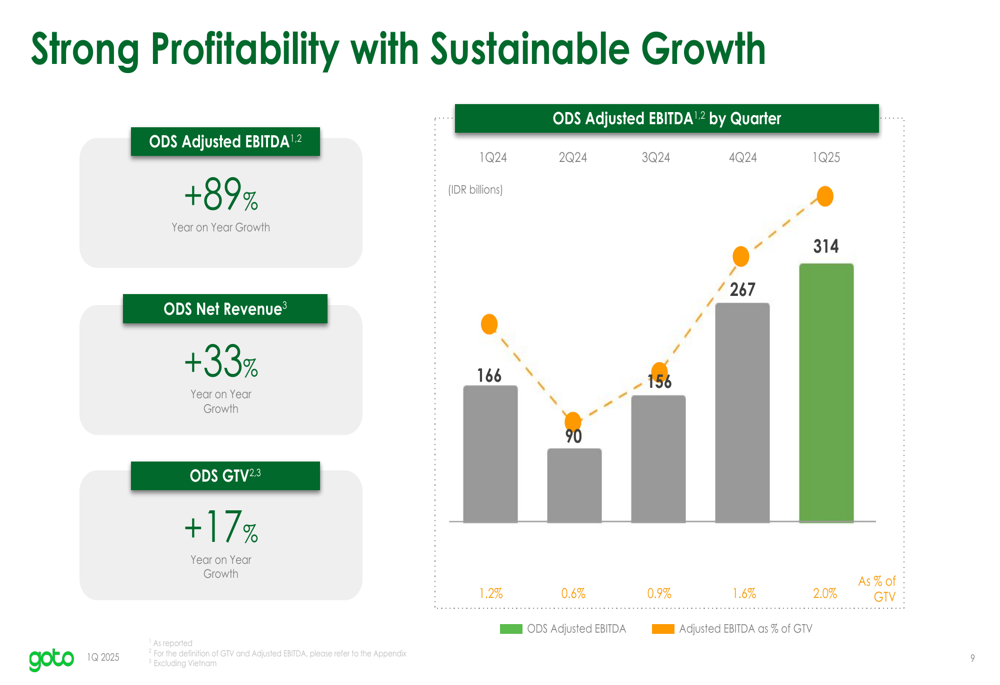

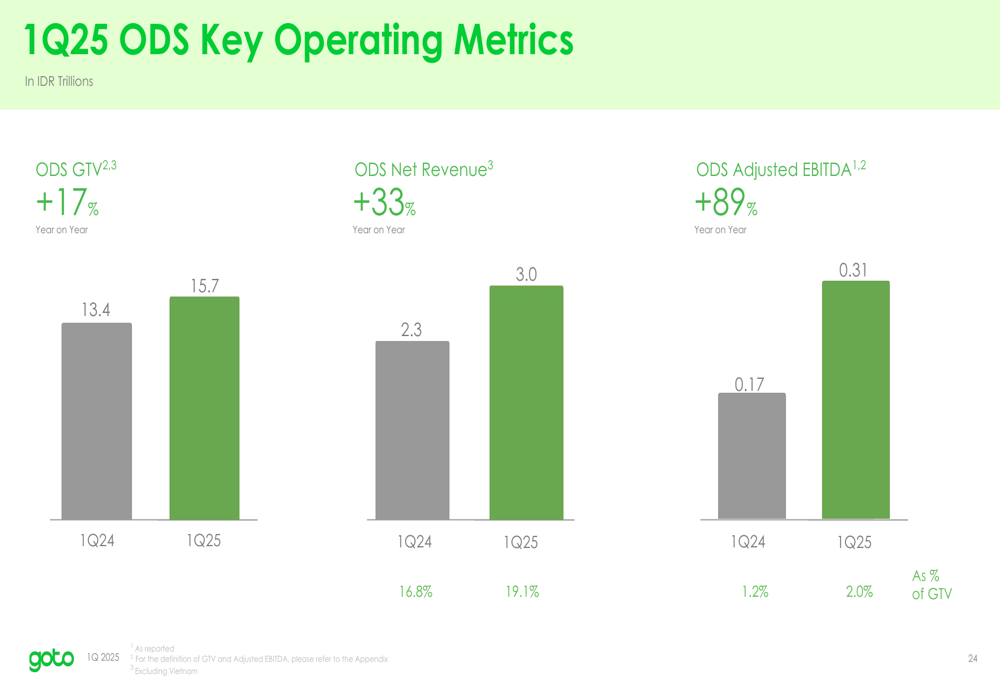

On-Demand Services Performance

The On-Demand Services (ODS) segment, which includes Mobility and Delivery, demonstrated strong profitability with sustainable growth. ODS Adjusted EBITDA grew by 89% year-over-year to IDR 314 billion, with Adjusted EBITDA as a percentage of GTV improving to 2.0% in Q1 2025 from 1.2% in Q1 2024.

The following chart illustrates the consistent improvement in ODS profitability:

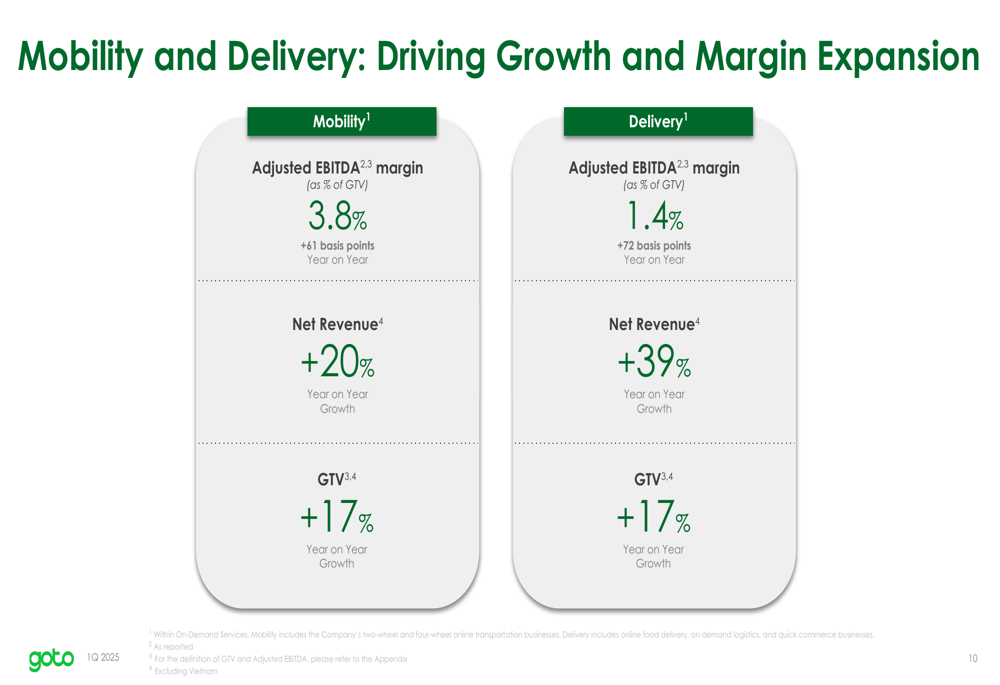

Breaking down the ODS segment, Mobility achieved an Adjusted EBITDA margin of 3.8% (up 61 basis points year-over-year) with Net Revenue growth of 20%. Meanwhile, Delivery reached an Adjusted EBITDA margin of 1.4% (up 72 basis points year-over-year) with impressive Net Revenue growth of 39%.

The performance comparison between Mobility and Delivery is shown in this slide:

The company’s ODS segment key metrics are summarized in the following slide:

Strategic Initiatives

GoTo highlighted several strategic initiatives driving its improved performance. The company has been optimizing incentive spending through enhanced engineering, analytics, and refined targeting capabilities, focusing on users who are most responsive to promotions.

