Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Greif Bros Corporation (NYSE:GEF) presented its second quarter 2025 earnings results on June 5, showing significant improvement in profitability metrics despite mixed volume performance across its business segments. The industrial packaging manufacturer reported substantial gains in Adjusted EBITDA and Free Cash Flow, leading management to raise the company’s full-year guidance.

The presentation comes after a challenging first quarter where Greif missed earnings expectations but has since demonstrated resilience through its cost optimization initiatives and strategic positioning in growth markets. The company’s stock, which closed at $55.76 on June 4, showed a 1.24% increase in aftermarket trading following the earnings announcement.

Quarterly Performance Highlights

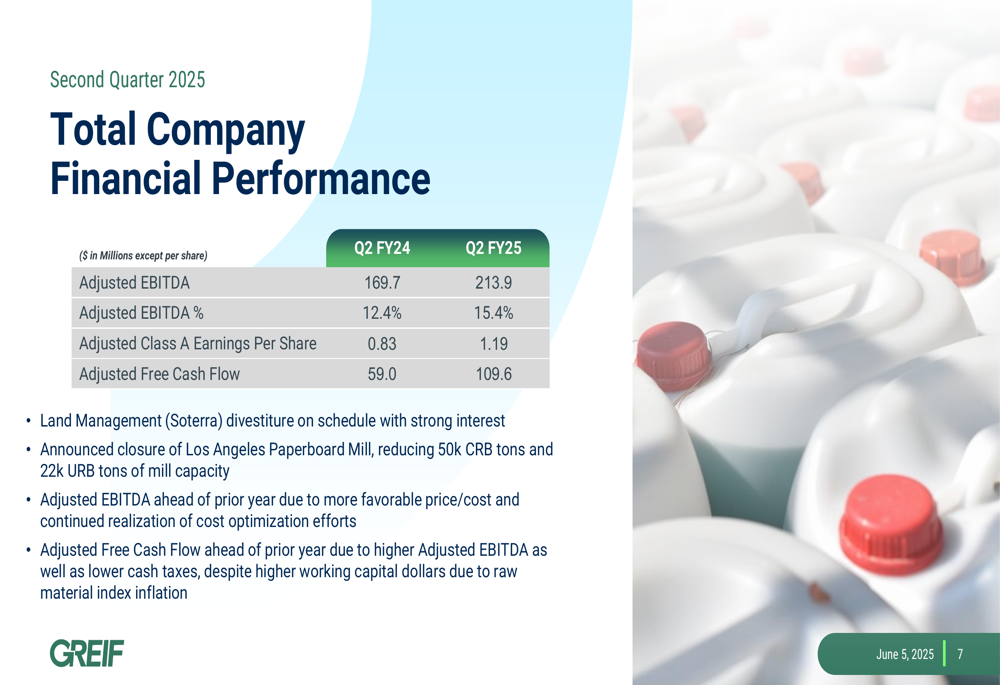

Greif reported substantial year-over-year improvements in its key financial metrics for Q2 2025. Adjusted EBITDA increased to $213.9 million, up 26% from $169.7 million in Q2 2024, while the Adjusted EBITDA margin expanded to 15.4% from 12.4% in the prior year period.

As shown in the following financial performance summary:

Adjusted Class A Earnings Per Share rose to $1.19 from $0.83 in the same quarter last year, representing a 43% increase. The company also reported Adjusted Free Cash Flow of $109.6 million, nearly doubling from $59.0 million in Q2 2024. Management attributed these improvements to a more favorable price/cost environment and continued realization of cost optimization efforts.

The strong Q2 results mark a significant recovery from the company’s Q1 2025 performance, when it reported an adjusted EPS of just $0.39, well below analyst expectations of $0.75.

