Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Granite Ridge Resources (NYSE:GRNT) released its Q2 2025 investor presentation highlighting strong operational performance against a backdrop of industry-wide production stagnation. The company’s strategy of investing in energy development projects through multiple commodity cycles has enabled it to achieve significant growth while maintaining financial discipline.

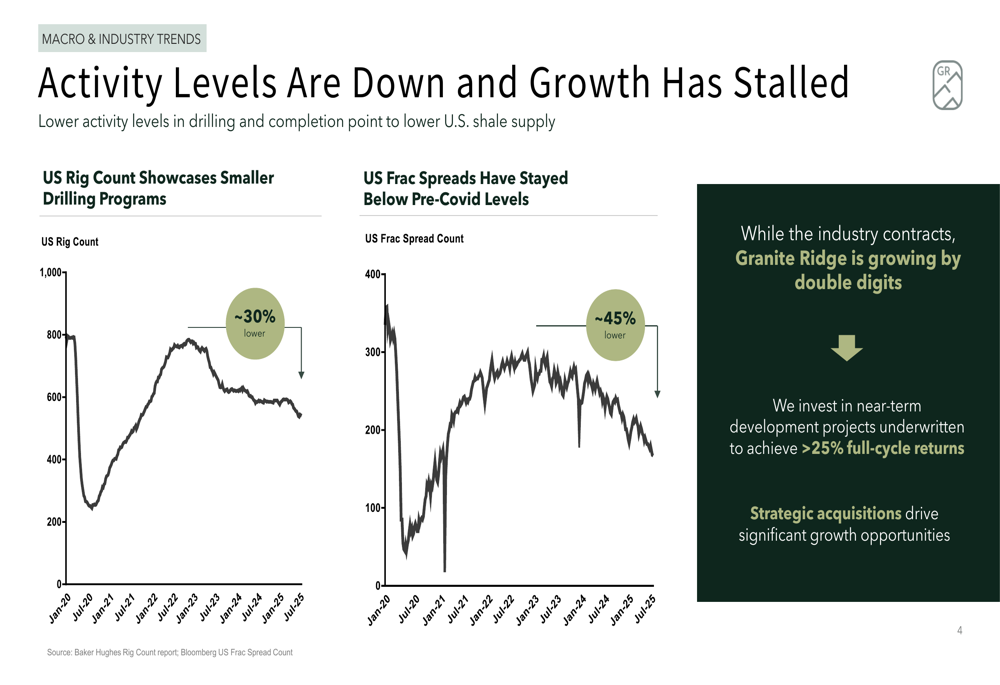

The presentation emphasizes how Granite Ridge is capitalizing on market conditions where U.S. onshore activity levels have declined substantially, with the U.S. rig count down approximately 30% and frac spreads remaining 45% below pre-COVID levels.

As shown in the following chart illustrating these industry headwinds:

Despite these challenging conditions, Granite Ridge positions itself as a growth-oriented company in a stagnant market, focusing on near-term development projects with greater than 25% full-cycle returns and strategic acquisitions that drive significant growth opportunities.

