Bitcoin price today: rises above $111k amid easing trade jitters; US CPI on tap

Introduction & Market Context

Graphic Packaging Holding Company (NYSE:GPK) presented its second quarter 2025 earnings on July 29, revealing a company navigating near-term profitability challenges while maintaining an optimistic long-term outlook. The packaging manufacturer reported modest volume growth despite a challenging consumer environment, with its stock trading near 52-week lows at $17.47 as of the latest close, down significantly from its 52-week high of $30.70.

The company’s diversified portfolio spans five major segments: Food (38%), Beverage (25%), Foodservice (21%), Household (12%), and Health & Beauty (4%). This diversification has provided some resilience as consumer spending patterns continue to shift in response to economic pressures.

As shown in the following product portfolio breakdown:

Quarterly Performance Highlights

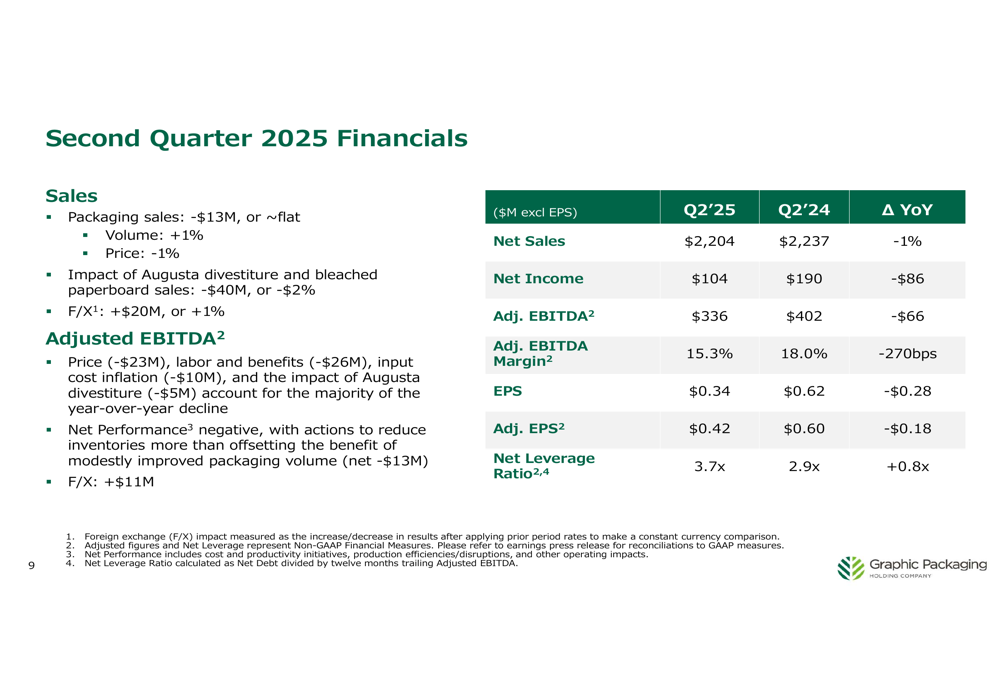

Graphic Packaging reported Q2 2025 net sales of $2,204 million, down 1% year-over-year, with volume increasing 1% while pricing decreased 1%. The company’s profitability metrics showed more significant pressure, with adjusted EBITDA falling to $336 million from $402 million in the prior year, resulting in an adjusted EBITDA margin of 15.3%, down 270 basis points year-over-year.

Net income declined to $104 million from $190 million, while adjusted EPS fell to $0.42 from $0.60 in Q2 2024. The company’s net leverage ratio increased to 3.7x from 2.9x a year earlier, reflecting ongoing capital investments.

The financial results reflect what the company described as a challenging consumer packaging environment, with uneven volumes across consumer staples, though beverage and health & beauty segments showed improvement while food, foodservice, and household segments remained steady.