Segment Performance Analysis

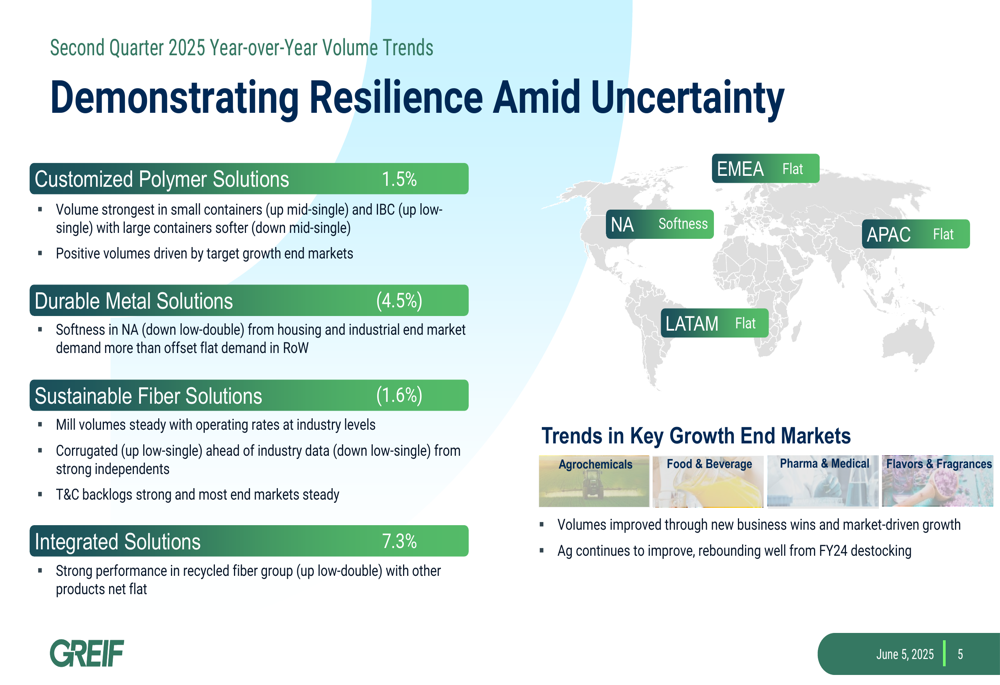

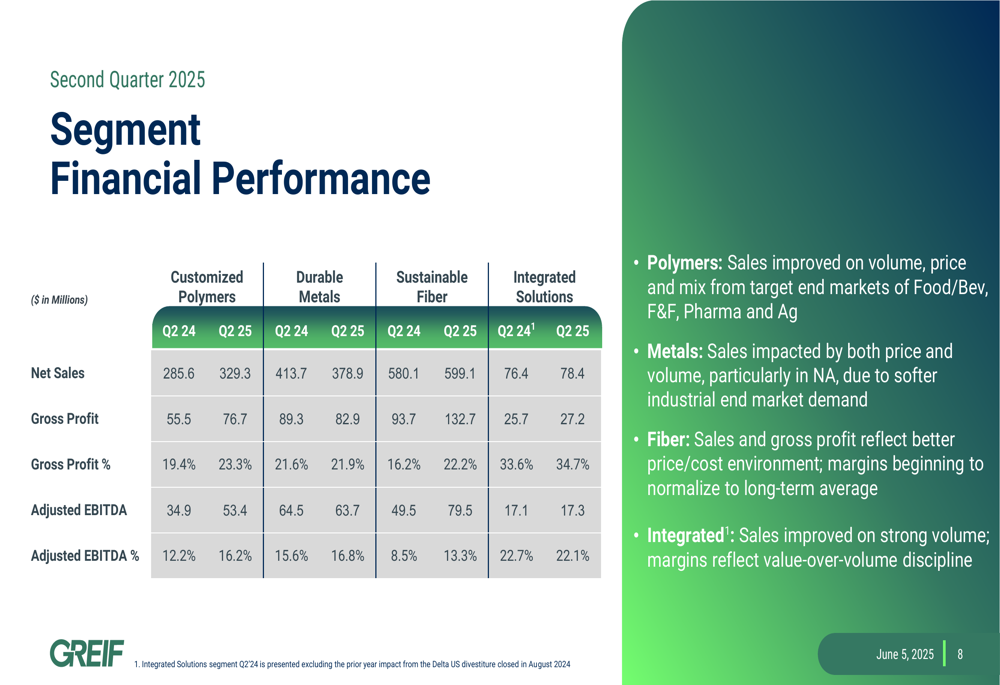

Greif’s volume performance varied significantly across its four business segments, reflecting different market dynamics. The company’s Integrated Solutions segment led growth with a 7.3% volume increase, while Customized Polymer Solutions grew modestly at 1.5%. However, both Durable Metal Solutions and Sustainable Fiber Solutions experienced volume declines of 4.5% and 1.6%, respectively.

The following chart illustrates these volume trends and highlights key growth markets:

Despite the mixed volume performance, all segments showed improved profitability metrics. The segment financial breakdown reveals the details of this performance:

Notably, the Sustainable Fiber Solutions segment showed significant improvement in gross profit and Adjusted EBITDA despite lower volumes, reflecting a better price/cost environment. The Integrated Solutions segment capitalized on strong volume growth to deliver improved results, while Customized Polymers benefited from volume, price, and mix improvements in target end markets.

