Street Calls of the Week

Introduction & Market Context

Greif, Inc. (NYSE:GEF) presented its third quarter 2025 earnings results on August 28, 2025, highlighting significant portfolio transformation initiatives and improved financial performance despite challenging market conditions in certain regions. The industrial packaging manufacturer is executing major divestments while focusing on margin expansion and cost optimization efforts.

The company’s stock closed at $66.33 on August 27, down 0.69% for the day, but showed signs of recovery with a 0.63% gain in after-hours trading. This follows an 8.95% surge after its Q2 earnings release earlier this year, when the company first signaled its improved outlook.

Portfolio Transformation

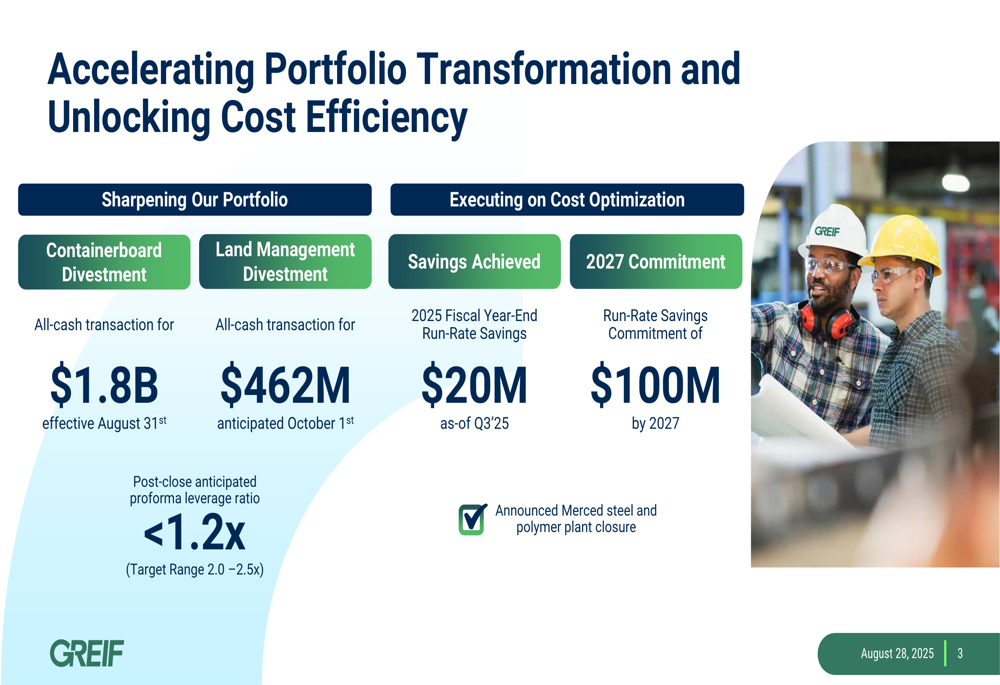

Greif announced two major divestments that will significantly reshape its business portfolio. The company has reached an agreement to sell its Containerboard Business to Packaging Corporation of America for $1.8 billion in an all-cash transaction, effective August 31, 2025. Additionally, Greif plans to divest its Land Management business for $462 million, with that transaction anticipated to close on October 1st.

These strategic moves align with management’s focus on higher-margin, less cyclical businesses. The company expects its post-close proforma leverage ratio to be less than 1.2x, well below its target range of 2.0-2.5x, providing significant financial flexibility.

As shown in the following strategic transformation slide:

The company is also making progress on its cost optimization program, having achieved $20 million in savings as of Q3 2025, with a commitment to reach $100 million by 2027. As part of these efforts, Greif announced the closure of its Merced, California steel and polymer plant.

