Tonix Pharmaceuticals stock halted ahead of FDA approval news

Gran Tierra Energy Inc. (NASDAQ:NYSE:GTE) presented its May 2025 corporate strategy, highlighting its transformation into a geographically diversified oil and gas producer following its strategic Canadian acquisition. Despite recent stock weakness, the company emphasized its strengthened reserve base and plans for debt reduction while maintaining shareholder returns.

Executive Summary

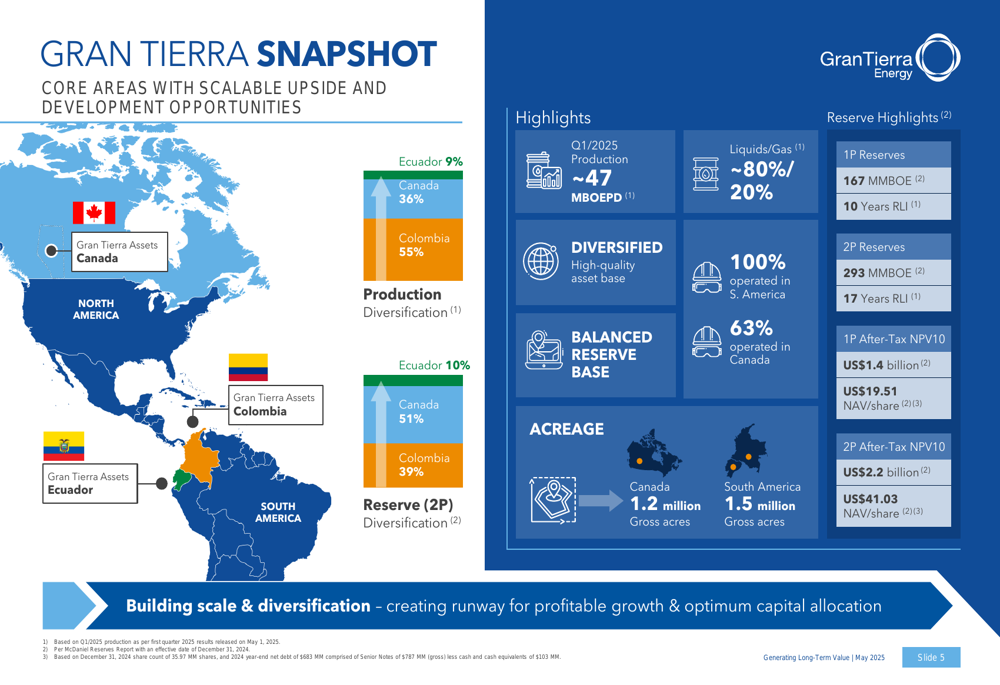

Gran Tierra’s presentation showcased its evolution into a diversified producer operating across Colombia (55%), Canada (36%), and Ecuador (9%). The company reported Q1/2025 production of approximately 47,000 barrels of oil equivalent per day (BOEPD), with an 80/20 liquids-to-gas ratio. Management emphasized the company’s strong reserve position, with 167 million BOE of 1P reserves (10-year reserve life) and 293 million BOE of 2P reserves (17-year reserve life).

As shown in the following snapshot of Gran Tierra’s portfolio diversification and key metrics:

Despite these positive developments, Gran Tierra’s stock has recently underperformed, dropping 11.64% following its Q4 2024 earnings announcement. While the company achieved a net income of $3 million in Q4 2024 (compared to a $6.3 million loss in Q4 2023), adjusted EBITDA decreased 8% to $367 million for the full year, potentially contributing to investor caution.