The following slide summarizes the key financial metrics:

Despite these challenges, Graphic Packaging raised its full-year 2025 net sales guidance to $8.4-8.6 billion from the previous $8.2-8.5 billion, while maintaining its adjusted EBITDA guidance of $1.45-1.55 billion. The company continues to project capital spending of approximately $850 million for the year, largely directed toward its Waco, Texas facility investment.

Strategic Initiatives

Innovation remains a cornerstone of Graphic Packaging’s strategy, with the company reporting $61 million in innovation sales growth during the quarter. Management emphasized a $15 billion addressable market opportunity across various packaging solutions, including trays & bowls ($5.0B), cups & containers ($4.0B), paperboard canisters ($2.5B), strength packaging ($2.0B), and multipacks ($1.5B).

The company’s innovation market opportunities are illustrated here:

A key example of the company’s innovation approach is its redesigned coffee pod packaging solution, which demonstrates improvements in sustainability, functionality, and convenience. The new design increases pallet efficiency from 80 to 104 salable units per pallet, addressing a $2.0 billion global strength packaging market opportunity while replacing plastic, bleached paperboard, and corrugated materials.

The following slide demonstrates this packaging innovation:

On the operational front, Graphic Packaging confirmed its Waco, Texas recycled paperboard investment remains on track for Q4 2025 startup, though final design and completion costs were higher than initially projected. The company also noted the closure of its Middletown, Ohio recycled paperboard facility on May 27, 2025, as part of its ongoing optimization efforts.

Forward-Looking Statements

Graphic Packaging’s Vision 2030 strategy outlines ambitious goals across innovation, culture, planet, and financial results. The financial model targets low-single-digit annual sales growth, mid-single-digit adjusted EBITDA growth, and high-single-digit adjusted EPS growth, with normalized capital expenditures expected to settle at approximately 5% of sales after 2025.

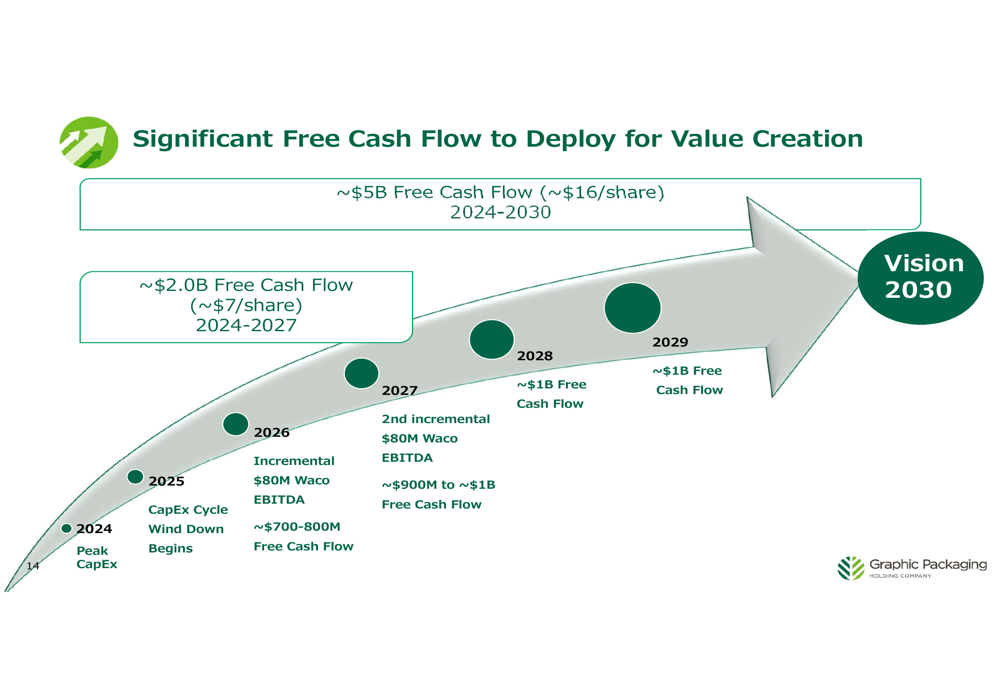

The company projects significant free cash flow generation, estimating approximately $2.0 billion ($7 per share) from 2024-2027 and $5.0 billion ($16 per share) from 2024-2030. This projection includes expected incremental EBITDA of $80 million from the Waco facility in 2026, with an additional $80 million in 2027, helping drive annual free cash flow to approximately $1 billion by 2028.