Quarterly Performance Highlights

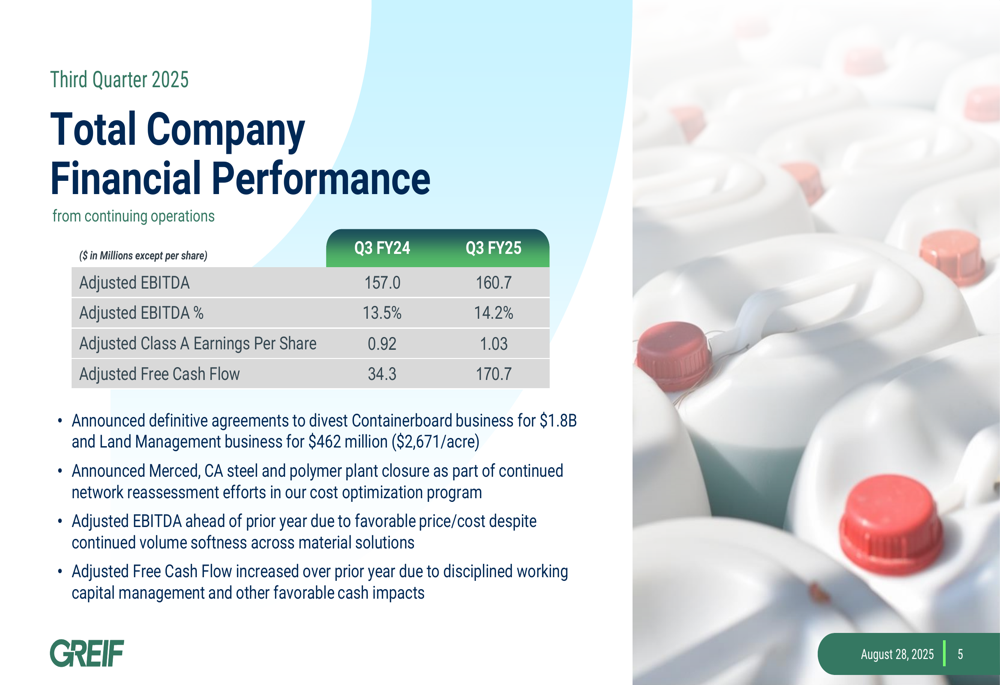

Despite volume challenges in some segments, Greif delivered improved financial results for the third quarter of 2025. Adjusted EBITDA reached $160.7 million, up from $157.0 million in the same period last year, while the adjusted EBITDA margin expanded to 14.2% from 13.5%. Adjusted Class A earnings per share increased to $1.03 from $0.92 in Q3 FY24.

The company’s adjusted free cash flow showed remarkable improvement, reaching $170.7 million compared to just $34.3 million in the prior-year period, demonstrating strong operational execution and working capital management.

The following slide illustrates these key financial metrics:

Detailed Financial Analysis

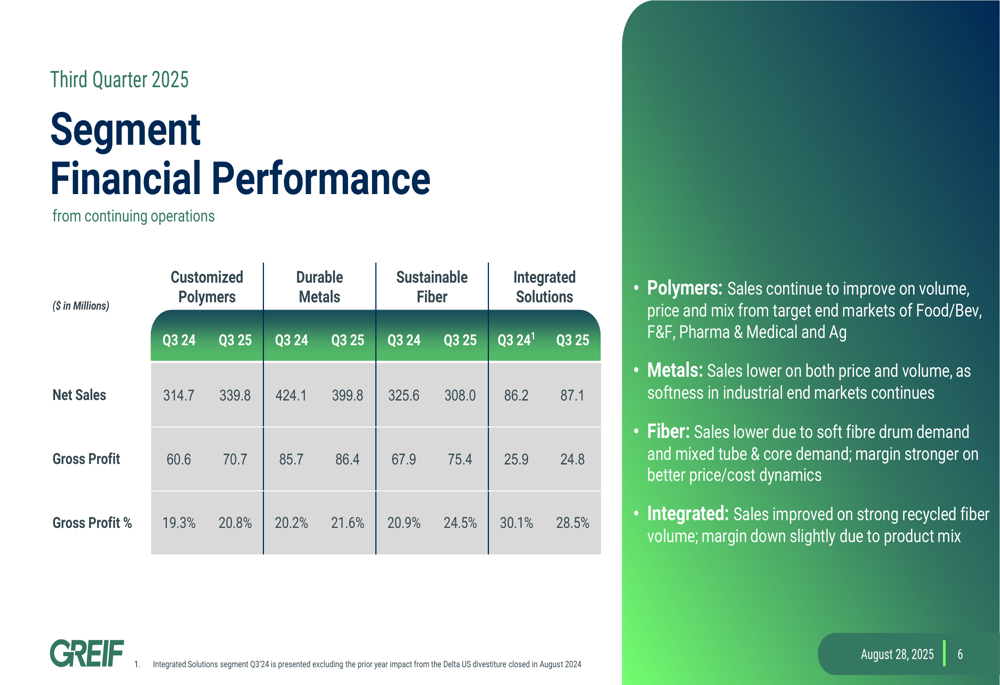

Greif’s performance varied across its business segments, reflecting different market dynamics. The Customized Polymers segment saw net sales increase from $314.7 million to $339.8 million, with gross profit rising from $60.6 million to $70.7 million, expanding gross margin to 20.8% from 19.3%.

The Durable Metals segment experienced a sales decline from $424.1 million to $399.8 million due to lower volumes and pricing, but still managed to improve gross profit to $86.4 million from $85.7 million, with margin expansion to 21.6% from 20.2%.

Sustainable Fiber Solutions also faced volume challenges with sales decreasing to $308.0 million from $325.6 million, yet delivered significant margin improvement with gross profit increasing to $75.4 million from $67.9 million, pushing gross margin to 24.5% from 20.9%.

The segment breakdown is detailed in this financial performance slide:

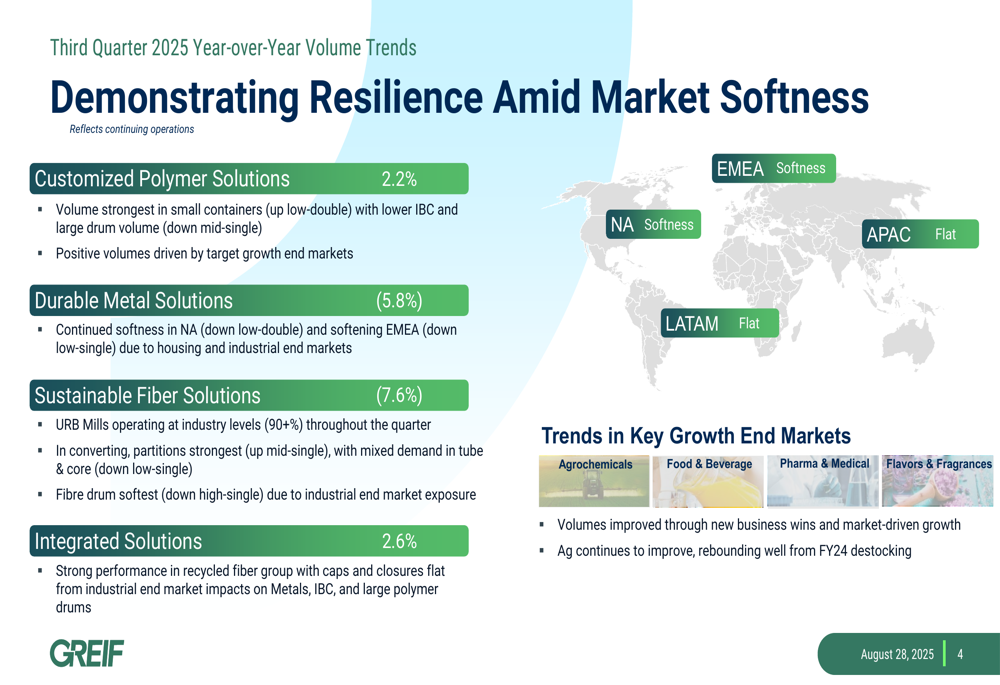

Volume trends varied significantly across segments, with Customized Polymer Solutions growing 2.2% and Integrated Solutions up 2.6%, while Durable Metal Solutions declined 5.8% and Sustainable Fiber Solutions fell 7.6%. Geographically, both North America and EMEA experienced market softness, while Latin America and Asia Pacific markets remained flat.

