Sana Biotechnology stock higher after Eric Jackson touts 100-bagger potential

Introduction & Market Context

WW Grainger Inc. (NYSE:GWW) presented its second-quarter 2025 earnings results on August 1, revealing solid sales growth but facing significant margin pressure from tariff challenges. The industrial supply company’s stock plunged 11.02% in pre-market trading to $925, reflecting investor concerns about the company’s reduced profit guidance despite higher sales projections.

The company reported quarterly sales of $4.6 billion, representing a 5.1% increase on a daily, constant currency basis. However, operating margin contracted by 50 basis points to 14.9%, and the company lowered its full-year profit outlook due to tariff-related headwinds.

Quarterly Performance Highlights

Grainger delivered diluted earnings per share of $9.97 in Q2 2025, a modest 2.2% increase from the prior year. The company’s return on invested capital (ROIC) declined by 230 basis points to 40.3%, while still maintaining strong shareholder returns with $336 million distributed through dividends and share repurchases during the quarter.

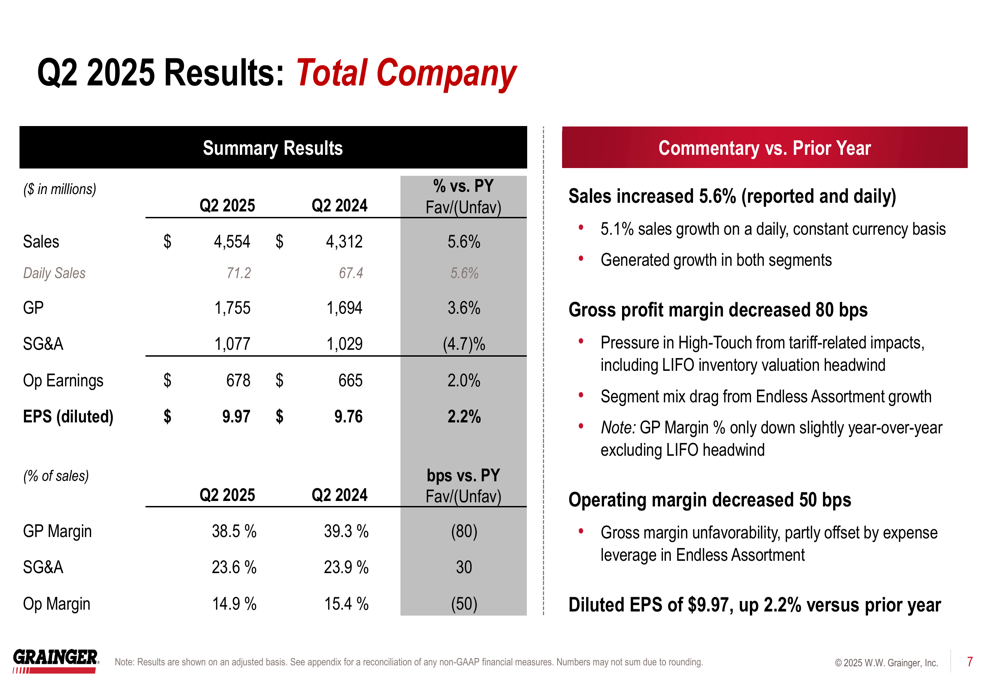

As shown in the following comprehensive results summary:

Total (EPA:TTEF) company sales reached $4.55 billion, up 5.6% compared to Q2 2024. Gross profit increased 3.6% to $1.76 billion, though gross profit margin contracted 80 basis points to 38.5%. SG&A expenses were well controlled, decreasing 4.7% to $1.08 billion, which helped partially offset the gross margin decline.

Segment Analysis

Grainger’s performance varied significantly across its business segments, with Endless Assortment showing remarkable growth while the larger High-Touch Solutions segment delivered more modest results.

