Asia tech stocks slide tracking Wall St losses amid AI doubts, govt. uncertainty

Introduction & Market Context

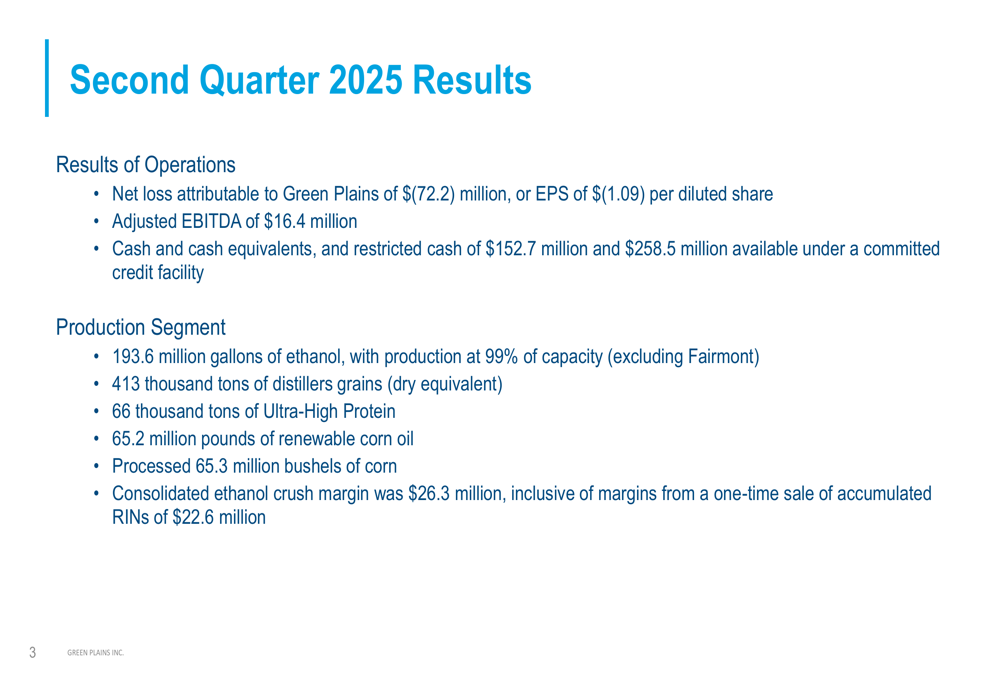

Green Plains Inc. (NASDAQ:GPRE) presented its second quarter 2025 business update on August 11, 2025, revealing a continued net loss but showing significant improvement in operational performance. The renewable fuels producer reported a net loss of $72.2 million, or $1.09 per diluted share, while achieving positive Adjusted EBITDA of $16.4 million. In premarket trading, Green Plains shares were up 2.16% to $7.56, suggesting investors are responding positively to signs of operational improvement despite the ongoing financial challenges.

The company has been working to reposition itself from a traditional ethanol producer to a more diversified renewable products company with a strong focus on decarbonization initiatives and higher-margin products. This strategic shift comes as the renewable fuels industry faces both challenges and opportunities in a rapidly evolving energy landscape.

Quarterly Performance Highlights

Green Plains reported second quarter 2025 revenues of $552.8 million, down from $618.8 million in the same period last year. Despite the revenue decline, the company achieved several operational milestones, including production at 99% of capacity (excluding the Fairmont facility) and a consolidated ethanol crush margin of $26.3 million, which included $22.6 million from a one-time sale of accumulated RINs.

As shown in the following financial results summary:

The company’s production segment processed 65.3 million bushels of corn and produced 193.6 million gallons of ethanol, 413 thousand tons of distillers grains, 66 thousand tons of Ultra-High Protein, and 65.2 million pounds of renewable corn oil.

Cash and cash equivalents stood at $152.7 million at quarter-end, with an additional $258.5 million available under committed credit facilities, providing substantial liquidity for ongoing operations and strategic initiatives.