Q2 2025 Performance Highlights

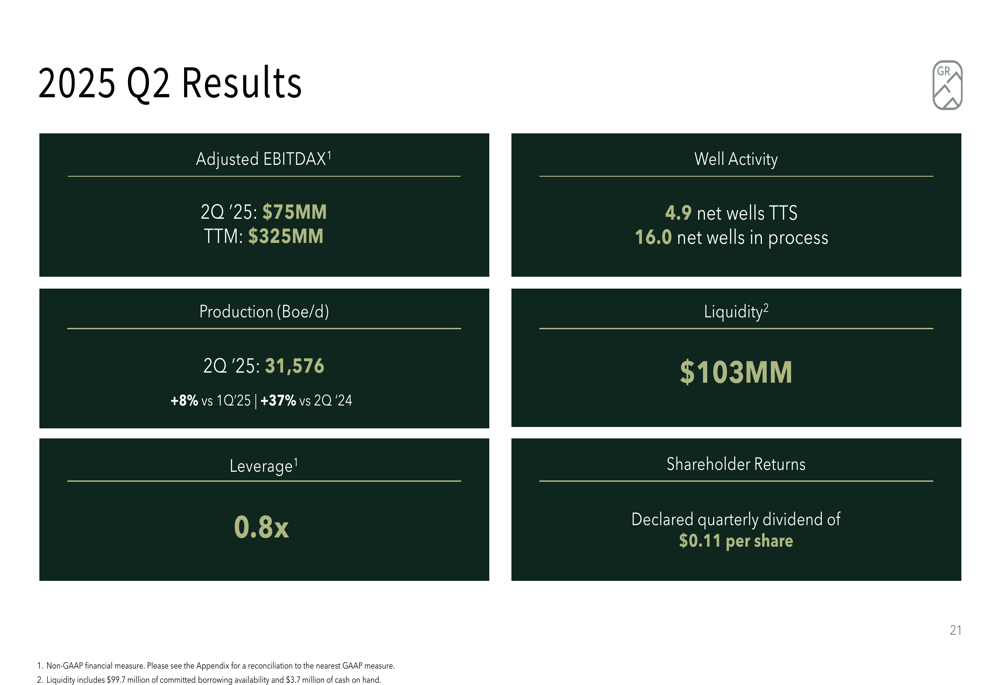

Granite Ridge reported impressive Q2 2025 results, with production reaching 31,576 barrels of oil equivalent per day (Boe/d), representing an 8% increase from Q1 2025 and a substantial 37% year-over-year growth compared to Q2 2024. The company’s production portfolio maintains a balanced 50/50 split between oil and natural gas across six premier U.S. basins.

The company’s financial performance remained strong with Adjusted EBITDAX of $75 million for the quarter and $325 million for the trailing twelve months. Granite Ridge maintained its disciplined approach to leverage with a ratio of 0.8x, while declaring a quarterly dividend of $0.11 per share.

The following slide summarizes the company’s Q2 2025 results:

Granite Ridge’s multi-basin portfolio spans the Permian (63%), DJ Basin, Haynesville, Eagle Ford, Utica, and Bakken regions, with partnerships with 65 different operators across approximately 3,100 gross wells. This diversification strategy has helped the company mitigate regional risks while maximizing exposure to the most productive U.S. energy basins.

