Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

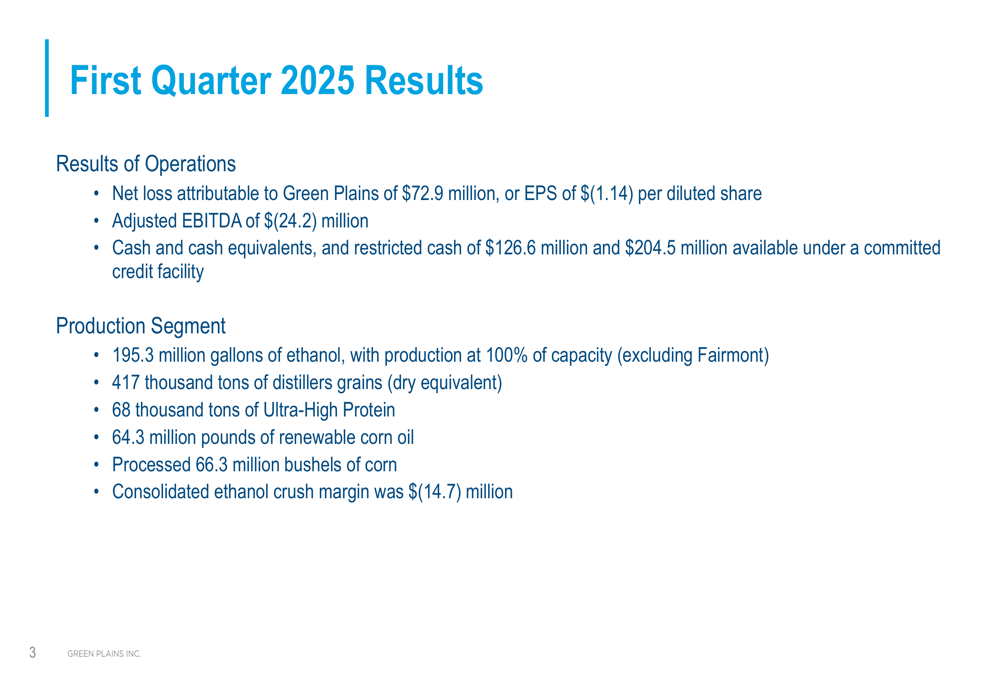

Green Plains Inc. (NASDAQ:GPRE) released its first quarter 2025 business update on May 8, revealing widening losses amid ongoing corporate restructuring efforts. The renewable fuels producer reported a net loss of $72.9 million, or $(1.14) per diluted share, significantly worse than the $51.4 million loss in the same period last year. The company’s stock, which has already fallen from a 52-week high of $20.54 to $3.77, dropped an additional 6.37% following the presentation.

The deteriorating financial performance marks a stark contrast to the company’s Q3 2024 results, which had shown positive EBITDA of $83.3 million, albeit boosted by asset sales. Despite operational challenges, Green Plains maintained full production capacity at its operating ethanol plants and continued to advance its carbon capture initiatives.