The following slide shows these volume trends and regional market conditions:

Forward-Looking Statements

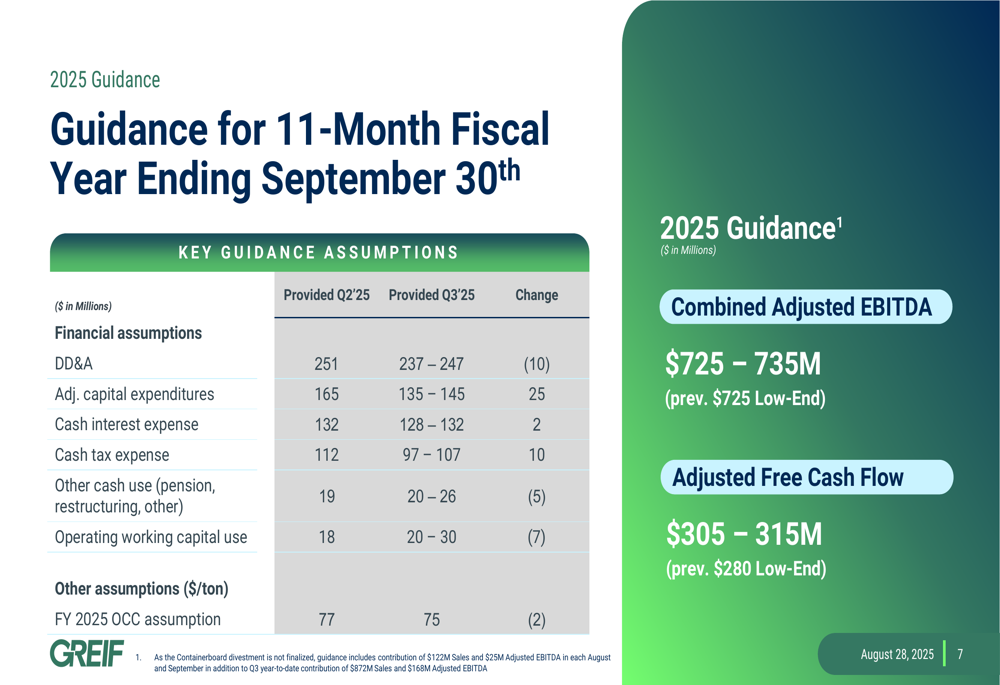

Based on its strong performance, Greif raised its guidance for the 11-month fiscal year ending September 30, 2025. The company now expects combined adjusted EBITDA of $725-735 million, up from its previous guidance of at least $725 million. Adjusted free cash flow guidance was also increased to $305-315 million, compared to the previous floor of $280 million.

Key assumptions for the remainder of the fiscal year include depreciation and amortization between $237-247 million, adjusted capital expenditures of $135-145 million, cash interest expense of $128-132 million, and cash tax expense of $97-107 million.

The updated guidance is presented in this slide:

Strategic Initiatives

Looking beyond the current fiscal year, Greif is positioning itself as a packaging leader to essential industries, with a focus on high-growth end markets including food and beverage, fragrances and flavors, pharmaceutical and medical, and agriculture. The company’s strategy centers on shifting its business mix toward higher-growth, less cyclical segments while driving margin expansion.

Management has set ambitious long-term targets, including achieving an adjusted EBITDA margin of 18%+ and adjusted free cash flow conversion of 50%+. The company also emphasized its commitment to returning cash to shareholders while pursuing disciplined M&A opportunities.

The investment thesis is summarized in this slide:

Executive Summary

Greif’s third quarter 2025 presentation demonstrates the company’s strategic transformation through major divestments and operational improvements. Despite volume challenges in certain segments and regions, the company delivered improved profitability and exceptional free cash flow generation. The raised guidance reflects management’s confidence in the company’s direction and ability to execute on its cost optimization initiatives.

With a strengthened balance sheet following the planned divestments, Greif will have significant financial flexibility to pursue its strategic priorities while returning capital to shareholders. The company’s focus on less cyclical, higher-margin businesses positions it well for sustainable growth and improved returns on capital.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.