Growth Strategy and Investment Approach

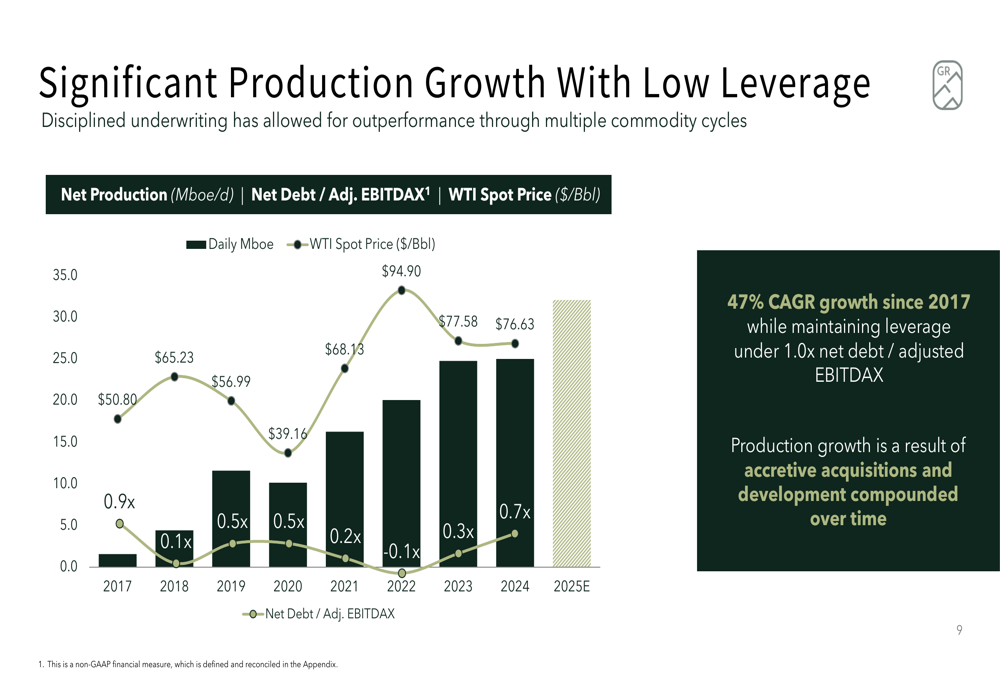

Granite Ridge employs a dual investment strategy focused on Operated Partnerships and Traditional Non-Operated interests, both underwritten to achieve 25% IRR full-cycle returns. This approach has enabled the company to achieve a 47% CAGR in production since 2017 while maintaining leverage consistently below 1.0x.

The company’s investment philosophy is illustrated in the following slide:

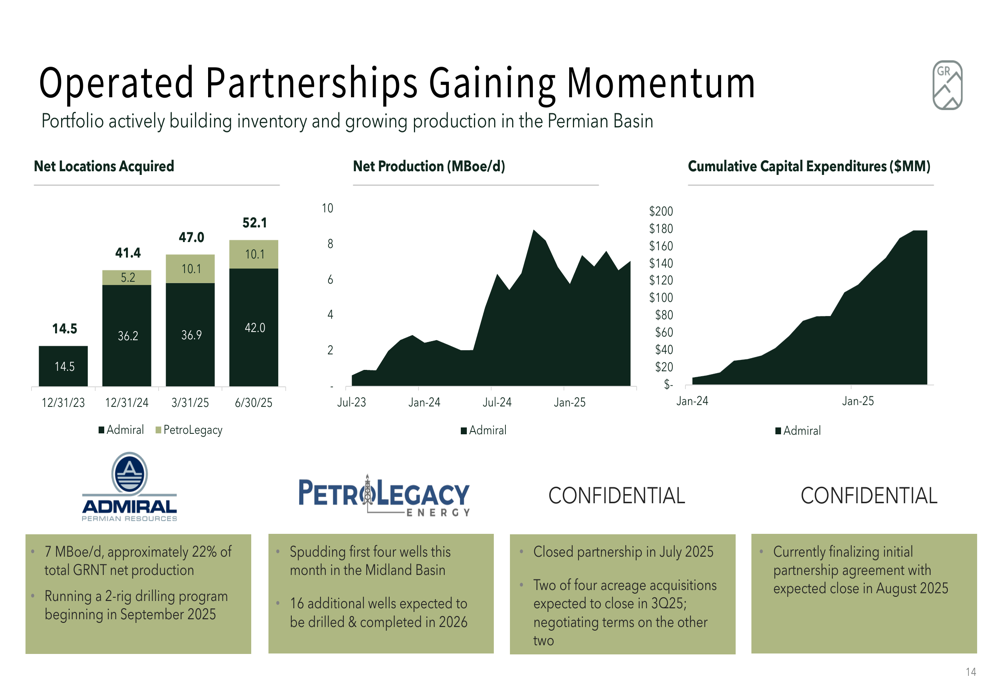

A key differentiator for Granite Ridge is its increasing focus on operated partnerships, which now account for approximately 22% of the company’s total production. The company is running a 2-rig drilling program beginning in September 2025 for Admiral Resources and has recently closed a partnership in July 2025, with additional agreements expected to close in August 2025.

The momentum in operated partnerships is demonstrated in this chart:

Granite Ridge’s ability to source and evaluate over 650 opportunities annually has allowed it to be highly selective, investing only in projects that meet its stringent return criteria. Since 2024, the company has screened over 1,100 transactions representing more than $12 billion in investment opportunities.