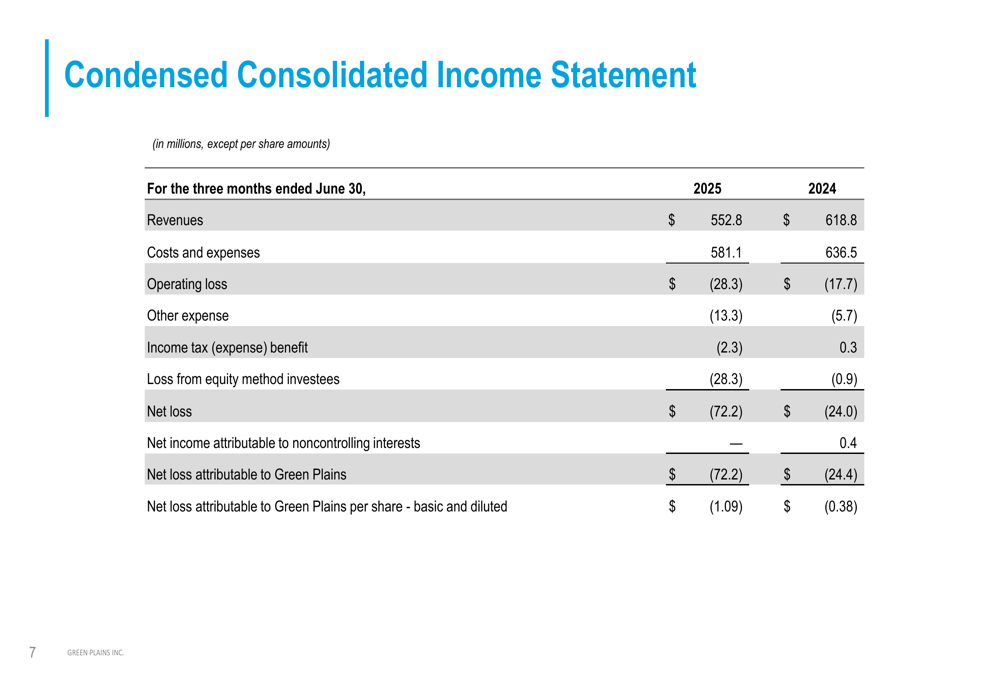

The company’s consolidated income statement reveals the extent of the financial challenges:

While the $72.2 million net loss represents a significant deterioration from the $24.0 million loss in Q2 2024, it’s worth noting that $27.0 million of the current loss came from the sale of an equity method investment, and the company recorded a $10.7 million impairment of assets held for sale.