Portfolio Diversification Strategy

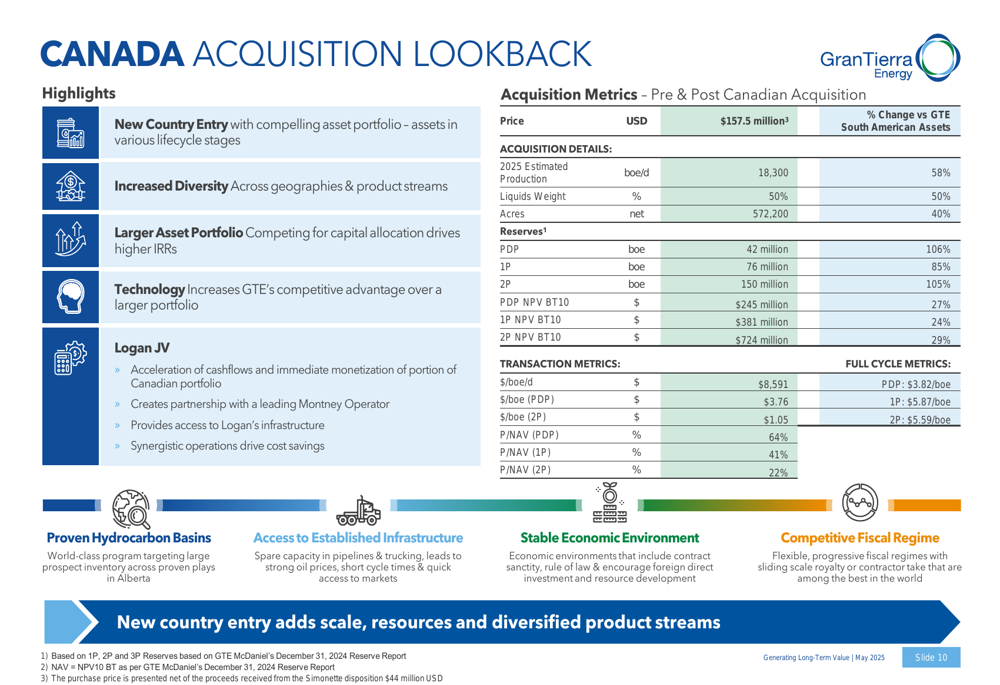

The centerpiece of Gran Tierra’s strategy is its recent Canadian acquisition, which has significantly reshaped its portfolio. The company provided a comprehensive overview of this strategic move:

The $157.5 million acquisition has added 18,300 BOE/d of estimated 2025 production (50% liquids) and 150 million BOE of 2P reserves. Management highlighted the acquisition’s compelling economics, with after-tax NPV values significantly exceeding the purchase price: $245 million for PDP reserves, $381 million for 1P reserves, and $724 million for 2P reserves.

This geographic diversification complements Gran Tierra’s established South American operations, creating what management described as a balanced portfolio across proven hydrocarbon basins with access to established infrastructure.