Financial Position and Shareholder Returns

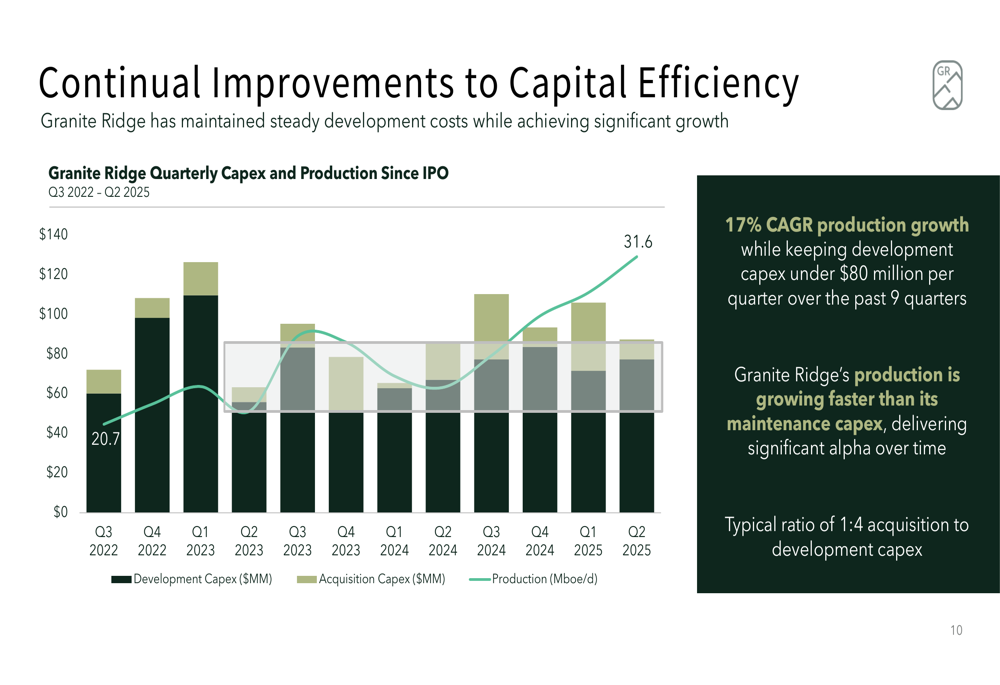

Granite Ridge has maintained strong capital efficiency while achieving significant growth. The company has kept development capex under $80 million per quarter over the past nine quarters while delivering 17% CAGR production growth. This efficiency is illustrated in the following chart:

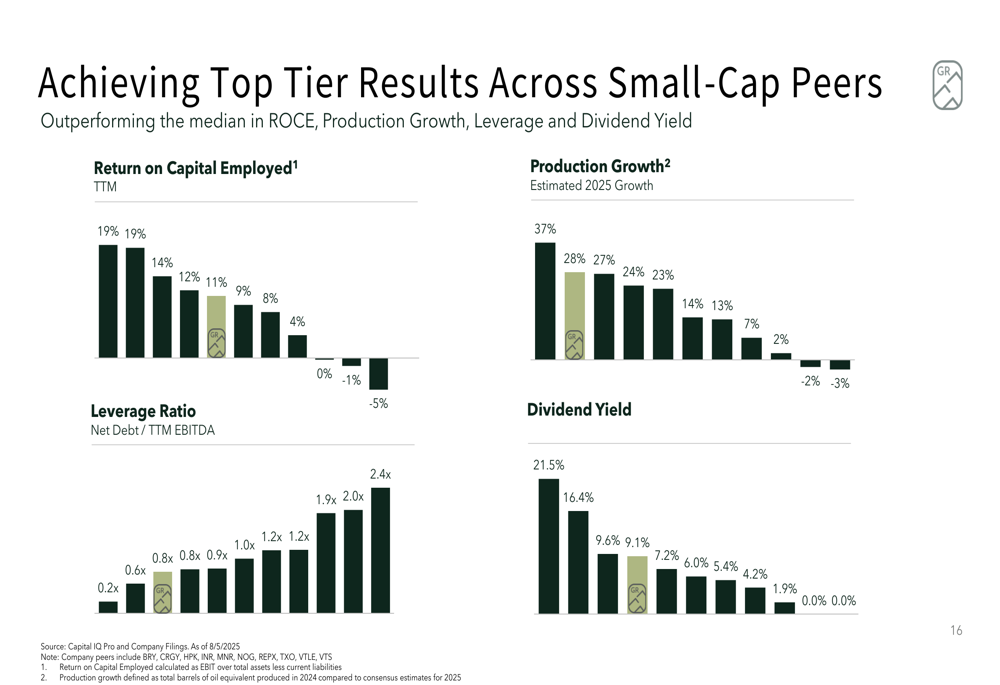

The company continues to outperform its small-cap peers across key metrics including Return on Capital Employed, Production Growth, Leverage Ratio, and Dividend Yield. With a dividend yield of approximately 9.1% based on the presentation data, Granite Ridge offers one of the more attractive returns in the sector.