Strategic Initiatives

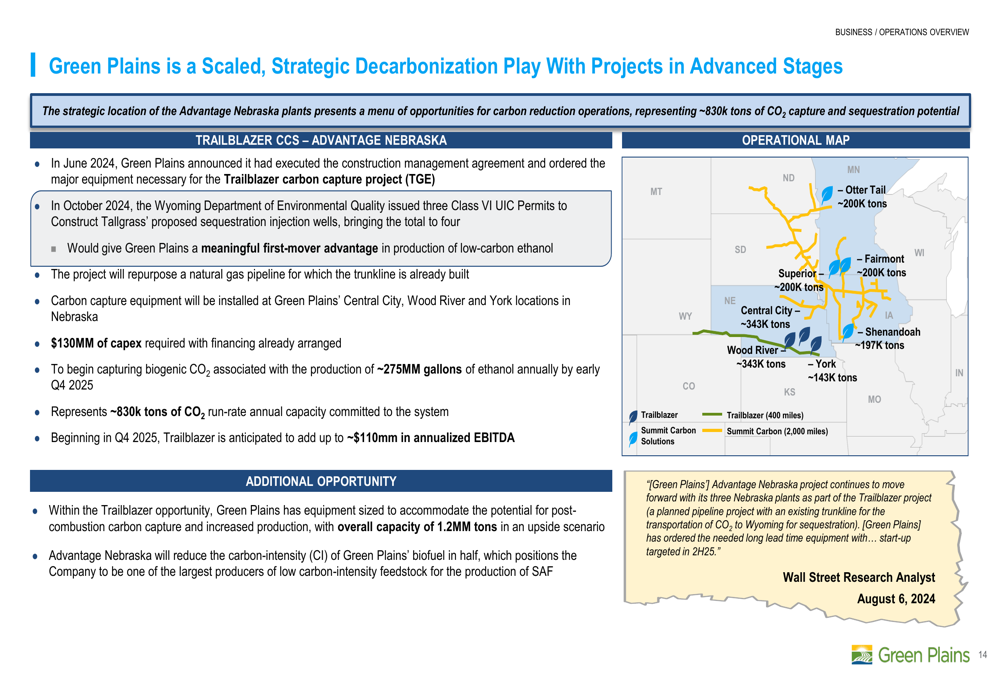

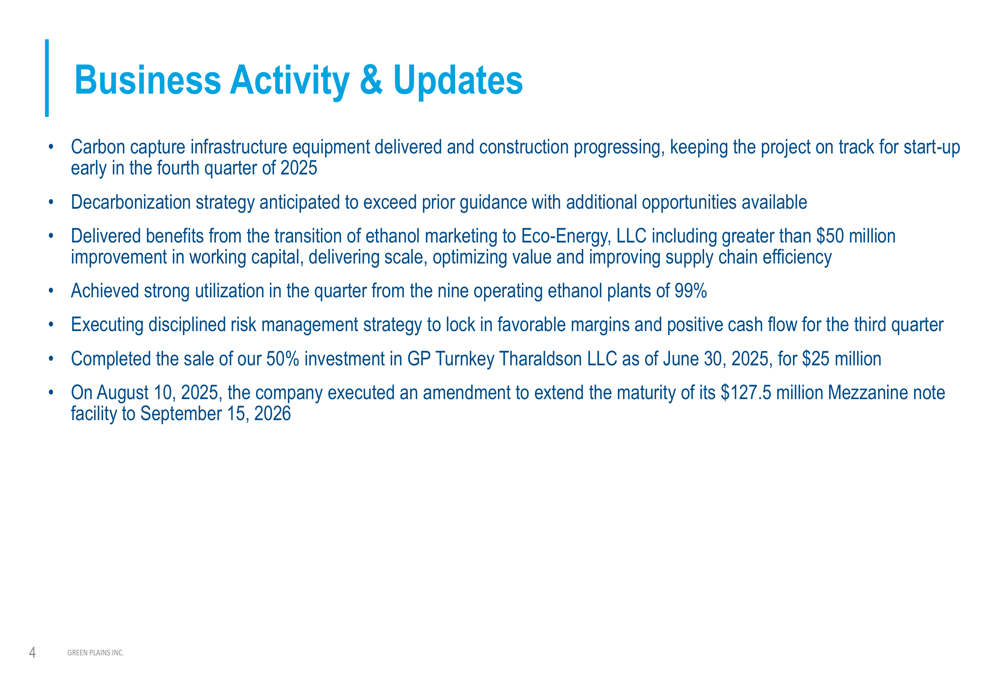

Green Plains continues to advance its strategic transformation, with particular emphasis on decarbonization projects and high-margin product development. The company’s carbon capture infrastructure construction is progressing on schedule, with startup expected in early Q4 2025.

The following slide illustrates Green Plains’ positioning as a decarbonization leader:

The Trailblazer carbon capture and sequestration (CCS) project is expected to capture biogenic CO2 from approximately 275 million gallons of ethanol annually, representing about 830,000 tons of CO2 run-rate annual capacity. Once operational in Q4 2025, management anticipates this project will add up to $110 million in annualized EBITDA.

