Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

Griffon Corporation (NYSE:GFF) released its first-quarter fiscal 2025 investor presentation on May 8, 2025, highlighting the company’s financial performance and strategic initiatives. The presentation comes after Griffon reported better-than-expected earnings with EPS of $1.39, exceeding analyst forecasts of $1.17, while revenue came in slightly below expectations at $632 million.

The building products and consumer goods manufacturer has seen its stock price fluctuate recently, closing at $67.90 on May 7, down 2.53% for the day, though the company’s shares had previously surged 8.72% following its earnings announcement. Despite some recent volatility, Griffon’s strategic positioning in repair and remodel markets continues to support its financial performance.

Executive Summary

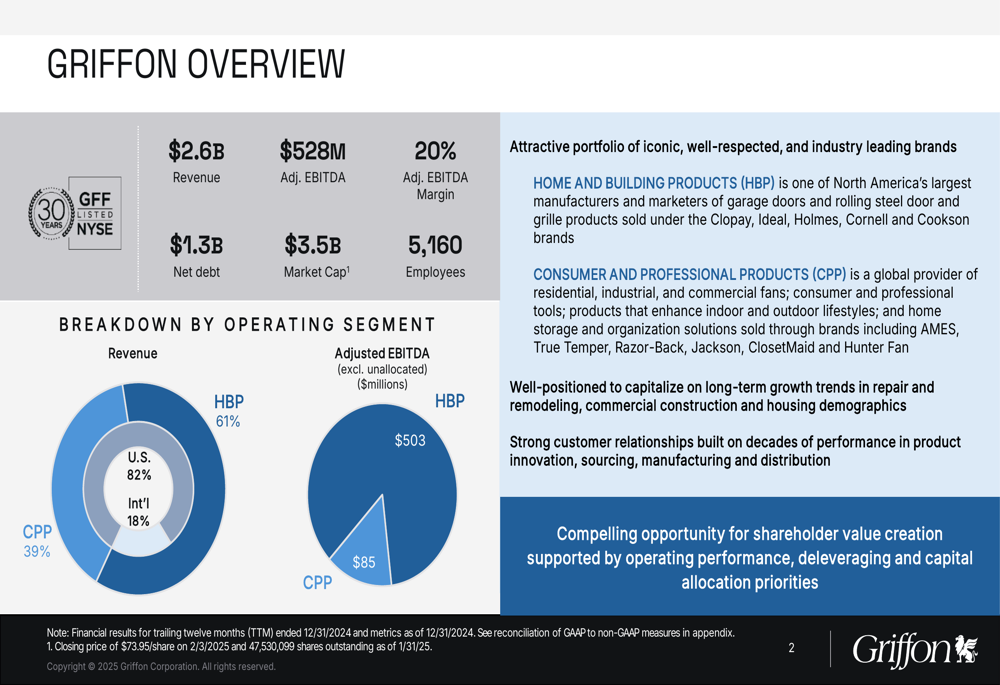

Griffon’s presentation emphasizes the company’s transformation into a more focused and profitable enterprise through strategic portfolio reshaping. With $2.6 billion in revenue and $528 million in adjusted EBITDA (representing a 20% margin), Griffon operates through two main segments: Home and Building Products (HBP), which contributes 61% of revenue, and Consumer and Professional Products (CPP), accounting for 39%.

As shown in the following comprehensive overview of the company’s structure and key metrics:

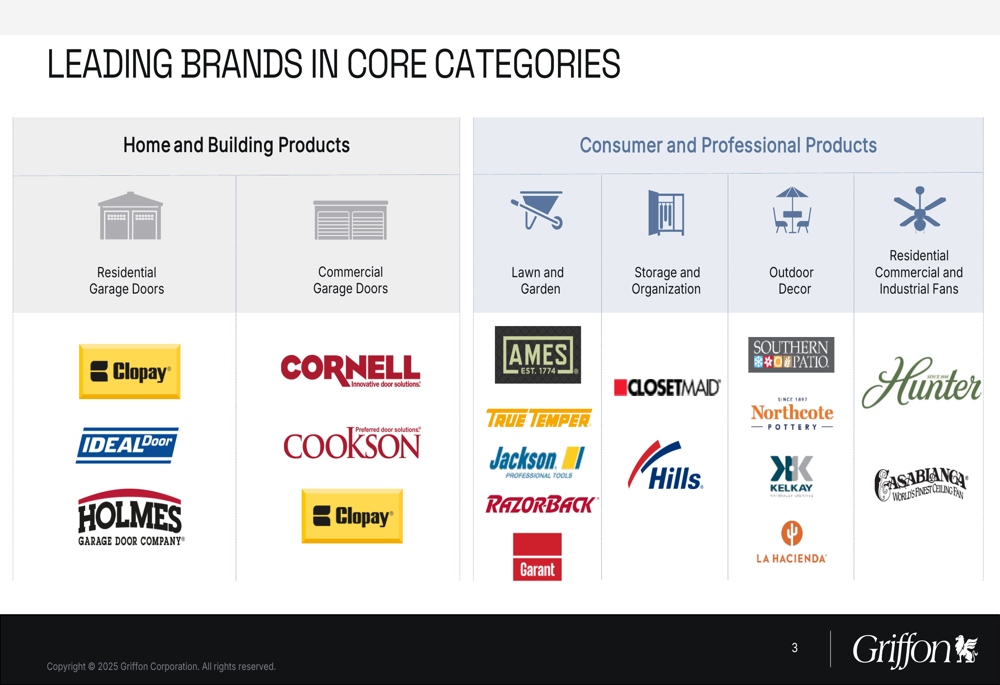

The company’s brand portfolio spans residential and commercial garage doors under the Clopay, Ideal, Holmes, Cornell, and Cookson brands, as well as consumer products including tools, storage solutions, and fans through brands such as AMES, True Temper, ClosetMaid, and Hunter Fan.

The presentation showcases Griffon’s impressive collection of market-leading brands across its core categories:

Detailed Financial Analysis

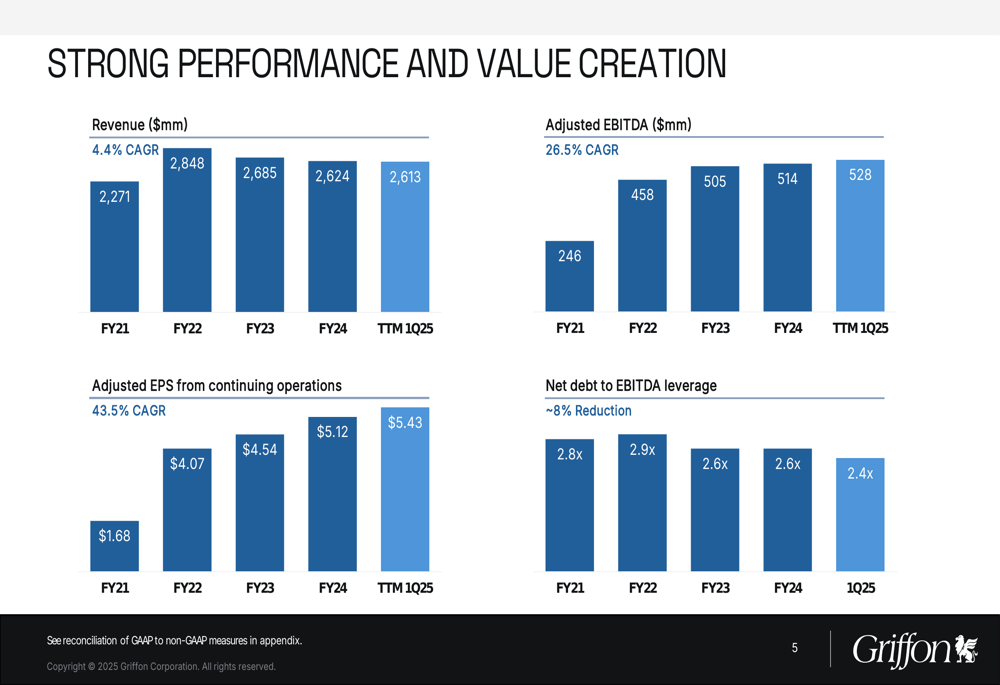

Griffon’s financial performance shows strong margin expansion and earnings growth despite relatively flat revenue. From fiscal 2021 through the trailing twelve months ended Q1 2025, the company achieved:

- Revenue CAGR of 4.4%, reaching $2.61 billion

- Adjusted EBITDA CAGR of 26.5%, growing to $528 million

- Adjusted EPS CAGR of 43.5%, increasing from $1.68 to $5.43

- Net debt to EBITDA leverage reduction from 2.8x to 2.4x

These trends are clearly illustrated in the following performance chart:

The company’s Q1 FY2025 earnings report aligns with these trends, showing an 11% year-over-year increase in adjusted EBITDA to $145 million and a significant improvement in gross margin to 41.8%, up 3.2 percentage points. This margin expansion has been a key driver of Griffon’s ability to deliver EPS growth despite modest revenue performance.

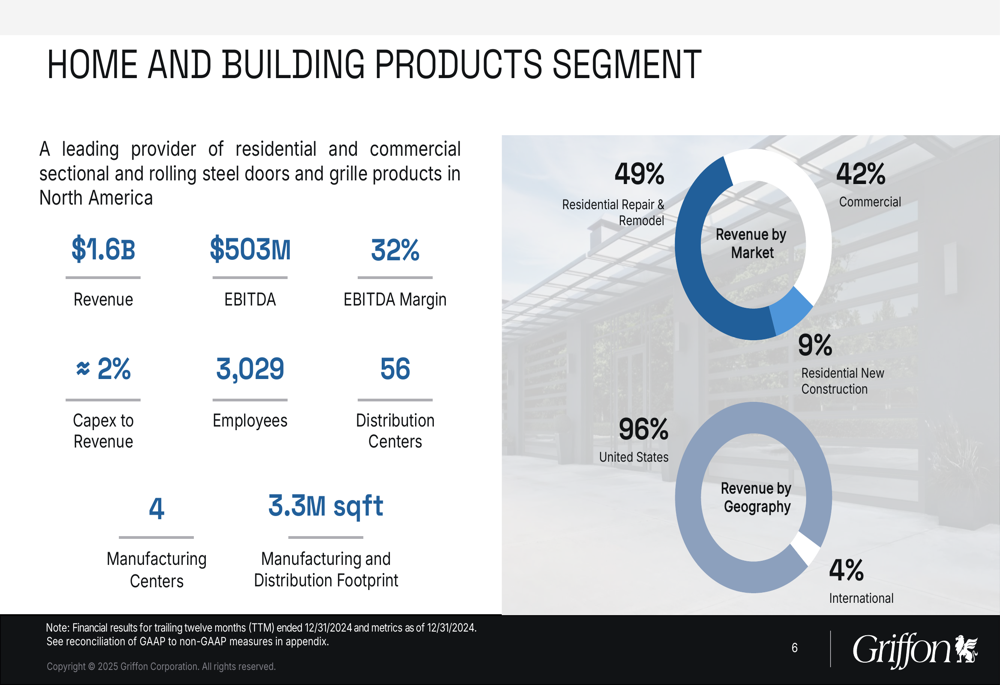

The Home and Building Products segment continues to be the primary profit driver, with an impressive EBITDA margin of 32% on $1.6 billion in revenue. This segment derives 49% of its revenue from residential repair and remodel, 42% from commercial, and 9% from residential new construction, with 96% of sales coming from the United States.