Reserve Growth and Asset Performance

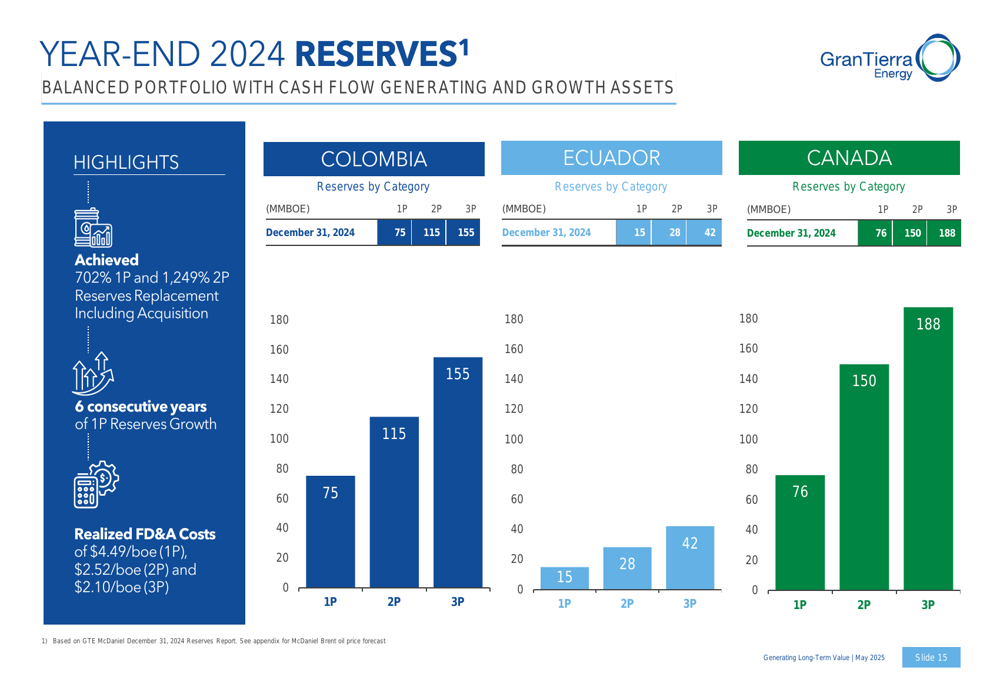

Gran Tierra reported impressive reserve replacement, achieving 702% for 1P and 1,249% for 2P reserves, including acquisitions. The company highlighted its sixth consecutive year of 1P reserves growth, with finding, development, and acquisition costs of $4.49/BOE (1P), $2.52/BOE (2P), and $2.10/BOE (3P).

The following chart illustrates the company’s year-end 2024 reserves by region:

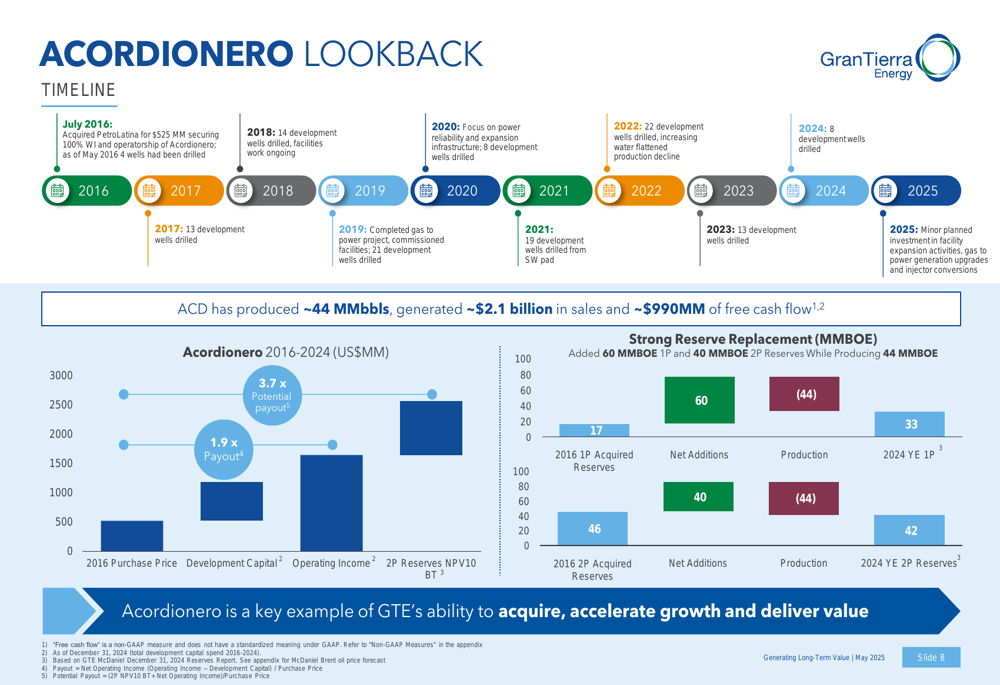

The company’s flagship Acordionero asset in Colombia continues to be a significant cash generator. Management provided a detailed timeline of this asset’s development since acquisition:

According to the presentation, Acordionero has produced approximately 44 million barrels since acquisition, generating about $2.1 billion in sales and $990 million in free cash flow. Management characterized it as a "cash cow," having generated $637 million in free cash flow over the past three years alone.