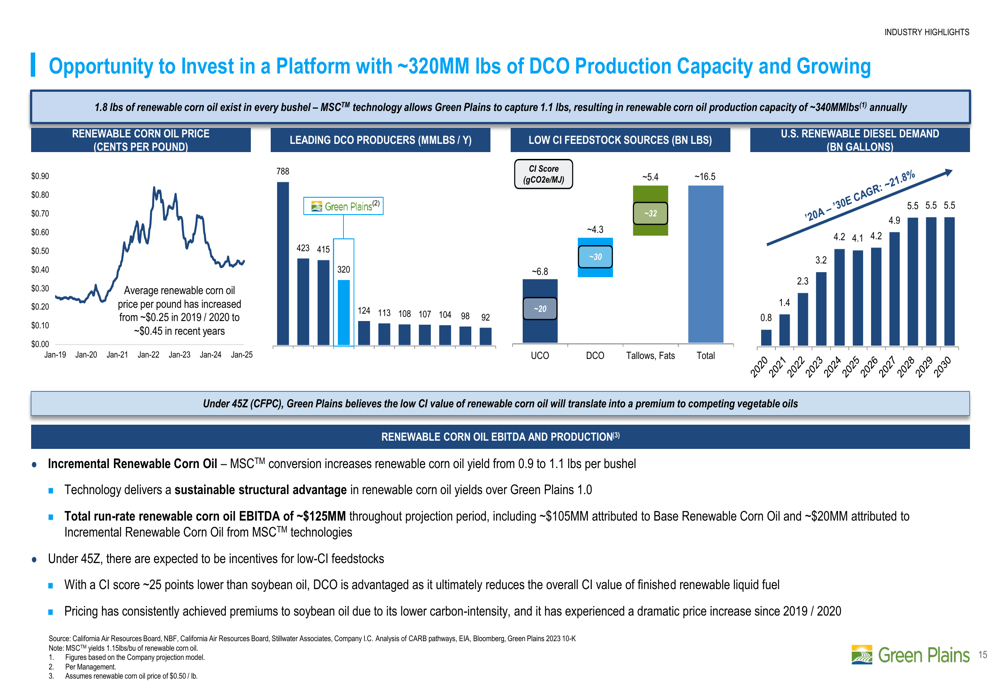

Green Plains is also expanding its renewable corn oil (RCO) production, positioning itself as a key supplier to the growing renewable diesel industry:

With RCO prices having increased from approximately $0.25 per pound in 2019/2020 to around $0.45 in recent years, and U.S. renewable diesel demand projected to grow from 0.8 billion gallons in 2020 to 5.5 billion gallons by 2030, this represents a significant growth opportunity. The company expects its total run-rate renewable corn oil EBITDA to reach approximately $125 million throughout the projection period.

Detailed Financial Analysis

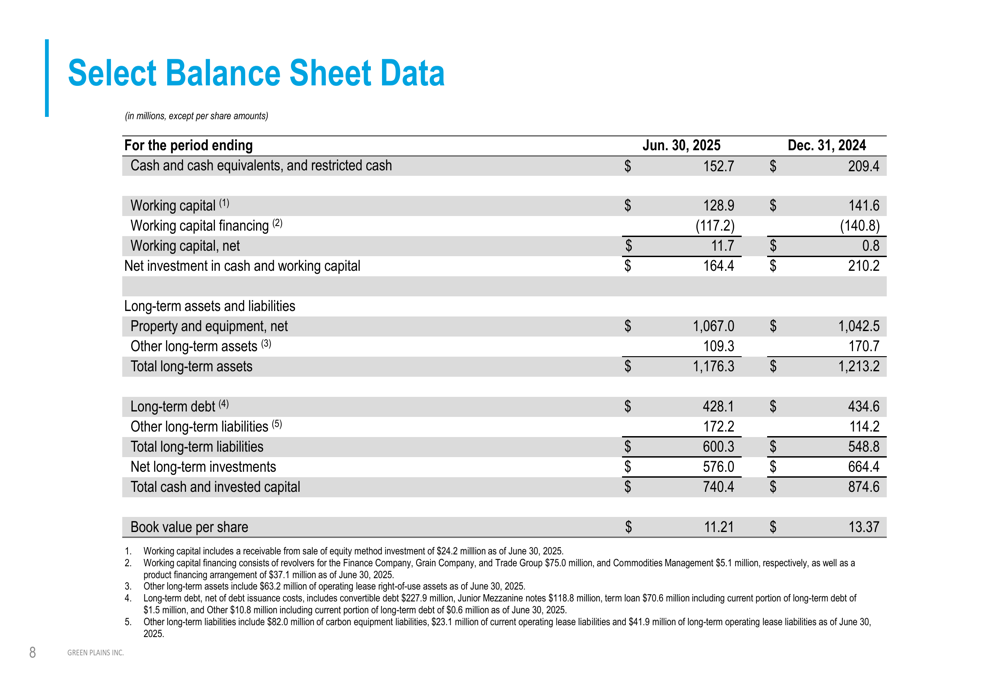

Green Plains’ balance sheet shows some improvement in working capital management, with net working capital increasing to $11.7 million from $0.8 million at the end of 2024. However, book value per share declined to $11.21 from $13.37 over the same period.

