Japan PPI inflation slips to 11-mth low in July

Introduction & Market Context

Granite Construction Incorporated (NYSE:GVA) presented its Q1 2025 results on May 1, 2025, highlighting a modest start to the year but maintaining confidence in its full-year outlook. The company reported that the current market environment continues to offer strong opportunities despite macroeconomic uncertainties, supported by the federal infrastructure bill and resilient private markets.

The stock closed at $81.29 on May 1, down 0.67% for the day, reflecting investors’ measured reaction to the seasonally slower first quarter results. This follows a strong performance in Q4 2024, when the company exceeded analyst expectations with an EPS of $1.23.

Quarterly Performance Highlights

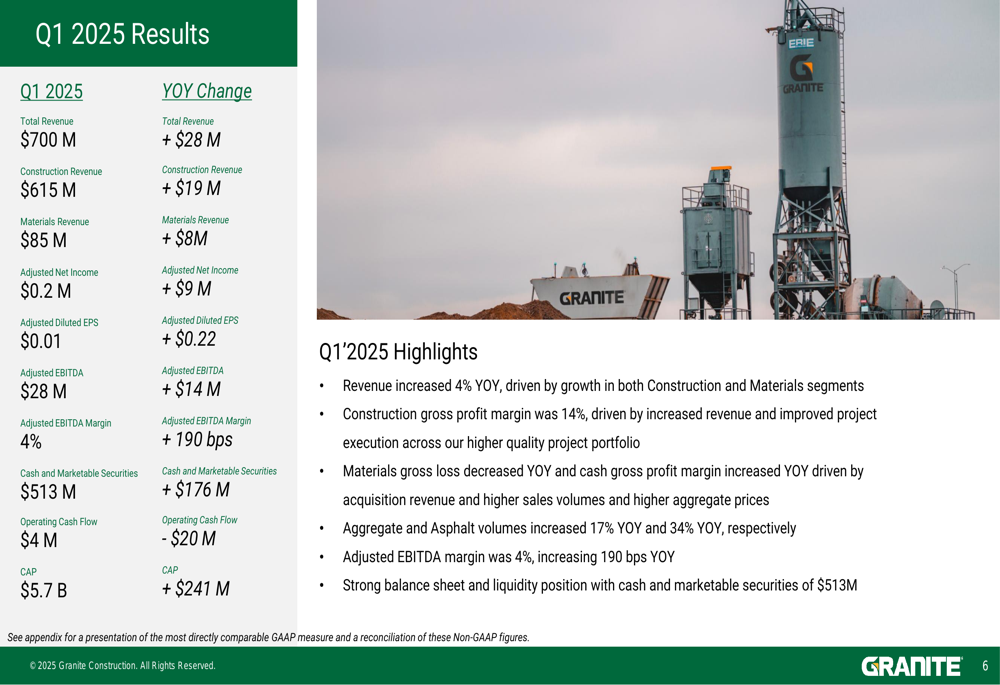

Granite reported total revenue of $700 million for Q1 2025, representing a $28 million or 4% increase year-over-year. The company achieved a slim adjusted net income of $0.2 million, improving by $9 million compared to Q1 2024, with adjusted diluted EPS of $0.01, up $0.22 year-over-year.

Adjusted EBITDA reached $28 million, a $14 million increase from the prior year, with the adjusted EBITDA margin expanding 190 basis points to 4%. The company maintained a strong balance sheet with $513 million in cash and marketable securities, a significant increase of $176 million year-over-year.

As shown in the following financial results summary:

Operating cash flow was $4 million, down $20 million from the previous year, but the company reiterated its target of achieving operating cash flow at 9% of revenue for the full year 2025. This cash generation is expected to support Granite’s capital allocation priorities, including continued M&A activity.