The free cash flow trajectory is illustrated in this forward-looking projection:

Capital Allocation Strategy

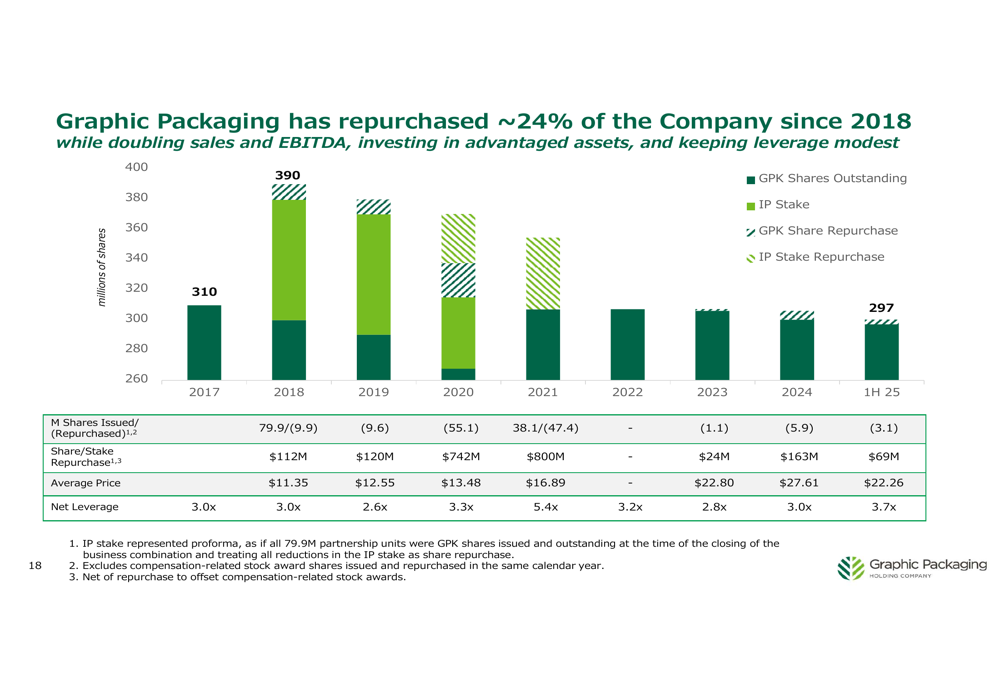

Despite near-term profitability challenges, Graphic Packaging maintained its commitment to shareholder returns in Q2 2025, repurchasing approximately 5.0 million shares at an average price of $22.26 per share for a total of $111 million. This represented a 1.6% reduction in shares outstanding during the quarter. Additionally, the company paid $33 million in cash dividends, bringing total capital returned to stockholders to $144 million for the quarter.

The company has a consistent history of share repurchases, having bought back approximately 24% of the company since 2018 while simultaneously doubling sales and EBITDA and investing in strategic assets. This approach reflects management’s confidence in the long-term outlook despite current market challenges.

The share repurchase history is detailed in the following slide:

Looking ahead, Graphic Packaging’s capital allocation priorities include reinvesting to expand capabilities, growing the dividend, repurchasing shares, achieving investment grade ratings, and pursuing tuck-in acquisitions. Management emphasized that after the completion of the Waco facility, the company will have the assets, capabilities, and team needed to achieve its Vision 2030 financial goals while generating cash "well in excess of reinvestment needs."

While the market appears skeptical given the stock’s proximity to 52-week lows, Graphic Packaging’s management remains confident in the company’s ability to navigate near-term challenges while positioning for long-term growth through innovation, sustainability initiatives, and strategic capital investments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.