Strategic Initiatives

Greif continues to make progress on its $100 million cost reduction plan, which aims to optimize its cost base by 2027. The company reported achieving $10 million in run-rate savings as of Q2 2025, on track toward its fiscal year 2025 commitment of $15-25 million.

The cost reduction strategy focuses on three key areas as illustrated below:

The company also announced the closure of its Los Angeles Paperboard Mill, which will reduce capacity by 50,000 CRB tons and 22,000 URB tons. Additionally, Greif reported that the divestiture of its Land Management business (Soterra) is proceeding on schedule with strong interest from potential buyers.

Greif highlighted its ability to manage tariff impacts through its extensive global footprint of over 250 facilities, which results in predominantly local-to-local business. The company anticipates a maximum annual impact of $10 million from tariffs before mitigating actions.

The company continues to strengthen its competitive advantages through employee engagement, customer service excellence, and sustainability initiatives. Greif received the Gallup Exceptional Workplace Award in 2025, ranking in the 86th percentile for manufacturing employee engagement, and was recognized with a 2024 Supplier Innovation Award from the United States Postal Service.

Forward-Looking Statements

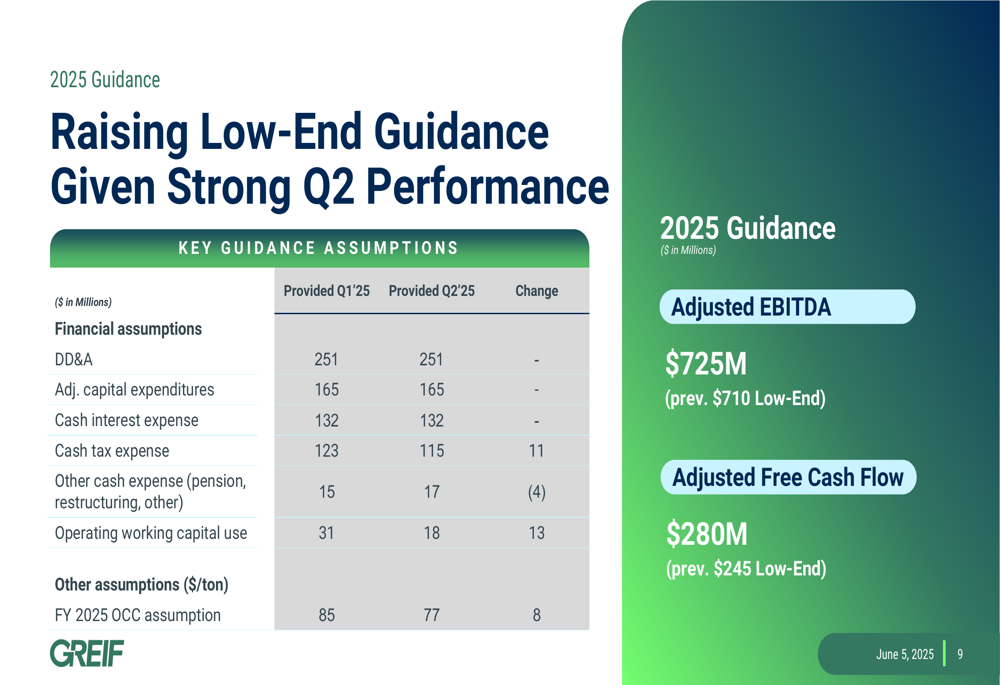

Based on its strong second-quarter performance, Greif has raised the low end of its fiscal year 2025 guidance. The company now expects Adjusted EBITDA of $725 million, up from the previous low-end guidance of $710 million. Similarly, Adjusted Free Cash Flow guidance has been increased to $280 million from the previous low-end estimate of $245 million.

The updated guidance reflects several key assumptions as detailed below:

Management noted that recent raw material inflation in response to trade uncertainty is expected to present near-term tailwinds to Adjusted EBITDA margins. The company also highlighted its key growth end markets, including Agrochemicals, Food & Beverage, Pharma & Medical (TASE:BLWV), and Flavors & Fragrances, with agricultural markets continuing to improve and rebounding from fiscal year 2024 destocking.

Greif’s investment thesis centers on its position as a packaging leader serving essential industries, its improved earnings power through ongoing mix shift to higher growth and less cyclical businesses, and its proactive capital allocation strategy. The company emphasizes its consistent return of cash to shareholders and disciplined approach to mergers and acquisitions.

With its global footprint, diversified business segments, and ongoing cost optimization initiatives, Greif appears well-positioned to navigate market challenges while continuing to improve profitability metrics through the remainder of fiscal year 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.