Segment Analysis

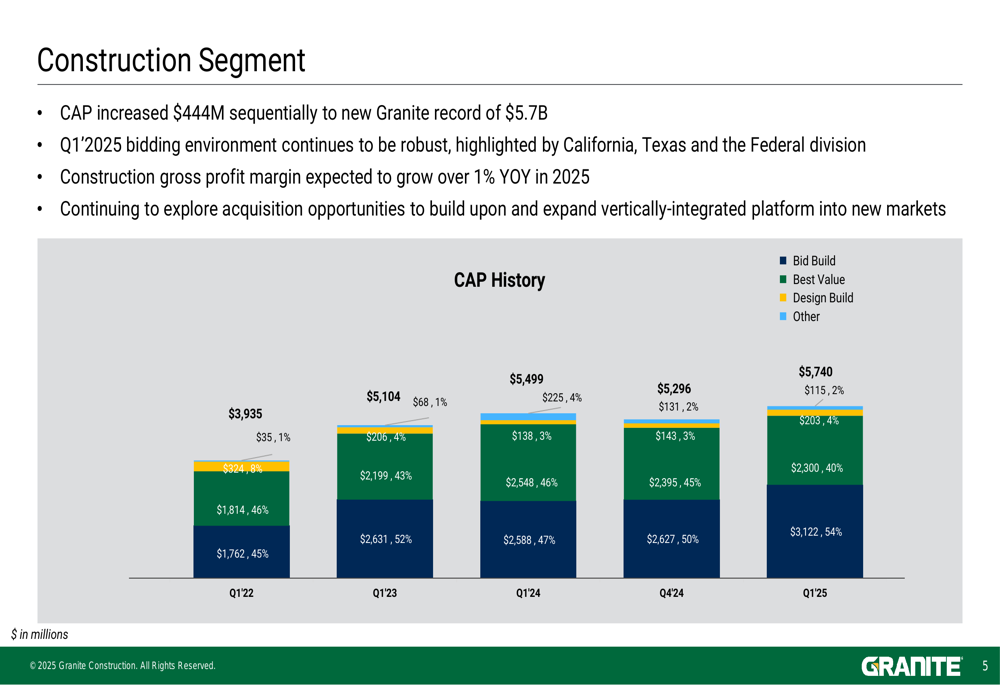

The Construction segment generated $615 million in revenue, up $19 million year-over-year, with a gross profit margin of 14%. Most notably, Granite’s Committed and Awarded Projects (CAP) increased by $444 million sequentially to a record $5.7 billion, providing substantial revenue visibility for the coming quarters.

The CAP breakdown shows a diversified mix of project types, with 54% in Bid Build, 40% in Best Value, 4% in Design Build, and 2% in Other categories:

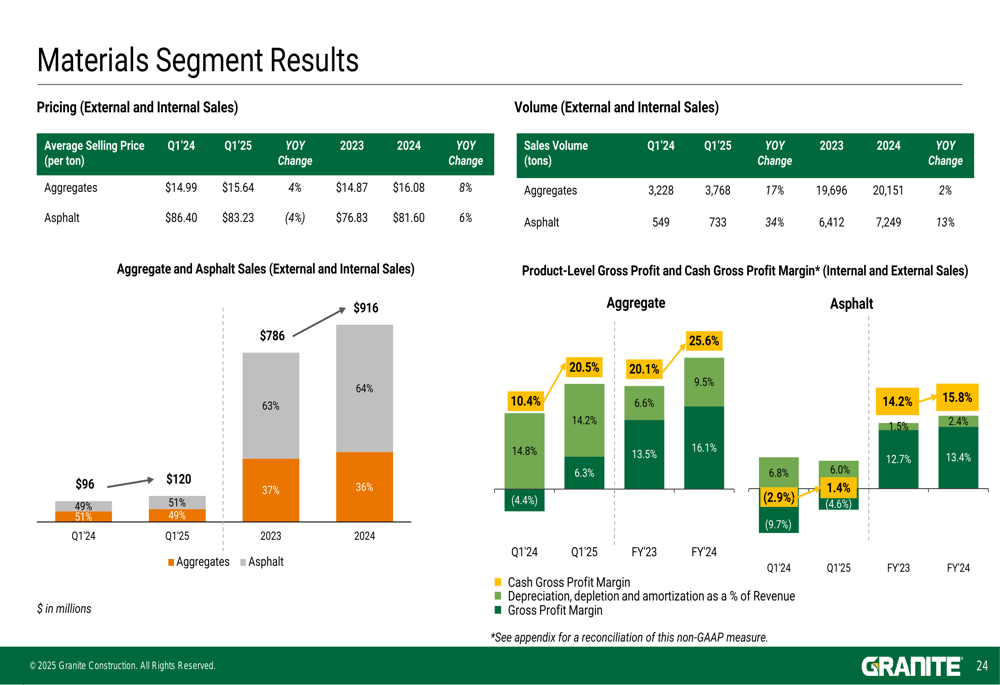

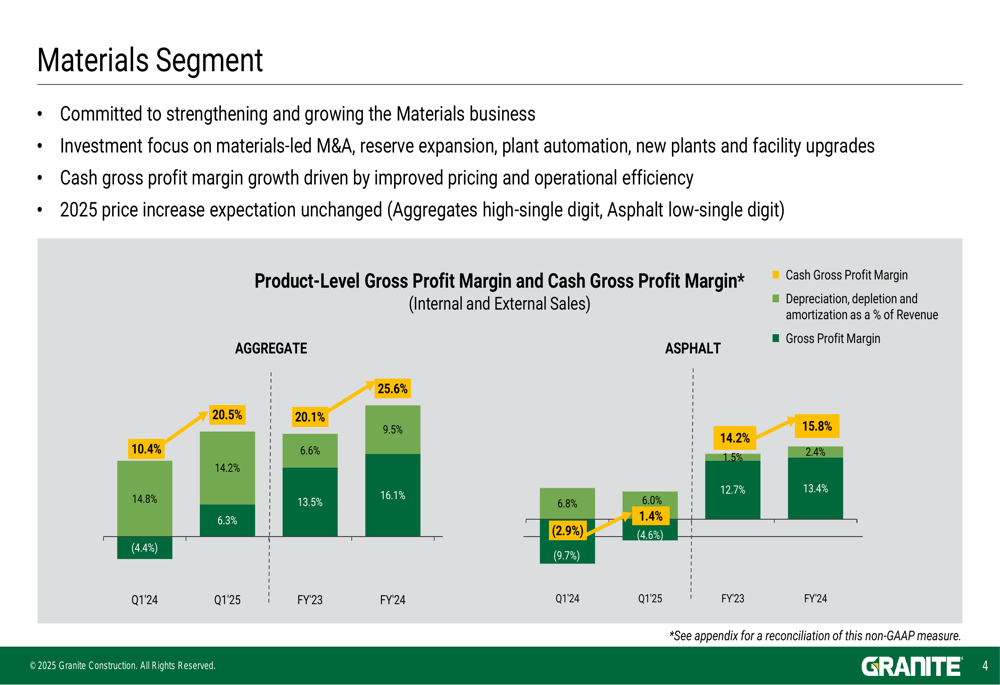

The Materials segment showed promising momentum with revenue of $85 million, an $8 million increase year-over-year. Aggregate and asphalt volumes increased significantly, up 17% and 34% respectively compared to Q1 2024. The segment’s cash gross profit margins also improved, particularly in aggregates, where the margin increased from 10.4% in Q1 2024 to 14.2% in Q1 2025.

The detailed breakdown of Materials segment performance shows improving pricing and volume trends:

The company’s focus on strengthening its Materials business through materials-led M&A, reserve expansion, plant automation, and upgrades is yielding results. The aggregate average selling price increased to $15.64 per ton in Q1 2025 from $14.99 in Q1 2024, while the asphalt average selling price decreased slightly to $83.23 from $86.40.

Strategic Initiatives and Growth Outlook

Granite continues to execute its strategic growth plan, with a focus on both organic growth and acquisitions. The company’s investment framework supports long-term growth through two main approaches: "Support & Strengthen" (solidifying core competencies) and "Expand & Transform" (expanding into new geographies).

Recent acquisitions, including Lehman-Roberts, Memphis Stone & Gravel, and Dickerson & Bowen, have expanded Granite’s footprint into the Southeast (Arkansas, Tennessee, Mississippi), creating a new platform for growth. These acquisitions have added seven asphalt plants and exclusive rights to an estimated 86 million tons of reserves from Lehman-Roberts and Memphis Stone & Gravel, plus four additional asphalt plants and three sand & gravel pits with an estimated 19 million tons of reserves from Dickerson & Bowen.

The company’s vertical integration strategy remains a key differentiator, enabling it to compete effectively in markets where owning materials is necessary, maximize productivity, ensure quality, and leverage lower production costs compared to external pricing.