The following slide details the HBP segment’s performance metrics:

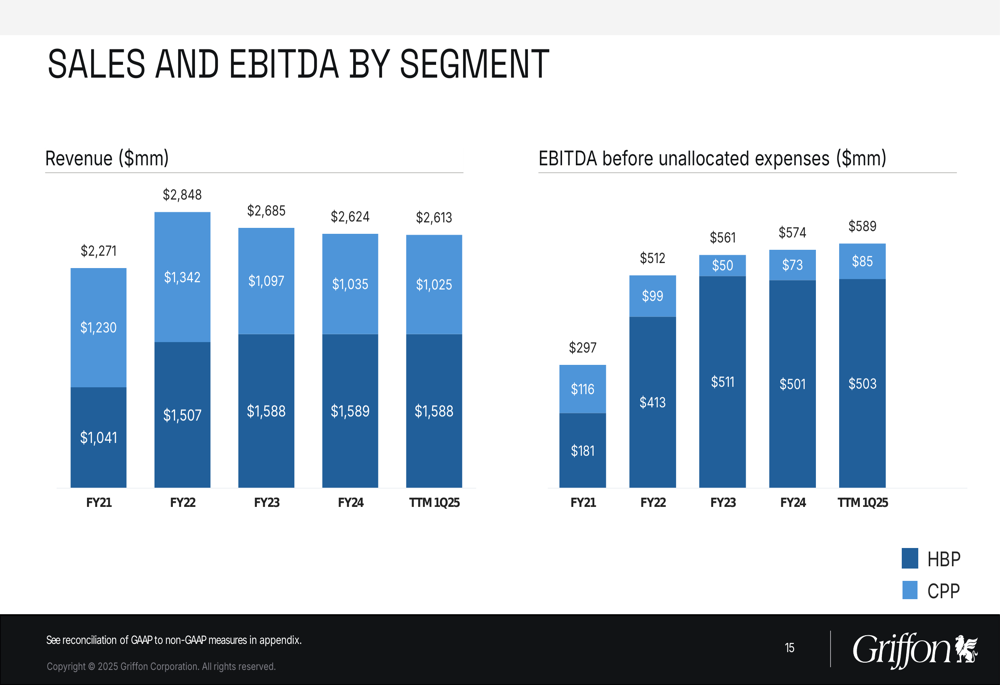

The Consumer and Professional Products segment, while generating $1.0 billion in revenue, operates at a lower EBITDA margin of 8.3%. However, management is targeting margin improvement in this segment, with FY2025 guidance of 9%+ compared to 7.0% in FY2024. CPP has a more diverse geographic footprint, with 60% of revenue from the United States and 33% from international markets excluding North America.

The segment breakdown of sales and EBITDA over time demonstrates the growing contribution of the higher-margin HBP segment:

Strategic Initiatives

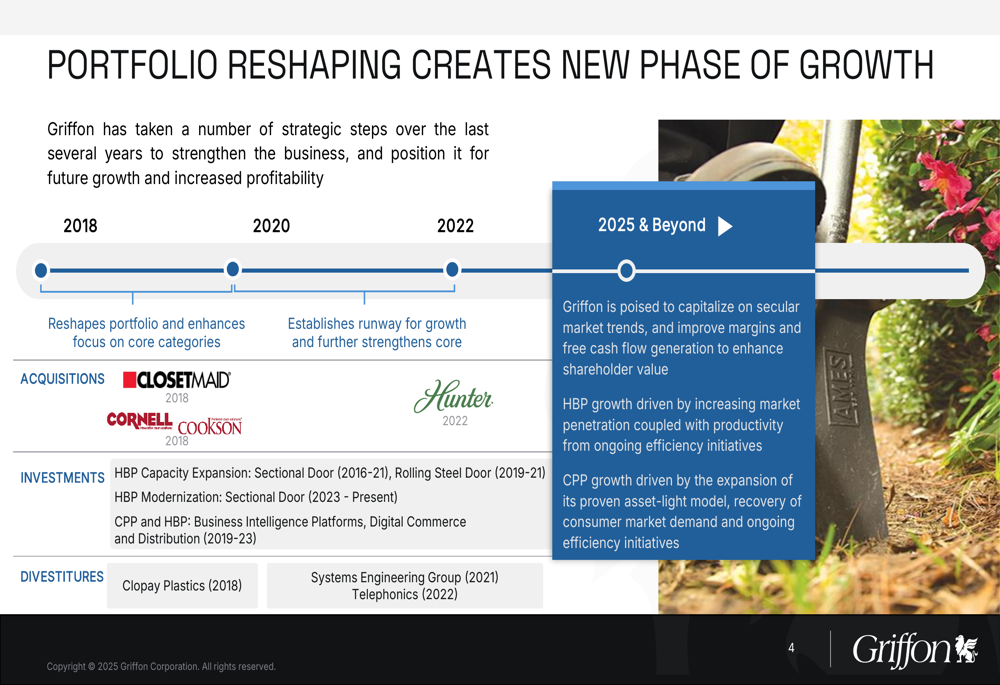

Griffon’s presentation outlines how the company has strategically reshaped its portfolio over the past several years to focus on its core categories. Key milestones include the acquisitions of ClosetMaid, Cornell, and Cookson in 2018, and Hunter in 2022, along with divestitures of non-core businesses.

The company’s strategic evolution is illustrated in this timeline:

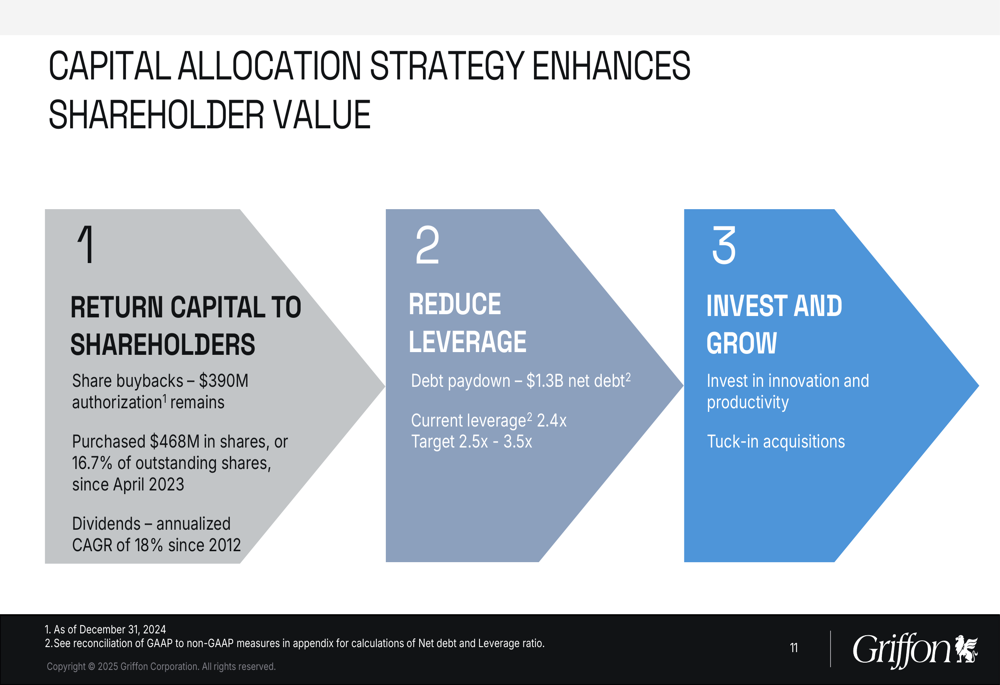

Looking ahead, Griffon’s capital allocation strategy focuses on three priorities: returning capital to shareholders, reducing leverage, and investing for growth. The company has $390 million remaining in its share buyback authorization and has purchased $468 million in shares (16.7% of outstanding shares) since April 2023. Griffon has also grown its dividend at an annualized CAGR of 18% since 2012.