Financial Position and Capital Allocation

Gran Tierra outlined its financial objectives for 2025 and beyond, focusing on free cash flow generation, debt reduction, and shareholder returns. The company expects to generate approximately $20 million in free cash flow in 2025 (base case) and plans to allocate up to 50% of this to share buybacks through its normal course issuer bid program.

The company’s debt management strategy includes targets to reduce its Net Debt to EBITDA ratio to 0.8-1.2x and gross debt to less than $600 million by the end of 2026, and further to less than 1.0x and $500 million, respectively, by the end of 2027. Current net debt stands at $683 million.

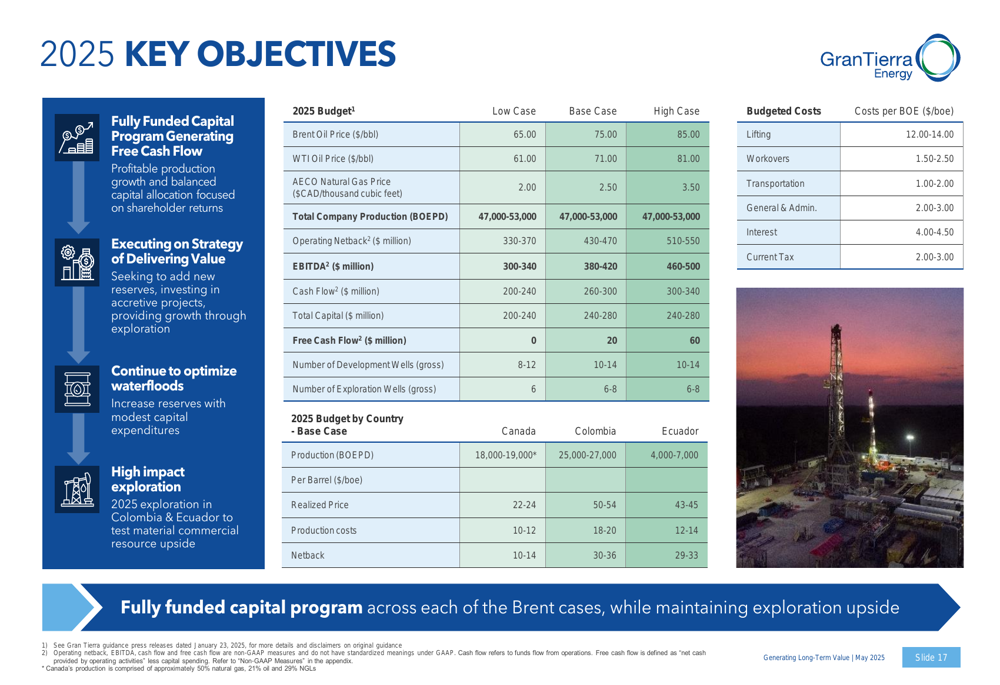

The following slide details the company’s 2025 key objectives across various price scenarios:

To protect against commodity price volatility, Gran Tierra has implemented a hedging strategy for both oil and gas production, as outlined in its presentation. The company emphasized its operational flexibility as an operator of the majority of its assets, allowing it to quickly respond to changes in commodity cycles.