The company has also been expanding its premium service offerings, with Mobility Premium Completed Orders growing 156% year-on-year and Food Express increasing its share of total food GTV for the fifth consecutive quarter.

Advertising has emerged as a significant profitability driver, with revenue increasing 45% year-on-year. Advertising now makes up 1.7% of Total (EPA:TTEF) Food GMV as of Q1 2025, up from 1.3% in Q1 2024.

The following slide illustrates the company’s advertising initiatives:

Merchant-funded promotions have also seen increased participation, with merchants’ total spend growing by more than 150% year-over-year in Q1 2025. The company attributes this to enhanced targeting and segmentation capabilities that improve customer reach.

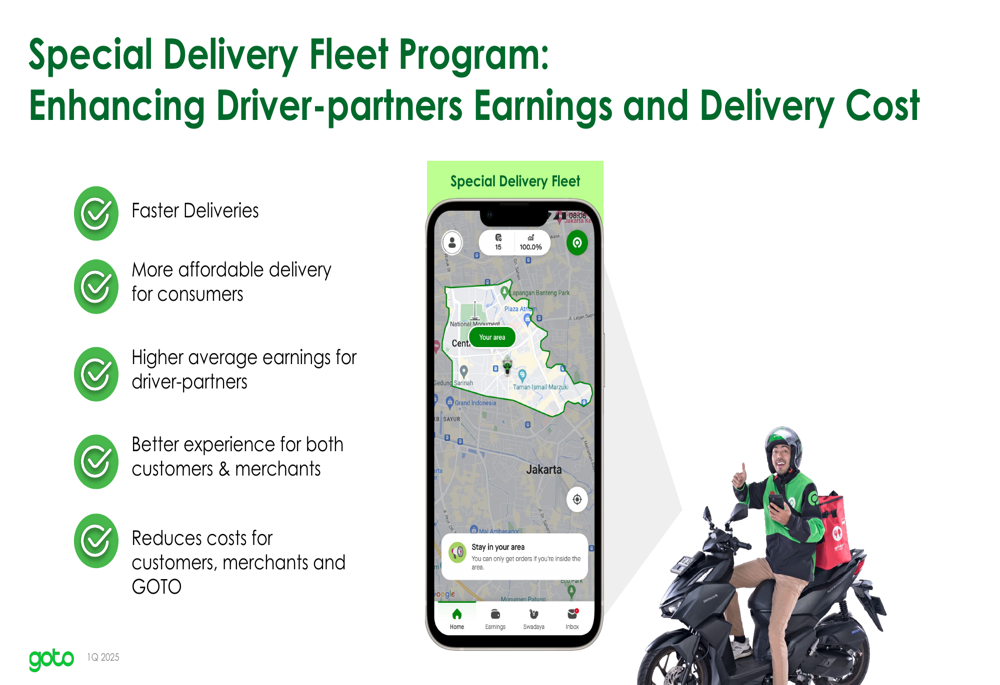

GoTo’s Special Delivery Fleet Program is another initiative aimed at improving operational efficiency, offering faster and more affordable deliveries for consumers while increasing average earnings for driver-partners.

Forward-Looking Statements

Looking ahead, GoTo provided guidance for FY25 Group Adjusted EBITDA in the range of IDR 1.4-1.6 trillion. The company plans to continue optimizing incentive spending as a percentage of GTV while maintaining healthy growth throughout 2025.

The company also noted the seasonal impact of the fasting period across its business lines, with varying effects on Mobility (decreased intra-city travel), Delivery (decreased food delivery during the day), Lending (reduced borrowing due to seasonal bonuses), and Payments (increased activity).

GoTo continues to invest in artificial intelligence through its Sahabat-AI large language model, which the company says is gathering pace with more partners joining the ecosystem and more use cases being developed, both internally and externally.

With all segments now contributing positively to Adjusted EBITDA and strong growth across the business, GoTo appears well-positioned to continue its profitability trajectory while maintaining its leadership position in Indonesia’s digital economy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.