AZTR receives NYSE delisting warning over equity requirement

Introduction & Market Context

Grenke AG (ETR:GLJ), a leading provider of financial services for small and medium-sized enterprises (SMEs), presented its Q1 2025 financial results on May 15, 2025. CFO Dr. Martin Paal delivered a presentation highlighting the company’s mixed performance, characterized by strong leasing business growth but declining profitability due to increased risk provisions.

The company maintained its diversified funding structure with senior unsecured debt (38%), Grenke Bank deposits (30%), asset-backed securities (15%), and equity (17%), providing stability amid challenging macroeconomic conditions.

Quarterly Performance Highlights

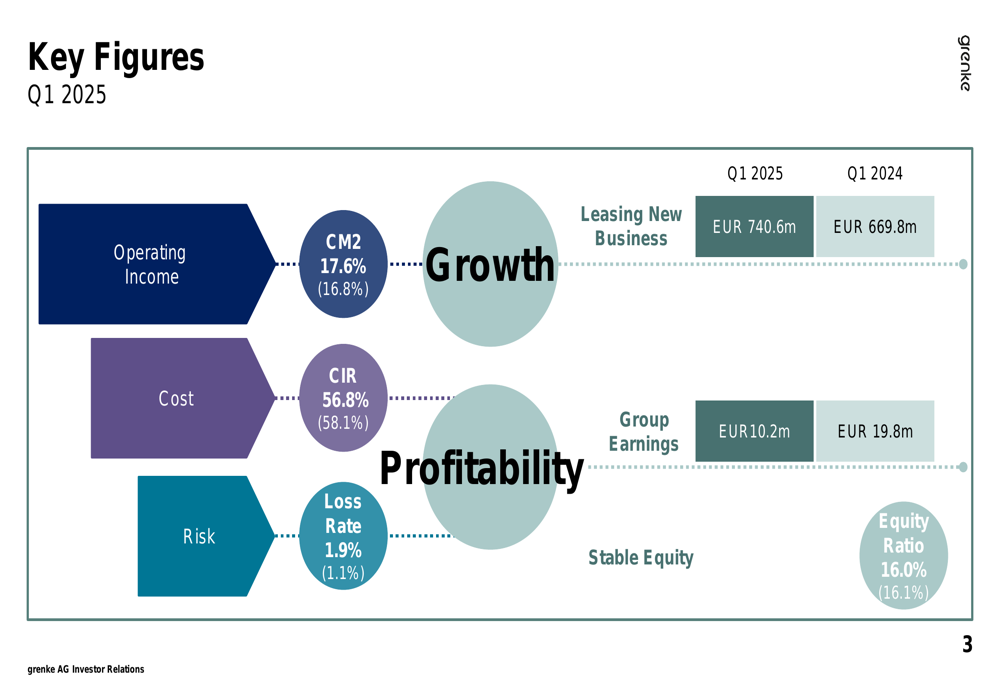

Grenke reported a 10.6% year-over-year increase in leasing new business, reaching EUR 740.6 million in Q1 2025 compared to EUR 669.8 million in Q1 2024. However, group earnings declined significantly to EUR 10.2 million, down 48.5% from EUR 19.8 million in the same period last year.

As shown in the following chart of key financial metrics, the company demonstrated improvements in contribution margin 2 (CM2) and cost income ratio (CIR), but faced challenges with an increased loss rate:

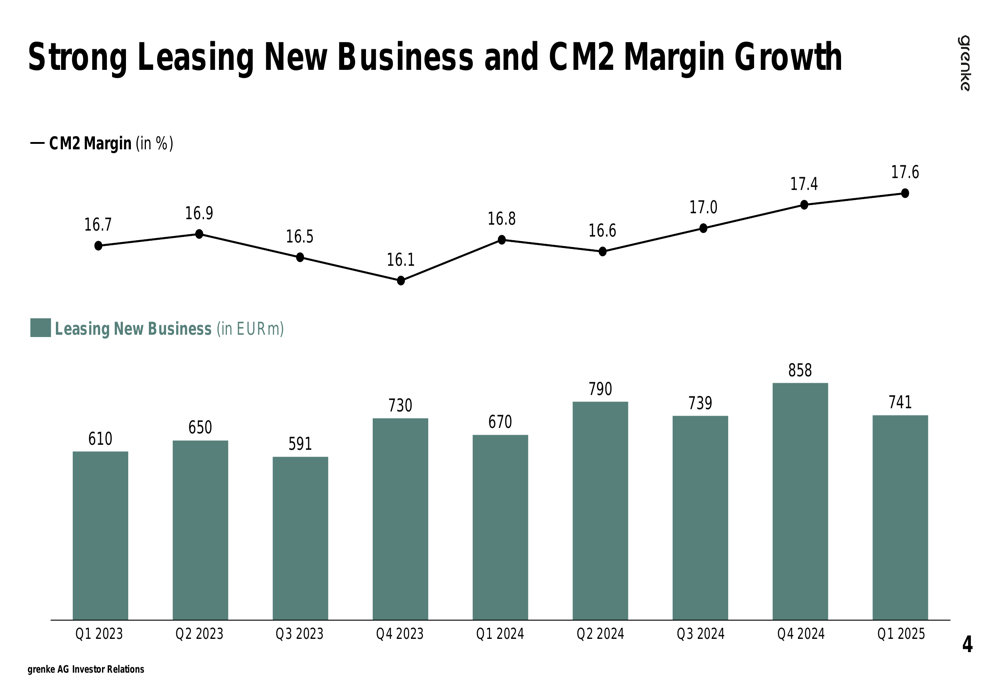

The company’s leasing new business has shown consistent growth over the past nine quarters, with CM2 margin also trending positively, reaching 17.6% in Q1 2025:

Detailed Financial Analysis

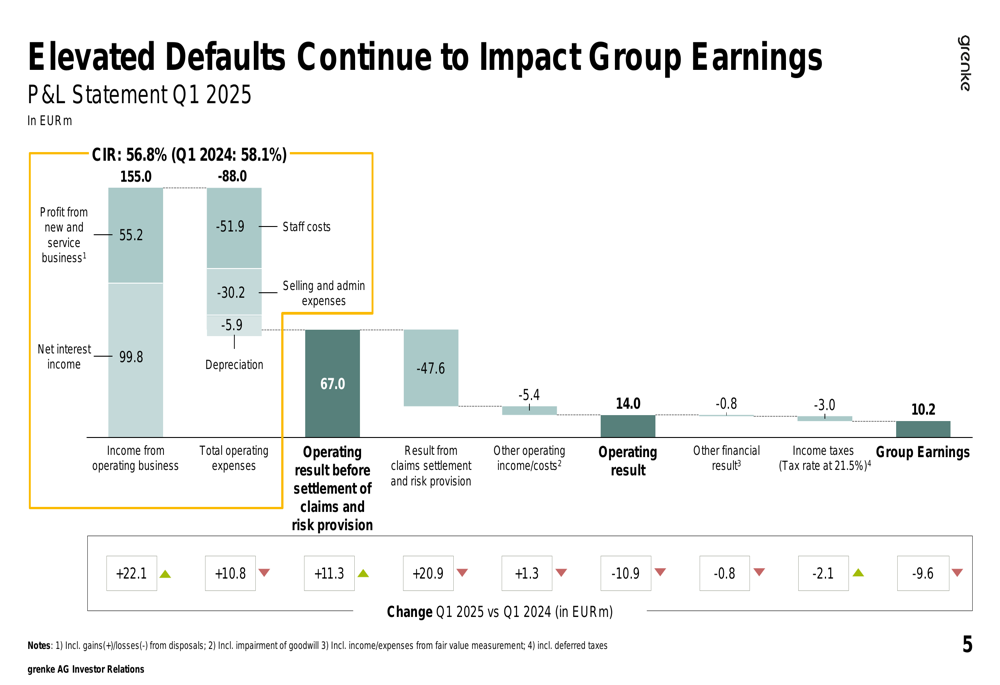

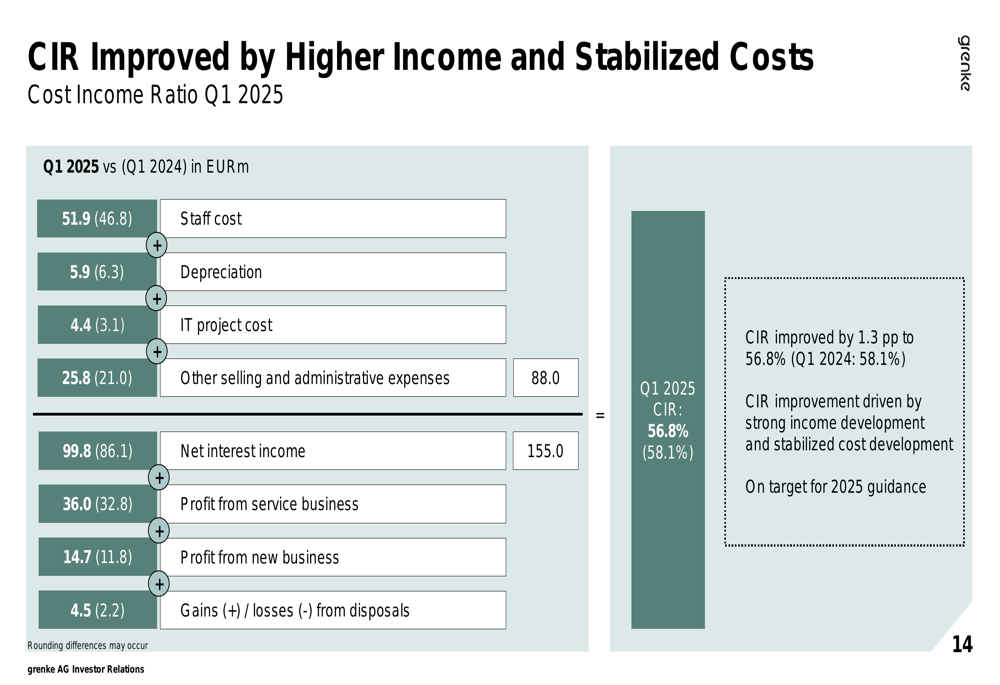

Grenke’s profit and loss statement reveals the primary factors affecting its Q1 performance. While the company improved its operational efficiency with a CIR of 56.8% (down from 58.1% in Q1 2024), the result from claims settlement and risk provision increased substantially to EUR 47.6 million, significantly impacting the bottom line:

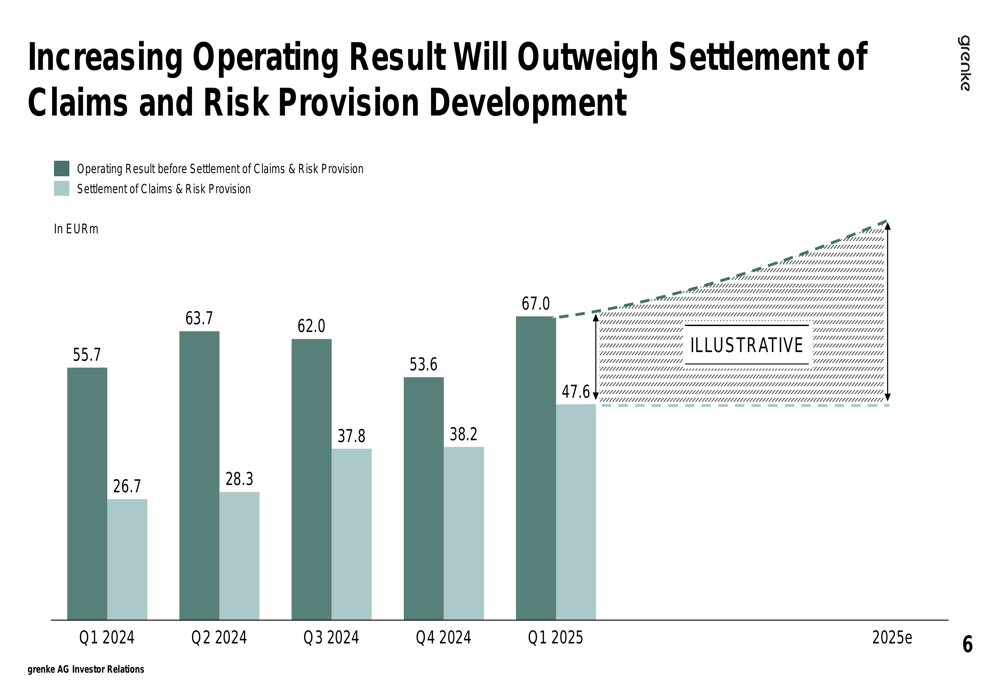

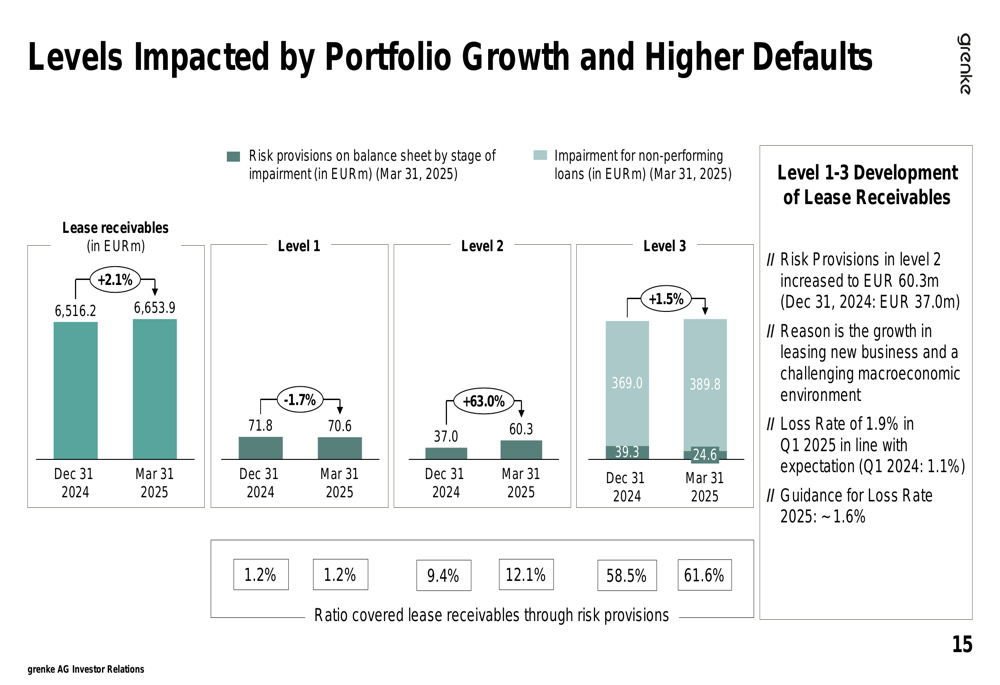

This increase in risk provisions represents a concerning trend, as illustrated in the following chart comparing operating results before settlement of claims and the actual settlement amounts:

The company’s cost income ratio improvement was driven by higher income generation and stabilized costs, as detailed in this breakdown:

The rise in risk provisions was attributed to both portfolio growth and higher defaults in a challenging macroeconomic environment. The loss rate increased to 1.9% in Q1 2025 from 1.1% in Q1 2024, though management indicated this was in line with expectations:

Strategic Initiatives

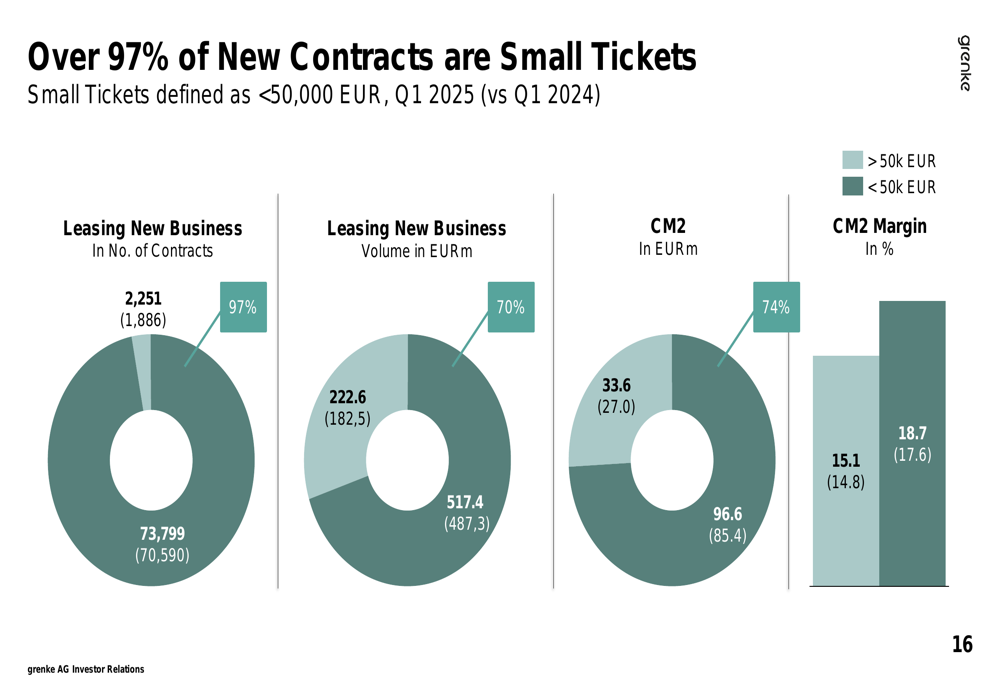

Grenke continues to focus on its core small-ticket leasing business, with contracts under EUR 50,000 representing 97% of total contracts and 70% of new business volume. This segment also generates 74% of the company’s CM2, demonstrating the effectiveness of this strategic focus:

To foster international growth, Grenke announced a strategic partnership with Intesa Sanpaolo (OTC:ISNPY), Italy’s largest bank. The collaboration between "grenke Locazione" and "INTESA SANPAOLO RENT FORYOU" is expected to contribute to new business and positively impact the P&L starting in 2026.

Forward-Looking Statements

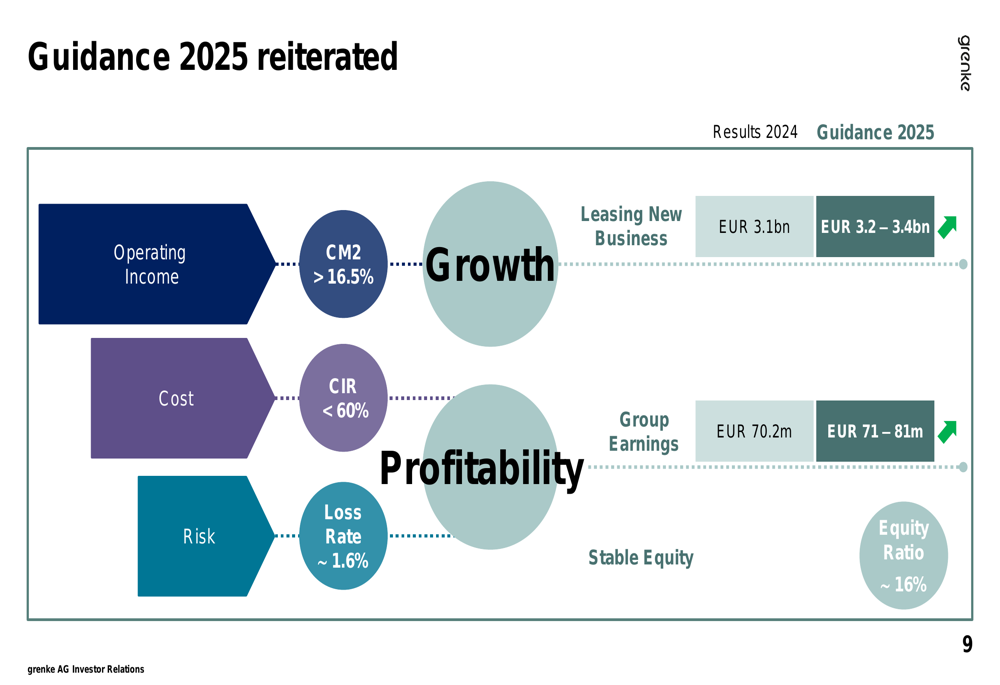

Despite the Q1 earnings decline, Grenke reiterated its full-year 2025 guidance, projecting:

- Leasing new business between EUR 3.2-3.4 billion (up from EUR 3.1 billion in 2024)

- Group earnings of EUR 71-81 million (up from EUR 70.2 million in 2024)

- CM2 margin above 16.5%

- CIR below 60%

- Loss rate around 1.6%

- Equity ratio of approximately 16%

The following chart illustrates the company’s 2025 guidance compared to 2024 results:

Management’s decision to maintain its guidance suggests confidence that the elevated risk provisions in Q1 will normalize throughout the year, allowing for improved profitability in subsequent quarters. However, investors may approach these projections with caution given the significant earnings decline in the first quarter and the challenging macroeconomic environment that contributed to higher default rates.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.