The following balance sheet data provides additional context:

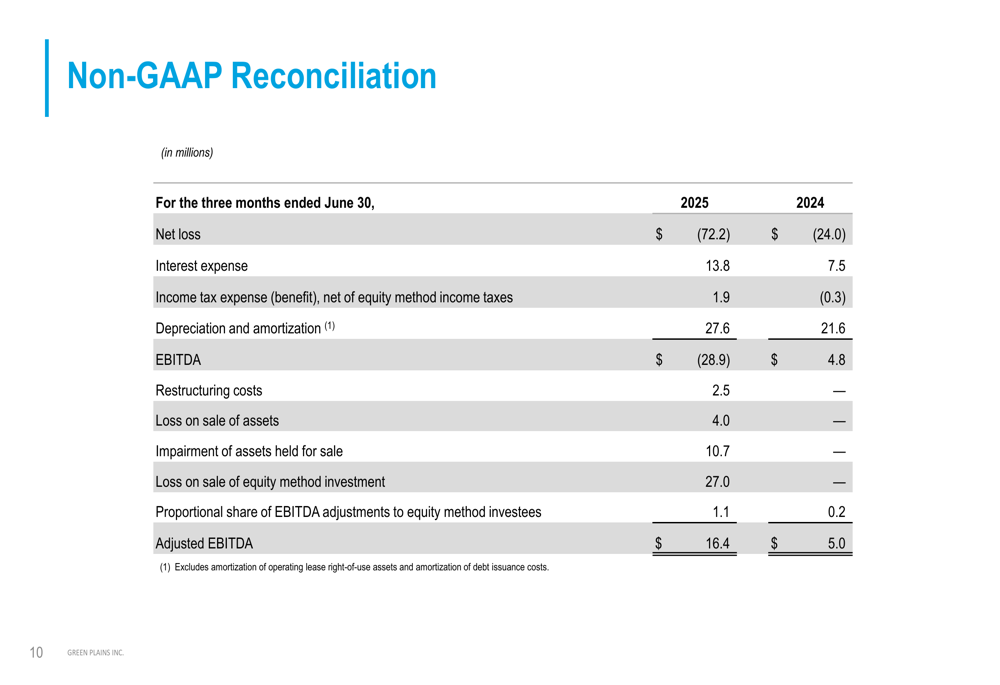

The company’s non-GAAP reconciliation reveals the components contributing to the positive Adjusted EBITDA of $16.4 million, a significant improvement from $5.0 million in Q2 2024:

This improvement in Adjusted EBITDA represents a dramatic turnaround from the negative $24.2 million reported in Q1 2025, suggesting that operational improvements are beginning to take effect despite the continued net losses.

Forward-Looking Statements

Green Plains has made several strategic moves to strengthen its financial position, including completing the sale of its 50% investment in GP Turnkey Tharaldson LLC for $25 million and executing an amendment to extend the maturity of its $127.5 million Mezzanine note facility to September 15, 2026.

The company’s business update highlighted several ongoing initiatives:

The transition of ethanol marketing to Eco-Energy, LLC has delivered benefits including a greater than $50 million improvement in working capital, while the company’s disciplined risk management strategy aims to lock in favorable margins and positive cash flow for the third quarter.

