TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

Green Dot Corporation (NYSE:GDOT) delivered a stellar performance in its first quarter of 2025, according to the company’s presentation released on May 8. The financial technology and banking company reported results that significantly exceeded expectations, driving its stock up 13.79% in aftermarket trading to $9.90.

The strong Q1 performance represents a notable turnaround from the company’s Q4 2024 results, which had disappointed investors with an EPS miss despite revenue growth. Green Dot’s focus on its B2B segment and operational efficiency appears to be paying dividends as the company continues its strategic transformation.

Quarterly Performance Highlights

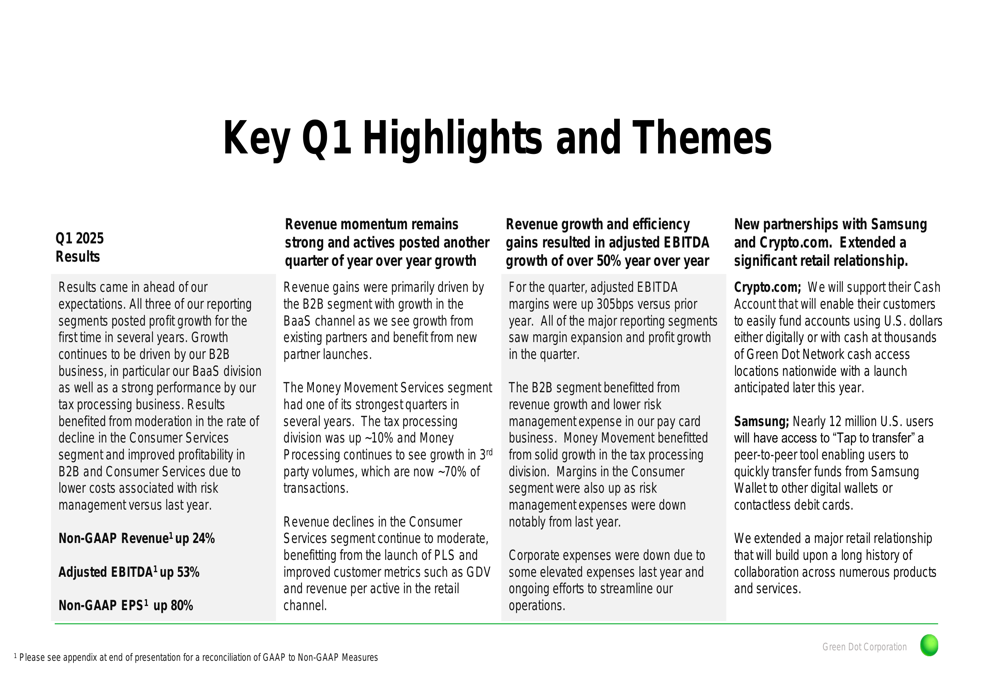

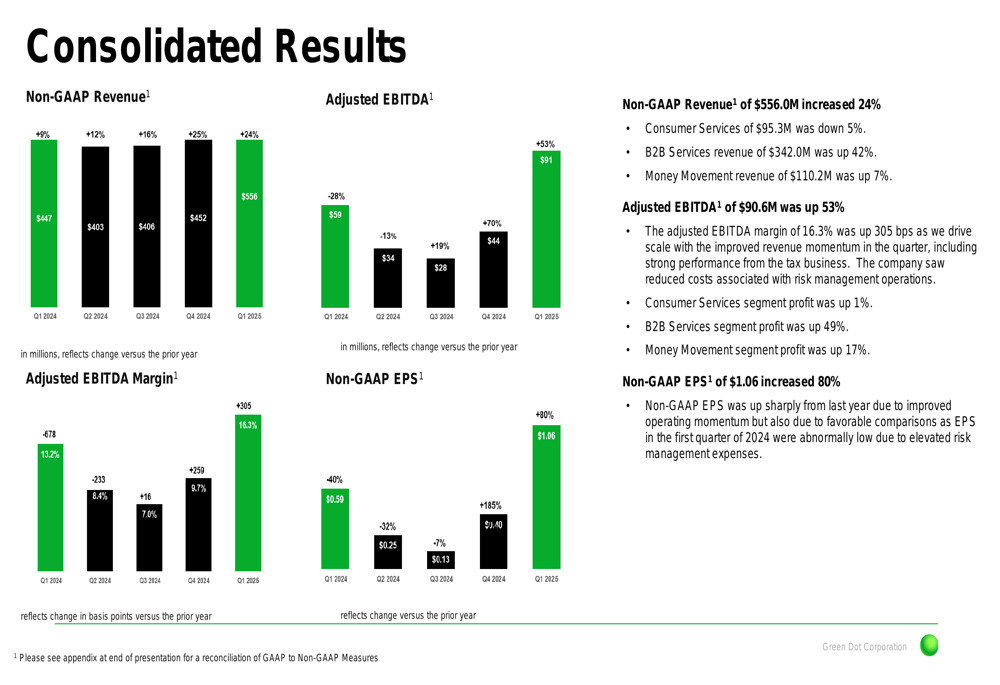

Green Dot reported impressive financial metrics across the board for Q1 2025. Non-GAAP revenue reached $556.0 million, representing a 24% increase year-over-year. Adjusted EBITDA surged 53% to $90.6 million, while non-GAAP EPS jumped 80% to $1.06.