Quarterly Performance Highlights

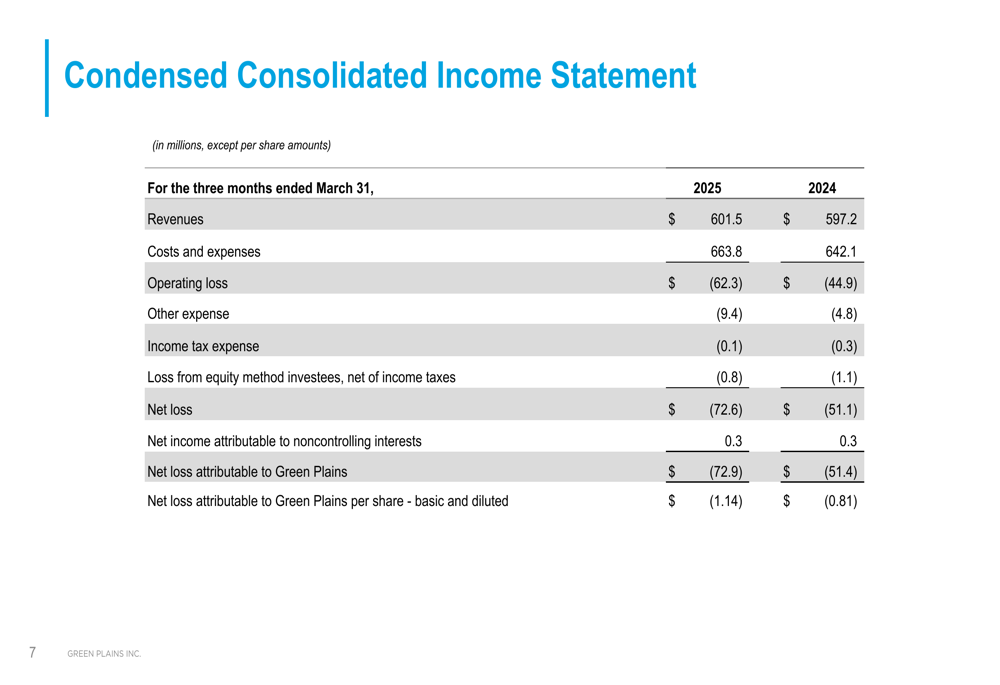

Green Plains’ first quarter results revealed significant financial challenges despite maintaining strong production levels. The company reported revenues of $601.5 million, a slight increase from $597.2 million in Q1 2024, but costs and expenses rose more substantially to $663.8 million from $642.1 million year-over-year.

As shown in the company’s quarterly results summary:

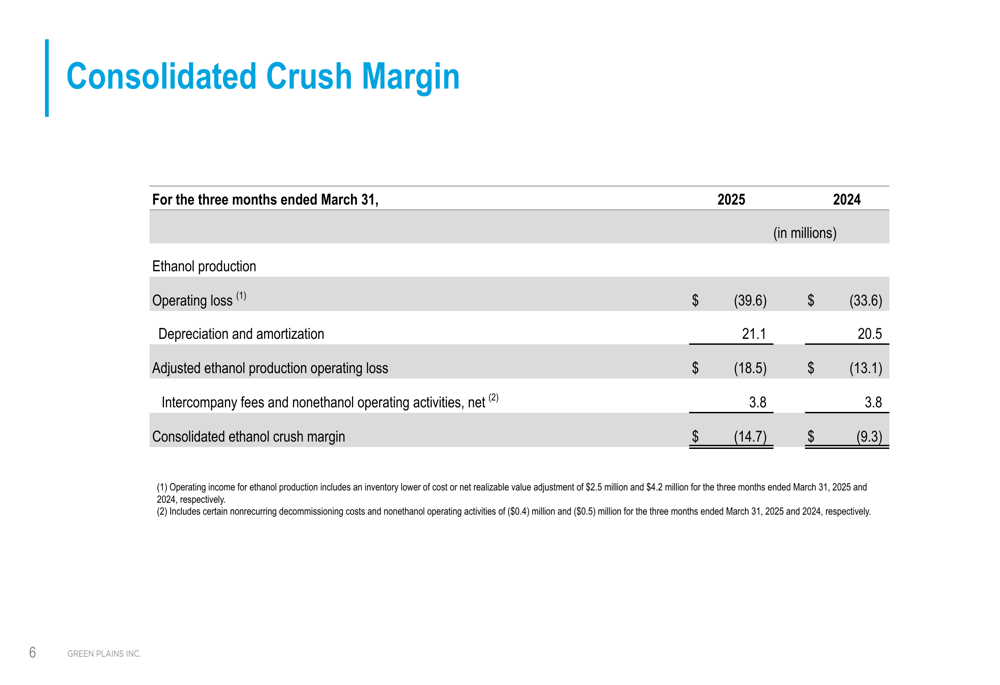

The company’s adjusted EBITDA deteriorated to $(24.2) million, while its consolidated ethanol crush margin worsened to $(14.7) million compared to $(9.3) million in the first quarter of 2024. Despite these challenges, Green Plains maintained strong production metrics, with ethanol production at 195.3 million gallons, representing 100% of capacity (excluding the Fairmont facility).