Financial Guidance and Medium-Term Targets

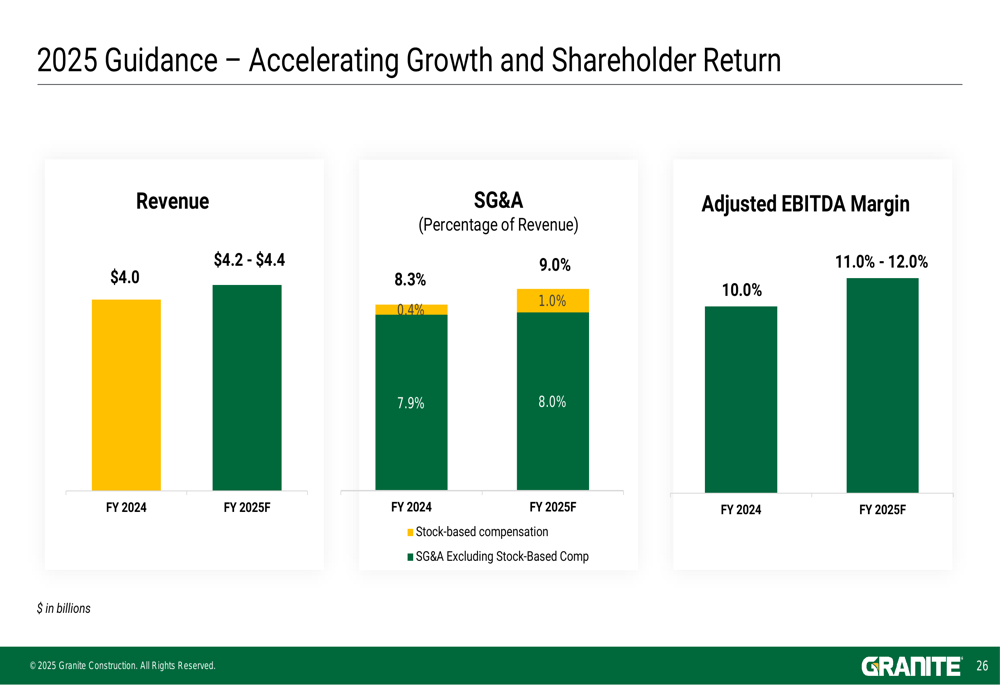

Despite the seasonally slower first quarter, Granite reaffirmed its 2025 guidance, projecting revenue between $4.2 billion and $4.4 billion, with SG&A at 9.0% of revenue (including 1.0% from stock-based compensation) and an adjusted EBITDA margin between 11.0% and 12.0%:

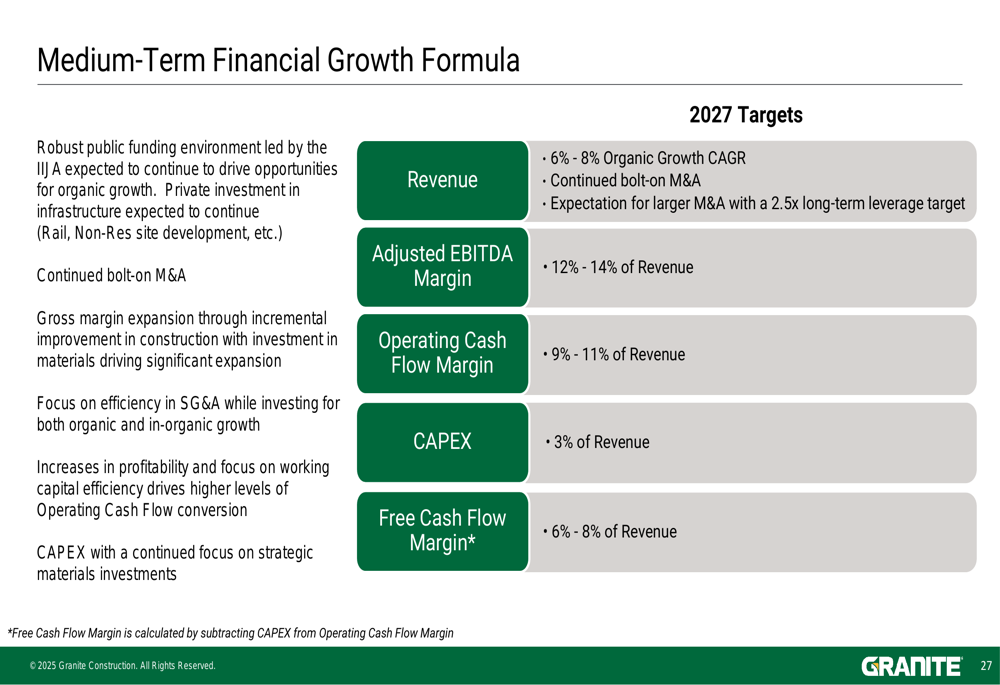

Looking further ahead, the company maintained its medium-term financial targets for 2027, including 6-8% organic growth CAGR, continued bolt-on M&A strategy with expectations for larger acquisitions, and a 2.5x long-term leverage target. Granite is targeting a 12-14% adjusted EBITDA margin, 9-11% operating cash flow margin, capital expenditures at 3% of revenue, and a 6-8% free cash flow margin:

The company’s capital allocation priorities remain focused on maintaining the current dividend level, supporting business operations via maintenance capex (1.5-2.0% of annual revenue), investing in growth capex and M&A, targeting 2.5x long-term leverage, and opportunistic share repurchases when cash exceeds operational and growth requirements.

In conclusion, while Granite Construction’s Q1 2025 results reflect the typical seasonality in the construction industry, the record CAP, improving materials segment performance, and reaffirmed guidance suggest the company remains on track to achieve its full-year targets. The strong balance sheet and clear strategic direction position Granite to capitalize on infrastructure spending and continue its growth trajectory through both organic expansion and strategic acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.