The following slide outlines the company’s approach to capital allocation:

During the recent earnings call, CFO Brian Harris emphasized the company’s view that its stock remains "opportunistically attractive," suggesting continued share repurchases. Management also indicated a preference for stock buybacks over debt reduction, reflecting confidence in the company’s financial position and focus on shareholder returns.

Forward-Looking Statements

Griffon’s presentation highlights several macroeconomic trends expected to drive product demand, including elevated repair and remodel activity, growing commercial construction demand, aging U.S. housing stock, increasing household formation from Millennial and Gen Z populations, and continued popularity of outdoor living.

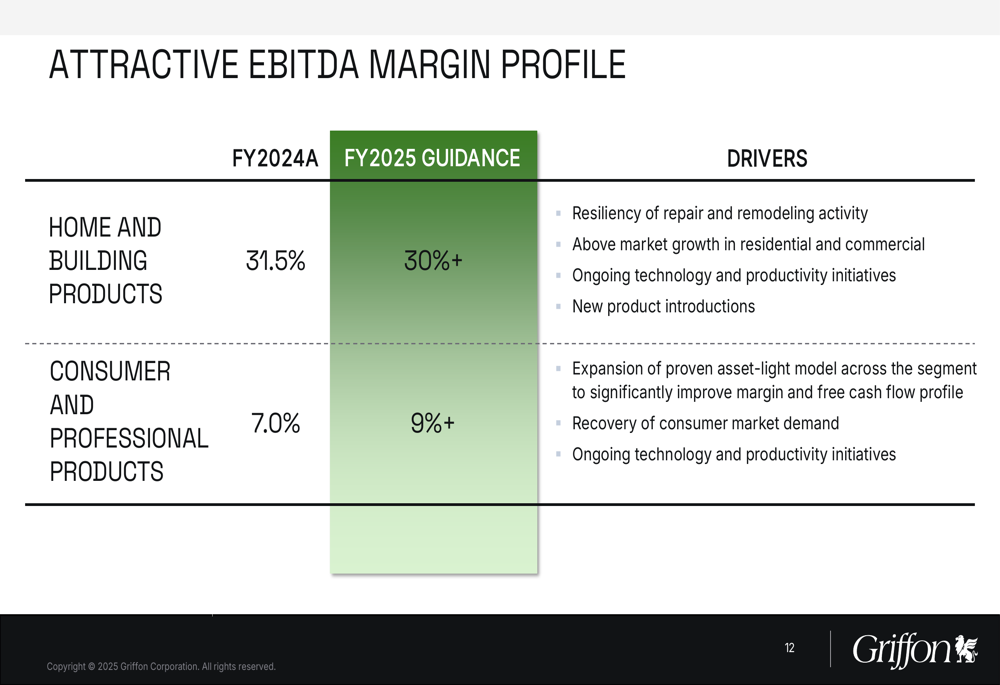

For fiscal 2025, Griffon maintained its guidance of $2.6 billion in revenue and segment adjusted EBITDA between $575 million and $600 million. The company expects the Home and Building Products segment to maintain EBITDA margins above 30%, while the Consumer and Professional Products segment is projected to improve to 9%+ from 7.0% in FY2024.

The margin guidance for both segments is presented in the following chart:

Management noted during the earnings call that they are monitoring potential tariff impacts but remain confident in meeting financial targets. The company also expects continued growth in the Australian market and projects free cash flow to exceed net income.

CEO Ron Kramer expressed confidence in the company’s outlook, stating, "We’re going to execute our business plan and continue to deliver outstanding performance," emphasizing Griffon’s commitment to maintaining its market leadership position. With its strategic focus on high-margin segments, capital allocation discipline, and exposure to resilient repair and remodel markets, Griffon appears well-positioned to continue its trajectory of margin expansion and earnings growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.