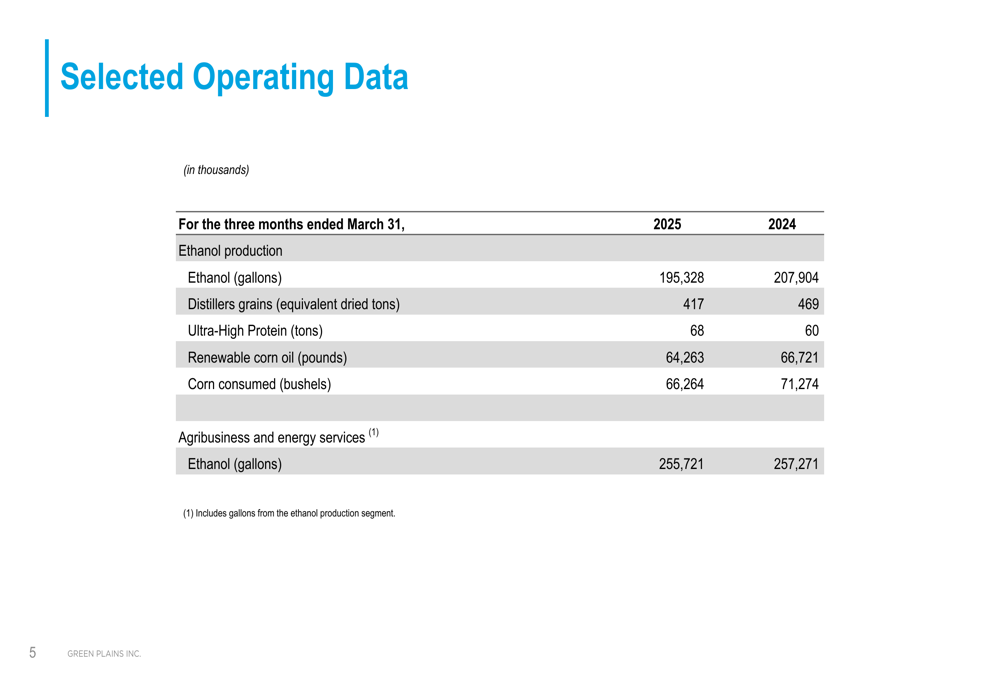

The company’s operational data shows mixed results compared to the previous year:

While ethanol production volumes decreased compared to Q1 2024, Ultra-High Protein production increased to 68,000 tons from 60,000 tons in the prior year, demonstrating progress in the company’s protein strategy despite financial headwinds.