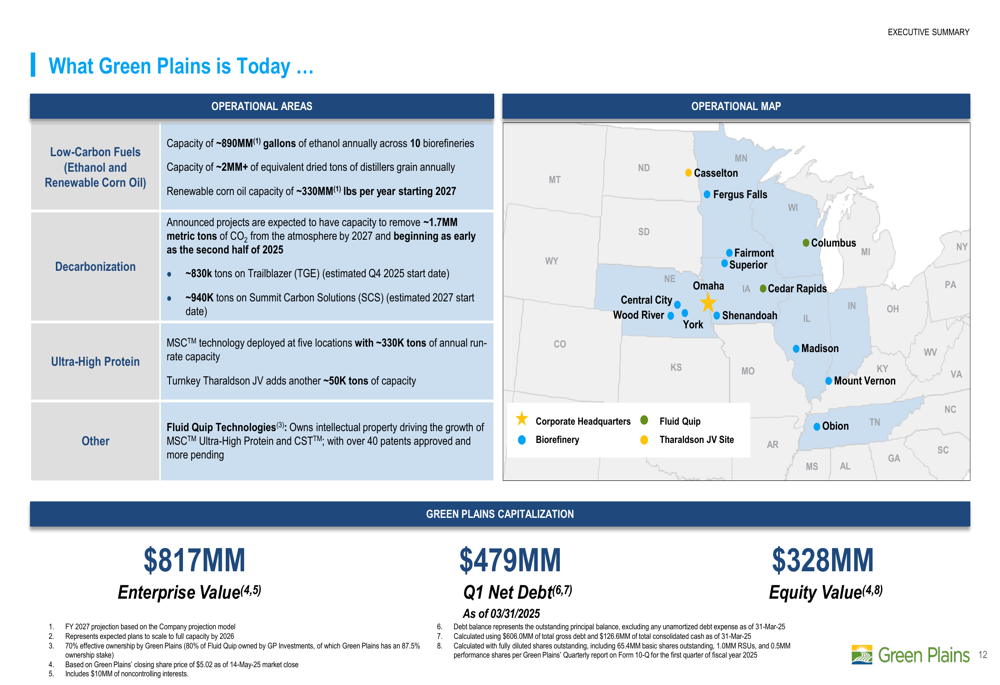

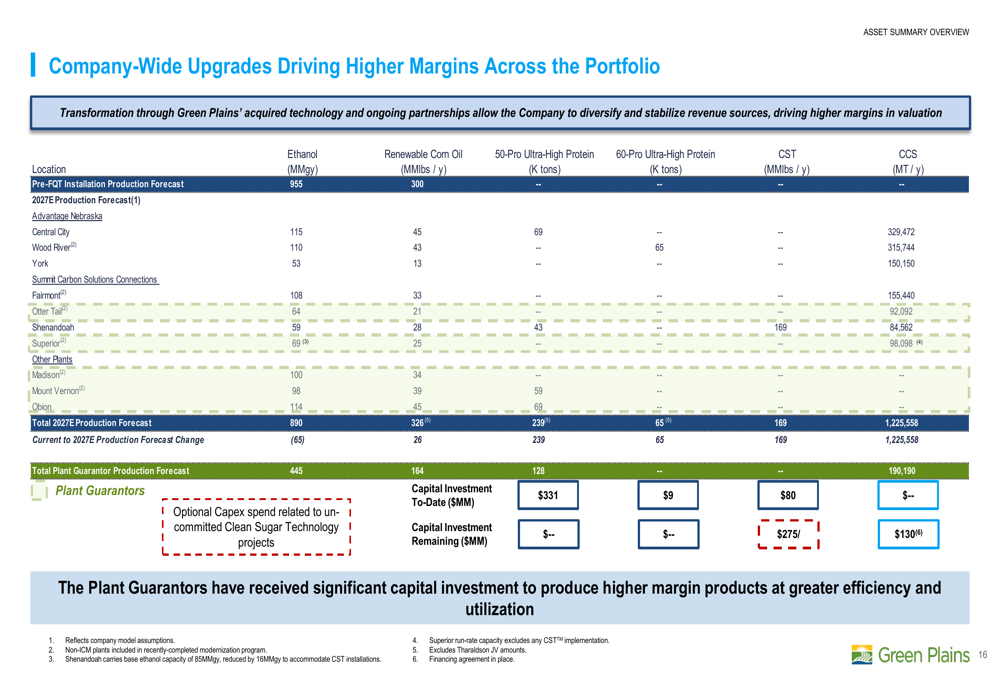

Green Plains continues to execute on its transformation strategy, as illustrated in this comprehensive asset overview:

With ethanol capacity of approximately 890 million gallons annually across 10 biorefineries, and projects expected to remove 1.7 million metric tons of CO2 by 2027, Green Plains is positioning itself as a leader in the renewable fuels industry’s transition toward lower-carbon, higher-margin operations.

The company’s ongoing investments in facility upgrades are designed to drive higher margins across its portfolio:

These upgrades focus on using Green Plains’ acquired technology and ongoing partnerships to improve production efficiency and product quality, particularly in its Ultra-High Protein and renewable corn oil segments.

While Green Plains continues to face financial challenges, the Q2 2025 presentation suggests that the company’s strategic transformation is progressing, with operational improvements beginning to show in the financial results. Investors will be watching closely to see if these positive trends continue in the coming quarters, particularly as the carbon capture infrastructure comes online in late 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.