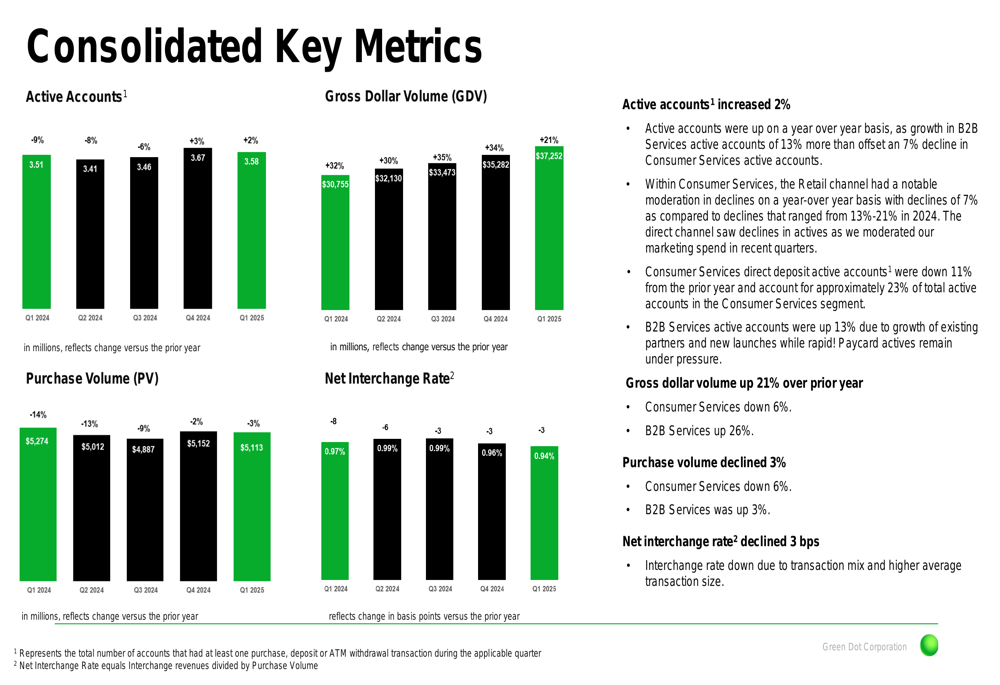

The company’s adjusted EBITDA margin expanded by 305 basis points to 16.3%, reflecting significant operational efficiency gains. Active accounts increased by 2% overall, with gross dollar volume (GDV) growing 21% to $37.25 billion, though purchase volume decreased 3% to $5.11 billion.

As shown in the following key highlights from the presentation:

The consolidated financial results demonstrate the company’s strong momentum across multiple quarters:

Segment Analysis

Green Dot’s performance varied significantly across its three main business segments, with B2B Services emerging as the clear growth driver.

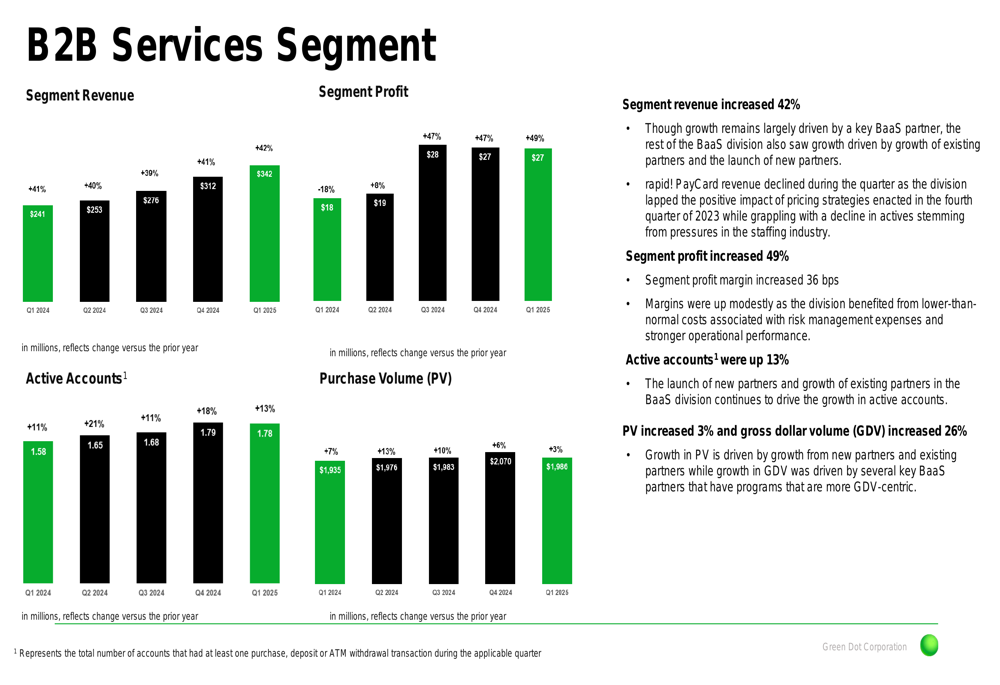

The B2B Services segment delivered exceptional results, with revenue increasing 42% to $342.0 million and segment profit growing 49%. Active accounts in this segment rose 13%, while gross dollar volume increased 26%. According to the presentation, this growth was largely driven by a key Banking-as-a-Service (BaaS) partner, along with the successful launch of new partnerships.