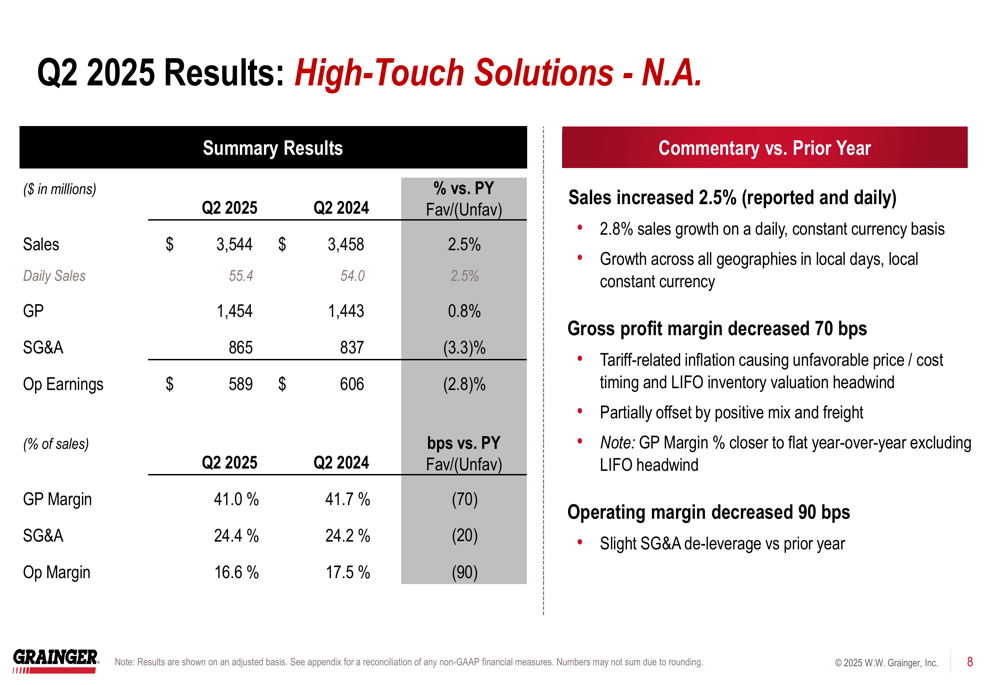

The High-Touch Solutions North America segment, which includes the company’s U.S. and Canadian operations, reported sales of $3.54 billion, up 2.5% year-over-year. However, operating margin in this segment declined 90 basis points to 16.6%, as illustrated in the segment breakdown:

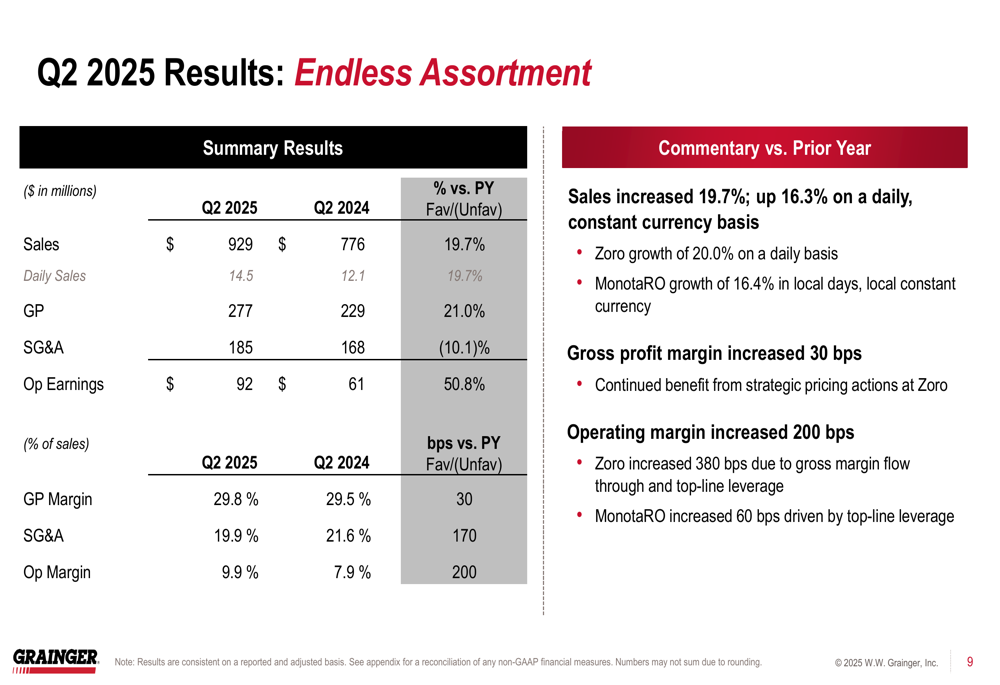

By contrast, the Endless Assortment segment, which includes MonotaRO and Zoro, demonstrated exceptional growth with sales increasing 19.7% to $929 million. More impressively, this segment expanded operating margin by 200 basis points to 9.9%, showing strong operational leverage as it scales:

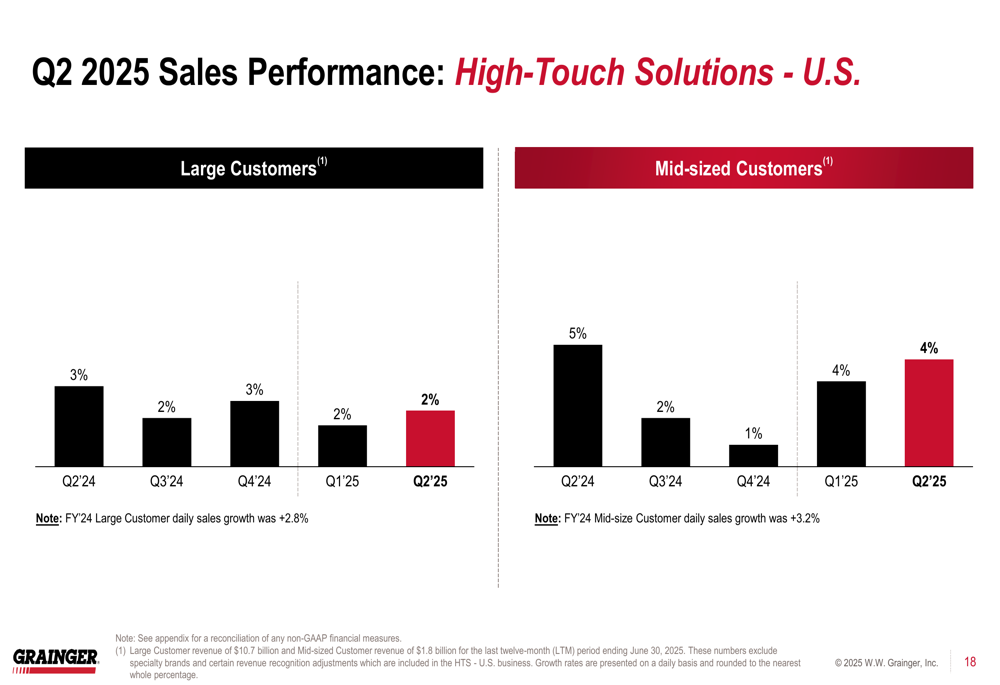

Further analysis of the High-Touch Solutions segment reveals different growth rates by customer size, with mid-sized customers growing faster than large customers:

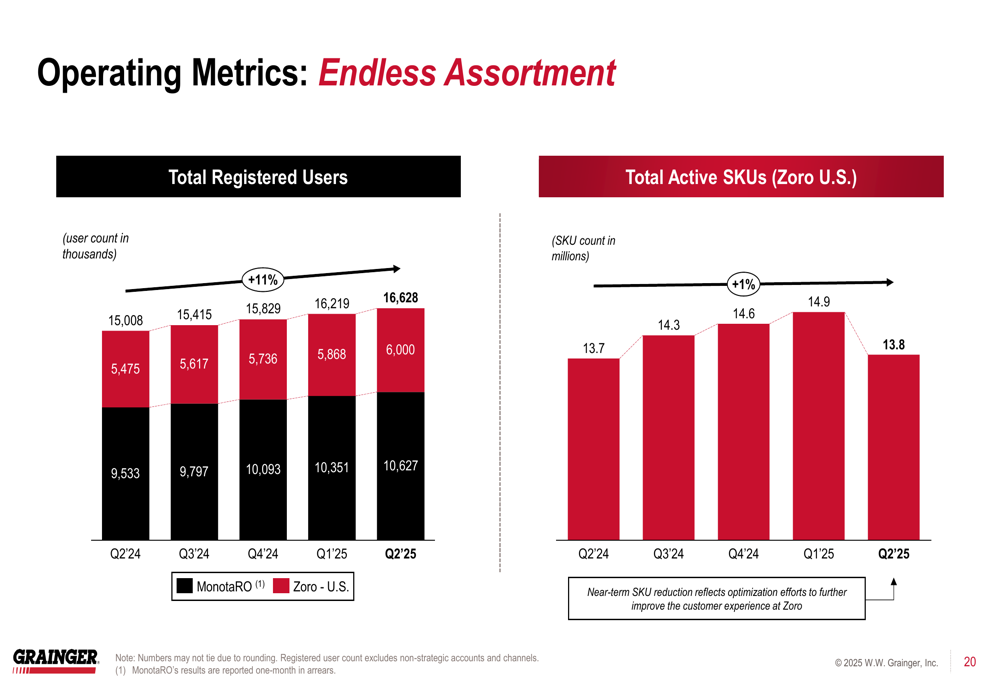

The Endless Assortment segment continues to expand its reach, with total registered users reaching 16,628 and active SKUs growing to 13.8 million, demonstrating the platform’s increasing scale and customer engagement:

Tariff Impact & Mitigation Strategy

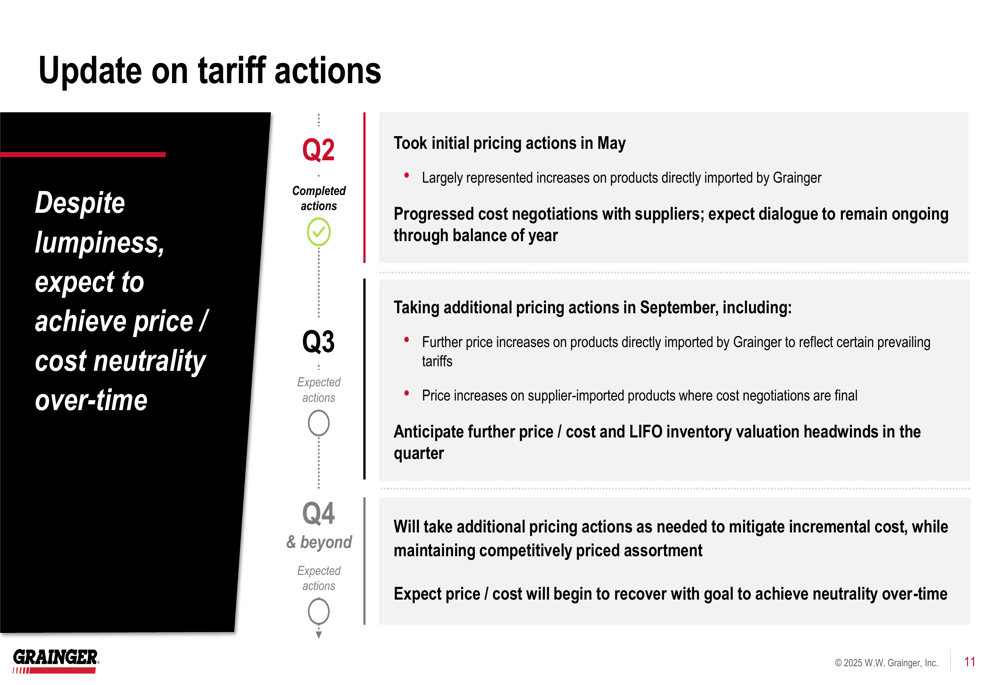

A significant focus of Grainger’s presentation was its approach to managing tariff challenges. The company outlined a phased strategy to address these headwinds, beginning with initial pricing actions in May 2025 and continuing with further adjustments planned for September.