Exploration and Growth Opportunities

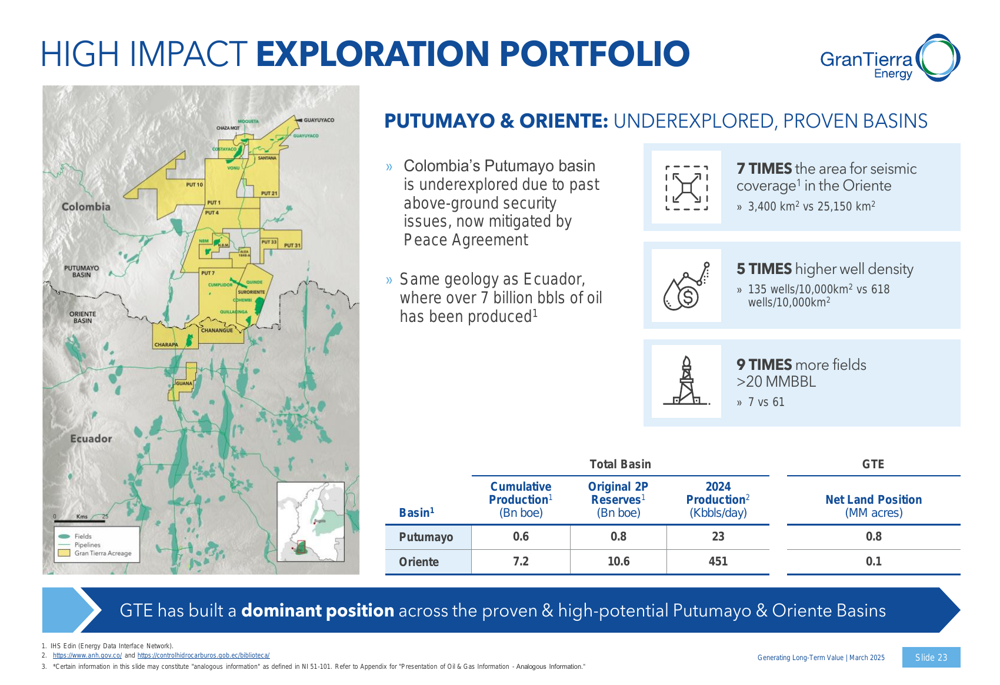

Gran Tierra highlighted its high-impact exploration portfolio, particularly in the Putumayo and Oriente basins. The company noted that Colombia’s Putumayo basin remains underexplored due to past security issues, which have been mitigated by peace agreements.

The following map illustrates the company’s exploration portfolio in these regions:

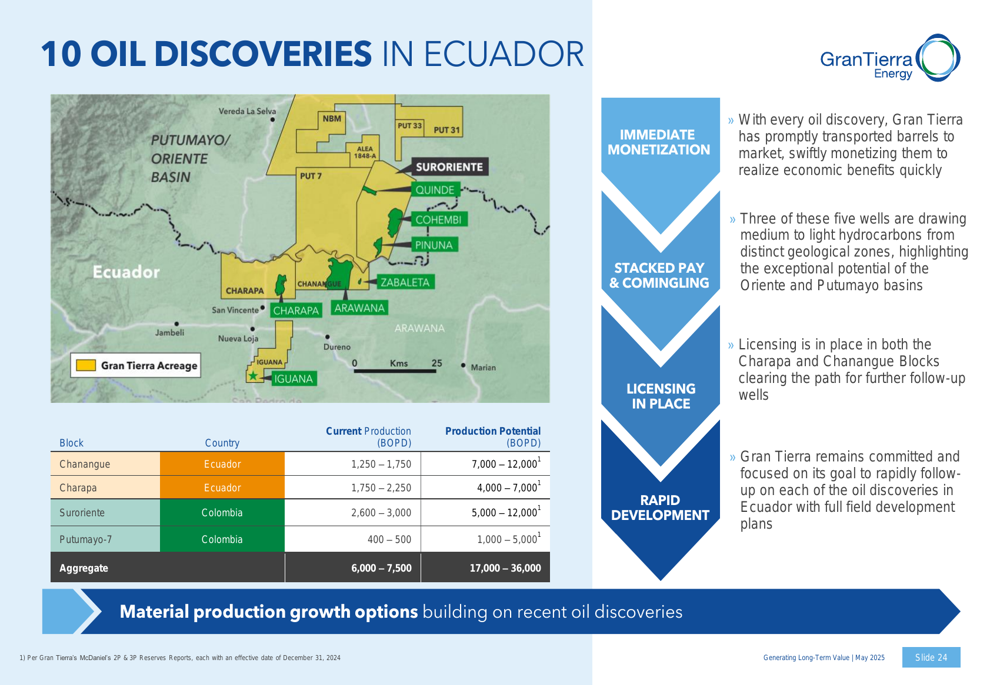

In Ecuador, Gran Tierra has made 10 oil discoveries and is focused on rapid monetization and development. The company emphasized its ability to quickly bring discoveries to market and implement efficient development plans:

Operational Strategy and Technology

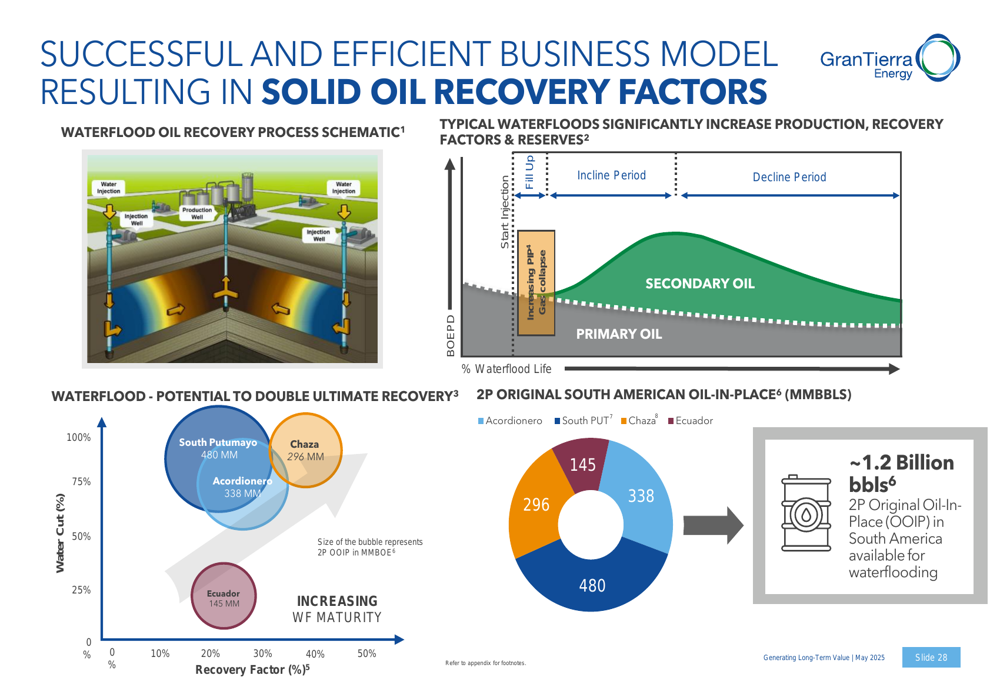

A key component of Gran Tierra’s operational strategy is its waterflood program, which the company describes as having the potential to double ultimate recovery from its reservoirs. The presentation highlighted the success of this approach in fields like Costayaco:

Management emphasized that its waterflood expertise is transferable across its portfolio, providing a competitive advantage in resource development and recovery optimization.

Outlook and Guidance

For 2025, Gran Tierra has provided production guidance of 47,000-53,000 BOE/d, representing potential growth from its Q1/2025 production level of approximately 47,000 BOE/d. The company’s capital program is expected to be fully funded by cash flow while targeting development programs and projects to increase production and reserves.

Looking beyond 2025, management indicated that the recent Canadian acquisition positions Gran Tierra for significant production growth in 2026 and beyond. The company plans to fulfill its entire Ecuador exploration program in 2025, potentially adding further growth opportunities.

While Gran Tierra’s presentation painted an optimistic picture of its diversified portfolio and growth prospects, investors appear to be taking a more cautious view, as reflected in the recent stock performance. The company’s ability to deliver on its debt reduction targets while maintaining production growth will likely be key factors in rebuilding investor confidence in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.