The following chart illustrates the B2B segment’s strong performance:

In contrast, the Consumer Services segment continued to face challenges, with revenue declining 5% to $95.3 million. Despite this, segment profit increased 1%, suggesting improved efficiency. Active accounts decreased 7%, with direct deposit active accounts down 11%. The company noted that revenue declines have moderated due to the Private Label Services (PLS) launch and improving operating expenses.

The Money Movement Services segment showed solid growth, with revenue increasing 7% to $110.2 million and segment profit up 17%. Revenue-generating cash transfers decreased 3%, while tax refunds processed were down 14%. The company attributed the division’s revenue growth to tax processing and third-party volumes.

Strategic Initiatives and Partnerships

Green Dot announced several strategic developments during the quarter that position the company for continued growth. New partnerships with Samsung (KS:005930) and Crypto.com were highlighted as significant wins that should contribute to future revenue growth. The company also extended an existing retail relationship, though specific details were not provided in the presentation.

The company’s strategy appears focused on expanding its B2B offerings while stabilizing its consumer business. The presentation noted that revenue momentum remained strong with active accounts posting another quarter of year-over-year growth, primarily driven by the B2B segment.

Green Dot’s consolidated key metrics show the overall business trends:

Forward Guidance and Outlook

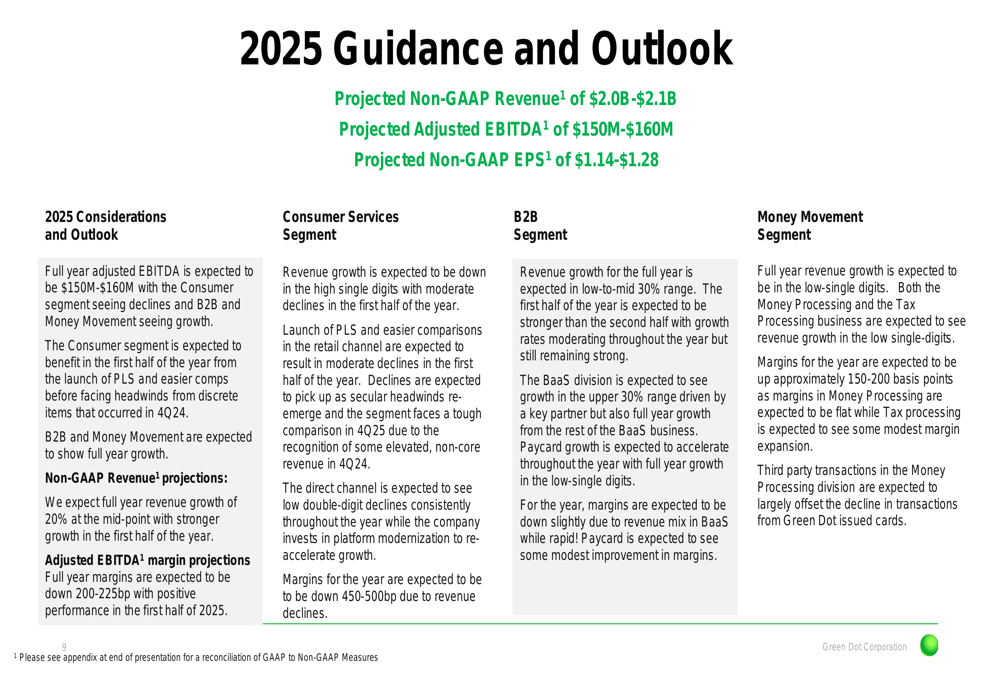

Following the strong Q1 results, Green Dot provided an optimistic outlook for the full year 2025. The company now projects non-GAAP revenue of $2.0-$2.1 billion, adjusted EBITDA of $150-$160 million, and non-GAAP EPS of $1.14-$1.28.

This guidance represents an increase from the previous outlook provided after Q4 2024 results, which had projected revenue between $1.85-$1.9 billion and adjusted EBITDA of $145-$155 million. The raised guidance reflects management’s increased confidence in the company’s growth trajectory and operational improvements.

The detailed 2025 guidance breaks down expectations by segment:

The guidance suggests continued strength in the B2B segment, with projected revenue growth of 30-35%. The Consumer Services segment is expected to see revenue decline by 5-10%, while Money Movement Services revenue is projected to grow by 5-10%.

Green Dot’s impressive Q1 2025 performance, particularly in its B2B segment, indicates that the company’s strategic shift is gaining traction. With expanded partnerships, improved operational efficiency, and raised guidance, Green Dot appears well-positioned to continue its positive momentum throughout 2025, despite ongoing challenges in its Consumer Services segment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.