The peer comparison is highlighted in this slide:

Granite Ridge’s stock closed at $4.88 as of August 7, 2025, with a 52-week range of $4.52 to $7.00. The company’s enterprise value to 2025 EBITDA ratio stands at 2.6x, suggesting potential undervaluation relative to peers and its growth profile.

Forward Outlook and Guidance

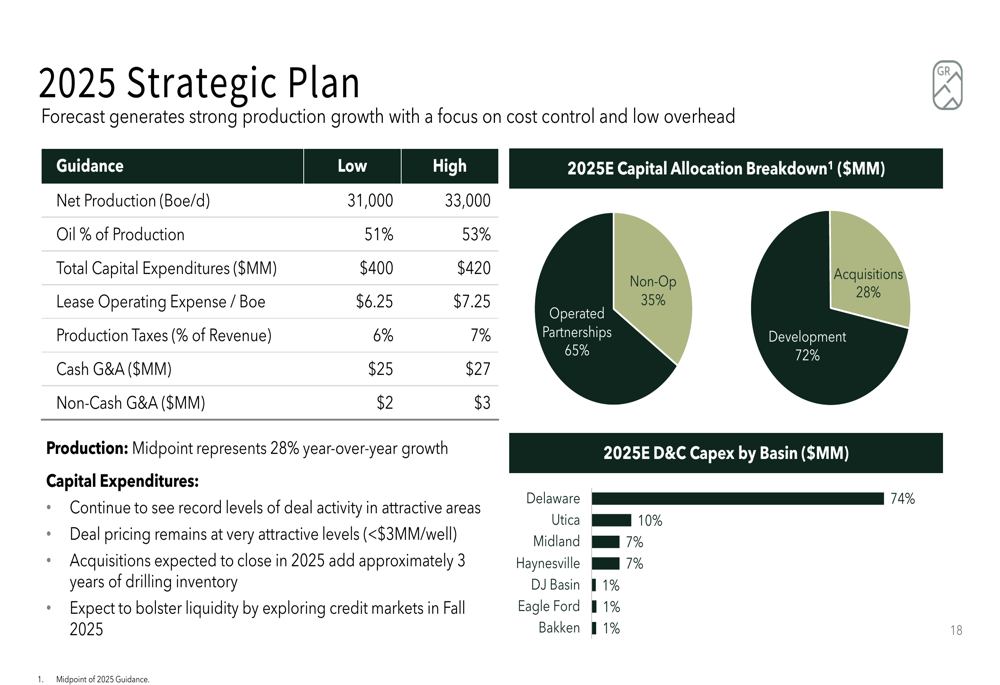

For 2025, Granite Ridge has outlined a strategic plan focused on strong production growth with cost control and low overhead. The company’s capital allocation strategy allocates 65% to Operated Partnerships and 35% to Non-Operated interests, with the majority of development and completion capex directed toward the Delaware Basin (74%).

The company’s 2025 strategic plan is summarized in the following slide:

Granite Ridge’s focus on financial discipline is underpinned by four strategic pillars: Asset Growth, Adaptability and Diversification, Financial Management, and Shareholder Focus. The company aims to drive growth by reinvesting cash flow into efficient, near-term development projects while maintaining a robust balance sheet and supporting its fixed annual dividend of $0.44 per share.

Looking ahead, Granite Ridge appears well-positioned to continue its growth trajectory despite industry headwinds. The company’s diversified approach, focus on high-return projects, and financial discipline provide a foundation for sustainable performance. With its dual investment strategy gaining momentum, particularly in operated partnerships, Granite Ridge offers investors exposure to U.S. energy development with the liquidity of a public company and returns typically associated with private equity investments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.