As detailed in the company’s tariff action timeline:

Grainger has already implemented price increases on directly imported products and is progressing with supplier cost negotiations. The company plans additional price increases in September on both directly imported products and supplier-imported items. Management expects to achieve price-cost neutrality over time, though near-term headwinds are anticipated in Q3 and Q4.

Updated 2025 Guidance

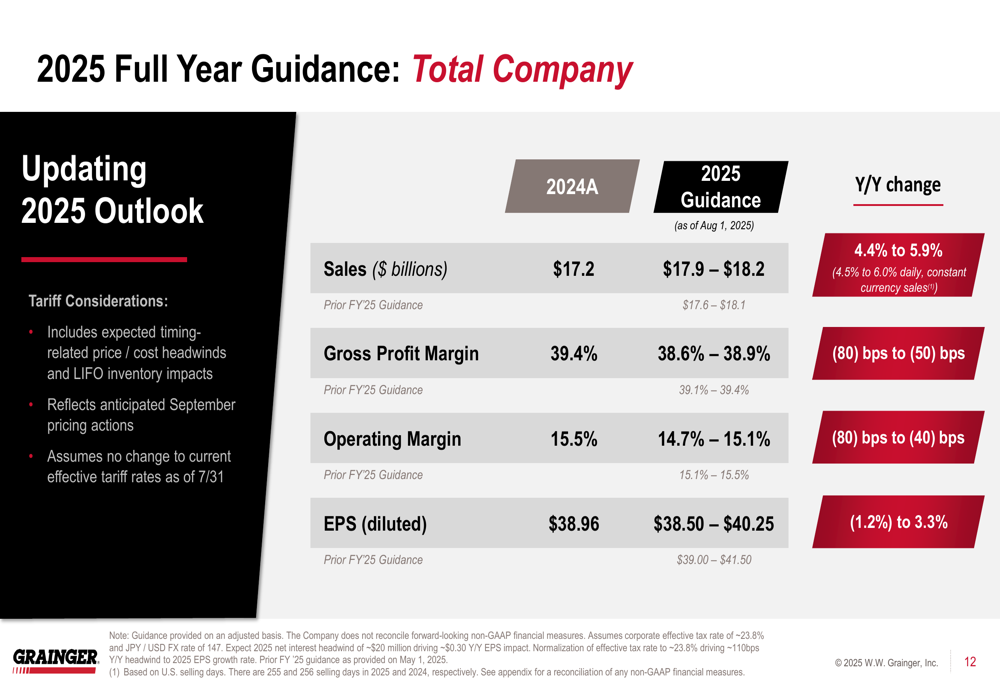

Despite the tariff challenges, Grainger actually raised its full-year sales guidance while lowering profit projections. The updated outlook reflects the company’s confidence in continued sales momentum but acknowledges margin pressure from tariffs:

The revised guidance projects sales of $17.9-18.2 billion (previously $17.6-18.1 billion), representing growth of 4.4% to 5.9%. However, gross profit margin is now expected to be 38.6-38.9%, down from the previous range of 39.1-39.4%. Similarly, operating margin guidance was lowered to 14.7-15.1% from 15.1-15.5%.

Most notably, diluted EPS guidance was reduced to $38.50-40.25 from the previous range of $39.00-41.50, reflecting the anticipated impact of tariff-related costs that haven’t yet been fully offset by pricing actions.

Market Reaction & Conclusion

The significant pre-market stock decline of 11.02% to $925 suggests investors are focusing on the reduced profit guidance rather than the sales growth. This reaction comes despite Grainger’s Q2 2025 results showing solid overall performance, particularly in the fast-growing Endless Assortment segment.

The market appears concerned about the company’s ability to fully offset tariff impacts through pricing actions, especially given the competitive nature of the industrial supply market. While Grainger maintains strong fundamentals with a 40.3% ROIC and continues to return capital to shareholders, the near-term profit outlook has clearly dampened investor sentiment.

Management’s strategy of phased pricing actions and supplier negotiations will be crucial to watch in coming quarters, as will the continued momentum in the Endless Assortment segment, which represents a significant growth engine for the company despite being a smaller portion of overall revenue.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.