Strategic Initiatives

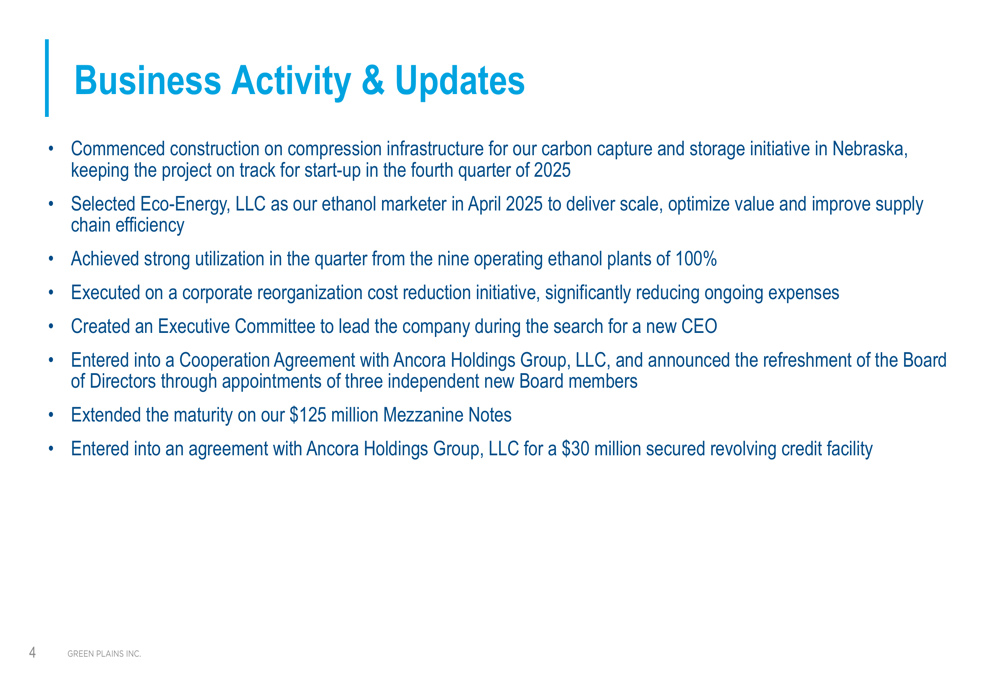

Despite financial challenges, Green Plains continues to advance several strategic initiatives aimed at transforming and stabilizing the business. The company commenced construction on compression infrastructure for its carbon capture and storage project in Nebraska, which remains on track for startup in Q4 2025. This initiative is expected to generate significant carbon credit revenues once operational.

The company also executed a corporate reorganization and cost reduction initiative while creating an Executive Committee to lead during its ongoing CEO search. Additionally, Green Plains entered into a Cooperation Agreement with Ancora Holdings Group, LLC, which resulted in three new independent board members.

Key business updates include:

The company also secured additional financial flexibility by extending the maturity on $125 million in Mezzanine Notes and entering into a $30 million secured revolving credit facility with Ancora Holdings Group. These financial maneuvers appear designed to provide runway as the company works through its current challenges.

Detailed Financial Analysis

Green Plains’ income statement reveals the extent of the company’s financial challenges in Q1 2025. Operating loss increased to $(62.3) million from $(44.9) million in the prior year period, while other expenses nearly doubled to $(9.4) million from $(4.8) million.

The consolidated income statement provides a comprehensive view of the deteriorating financial performance:

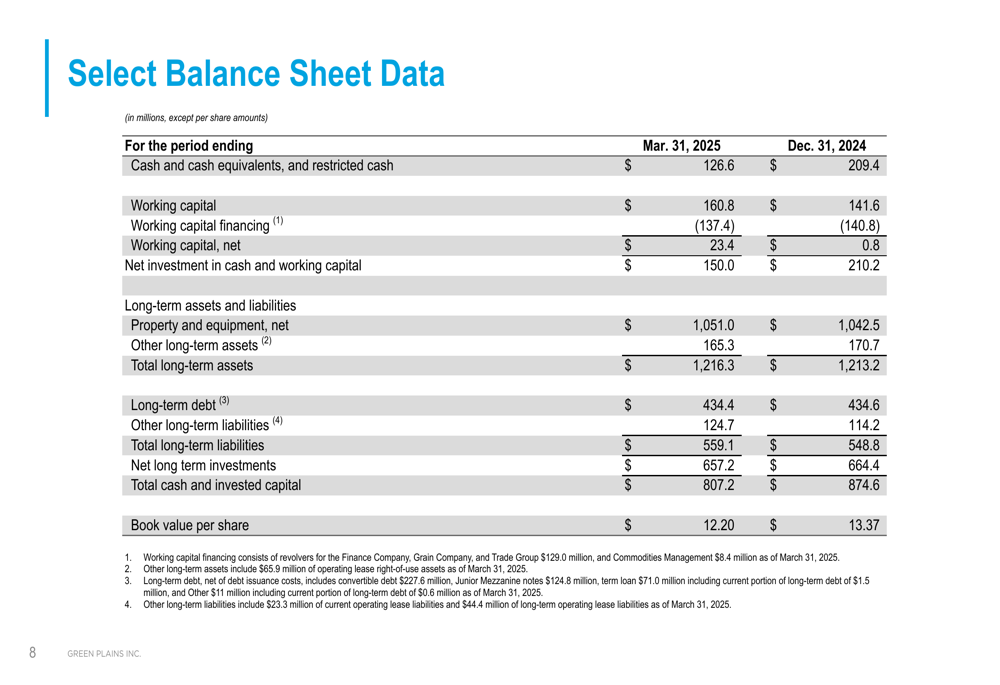

The company’s balance sheet also shows concerning trends, with cash and cash equivalents declining to $126.6 million as of March 31, 2025, compared to $209.4 million at the end of 2024. Book value per share fell to $12.20 from $13.37 over the same period.

Key balance sheet metrics include:

The company’s consolidated crush margin, a critical metric for profitability in the ethanol industry, showed significant deterioration:

This worsening crush margin highlights the challenging market conditions facing Green Plains, with operating losses in ethanol production increasing despite relatively stable production volumes.

Forward-Looking Statements

Green Plains’ carbon capture initiative remains a key component of its future strategy, with the company maintaining its timeline for startup in Q4 2025. This aligns with previous statements from Q3 2024 that projected significant earnings from carbon credits starting in late 2025.

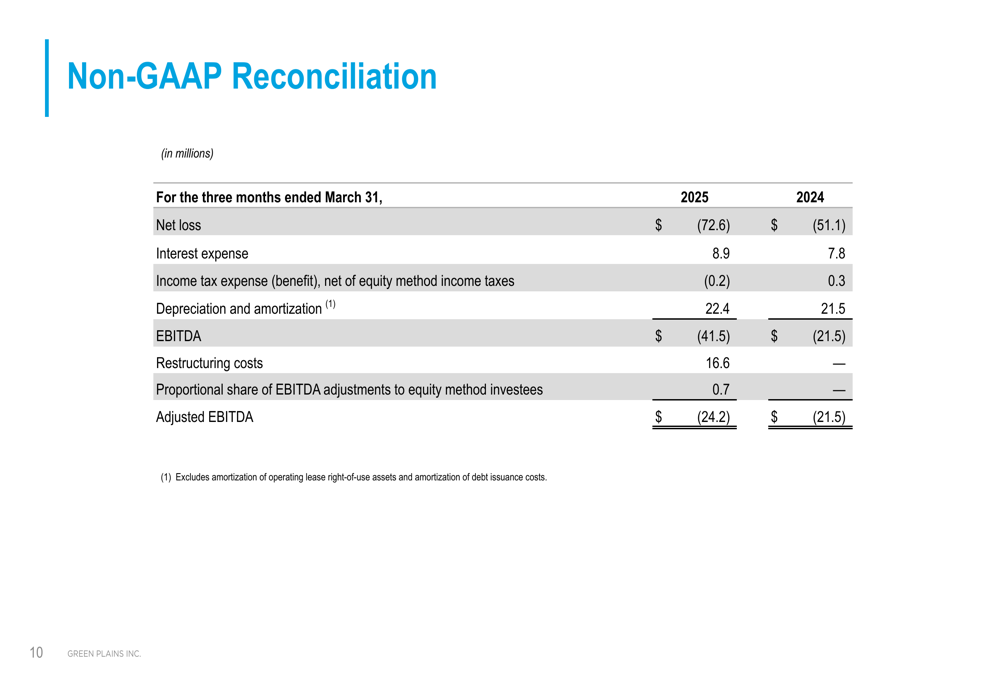

The company’s non-GAAP reconciliation provides insight into the adjustments made to calculate adjusted EBITDA, including significant restructuring costs:

The $16.6 million in restructuring costs in Q1 2025 reflects the company’s efforts to realign its operations amid financial challenges. Despite these adjustments, adjusted EBITDA still deteriorated year-over-year, highlighting the fundamental challenges facing the business.

Green Plains faces a critical period as it navigates leadership transition, implements cost reduction initiatives, and advances strategic projects like carbon capture while dealing with challenging market conditions in its core ethanol business. The significant stock price decline over the past year reflects investor concerns about the company’s path to profitability, despite its continued operational achievements in areas like Ultra-High Protein production.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.